State Pension potential shortfall warning

Discussion

Due to the little known new rules introduced in 2016, lots of people who retire before state pension age, and DONT continue to pay their NI contributions, MAY see a shortfall in their state pension.

However, the only way to pay NI is from a wage, you can't pay it from a private pension (though you can claim to be self employed and pay a voluntary amount each year). Previously you just needed to have paid the minimum number of years NI contributions (35ys) but thats now changed. Even if you've paid NI for 35yrs, if you don't keep paying NI after you've retired and right upto applying for your state pension, you may receive a smaller state pension than the maximum you could be expecting to receive.

The snag is, nobody makes you aware of this, even the gov.uk state pension forecast website doesn't tell you, instead it says you will receive the higher mount and that you won't need to pay any extra NI.

The good news is that you can pay buy back the missing years of NI. Some folk I know are expecting a shortfall in theiry state pension of £20/week and to negate this they can buy back the missing years of NI at around £780 for each missing year. So, retire at age 55 and with the state pension age of 67 that means having to buy back 12yrs of NI.

So, if you are planning to retire before state pension age, telephone the pension helpline on gov.uk and make checks for your own personal circumstances.

However, the only way to pay NI is from a wage, you can't pay it from a private pension (though you can claim to be self employed and pay a voluntary amount each year). Previously you just needed to have paid the minimum number of years NI contributions (35ys) but thats now changed. Even if you've paid NI for 35yrs, if you don't keep paying NI after you've retired and right upto applying for your state pension, you may receive a smaller state pension than the maximum you could be expecting to receive.

The snag is, nobody makes you aware of this, even the gov.uk state pension forecast website doesn't tell you, instead it says you will receive the higher mount and that you won't need to pay any extra NI.

The good news is that you can pay buy back the missing years of NI. Some folk I know are expecting a shortfall in theiry state pension of £20/week and to negate this they can buy back the missing years of NI at around £780 for each missing year. So, retire at age 55 and with the state pension age of 67 that means having to buy back 12yrs of NI.

So, if you are planning to retire before state pension age, telephone the pension helpline on gov.uk and make checks for your own personal circumstances.

Wife purchased additional years for when she's only been part time and not earned much, her forecast now shows full state pension entitlements and she's fully retiring early next year at 56, there is nothing to show contrary on the gov website around this topic. It definitely shows a guaranteed pension and years contributed.

There were changes in 2016 but the core ability to buy back years doesn't seem to have changed at all.

The changes in 2016 just seem to have doubled the number of pages you need to read to work out wtf is going on.

Online check still says for me I'll be getting the Full State Pension as I've already paid the 35 yrs min required.

And it doesn't matter what I do from now on that wont change - Which I've always felt is slightly unfair.

If you continue to pay into the NI system you should get some benefit for that when you eventually retire - but that's a different issue

The changes in 2016 just seem to have doubled the number of pages you need to read to work out wtf is going on.

Online check still says for me I'll be getting the Full State Pension as I've already paid the 35 yrs min required.

And it doesn't matter what I do from now on that wont change - Which I've always felt is slightly unfair.

If you continue to pay into the NI system you should get some benefit for that when you eventually retire - but that's a different issue

I checked my State Pension entitlement recently.

You need to do two things to check your State Pension entitlement;

1- check your National Insurance record here https://www.gov.uk/check-national-insurance-record

you will need to sign into your Gov Gateway, it will show how many years 'full' NI contributions you

have made

2- check here, signing in with Gov Gateway https://www.gov.uk/check-state-pension

where it will show the forecast for the max sum of state pension when you retire, and their estimate as

to how much you will get in state pension

However, if you previously 'COPEed out' someSERPS NI contributions into your private pension scheme, then although you may have a 'full' 35 years NI record, it will not be 35 full years worth towards pension contributions, and you could end up like I did, with 35 years NI contributions, but still 7 years short of max State Pension entitlement.

