AML - Stock Market Listing

Discussion

We have discussed some aspects of this subject already, but an event has now occurred, which illustrates the concerns which I have previously referred to.

Motor manufacturing is a cyclical business. That was dramatically illustrated in 2008, when Aston Martin annual production numbers plummeted. There were redundancies at Gaydon to reduce existing costs, but as a private company they were abke to remain 'under the radar' and get on with the job. As the economic climate gradually improved, so did the company.

Once a company becomes a quoted company, some different circumstances arise. When difficult trading times occur, then sometimes predators become interested.

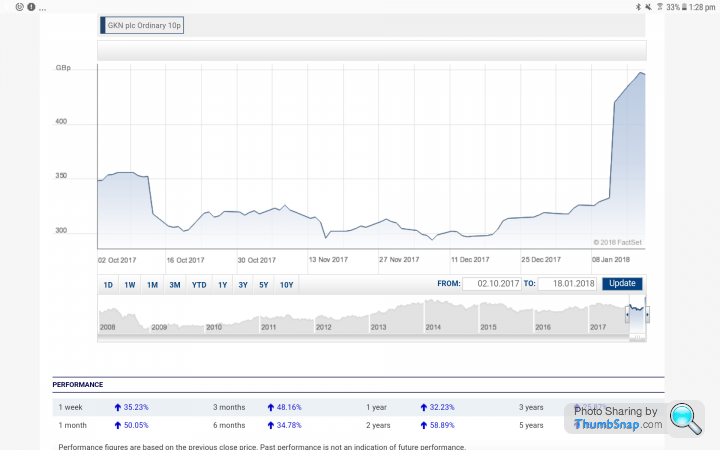

This has just happened to GKN (vested interest). The share price chart below tells the story. A few months ago GKN announced a profits warning (the share price drop). This week, an unsolicited takeover bid has been announced (the share price rise).

Anyone can attempt a takeover when a company is publicly quoted, but it could not happen to Aston Martin now.

Many of you will know all about this post flotation risk, but I thought it might be worth mentioning again.

If the present majority shareholders decide to float the Company though, then that is what will happen.

I fear this is quite awkward.

Usually a private equity shareholder wants to sell after a few years, and obviously at the best price.

Often an IPO can achieve a good price.

They are in business to take risks and make money. Nothing wrong with that.

After they have left the scene though, it is just another deal completed for them.

Aston Martin PLC would then be in the 'jungle', with a risk of being bought by anybody, particularly during difficult trading periods, because then the maket value would be lower.

Most companies are potentially for sale all the time at the right price.

Smaller companies (and especially those with ownership changes) do not not have the problem of a large pension fund (and potential deficit) with loads of deferred, current and future pensioners.

From my experience (a few years back) lots of businesses went buy way of trade sales with bidders even if a IPO being looked at. Trade sale a hell of at lot cheaper and quicker.

Those new engines & the 5% might be a good thing after all.

Although an IPO of 30% to allow development of company and brand and then further % sales should produce a lot more value over time.

Smaller companies (and especially those with ownership changes) do not not have the problem of a large pension fund (and potential deficit) with loads of deferred, current and future pensioners.

From my experience (a few years back) lots of businesses went buy way of trade sales with bidders even if a IPO being looked at. Trade sale a hell of at lot cheaper and quicker.

Those new engines & the 5% might be a good thing after all.

Although an IPO of 30% to allow development of company and brand and then further % sales should produce a lot more value over time.

Some of you might need to translate this

http://www.affaritaliani.it/economia/aston-martin-...

found right link

http://www.affaritaliani.it/economia/aston-martin-...

found right link

Edited by RL17 on Thursday 18th January 20:34

Zod said:

I depends on how much they float. Few IPOs these days are of more than 28-29%. You can't launch a bid with that level of free float unless you get enough of the pre-IPO shareholders on side.

Thank you Zoe, an important point.

Is there a pattern, whereby when private equity firms sell, it is usually their entire stakes ?

I think in this case, the holding is stated as 37.5%, so still below the crucial level.

The other shareholders, I think have been much longer-term (since the Ford sale), not that we can read anything into that.

They have 50% of voting stock/votes per the Italian article - looks like a single person controlled entity under Andrea Bonomi.

Believe other shareholders still including Kuwaiti TID and Adeem (54.5% by value) still involved, TID had big debt restructuring problems in 2015. Would give management slightly less than Daimler AG.

[Edit maybe just InvestIndustrial (Italy) controlling and The Investment Dar (TID) plus minor stakes now. Given TID's years of restructuring and trying to bundle assets (incl AM shares) out to creditors maybe (probably) a bigger float percentage would be offerered]

Believe other shareholders still including Kuwaiti TID and Adeem (54.5% by value) still involved, TID had big debt restructuring problems in 2015. Would give management slightly less than Daimler AG.

