Now that everyone is renting their music and cars

Discussion

DonkeyApple said:

Yipper said:

Interesting chart.

The rise in UK home ownership coincided almost exactly with Britain's fall in economic wealth.

Britain was Western Europe's no.1 richest economy in 1920 (by a gigantic margin)... In 2000, it was somewhere around 10th.

Britain has used home ownership and rising assets (perceived, real, or on-paper) as a comfort blanket to distract from its economic failure.

We don't dig or make anything the world wants anymore, but at least the fire is warm and Rightmove says my house is worth 6-figs.

That is 100% total bullsThe rise in UK home ownership coincided almost exactly with Britain's fall in economic wealth.

Britain was Western Europe's no.1 richest economy in 1920 (by a gigantic margin)... In 2000, it was somewhere around 10th.

Britain has used home ownership and rising assets (perceived, real, or on-paper) as a comfort blanket to distract from its economic failure.

We don't dig or make anything the world wants anymore, but at least the fire is warm and Rightmove says my house is worth 6-figs.

t. It’s just made up drivel by an absolute mentalist.

t. It’s just made up drivel by an absolute mentalist. Mods should be onto troll accounts like this - does the forum no favours.

Lanker22 said:

I’m 23 and have £30k saved up due to living like a monk for the past few years,

There we go, fair play to you Lanker. It can be done.I'm not saying house prices are not screwed, I'm not saying it is easy. Plainly, the opposite is true.

But I am saying people need to deal with it. Save up like lanker and make sacrifices . If people can't afford to buy a house in the south east, and owning a house is important to them then they should think about moving elsewhere . Not ideal i know and in an ideal world it wouldn't be necessary.

Edited by covmutley on Sunday 18th February 18:54

Tyre Smoke said:

TooMany2cvs said:

Tyre Smoke said:

The rot truly set in under Tony Blair. He told everyone that things would be better, they were worth more than this and utopia for all was around the corner.

He started what I call the L'Oreal generation (Because I'm worth it). A nation of entitled want it now, it's not my fault spineless workshy drains on society.

Apart from the minor detail that it's now 11 years since his 10yr stint as PM finished, does that mean this is unique to the UK...?He started what I call the L'Oreal generation (Because I'm worth it). A nation of entitled want it now, it's not my fault spineless workshy drains on society.

Lanker22 said:

I’m 23 and have £30k saved up due to living like a monk for the past few years, which I’m reasonably happy with.

Certainly not looking forward to a few more years of living like a monk but it’s got to be done I guess.

However the temptation to buy a nice new car/bike on PCP is ever-present. It does feel a bit like I’m wasting a large portion of my youth scrimping and saving for a place. At the end of the day life is about enjoyment.

It is but life is much longer than you think it is when you’re young and the sooner you start planning for the whole of your life rather than the next five minutes then the easier and more enjoyable it is. Certainly not looking forward to a few more years of living like a monk but it’s got to be done I guess.

However the temptation to buy a nice new car/bike on PCP is ever-present. It does feel a bit like I’m wasting a large portion of my youth scrimping and saving for a place. At the end of the day life is about enjoyment.

The key is about finding the right balance and compromise and as you say, it is much harder for people in their 20s today in regards to keeping the money in the bank as there are just so many things to piss it away on and it is so easy to do.

I bought a TVR Griffith in my early 20s but it was done with cash and with money that didn’t impact on building up a flat deposit which was my primary goal. I still spent money on going out but it was never extravagant and never to the detriment of the key objective.

The hardest bit about your 20s is working out the sensible balance that is right for you and allows you to do some of the things you’d like to do but still able to build a suitable deposit at a suitable rate. For some it’s living like a monk and others it’s partying like Sylvester. Someone inbetween is going to be the more usual balance.

DonkeyApple said:

It is but life is much longer than you think it is when you’re young and the sooner you start planning for the whole of your life rather than the next five minutes then the easier and more enjoyable it is.

The key is about finding the right balance and compromise and as you say, it is much harder for people in their 20s today in regards to keeping the money in the bank as there are just so many things to piss it away on and it is so easy to do.

I bought a TVR Griffith in my early 20s but it was done with cash and with money that didn’t impact on building up a flat deposit which was my primary goal. I still spent money on going out but it was never extravagant and never to the detriment of the key objective.

The hardest bit about your 20s is working out the sensible balance that is right for you and allows you to do some of the things you’d like to do but still able to build a suitable deposit at a suitable rate. For some it’s living like a monk and others it’s partying like Sylvester. Someone inbetween is going to be the more usual balance.