I am currently SE and pay Class2 NI contributions at £2.95pw(going up soon), each subsequent full year of NI contributions I pay (I need 7) will mean an additional £4.81 of state pension per week for me.

So I'll technically end up needing 42 years of NI contributions to receive a full state pension.

You need to do two things to check your State Pension entitlement;

1- check your National Insurance record here https://www.gov.uk/check-national-insurance-record

you will need to sign into your Gov Gateway, it will show how many years 'full' NI contributions you

have made

2- check here, signing in with Gov Gateway https://www.gov.uk/check-state-pension

where it will show the forecast for the max sum of state pension when you retire, and their estimate as

to how much you will get in state pension

However, if you previously 'COPEed out' some

I am currently SE and pay Class2 NI contributions at £2.95pw(going up soon), each subsequent full year of NI contributions I pay (I need 7) will mean an additional £4.81 of state pension per week for me.

So I'll technically end up needing 42 years of NI contributions to receive a full state pension.

Edited by the tribester on Thursday 2nd January 11:24

anonymous said:

[redacted]

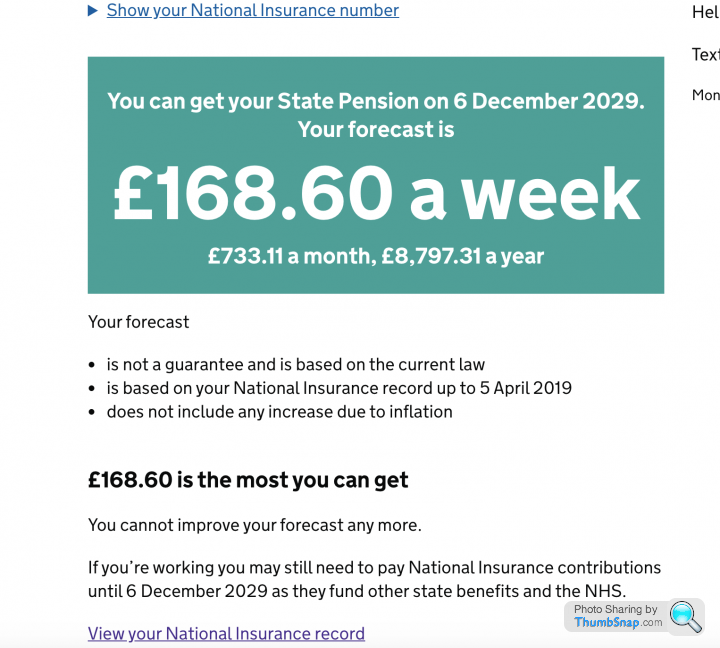

OK, now I get it. I contracted out from 1987 to 2012, so was surprised that my state pension forecast showed £168.60. This explains why.It did say something about not being entitled to a COPE additional amount of £72/week, which I assume is the bit I missed out on by contracting out. So £3744 a year lost. But seeing as my contracted out pension pot is now worth circa £120K, I'm still miles ahead of the game. I'd have to live for 32 years beyond 67, so 99 to be worse off. And that doesn't allow for further growth on my £120K pot. And it seems to grow by about 5% a year give or take.

LeadFarmer said:

Due to the little known new rules introduced in 2016, lots of people who retire before state pension age, and DONT continue to pay their NI contributions, MAY see a shortfall in their state pension.

However, the only way to pay NI is from a wage, you can't pay it from a private pension (though you can claim to be self employed and pay a voluntary amount each year). Previously you just needed to have paid the minimum number of years NI contributions (35ys) but thats now changed. Even if you've paid NI for 35yrs, if you don't keep paying NI after you've retired and right upto applying for your state pension, you may receive a smaller state pension than the maximum you could be expecting to receive.

The snag is, nobody makes you aware of this, even the gov.uk state pension forecast website doesn't tell you, instead it says you will receive the higher mount and that you won't need to pay any extra NI.

