AML - Stock Market Listing

Discussion

Either way, it is an awful lot of people isn’t it? Some 2 billion viewers globally. Aston has plans to sell 6k cars this year.

His presentation style maybe a touch wooden but given (his) research suggests that 1.6bn are would be performance car buyers, he only needs to successfully market to 0.000375 percent of them to be on track!

It appears to be a cost free option as well. He may just be onto something here!

His presentation style maybe a touch wooden but given (his) research suggests that 1.6bn are would be performance car buyers, he only needs to successfully market to 0.000375 percent of them to be on track!

It appears to be a cost free option as well. He may just be onto something here!

CB07 said:

It appears to be a cost free option as well.

It is thought that AML were paying Red Bull about £10 million annually to be their 'title sponsor'.

LS indicated a lower amount for Racing Point this year.

Think AML are also paying SB, to be a brand ambassador. Probably not at minimum wage rate.

I posted LS's quotes on this topic, because sometimes it can be interesting, looking back to what has been said.

That 2.3 billion audience figure.

For a season with 21 races, would that mean 2.3 billion total for the whole season?

If so, then they are counting the same fans multiple times.

Then there is his 80% claim. I don't think 1,800,000,000 performance cars are sold every year, even if you include the Special Performance edition of the Kia Cee'd.

From a very crude google search it appears to be a cumulative seasons total. On reflection 1/4 of the worlds population are probably not tuning in every week. Not that it matters for a press release.

Unique views in one article mentions 475m. Which is still enormous!

Having said that, the “performance car” stat probably comes

from an online sample survey of say 10k qualified F1 fans from across the world who were invited by clicking on affiliate links on YouTube or wherever.

Questions could simply be “who is your favourite F1 driver” “how often do you watch F1” “are you expecting to buy a new car in the next 5 years” “do you like performance cars” “if money was no object would that be a) Ferrari b) Mclaren c) Lamborghini d) Aston Martin

Stats are stats and you can easily manipulate anything to sound fancy enough.

Equally they could survey this parish on here and get solid feedback on grills, engines, parts bin heritage or indeed integrated say nav and all that fun stuff. Not sure it would make the headlines in quite the same way though so I can see why he has picked some sensational sounding ones instead.

On balance I think I quite like him!

Unique views in one article mentions 475m. Which is still enormous!

Having said that, the “performance car” stat probably comes

from an online sample survey of say 10k qualified F1 fans from across the world who were invited by clicking on affiliate links on YouTube or wherever.

Questions could simply be “who is your favourite F1 driver” “how often do you watch F1” “are you expecting to buy a new car in the next 5 years” “do you like performance cars” “if money was no object would that be a) Ferrari b) Mclaren c) Lamborghini d) Aston Martin

Stats are stats and you can easily manipulate anything to sound fancy enough.

Equally they could survey this parish on here and get solid feedback on grills, engines, parts bin heritage or indeed integrated say nav and all that fun stuff. Not sure it would make the headlines in quite the same way though so I can see why he has picked some sensational sounding ones instead.

On balance I think I quite like him!

Jon39 said:

I posted LS's quotes on this topic, because sometimes it can be interesting, looking back to what has been said.

That 2.3 billion audience figure.

For a season with 21 races, would that mean 2.3 billion total for the whole season?

If so, then they are counting the same fans multiple times.

Then there is his 80% claim. I don't think 1,800,000,000 performance cars are sold every year, even if you include the Special Performance edition of the Kia Cee'd.

Best Regards

Minglar

Minglar said:

<clip> the F1 car does look pretty good though, and I will watch the races, supporting the team. It will be interesting to see how they fare against Hamilton and Mercedes next season...

If you are into F1 it has the prospects being a very good season. Hamilton going for a record 8th WDC. Vettel out to prove himself after his abject decline at Ferrari. Perez also with a point to prove after being unceremoniously sacked by the team to which he had given his all. He needs no more motivation to beat the Astons and pitch himself up there against Red Bull's favoured one. Not forgetting it was actually McLaren who finished in 3rd place as a constructor and they now have the Mercedes engine and a great driver combination, I can't see them being any slower! Whilst I will be looking forward to seeing Hamilton win, I will be keeping a close eye on the battles immediately behind. I can't wait! There are reports now of 200 redundancies at St Athan.

