Understanding how to draw down tax free out of pension

Discussion

nickfrog said:

You shouldn't be far off £1 million by the time you're 70 on that basis.

Also, be mindful the TFC £18k drawdown will slowly nibble away the LTA too (currently @ £1.055 mio with annual limit increased by inflation).Fag packet calculation £18,000 x 15 years (assume you drawdown between age 55-70) = £270k utilised against LTA .

Add the potential £1.0 mio DC pot (more if market return exceeds your assumed 4.5% growth), and you could have a healthy DC pot which HMRC will be taking a considerable interest when you hit 75 for the final BCE. First world problem I know, but worth keeping an eye on the LTA excess tax charge (or just spend more of your pension to prevent this situation ever arising

)

) Is there any reason why someone who's starting to use their pension pot for drawdown would *not* take the maximum they can in tax free cash and invest this elsewhere, and simultaneously start the drawdown process against the balance, at a rate which is sensible in the context of their life expectancy?

My thinking is that the 25% tax free cash (for pots within the LTA) which is currently available could be withdrawn, and taking advantage of it now has no disadvantage.

Is that thinking correct or am I missing a trick?

My thinking is that the 25% tax free cash (for pots within the LTA) which is currently available could be withdrawn, and taking advantage of it now has no disadvantage.

Is that thinking correct or am I missing a trick?

I had thought (but may well be wrong!) that the advantage was that 25% of the growth in the pot that wasn't moved to drawdown was then also tax free.

So - pot £500k, age 55, draw £125k tax free, do nothing for 20 years, assume growth of 50% have larger pot (£562.5k) which is all then potentially taxable.

Pot £500k, draw 25k tax free, do nothing for 25 years, assume growth of 50%, larger pot (£675k) of which I think 25% of £562.5 (balance moved to drawdown when first 25k taken) is taxable so £140k (approx).

I appreciate one can replicate the tax free growth in an ISA etc but otherwise there would seem to be benefits to waiting.

However, there are proper experts on here so they should confirm and check my maths!

So - pot £500k, age 55, draw £125k tax free, do nothing for 20 years, assume growth of 50% have larger pot (£562.5k) which is all then potentially taxable.

Pot £500k, draw 25k tax free, do nothing for 25 years, assume growth of 50%, larger pot (£675k) of which I think 25% of £562.5 (balance moved to drawdown when first 25k taken) is taxable so £140k (approx).

I appreciate one can replicate the tax free growth in an ISA etc but otherwise there would seem to be benefits to waiting.

However, there are proper experts on here so they should confirm and check my maths!

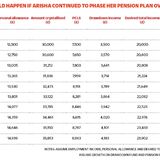

Been relevant to this thread, I attach an use case (good old Google!) showing Arisha with a part-time income + phased drawdown income from her DC pension pot to obtain an annual income of £20,000 without paying any income tax.

Table is located from the link below:

https://www.moneymarketing.co.uk/analysis/rachel-v...

Simple but clear use case as it highlights how to "stretch" your pension pot using phased drawdown:

Table is located from the link below:

https://www.moneymarketing.co.uk/analysis/rachel-v...

Simple but clear use case as it highlights how to "stretch" your pension pot using phased drawdown:

- combine use of the 25% tax free cash (referred to as PCLS in the use case) & personal allowance to maximise her annual income

- how phased drawdown could generates additional (25%) tax free entitlement on the uncrystallised part of your pension (Year 19/20, the uncrystallised pot is £270,000 which grows by 3% to £278,100 then she crystallise a further £30,600 in Year 20/21 to use the 25% tax free cash £7,650. New uncrystallised pot is £247,500 which grows by 3% again...and so on)

Edited by chip* on Saturday 25th January 10:58

Thanks Chip. Very useful. From earlier in this thread it looks like some pension providers offer the facility of setting up the phasing, like Aviva. I wonder if that attracts any additional fees on top of the "normal" fees.

We have half with Aviva and half with Aegon so this could make the difference between staying with one or move to the other.

We have half with Aviva and half with Aegon so this could make the difference between staying with one or move to the other.