Agreed. I fThe key is about finding the right balance and compromise and as you say, it is much harder for people in their 20s today in regards to keeping the money in the bank as there are just so many things to piss it away on and it is so easy to do.

I bought a TVR Griffith in my early 20s but it was done with cash and with money that didn’t impact on building up a flat deposit which was my primary goal. I still spent money on going out but it was never extravagant and never to the detriment of the key objective.

The hardest bit about your 20s is working out the sensible balance that is right for you and allows you to do some of the things you’d like to do but still able to build a suitable deposit at a suitable rate. For some it’s living like a monk and others it’s partying like Sylvester. Someone inbetween is going to be the more usual balance.

ked up my 20s and early 30s and am only now really clawing back the missed opportunities to some degree.DoubleD said:

227bhp said:

DoubleD said:

227bhp said:

DoubleD said:

covmutley said:

All just part of the entitlement snowflake cultIt's where kids grow up being told that they have rights, no winners or losers everything is society's fault and the government needs to solve their problems

This paragraph is such a commonly written thing on PH. Its rather tedious to be honest.Edited by covmutley on Saturday 17th February 18:16

But if you're referring to the other post then no I don't, everybody views things differently. Generations have gone through different times of good and bad, austerity and indulgence. It would be interesting to look at a log of peoples perceptions over the years.

Flibble said:

dazwalsh said:

Purely down to people only having eyes on an overpriced new build as their first house rather than making that first and necessary step of a disgusting damp back to back in the inner city.

Maybe I'm odd, but I have been actively avoiding new builds as I don't like them. The walls are too thin and everything feels like it is a shiny but thin veneer over crap.Porridge GTI said:

Are you at all tempted to forget about or relinquish home ownership and rent your way forwards?

Nipping back to the original post. Private home ownership in the U.K. is actually a relatively recent phenomenon and there are many who believe that it will transpire to be a short blip in the history books. Many will also argue that not owning is a bad thing, the oft touted phrase on PH being that rent is dead money but we are still in a property bull market fuelled by political beliefs. First in the 80s it was about securing Conservative votes by releasing State owned assets at heavily deflated values and then by Labour by removing lending restrictions to create a synthetic wealth boom that again garners votes. I actually believe that despite the many clustre f

ks of the current government they have been the first govt in my lifetime to stabilise the housing market. They’ve ended the insane lending by putting vital restrictions back in place, no more ‘light touch regulation’ of the feckless days and they’ve placed heavy taxes on the corporate and offshore money that was driving prices well beyond domestic affordability and stagnated the top end of the market which has impinged on the ultra wealthy while protecting the normal worker properties from the knock on inflation. They’ve also halted the insanity of the punters BTL market again targeting high risk speculators without hitting the home owner. If I were in my mid 20s again and facing a decision whether to step into the housing ladder I would be very aware that we are at the end of the downward leg of the most recent rate cycle and that debt will be getting more expensive from here in the West. Rates control asset prices but wages control rents, hence why in a period of zero wage inflation (outside of London) we’ve seen stable and low rents, also helped by a large growth in rental supply due to the BTL boom.

So, I would be considering that over the next decade we are not likely to see significant wage inflation so rents are set to remain stable whereas the cost of debt will continue to rise and this will slow asset inflation and indeed, possibly reverse it. At the same time, rate rises are only ever controlled at the start and always over shoot targets to retain economic control and it as it this point of loss of control that you see price falls and buying opportunities.

As a tactic I would probably consider playing both sides and buying a modest property in an area of solid employment purely to rent it out and with no intent of ever living in the property. That would be my exposure to the property market and the right property in the right area with very low leverage will take care of itself. Simultaneously, I would take advantage of low rents to rent my own place to live. This has the huge upside of allowing you to live in a nicer property and area than you could afford to buy in while also leaving you 100% flexible to make the geographic moves that your career may need to take in order to maximise your income potential. My guess is that as rates rise from such a very long period of artificially deflated levels and given just how much debt people hold we are potentially facing a period ahead of very fluid times and owning a modest BTL while renting your own home could transpire to be an incredibly beneficial and prudent way to navigate the next 20 years while leaving all routes and option open to be seized and taken advantage of.

If I was in Russel’s Situation of high salary, big deposit but no desire to yet have my own home but a need to be doing something then I would be using that deposit to buy a low leverage investment asset in a key location with the intent to rent a home when the time was right to move out of the family home. I would never find myself sitting on £60k cash and not using it to better myself.