Some of those are said to be employees and a number are working through an employment provider.

Should we question therefore, whether production of the new DBX is running at a high rate, to meet a strong level of initial orders? As we all know, the success of this model, is vital to the immediate financial future of AML.

AdamV12V said:

Yes, I glanced through that yesterday Adam, but when the HSBC analyst incorporates such obvious factual errors in their report, it does not provide much confidence about their knowledge of AML.

Wonder if the same analyst wrote any guidance, prior to the IPO? Does anyone know?

AdamV12V said:

They also quote:"High risk, high reward: upgrade to Buy (from Hold) ... AML is not "another Ferrari" today and it won't be in 2026 either.

I fear I see the usual "new management" playbook that has been operating in the industry for years. it goes something like this:

- New management arrives

- Previous management is reported as the worst in history of management; situation much worse than first thought

- Announce that previous management's plan was unrealistic and will need to be revised

- (optional) Engage management consultancy vultures like McKinsey to give credibility to the new management actions

- Load all the issues, debt, costs of restructuring, costs for new plan into a big, toxic debt ball and blame the previous management

- Announce that there will have to be streamlining - reluctantly announce "staff restructuring" (aka redundancies) and blame the previous management

- Announce "new, realistic but dynamic plan". Use "management bulls

t bingo" phrase generator to sprinkle message with impressive-sounding phrases like "maximising synergy", "lean, nimble and focussed" "leveraging our assets"; "our people are the key"; "unleashing untapped potential"

t bingo" phrase generator to sprinkle message with impressive-sounding phrases like "maximising synergy", "lean, nimble and focussed" "leveraging our assets"; "our people are the key"; "unleashing untapped potential" - Analysts who don't understand the industry are impressed with the new, dynamic management; share price rises

- time passes

- Discover the reduced, lean workforce cannot deliver the ambitious new business plan

- Surreptitiously re-hire some or all of the previously-reduced payroll "fat" in an attempt to make the numbers and models forecast

- Realise that you can't blame the previous management any more

- Analysts and shareholders begin to realise that the emperor may be, at best, just wearing underwear (the employees realised this months ago)

- Go to step 1

Jon39 said:

AdamV12V said:

Yes, I glanced through that yesterday Adam, but when the HSBC analyst incorporates such obvious factual errors in their report, it does not provide much confidence about their knowledge of AML.

Wonder if the same analyst wrote any guidance, prior to the IPO? Does anyone know?

I don’t know if it’s been linked further back in this thread but this is a great blog post talking about Aston’s current situation. The writer used to be known as Secret Supercar Owner in Evo and does frequent PH. There are previous blog posts on Aston’s financial situation too.

https://karenable.com/aston-martins-q4-full-year-2...

Cheib said:

I don’t know if it’s been linked further back in this thread but this is a great blog post talking about Aston’s current situation. The writer used to be known as Secret Supercar Owner in Evo and does frequent PH. There are previous blog posts on Aston’s financial situation too.

He provides a very detailed analysis but does annoy me slightly, by quoting the wrong peak production figure at least twice.

Seemed to be more bearish in his latest report, than the earlier one.

Based on the ups and downs during its long history and also considering the huge debt burden, i think a bearish view must be the right one, unless the DBX can maintain sales at the maximum production.level. As referenced by Cheib, debt has become difficult. It originated when the business was purchased from Ford and in recent years has increased considerably, just to maintain cash flow. Followng the recent refinancing, servicing costs increased from the previous level and that at a time of record low interest rates. Imagine that situation at the next time of refinancung. If the servicing costs continue to escalate, then eventually disaster looms.

Sorry to be gloomy, but car manufacturing can be a tough competitive business.

SFO said:

HSBC investment research is not top tier .. very much second, if not third, tier

The whole premise of that rating “bullish on new management” is just poor. Whatever Moers does in terms of cost cutting etc is frankly just peripheral noise for the next 12 months around the issue of whether Aston can sell enough DBX’s. Jon39 said:

Then there is his 80% claim. I don't think 1,800,000,000 performance cars are sold every year, even if you include the Special Performance edition of the Kia Cee'd.

