AML - Stock Market Listing

Discussion

An interesting AMLGH situation has arisen regarding the new Vantage.

Many PHers new to the Aston Martin forum have told us, they have recently obtained a new Vantage, because there are unbelievable finance deals.

I think one example was in respect of a £150,000 car, for just £1,000 deposit and then 24 monthly payments of £1,000.

Two years use for only £25,000 and all the options seem to be free.

What is going on, because the early buyers presumably would have paid normal prices for their cars ?

How can there be any profit for AML with that arithmetic ?

I have no inside knowledge, but thinking about these remarkably enticing deals, I just wonder whether there was initial period showroom and demonstrator stocking at all the dealers, which kept Gaydon busy. If the retail sales were then slower than target, eventually the dealers become overstocked and don't order further stock from AML. That is the point at which it would impact Gaydon production.

What do you think ?

One PHer even described, 'No deposit and 24 monthly payments of £1,000' - as a no brainer for a £130,000 new car.

Jon39 said:

An interesting AMLGH situation has arisen regarding the new Vantage.

Many PHers new to the Aston Martin forum have told us, they have recently obtained a new Vantage, because there are unbelievable finance deals.

I think one example was in respect of a £150,000 car, for just £1,000 deposit and then 24 monthly payments of £1,000.

Two years use for only £25,000 and all the options seem to be free.

What is going on, because the early buyers presumably would have paid normal prices for their cars ?

How can there be any profit for AML with that arithmetic ?

I have no inside knowledge, but thinking about these remarkably enticing deals, I just wonder whether there was initial period showroom and demonstrator stocking at all the dealers, which kept Gaydon busy. If the retail sales were then slower than target, eventually the dealers become overstocked and don't order further stock from AML. That is the point at which it would impact Gaydon production.

What do you think ?

One PHer even described, 'No deposit and 24 monthly payments of £1,000' - as a no brainer for a £130,000 new car.

Bobajobbob said:

I've never bought a car this way. What happens at the end of the 24 months? Do you simply hand back the car or pay the £105k balance or pay the difference between £105k and the market value at the time?

I don't know how a lease works in the UK. But in the US, yes you either pay the £105K plus any taxes on top of that. Or turn the car in and walk away, once the car is is inspected for excess mileage or damage other than normal wear and tear. The leasing company won't make a deal on the price, other than possibly refinance the balance if wanted. Leases are good if you want to drive a car you otherwise would not afford, can write it of as a business expense, or plan to buy it out with cash at the end of the lease. Otherwise you basically just renting the car. Insurance tends to be more expensive aswell.

Bobajobbob said:

I've never bought a car this way. What happens at the end of the 24 months? Do you simply hand back the car or pay the £105k balance or pay the difference between £105k and the market value at the time.

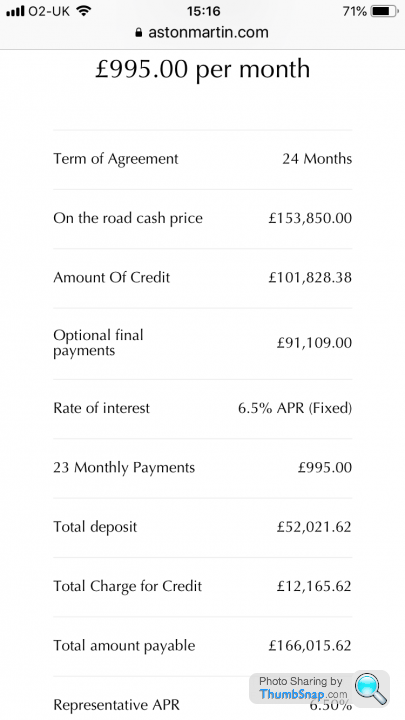

On the New Vantage chat topic, one of the stated amounts to pay after 24 months, is about £89,000.

This topic is more to do with the corporate side of AML, so when I asked what is going on, rather than the contract payment details, it was more wondering why AML is offering £150,000 cars, at a pay later price of £115,000.

Could it perhaps just be a temporary offer, to move on a quantity of stock (possibly at a loss), so that the production rates can be maintained.

Bobajobbob said:

Jon39 said:

An interesting AMLGH situation has arisen regarding the new Vantage.

Many PHers new to the Aston Martin forum have told us, they have recently obtained a new Vantage, because there are unbelievable finance deals.

I think one example was in respect of a £150,000 car, for just £1,000 deposit and then 24 monthly payments of £1,000.

Two years use for only £25,000 and all the options seem to be free.

What is going on, because the early buyers presumably would have paid normal prices for their cars ?

How can there be any profit for AML with that arithmetic ?

I have no inside knowledge, but thinking about these remarkably enticing deals, I just wonder whether there was initial period showroom and demonstrator stocking at all the dealers, which kept Gaydon busy. If the retail sales were then slower than target, eventually the dealers become overstocked and don't order further stock from AML. That is the point at which it would impact Gaydon production.

What do you think ?

One PHer even described, 'No deposit and 24 monthly payments of £1,000' - as a no brainer for a £130,000 new car.

After 24 months (or frequently less than 24 months if you can exit lease early at minimal cost) you lease the next car on your wish list within your monthly cost range. No MOTs, no service costs usually and no out of warranty surprises or clutch worries. Keep car in reasonable condition and drive it hard without going through tyres and don't exceed the agreed mileages - fixed cost motoring.