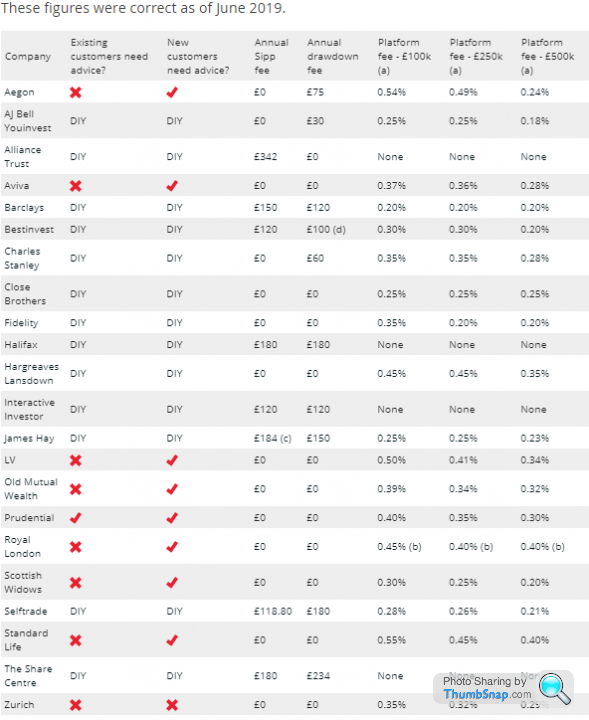

Yep, it's another minefield come drawdown time as fees can differ (some fixed and some a percentage of fund) across the SIPP platform provider. Attached is a comparison table compiled last year by Which which highlights the variation between the main players including your current providers Aegon and Aviva. It appears they are both almost fee free, but this is offset by the toppy platform fee.

.

Per table above, ii for £240 on paper looks cheap compared to HL @ 0.45% for a £250k pot, but then AJ bell is cheaper for a smaller £50k pot. There's no obvious clear winner as every individual circumstance will differ plus other factors should be considered too e.g. decent customer service, other trading cost, financially stable company (I would avoid small tinpot company even if they are the cheapest) investment fund choice, and not forgetting fund performance too..etc

I retired at 47 so have a number of years before drawdown, but it's definitely an area that warrants further investigation as switching platform could have significant savings.

.

Per table above, ii for £240 on paper looks cheap compared to HL @ 0.45% for a £250k pot, but then AJ bell is cheaper for a smaller £50k pot. There's no obvious clear winner as every individual circumstance will differ plus other factors should be considered too e.g. decent customer service, other trading cost, financially stable company (I would avoid small tinpot company even if they are the cheapest) investment fund choice, and not forgetting fund performance too..etc

I retired at 47 so have a number of years before drawdown, but it's definitely an area that warrants further investigation as switching platform could have significant savings.

Edited by chip* on Sunday 26th January 11:12

Once again thank you so much chip, that's invaluable. I am not in drawdown mode yet and I am paying 0.55% up to £30k, 0.3% up to £200k and 0% beyond that with Aegon. It is my workplace thing so maybe they negociated a better deal, hence the difference.

Or do the platform fees come on top of that once I start drawing down? I hope not and that the only added cost in drawdown mode is the £75 pa fee. Not sure, would you by any chance know?

and that the only added cost in drawdown mode is the £75 pa fee. Not sure, would you by any chance know?

Or do the platform fees come on top of that once I start drawing down? I hope not

and that the only added cost in drawdown mode is the £75 pa fee. Not sure, would you by any chance know? nickfrog said:

Once again thank you so much chip, that's invaluable. I am not in drawdown mode yet and I am paying 0.55% up to £30k, 0.3% up to £200k and 0% beyond that with Aegon. It is my workplace thing so maybe they negociated a better deal, hence the difference.

Or do the platform fees come on top of that once I start drawing down? I hope not and that the only added cost in drawdown mode is the £75 pa fee. Not sure, would you by any chance know?

Platform fees are only a small slice of the overall costs. Fund management fees and adviser fees come on top of this.Or do the platform fees come on top of that once I start drawing down? I hope not

and that the only added cost in drawdown mode is the £75 pa fee. Not sure, would you by any chance know? Forgive me, but would you mind saying who is providing the drawdown for £75 a year?

JulianPH said:

Platform fees are only a small slice of the overall costs. Fund management fees and adviser fees come on top of this.

Forgive me, but would you mind saying who is providing the drawdown for £75 a year?

Aegon, first on the table. Are you saying that platform fees only kick in when you start drawing down? The fees I have described are the only ones I am paying AFAIK. Forgive me, but would you mind saying who is providing the drawdown for £75 a year?

nickfrog said:

JulianPH said:

Platform fees are only a small slice of the overall costs. Fund management fees and adviser fees come on top of this.

Forgive me, but would you mind saying who is providing the drawdown for £75 a year?

Aegon, first on the table. Are you saying that platform fees only kick in when you start drawing down? The fees I have described are the only ones I am paying AFAIK. Forgive me, but would you mind saying who is providing the drawdown for £75 a year?

I am guessing you might be using Cofunds (now part of Aegon). This is not bad pricing, to be honest.

JulianPH said:

No, I am saying that (if you use one) platform fees are payable at all times, but are only part of your overall fees. They frequently increase during drawdown, but not always (if they were expensive enough to start with).

I am guessing you might be using Cofunds (now part of Aegon). This is not bad pricing, to be honest.

I have no other fees though. But I will double check. So if the only additional cost is the £75 pa once I go into drawdown then I'm laughing. I am guessing you might be using Cofunds (now part of Aegon). This is not bad pricing, to be honest.

Not with Cofunds.

I thought I would revive this thread which I know has helped others.

