PCP: How many people actually pay the balloon

Discussion

I think the Fabia vs Elise point was that if you run a used car you can choose the car.

If you keep going back for yet another lease, you take what you can get. In poor spec, with no options added to drive the monthly up in case you have to admit your sums don't work after all...

You'll end up with a Fabia. Or a Tiguan TDi.

If you go look for prices on something that a PHer might actually WANT to drive, the deals vanish and the sums no longer work.

If you want cheap, buy used. If you want new, just admit that you like having a new car for no other reason than it's new. Don't pretend new is cheap.

If you keep going back for yet another lease, you take what you can get. In poor spec, with no options added to drive the monthly up in case you have to admit your sums don't work after all...

You'll end up with a Fabia. Or a Tiguan TDi.

If you go look for prices on something that a PHer might actually WANT to drive, the deals vanish and the sums no longer work.

If you want cheap, buy used. If you want new, just admit that you like having a new car for no other reason than it's new. Don't pretend new is cheap.

I did. Skoda VRS on 0% PCP for 3.5 yrs paid the balloon at the end. Looked at other cars but none ticked all the boxes that the Skoda did so what was the point in another PCP deal when a bank transfer meant £0 per month in finance payments. When the car gets replaced I'm sure I will look at another deal but at the moment having no car payments is nice.

TartanPaint said:

If you go look for prices on something that a PHer might actually WANT to drive, the deals vanish and the sums no longer work.

Considering that "PHish" cars tend to have stronger residuals than mainstream ones, that's a bit odd really. I suppose it comes down to the fact that discounts on new low-volume cars tend to be smaller than those on mainstream ones. my last 2 cars were on pcp and both were paid off early

1st one (Vw tiguan) the pcp was paid off within a couple of weeks of getting the car,

the only reason we pcp'd it was to gain the £1500 deposit contribution, but with an apr of 6.5% it didn't make sense to keep it going

the second (a Ford fiesta) the incentive of a £500 contribution and a rate of 0.9% apr was too good to good to ignore

I paid this off after 11 months because I wasn't using the car and decided to sell it.

When I was at Citroen, they were doing a £4000 deposit contribution on ds4 same lots of people took it out and paid it off within a few months.

Wouldn't call this paying the balloon though as Citroen pretty much knew every single customer was planning to do it on this sort of vehicle and not keep it the 35 months or so

Wouldn't call this paying the balloon though as Citroen pretty much knew every single customer was planning to do it on this sort of vehicle and not keep it the 35 months or so

kambites said:

nickfrog said:

What are you on about ? I am comparing like for like - older family car to new leased family car.

Oh sorry, since you quoted me I assumed you were responding to my post. If you meant to quote someone else, apologies.

. Forget about the Elise and compare the actual total cost of a leased new Octavia and a 10 year old similar Octavia. As I said, the actual delta is very small. But if it's too large a delta for you to prefer the 10 year old car, fair enough, each to their own.

. Forget about the Elise and compare the actual total cost of a leased new Octavia and a 10 year old similar Octavia. As I said, the actual delta is very small. But if it's too large a delta for you to prefer the 10 year old car, fair enough, each to their own.TartanPaint said:

I think the Fabia vs Elise point was that if you run a used car you can choose the car.

If you keep going back for yet another lease, you take what you can get. In poor spec, with no options added to drive the monthly up in case you have to admit your sums don't work after all...

You'll end up with a Fabia. Or a Tiguan TDi.

If you go look for prices on something that a PHer might actually WANT to drive, the deals vanish and the sums no longer work.

If you want cheap, buy used. If you want new, just admit that you like having a new car for no other reason than it's new. Don't pretend new is cheap.

?If you keep going back for yet another lease, you take what you can get. In poor spec, with no options added to drive the monthly up in case you have to admit your sums don't work after all...

You'll end up with a Fabia. Or a Tiguan TDi.

If you go look for prices on something that a PHer might actually WANT to drive, the deals vanish and the sums no longer work.

If you want cheap, buy used. If you want new, just admit that you like having a new car for no other reason than it's new. Don't pretend new is cheap.

You can lease any car you want with whatever spec you want assuming you have the budget. I don't see how that's any different from buying used, and at least the car can be specified exactly how you want it rather than hoping to find a used example where someone else thinks the same way as you do?