I'm not sure if the 80% thing is a misspoke or a misquote, but a quote in the 2020 results turns it upside down:"80% of luxury/premium car buyers are interested in F1" which is very different from the "80% of F1 viewers are performance car buyers".

ETA - I just watch the interview - He also said "There's about 100 people that watch every formula one race" Seriously?

https://amsc-prod-cd.azureedge.net/-/media/corpora...

200 jobs going at St Athan is bad news (25-30% of the workforce?) and the savings (maybe £10-15m p/a?) are a drop in the ocean compared to the losses.

Edited by silentbrown on Thursday 11th March 10:14

Cheib said:

Jon39 said:

AdamV12V said:

Yes, I glanced through that yesterday Adam, but when the HSBC analyst incorporates such obvious factual errors in their report, it does not provide much confidence about their knowledge of AML.

Wonder if the same analyst wrote any guidance, prior to the IPO? Does anyone know?

I don’t know if it’s been linked further back in this thread but this is a great blog post talking about Aston’s current situation. The writer used to be known as Secret Supercar Owner in Evo and does frequent PH. There are previous blog posts on Aston’s financial situation too.

https://karenable.com/aston-martins-q4-full-year-2...

I believe you are spot on. It is currently about servicing and refinancing the debt.

Jon39 said:

Cheib said:

I don’t know if it’s been linked further back in this thread but this is a great blog post talking about Aston’s current situation. The writer used to be known as Secret Supercar Owner in Evo and does frequent PH. There are previous blog posts on Aston’s financial situation too.

He provides a very detailed analysis but does annoy me slightly, by quoting the wrong peak production figure at least twice.

Seemed to be more bearish in his latest report, than the earlier one.

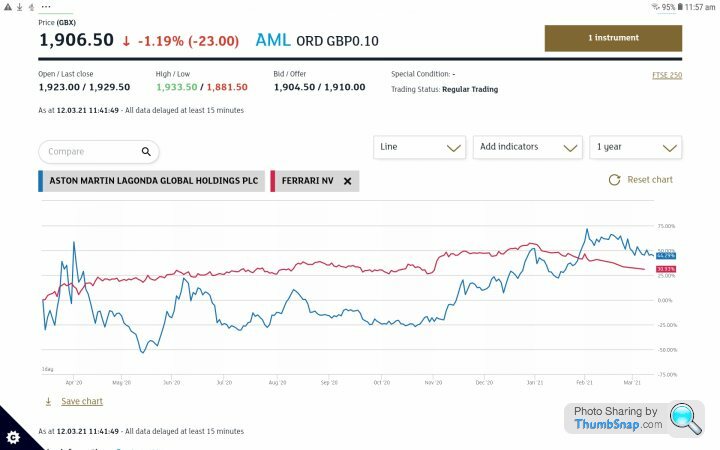

Just idly looking at the share price (disclaimer: I don't have any) and I noticed this - and I'm sure I'm not the only one. The 2020 results clearly went down well.

Graph courtesy of London Stock Exchange website; coloured lines are mine, are just visual "best fit" and the approximate presentation date of 25th February

edited to add source

Graph courtesy of London Stock Exchange website; coloured lines are mine, are just visual "best fit" and the approximate presentation date of 25th February

edited to add source

Edited by LTP on Friday 12th March 11:45

LTP said:

Just idly looking at the share price (disclaimer: I don't have any) and I noticed this - and I'm sure I'm not the only one. The 2020 results clearly went down well.

Graph courtesy of London Stock Exchange website; coloured lines are mine, are just visual "best fit" and the approximate presentation date of 25th February

Graph courtesy of London Stock Exchange website; coloured lines are mine, are just visual "best fit" and the approximate presentation date of 25th February

Now we are motoring Paul (or as LS likes to say gangbustering).

Seem to be leading Ferrari after 12

Gassing Station | Aston Martin | Top of Page | What's New | My Stuff