The good news is that you can pay buy back the missing years of NI. Some folk I know are expecting a shortfall in theiry state pension of £20/week and to negate this they can buy back the missing years of NI at around £780 for each missing year. So, retire at age 55 and with the state pension age of 67 that means having to buy back 12yrs of NI.

So, if you are planning to retire before state pension age, telephone the pension helpline on gov.uk and make checks for your own personal circumstances.

I'd also like to see a source one on this. However, the only way to pay NI is from a wage, you can't pay it from a private pension (though you can claim to be self employed and pay a voluntary amount each year). Previously you just needed to have paid the minimum number of years NI contributions (35ys) but thats now changed. Even if you've paid NI for 35yrs, if you don't keep paying NI after you've retired and right upto applying for your state pension, you may receive a smaller state pension than the maximum you could be expecting to receive.

The snag is, nobody makes you aware of this, even the gov.uk state pension forecast website doesn't tell you, instead it says you will receive the higher mount and that you won't need to pay any extra NI.

The good news is that you can pay buy back the missing years of NI. Some folk I know are expecting a shortfall in theiry state pension of £20/week and to negate this they can buy back the missing years of NI at around £780 for each missing year. So, retire at age 55 and with the state pension age of 67 that means having to buy back 12yrs of NI.

So, if you are planning to retire before state pension age, telephone the pension helpline on gov.uk and make checks for your own personal circumstances.

I 'retired' at 54 - living on savings etc until pensions etc kick in. I have more than 35 years contributions and haven't contributed in the 3 years since I 'retired'. On line is showing full £168 with no extra contributions required.

I rang HMRC and they said I didn't need to continue to pay,

i4got said:

I'd also like to see a source one on this.

I 'retired' at 54 - living on savings etc until pensions etc kick in. I have more than 35 years contributions and haven't contributed in the 3 years since I 'retired'. On line is showing full £168 with no extra contributions required.

I rang HMRC and they said I didn't need to continue to pay,

Does your state pension estimate/statement mention any amount for COPE?I 'retired' at 54 - living on savings etc until pensions etc kick in. I have more than 35 years contributions and haven't contributed in the 3 years since I 'retired'. On line is showing full £168 with no extra contributions required.

I rang HMRC and they said I didn't need to continue to pay,

If not, and they say you'll get the full £168 at today's prices, fair enough.

However, this means you've never been part of a occupational pension scheme for which you were opted out of SERPS and as a result paid reduced NI contributions from 1988 to 2016.

croyde said:

I contracted out at some point, no idea why or who too, but according to the records I did.

I presume when I was young and daft. I wouldn't even know where to begin in order to find out what happened

Looks to me that you were in an employer sponsored pension plan for its employees, and the employer took the financial decision to contract out all the plan members. If so, members did not have the option to be contracted out of SERPS or not: the decision was for the employer. So, you paid less NICs, have a reduced State SERPS pension the latter being replaced (or more likely bettered) by your pension from the employer. Nothing lost, likely something gained.I presume when I was young and daft. I wouldn't even know where to begin in order to find out what happened

R.

uknick said:

Does your state pension estimate/statement mention any amount for COPE?

If not, and they say you'll get the full £168 at today's prices, fair enough.

However, this means you've never been part of a occupational pension scheme for which you were opted out of SERPS and as a result paid reduced NI contributions from 1988 to 2016.

Nothing about COPE.If not, and they say you'll get the full £168 at today's prices, fair enough.

However, this means you've never been part of a occupational pension scheme for which you were opted out of SERPS and as a result paid reduced NI contributions from 1988 to 2016.

croyde said:

If I can find the money. I did a couple or three full time jobs back in the early 90s.

All three companies are not around today.

Plus one job was just over a year and the other two were maybe 6 months.

Looks like money lost.

There's a pension tracing service may be worth a go.All three companies are not around today.

Plus one job was just over a year and the other two were maybe 6 months.

Looks like money lost.

Edited by croyde on Thursday 2nd January 13:00

https://www.gov.uk/find-pension-contact-details

Gassing Station | Finance | Top of Page | What's New | My Stuff