Of course it's more expensive than buying an older car (+5 years) but is a far easier experience and it is a nice feeling knowing it's not been thrashed or messed with by anyone else. Once you're talking about 2-3 year old used the numbers can be surprisingly close if you take your time and are smart in the deal you get, again this is from actual experience of having done both numerous times.

TartanPaint said:

I think the Fabia vs Elise point was that if you run a used car you can choose the car.

If you keep going back for yet another lease, you take what you can get. In poor spec, with no options added to drive the monthly up in case you have to admit your sums don't work after all...

You'll end up with a Fabia. Or a Tiguan TDi.

If you go look for prices on something that a PHer might actually WANT to drive, the deals vanish and the sums no longer work.

If you want cheap, buy used. If you want new, just admit that you like having a new car for no other reason than it's new. Don't pretend new is cheap.

The car I WANT to drive (as opposed to NEED to drive when on a family trip) is far cheaper to own than to rent, so I own it. You can't track a leased car anyway.If you keep going back for yet another lease, you take what you can get. In poor spec, with no options added to drive the monthly up in case you have to admit your sums don't work after all...

You'll end up with a Fabia. Or a Tiguan TDi.

If you go look for prices on something that a PHer might actually WANT to drive, the deals vanish and the sums no longer work.

If you want cheap, buy used. If you want new, just admit that you like having a new car for no other reason than it's new. Don't pretend new is cheap.

I insist on new because it's only slightly cheaper than a 3/4 year old car, the difference is immaterial, probably 20%/£50/month, I don't need to pretend anything, it's cheap as chips and new/warrantied, what's not to like? If the difference was greater, then I would certainly consider second hand, but I don't have to. The Tiguan was cheaper new than if we had bought a two-year old one when you look at all the parameters already listed.

Edited by nickfrog on Thursday 19th October 17:23

nickfrog said:

You're good as passive-aggressive I give you that . Forget about the Elise and compare the actual total cost of a leased new Octavia and a 10 year old similar Octavia. As I said, the actual delta is very small. But if it's too large a delta for you to prefer the 10 year old car, fair enough, each to their own.

Our Octavia has worked out somewhere around the £100 a month mark in total I think (I don't track the Skoda's running costs anywhere near as accurately as the Lotus). I must admit I haven't a clue what a new one costs; if you can get one for £150 a month including insurance and everything that's fair enough, that's bloody good value. I'd assumed it'd be more like £250-300!. Forget about the Elise and compare the actual total cost of a leased new Octavia and a 10 year old similar Octavia. As I said, the actual delta is very small. But if it's too large a delta for you to prefer the 10 year old car, fair enough, each to their own.Edited by kambites on Thursday 19th October 17:32

I leased a Volvo S80 in 2009. Lease payments were 10K over the 3 years. Bought it from the leasing company at the end of the lease for 11k. Still have it 8 years later. List price was 27k so paying 21k for it isn't too bad. Again, I think I'm probably unusual in doing this but as mentioned by another poster, I'd looked after it and it had been and still is 100% reliable. At the end of the 3yrs there wasn't anything else at the time that I wanted, I had the cash and I didn't want to commit to another finance agreement.

kambites said:

nickfrog said:

You're good as passive-aggressive I give you that . Forget about the Elise and compare the actual total cost of a leased new Octavia and a 10 year old similar Octavia. As I said, the actual delta is very small. But if it's too large a delta for you to prefer the 10 year old car, fair enough, each to their own.

Our Octavia has worked out somewhere around the £100 a month mark in total I think (I don't track the Skoda's running costs anywhere near as accurately as the Lotus). I must admit I haven't a clue what a new one costs; if you can get one for £150 a month including insurance and everything that's fair enough, that's bloody good value. I'd assumed it'd be more like £250-300!. Forget about the Elise and compare the actual total cost of a leased new Octavia and a 10 year old similar Octavia. As I said, the actual delta is very small. But if it's too large a delta for you to prefer the 10 year old car, fair enough, each to their own.Edited by kambites on Thursday 19th October 17:32

I always used to buy cars at 3 years old and 30-40k mileage or so once they'd take the biggest depreciation hit and then run them for a couple of years. I'd always pay for an extended or good quality warranty at about £1000 over the 2 years + breakdown cover etc.