[Edit maybe just InvestIndustrial (Italy) controlling and The Investment Dar (TID) plus minor stakes now. Given TID's years of restructuring and trying to bundle assets (incl AM shares) out to creditors maybe (probably) a bigger float percentage would be offerered]

Edited by RL17 on Friday 19th January 19:53

Edited by RL17 on Friday 19th January 19:54

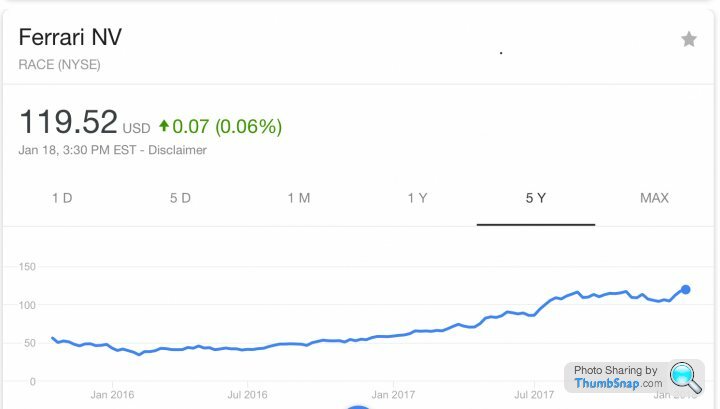

So Ferrari had a sticky start in 2015 but since a drop from $52 to $40ish, stock has tripled to over $120 and MV of $22.5bn (PE ratio of 35)

Seen reports of Aston at £5bn or just under $7bn.

Ferrari float just 10% but owned by Fiat Chrysler?

So IPO if bull market continues for 6-9 months (or IPO)? or trade sale at 75-80% of above value after a dip (or less after a bigger correction)?

Re Daimler (MB) - their PE is 9.5 and they are potentially under pressure (due to Ferrari values etc) to consider possibilities to spin off high end brands -say AMG, which makes investing at the high end valuations talked about to do the reverse unlikely?

Seen reports of Aston at £5bn or just under $7bn.

Ferrari float just 10% but owned by Fiat Chrysler?

So IPO if bull market continues for 6-9 months (or IPO)? or trade sale at 75-80% of above value after a dip (or less after a bigger correction)?

Re Daimler (MB) - their PE is 9.5 and they are potentially under pressure (due to Ferrari values etc) to consider possibilities to spin off high end brands -say AMG, which makes investing at the high end valuations talked about to do the reverse unlikely?

RL17 said:

So Ferrari ...MV of $22.5bn (PE ratio of 35)

Seen reports of Aston at £5bn, or just under $7bn.

Seen reports of Aston at £5bn, or just under $7bn.

The Ferrari PE is historic presumably?

Would you consider Ferrari to be completely unique? A car manufacturer, supplier of branded 'objects' and operator of profitable theme parks. I hear that they don't even have to sell cars anymore. Customers apply and apparently are then vetted, to see if they are eligible to buy one.

For AM, the talk we have heard, about luxury goods ratings for a car manufacturer puzzles me.

Perhaps depends on whether one is a seller, or buyer of the stock.

2016 Pre Tax Loss was said to be -£162.8 million.

A 2017 Pre tax positive figure I think is forecast, but for an IPO MV of £5bn, how high would that make the PE ?

Edited by Jon39 on Friday 19th January 22:38

Results per AM mentions looking at IPO

https://www.astonmartin.com/en/live/news/2018/02/2...

and DT write up

http://www.telegraph.co.uk/business/2018/02/26/ast...

https://www.astonmartin.com/en/live/news/2018/02/2...

and DT write up

http://www.telegraph.co.uk/business/2018/02/26/ast...

Excellent news. Back in the black.

Thought the talk of ' Profits grow by quarter of a billion pounds ' was just a little too much hype, when the pre-tax was £87m.

"Job done", AP is reported to have said. I hope those were not his words.

I have mentioned before, but there is an interesting pattern now developing, in comparison to the period when the DB9 and Vantage were introduced.

The Company was profitable from 2000 to 2010 (except 2004). Peak production at Gaydon was 7281 cars in 2007. Peak pre-tax profit of that period was £57m in 2006, the year before the Ford sale.

I will look at the 2017 accounts, when they appear at Companies House.

New Articles of Association were adopted in May 2017, and I noticed the signature of Dr. Bez. Presumably he has retained his shareholding.

ajr550 said:

That knighthood for Andy Palmer that nobody wanted to support must be getting closer !

He's already a Companion of The Most Distinguished Order of St Michael and St George (CMG) for his work at Nissan.The logical next step is adding Knight Commander (KCMG) which has a nice ring to it!

If he continues the way he's going, he'll thoroughly deserve it!

Gassing Station | Aston Martin | Top of Page | What's New | My Stuff