I have accepted that it will make sense to sell off our BTL property when I retire at 55, not only because I reckon the CGT exposure will start being unreasonable by then (unless the property market collapses) but also because the rental yield eats up into my tax free allowance.

I therefore have two questions on the assumption that I will have no other taxable income than our pension:

- is it right that we can pay in £2,880 each into our pension and that HRMC still tops up to £3,600 even if we pay £0 income tax ?

- does it make sense to invest the property sales proceeds via ISA at a rate of £20k a year each ? Or should we / can we pay it into our pension without HMRC's top up ? I can see that ISA savings won't trigger any tax on exit either as an income or a capital growth.

Thanks for any pointers.

Nick

I have accepted that it will make sense to sell off our BTL property when I retire at 55, not only because I reckon the CGT exposure will start being unreasonable by then (unless the property market collapses) but also because the rental yield eats up into my tax free allowance.

I therefore have two questions on the assumption that I will have no other taxable income than our pension:

- is it right that we can pay in £2,880 each into our pension and that HRMC still tops up to £3,600 even if we pay £0 income tax ?

- does it make sense to invest the property sales proceeds via ISA at a rate of £20k a year each ? Or should we / can we pay it into our pension without HMRC's top up ? I can see that ISA savings won't trigger any tax on exit either as an income or a capital growth.

Thanks for any pointers.

Nick

Couple of probably ill informed comments from a 67 year old dummy

Once you start drawing the pension you can only add up to £4000/annum

When you take money from your fund you'll get it gross now and HMRC will steal a bit later (or guess what you are gong to take and provide a revised tax code). Last year the provider took money out to cover the 20%.tax on the balance after the 25% tax free bit.

And be prepared for a few puzzling phone calls from you to HMRC while you try to understand why the tax code has reduced by the amount of your state pension sum. I couldn't get my head around that.

Once you start drawing the pension you can only add up to £4000/annum

When you take money from your fund you'll get it gross now and HMRC will steal a bit later (or guess what you are gong to take and provide a revised tax code). Last year the provider took money out to cover the 20%.tax on the balance after the 25% tax free bit.

And be prepared for a few puzzling phone calls from you to HMRC while you try to understand why the tax code has reduced by the amount of your state pension sum. I couldn't get my head around that.

nickfrog said:

- is it right that we can pay in £2,880 each into our pension and that HRMC still tops up to £3,600 even if we pay £0 income tax?

Yes, that's correct. Note the limit once you go into drawdown though.nickfrog said:

- does it make sense to invest the property sales proceeds via ISA at a rate of £20k a year each ? Or should we / can we pay it into our pension without HMRC's top up ? I can see that ISA savings won't trigger any tax on exit either as an income or a capital growth.

It's surely not worthwhile paying extra into a pension if you're not getting any tax relief going in & it's subject to tax (possibly) when you withdraw any money. The main advantage of a pension is the tax relief on the contributions whereas the advantage of ISAs is that withdrawals (& any gains) are not subject to income tax.Skyedriver said:

Couple of probably ill informed comments from a 67 year old dummy

Once you start drawing the pension you can only add up to £4000/annum

When you take money from your fund you'll get it gross now and HMRC will steal a bit later (or guess what you are gong to take and provide a revised tax code). Last year the provider took money out to cover the 20%.tax on the balance after the 25% tax free bit.

And be prepared for a few puzzling phone calls from you to HMRC while you try to understand why the tax code has reduced by the amount of your state pension sum. I couldn't get my head around that.

Cheers. I think I got the £2,880 wrong as this is only if income is less than £3,600/year. I am probably still limited by the recycling rule but even if I don't fall foul of that, the ISA route might be better anyway in my case.Once you start drawing the pension you can only add up to £4000/annum

When you take money from your fund you'll get it gross now and HMRC will steal a bit later (or guess what you are gong to take and provide a revised tax code). Last year the provider took money out to cover the 20%.tax on the balance after the 25% tax free bit.

And be prepared for a few puzzling phone calls from you to HMRC while you try to understand why the tax code has reduced by the amount of your state pension sum. I couldn't get my head around that.

I can see why HMRC would lower your tax code as state pension is taxable I guess.

Mr Pointy said:

nickfrog said:

- is it right that we can pay in £2,880 each into our pension and that HRMC still tops up to £3,600 even if we pay £0 income tax?

Yes, that's correct. Note the limit once you go into drawdown though.Mr Pointy said:

nickfrog said:

- does it make sense to invest the property sales proceeds via ISA at a rate of £20k a year each ? Or should we / can we pay it into our pension without HMRC's top up ? I can see that ISA savings won't trigger any tax on exit either as an income or a capital growth.

It's surely not worthwhile paying extra into a pension if you're not getting any tax relief going in & it's subject to tax (possibly) when you withdraw any money. The main advantage of a pension is the tax relief on the contributions whereas the advantage of ISAs is that withdrawals (& any gains) are not subject to income tax.Gassing Station | Finance | Top of Page | What's New | My Stuff