The issue was that no matter how good the extended or third party warranty there were always issues if needing to make a claim as it's never the same as a new car warranty. Between 40-70k things like brake pads and discs needed paying for as well as major services, MOT's, roadtax etc.

Once I'd actually added up the real cost of ownership over 2 years and 30k in comparison to leasing a brand new comparible car I found the difference to be far smaller than I'd imagined and for me at least well worth the reduction in aggravation of running a second hand car and then trying to sell it on after 2 years (which after a month of time-wasters ended in a reduced price trade in to a WWAC type of outfit)

This was comparing a 3 year old 5 Series to a leased E Class. From memory the figures were something like £750 loan interest, £5k depeciation, £1k warranty, £300 tax, £100 MOT's, £600 servicing, £500 brakes for the 5 series (about £8-8.5K in total) and £9250 for the E class all in at £1800 down and £300 a month over 2 years + a minor service..

SWoll said:

For me that's far too wide an age gap for their to be any point in comparing the two.

Fair point, although ours was only four years old when we got it; there has just been no reason to change it since. With the post which started this I wasn't trying to say there was anything wrong with paying £200+ a month for a new Fabia; just that for me personally running our aging pair of cars for roughly the same total money combined represents better value. For others, the Fabia may very well be the better value proposition which is good because if people didn't find new car leases better value than second-hand ones, we'd almost certainly have something of a shortage of second-hand ones.

Edited by kambites on Friday 20th October 06:01

Baloon payments on PCP are usually set up to be around 80% of the book value at the time. It makes no financial sense to hand it back.

I think the fact that many do shows the success of the sales tactics evolved around it. I know several people who think they have been offered a great deal for a new PCP, without realising the dealer is simply redeplying the excess profit they are making by taking a car back at 80% of it's value.

People like shiny new things and they are easily confused by the 'man maths' techniques the dealers have pretty much perfected.

I think the fact that many do shows the success of the sales tactics evolved around it. I know several people who think they have been offered a great deal for a new PCP, without realising the dealer is simply redeplying the excess profit they are making by taking a car back at 80% of it's value.

People like shiny new things and they are easily confused by the 'man maths' techniques the dealers have pretty much perfected.

Elysium said:

Baloon payments on PCP are usually set up to be around 80% of the book value at the time. It makes no financial sense to hand it back.

I think the fact that many do shows the success of the sales tactics evolved around it. I know several people who think they have been offered a great deal for a new PCP, without realising the dealer is simply redeplying the excess profit they are making by taking a car back at 80% of it's value.

People like shiny new things and they are easily confused by the 'man maths' techniques the dealers have pretty much perfected.

When the time comes, I'll sell you my car for the balloon payment figure, if you like. Sounds like you're certain there's a 25% profit to be made.I think the fact that many do shows the success of the sales tactics evolved around it. I know several people who think they have been offered a great deal for a new PCP, without realising the dealer is simply redeplying the excess profit they are making by taking a car back at 80% of it's value.

People like shiny new things and they are easily confused by the 'man maths' techniques the dealers have pretty much perfected.

kambites said:

Our Octavia has worked out somewhere around the £100 a month mark in total I think (I don't track the Skoda's running costs anywhere near as accurately as the Lotus). I must admit I haven't a clue what a new one costs; if you can get one for £150 a month including insurance and everything that's fair enough, that's bloody good value. I'd assumed it'd be more like £250-300!

It's sometimes quite surprising how the numbers work out with new vs. old. I admit, this one is a very specific case and for every case like this you could find some extreme numbers the opposite way but alas... Edited by kambites on Thursday 19th October 17:32

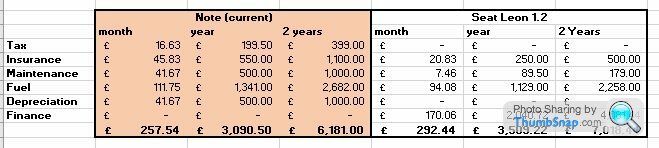

My wife has an old Nissan Note. It's the family wagon and a little bit shabby in places and being 10 years old and about 90k miles, there are a couple of biggish jobs looming, tyres being the main one and they're an awkward size, nothing horrendous though. It's a 1.6 petrol and used predominantly around town and averages around 32mpg over about 8k per year. Neither her nor I like it very much so were considering a change to 1.2TSi Leon Lease over 2 years. For some reason a Seat is far cheaper for her to insure. I estimate it would do round 38mpg under same sort of driving and lease costs 'amortise' at about £170 per month. These are the numbers I calculated. Not foolproof but I tried to be realistic.