227bhp said:

You're picking off the low hanging fruit and leaving the bits that don't suit you, but from what you have said you are a prime example of that generation.

Sweeping statements about an ENTIRE generation make no sense. I simply said that house prices have increased massively quicker than income, and that if you were lucky enough to buy your first house 20 years ago like me, you could be pretty thick and do well wheras now you can be pretty smart and still struggle to buy a house. Surely this can't be argued ? You have no idea how I brought up my kids but at least they use far more critical thinking than you and have their head pretty screwed on (the oldest is on £36k at 21 so not too bad so far).48 have only ever rented

Reason being that my career has meant moving countries every few years, often places where tax or law discourages or bans foreign ownership. Plus if only in a place for a few years, transaction costs make no sense to buy

We always try to rent from large companies, or professional landlords Nothing more annoying with dealing with an amateur LL who quibbles when the dryer needs replacing. We normally insist on redecoration/ landscaping at lease renewal time to capture some of the value of the property not being void (normally people will not agree to rent reduction, but will agree to spend 1-2 months rent on making the place nicer)

I’ve invested into property, mostly via shares and a couple of small development projects with family.

We recently bought our first place - an apartment in Australia. On retirement we will use it for 4-5 months a year. Rest of the year in Indonesia

Reason being that my career has meant moving countries every few years, often places where tax or law discourages or bans foreign ownership. Plus if only in a place for a few years, transaction costs make no sense to buy

We always try to rent from large companies, or professional landlords Nothing more annoying with dealing with an amateur LL who quibbles when the dryer needs replacing. We normally insist on redecoration/ landscaping at lease renewal time to capture some of the value of the property not being void (normally people will not agree to rent reduction, but will agree to spend 1-2 months rent on making the place nicer)

I’ve invested into property, mostly via shares and a couple of small development projects with family.

We recently bought our first place - an apartment in Australia. On retirement we will use it for 4-5 months a year. Rest of the year in Indonesia

nickfrog said:

227bhp said:

You're picking off the low hanging fruit and leaving the bits that don't suit you, but from what you have said you are a prime example of that generation.

Sweeping statements about an ENTIRE generation make no sense. I simply said that house prices have increased massively quicker than income, and that if you were lucky enough to buy your first house 20 years ago like me, you could be pretty thick and do well wheras now you can be pretty smart and still struggle to buy a house. Surely this can't be argued ? You have no idea how I brought up my kids but at least they use far more critical thinking than you and have their head pretty screwed on (the oldest is on £36k at 21 so not too bad so far).DoubleD said:

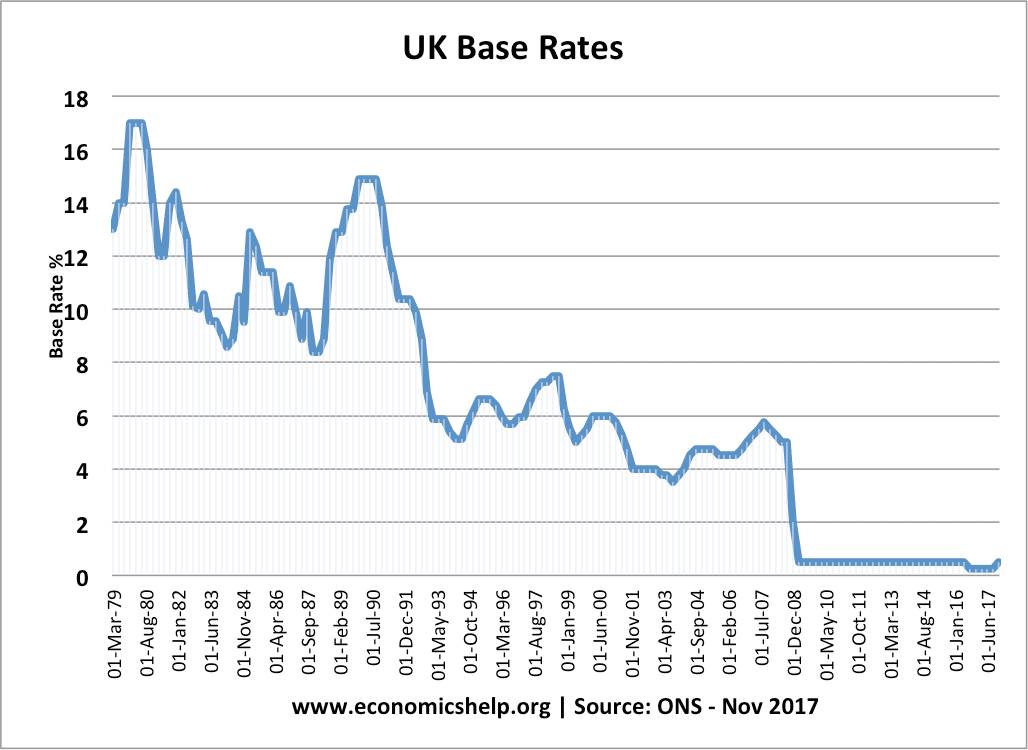

Werent interest rates an awful lot higher back then?