So if I'm anywhere close to being right, it's less £1000 difference over 2 years for the Leon vs. 10 year old Note. Which seems good value on the face of it. I realised I didn't include breakdown cover for the Note but it doesn't change numbers massively.

Being totally honest about the situation, there are cheaper options again by buying an older car that requires less maintenance or depreciates less or is far better on fuel but there is some unqunatifiable value in having a new car under warranty.

swerni said:

We have a financial genius who drives a Fiesta and probably lives with his mummy....

I’ve just PCP’d an Africa Twin ( like a number of other PHers)

0 deposit (dealer paid the £3k)

£70 a month.

£6k ish balloon.

I’m renting a bloody bike for £70 a month, why an earth would I want to pay cash for it ?

I’ve just PCP’d an Africa Twin ( like a number of other PHers)

0 deposit (dealer paid the £3k)

£70 a month.

£6k ish balloon.

I’m renting a bloody bike for £70 a month, why an earth would I want to pay cash for it ?

I particularly love the 'probably lives with his mummy' comment - wow with razor sharp debating skills like those, who knows what gold is in your other 20,000 posts!

Just to be clear, is your point that

a) The Fiesta ST is such a crap car that someone should be ridiculed for owning it (outright, as it happens)

b) Owning a car universally lauded for being great bang for buck and a performance bargain makes me LESS qualified to comment on financial issues

c) Both of the above (plus I live with 'my mummy' apparently).

Regarding the rented bike that you don't own, what makes ladies throw themselves as you more - the sight of you in your leathers riding it or the bit where you stop, look back and wink 'I pay £70 a month to PCP this ladies!'

I mean don't get me wrong, renting rather than owning things is a sure fire winner with the very hottest of birds, that point would never be up for debate, never.

Edited by HumanDoing on Friday 20th October 09:13

I think people handing them back isnt really about the financial aspect, so many folk are clueless when it comes to selling a car privately, it can be a massive faff, throw in the lure of a shiny new one, pretend to pay attention about APR's, terms and stuff and then drive out with a nice new car costing broadly the same per month as the old one.

With various commitments I have currently, I dont really have the disposable income to do that and not really worry about that cost, and what I could do it for.

Most dont have 25 grand or so sat around in cash for a car, and if we do, we like to keep it there, just in case and see that as long term savings where the car is a monthly cost.

I dont rule it out but thus far I have been pretty old school but can totally see how it works for so many people, as long as you cut your cloth accordingly and dont use it as a method to overstretch then I dont see the problem, I get the impression though that people turn a blind eye to the cost of that new Evoque or whatever, £350 a month, plus insurance which is all out of your cleared income you have been hammered for tax and NI on, makes you realise how much you have to earn to pay for a car like that, from your gross salary its like six or seven grand a year.

My motoring for the next few months is covered by £20 a year tax and £150 insurance, 45 plus to the gallon on a car I bought outright six years ago, I think walking would be more expensive, it will be joined by a seven type thing for fun, little depreciation, cheap insurance and sorn it when not in use.

With various commitments I have currently, I dont really have the disposable income to do that and not really worry about that cost, and what I could do it for.

Most dont have 25 grand or so sat around in cash for a car, and if we do, we like to keep it there, just in case and see that as long term savings where the car is a monthly cost.

I dont rule it out but thus far I have been pretty old school but can totally see how it works for so many people, as long as you cut your cloth accordingly and dont use it as a method to overstretch then I dont see the problem, I get the impression though that people turn a blind eye to the cost of that new Evoque or whatever, £350 a month, plus insurance which is all out of your cleared income you have been hammered for tax and NI on, makes you realise how much you have to earn to pay for a car like that, from your gross salary its like six or seven grand a year.

My motoring for the next few months is covered by £20 a year tax and £150 insurance, 45 plus to the gallon on a car I bought outright six years ago, I think walking would be more expensive, it will be joined by a seven type thing for fun, little depreciation, cheap insurance and sorn it when not in use.

Gassing Station | General Gassing | Top of Page | What's New | My Stuff