Gawd, yes.

Meanwhile, in another place, somebody is asking about whether they can possibly get a mortgage and become FTB... Household income of damn near £80k, no mention of any savings at all towards a deposit - and recent payday loans and defaults...

In 2009 I was 26 and was living in hoxton with my missus in a rented flat which cost us a grand a month plus bills. Our income was about 65k I think at that point. In 2010-2011 our incomes went up to about 95k joint.

By that point we had saved 25k which was a 10pc deposit on a 1 bed flat near bethnal green / bow, we probably should have saved more than that but we were where we were. No stamp duty as there was an exemption.

Lived there for 3.5 years. At that point our income remained about 95k ish. The fixed outgoings for that flat was 2k a month for the mortgage bills and service charge.

Wife then got made redundant and got a nice little payout.

All the while we had been ploughing any spare cash over and above a few k in a rainy day fund , into the mortgage- regularly overpaying 1.5-2k a month.

Sold the flat 3.5 years later for 185k more than we had paid for it. Purchased a freehold house 2.5 miles up the road for 388k. Spent just over 50k extending it and doing it up. Now its a 4 bed 3 bath house worth 600k and we owe 90 grand on it.

So it's worked out.

However, at the point we purchased the flat in 2011 part of me said this could be a very very bad decision. The service charge was extortion, the mortgage rate was 6.09pc (I paid 4k to get out of it early after a year to refinance it to 3pc in 2012) and the general outlook for property wasn't looking all that rosy in 2010/2011.

However there never is a ' good' time to buy property. If you've done your sums and research and it looks like a reasonable deal and you can afford it with a bit of wiggle room, then you may as well just get on with it.

By that point we had saved 25k which was a 10pc deposit on a 1 bed flat near bethnal green / bow, we probably should have saved more than that but we were where we were. No stamp duty as there was an exemption.

Lived there for 3.5 years. At that point our income remained about 95k ish. The fixed outgoings for that flat was 2k a month for the mortgage bills and service charge.

Wife then got made redundant and got a nice little payout.

All the while we had been ploughing any spare cash over and above a few k in a rainy day fund , into the mortgage- regularly overpaying 1.5-2k a month.

Sold the flat 3.5 years later for 185k more than we had paid for it. Purchased a freehold house 2.5 miles up the road for 388k. Spent just over 50k extending it and doing it up. Now its a 4 bed 3 bath house worth 600k and we owe 90 grand on it.

So it's worked out.

However, at the point we purchased the flat in 2011 part of me said this could be a very very bad decision. The service charge was extortion, the mortgage rate was 6.09pc (I paid 4k to get out of it early after a year to refinance it to 3pc in 2012) and the general outlook for property wasn't looking all that rosy in 2010/2011.

However there never is a ' good' time to buy property. If you've done your sums and research and it looks like a reasonable deal and you can afford it with a bit of wiggle room, then you may as well just get on with it.

I'm praying for a massive house price correction! It's just not sustainable, how many families are earning 6 figures to buy all these houses down south? I mean our 3 bed end of terrace is worth over £600k?? It's just mind boggling that there are enough people out there to buy them... bring on the crash and interest rate increases!

That’s another slight issue with market corrections. It’s only those with the capital today to move to the next rung up who are generally able to swallow the capital hit and obtain a mortgage after a correction. Those who haven’t the funds to move up now usually can’t move up when prices have come off either.

Big corrections only favour the cash rich generally speaking.

Big corrections only favour the cash rich generally speaking.

TooMany2cvs said:

Gregmitchell said:

I'm praying for a massive house price correction!

I mean our 3 bed end of terrace is worth over £600k??

So let's say there's a 50% reduction in house prices.I mean our 3 bed end of terrace is worth over £600k??

How much will that wipe off your equity?

Right question: how many people will that send into massive negative equity & what effect will that have on the housing market, house builders & the economy generally?

Gassing Station | Homes, Gardens and DIY | Top of Page | What's New | My Stuff