Jon39 said:

On the New Vantage chat topic, one of the stated amounts to pay after 24 months, is about £89,000.

This topic is more to do with the corporate side of AML, so when I asked what is going on, rather than the contract payment details, it was more wondering why AML is offering £150,000 cars, at a pay later price of £115,000.

Could it perhaps just be a temporary offer, to move on a quantity of stock (possibly at a loss), so that the production rates can be maintained.

Bobajobbob said:

Jon39 said:

On the New Vantage chat topic, one of the stated amounts to pay after 24 months, is about £89,000.

This topic is more to do with the corporate side of AML, so when I asked what is going on, rather than the contract payment details, it was more wondering why AML is offering £150,000 cars, at a pay later price of £115,000.

Could it perhaps just be a temporary offer, to move on a quantity of stock (possibly at a loss), so that the production rates can be maintained.

So not free cash to AM.

Interest cost alone to AM in full year equates to about 1,250 car sales! (average revenue to AM (incl specials £167k) and 37% gross profit margin).

Assume finance houses as part of big banks etc must be get cash at very low rates and interest margin (and low up front car cost) makes up for risk on guaranteed value at 24 months. More isolated financing companies could be more at risk.

Jon39 said:

0.

This topic is more to do with the corporate side of AML, so when I asked what is going on, rather than the contract payment details, it was more wondering why AML is offering £150,000 cars, at a pay later price of £115,000.

.

It’s called “pipeline filling” and there has been an awful lot of that recently (not only from AML). I can only speculate that AML is picking up the bill at the end once the two year lease deal is expiring in order to get the dealers to shift cars. As an earlier poster said. Cash (rather than profit) is king at this stage of AML’s short life as a listed company.

Jon39 said:

An interesting AMLGH situation has arisen regarding the new Vantage.

Many PHers new to the Aston Martin forum have told us, they have recently obtained a new Vantage, because there are unbelievable finance deals.

I think one example was in respect of a £150,000 car, for just £1,000 deposit and then 24 monthly payments of £1,000.

Two years use for only £25,000 and all the options seem to be free.

What is going on, because the early buyers presumably would have paid normal prices for their cars ?

How can there be any profit for AML with that arithmetic ?

I have no inside knowledge, but thinking about these remarkably enticing deals, I just wonder whether there was initial period showroom and demonstrator stocking at all the dealers, which kept Gaydon busy. If the retail sales were then slower than target, eventually the dealers become overstocked and don't order further stock from AML. That is the point at which it would impact Gaydon production.

What do you think ?

One PHer even described, 'No deposit and 24 monthly payments of £1,000' - as a no brainer for a £130,000 new car.

It’s pub talk

AMVSVNick said:

Thankyou4calling said:

No member of the public is putting £1000 down and £1000 a month for the car.

It’s pub talk

No it's not...It’s pub talk

)

)All the dealers have the offer, its not just Stratstone, and it's clearly keeping them busy running down the stock levels. For anyone interested AML do now publish wholesale volumes (what they sell to the dealers) and retail volumes (what the dealers sell to customers) on a quarterly basis.

There's two aspects to this deal that are unclear:

1. Who is taking the pain? My sense, from one or two conversations, is that its being shared between the dealers (one reason why some are not pushing it) and AML. But I don't know the mix

2. Why is it being done? Optically, AML records a sale in its P&L when it delivers the car to the dealer. So dealers being better equipped to reduce their stock levels doesn't, directly, benefit AML (its not as if it will boost AML sales in 19Q4 as I doubt dealers will be reloading on new stock so quickly). So it could be a) AML doing a favour to the dealers (as it helps the latter's cashflow) or b) AML wanting to make the Retail vs Wholesale numbers look more favourable come year end.

I personally think its more likely to be 'a'. AML and the dealers work on a "you scratch our back, we scratch yours basis". It may well be that AML felt the need to help the dealers out with their excess Vantage stock in order to ease the transition into the DBX (they will want dealers to have the space and cash available to take initial stock there). But I'd add this is purely speculation, I've not heard that directly from anyone.

Whichever way you look at it, it feels like a very good deal for a new customer (less good for anyone who's paid full whack in recent months)

I bought one on exactly this deal last week, have say I'm very impressed with the way it drives. What interests me is how AM are going to sell cars in the future when they do deals like this, I mean who would pay full price now? Its like going to Pizza Express without a voucher code.

Quarterly said:

I bought one on exactly this deal last week, have say I'm very impressed with the way it drives. What interests me is how AM are going to sell cars in the future when they do deals like this, I mean who would pay full price now? Its like going to Pizza Express without a voucher code.

1k down 1k/mo? That is genuinely amazing. Congrats!As Rob said........”Whichever way you look at it, it feels like a very good deal for a new customer (less good for anyone who's paid full whack in recent months)”

And there in lies a big part of the problem. We have said it before, but AML have got the pricing of the new Vantage wrong. Early adopting is rarely a good idea on any new product, especially one that is priced too highly. I’ve driven the new car and liked many aspects of it. However, the cost to change at the time was eye watering, and in my opinion, not worth it. So it’s easy to see why people now think that the lower pricing and the deals available may overcome some of the other issues. I was looking at the new F-Type today just out of curiosity. New build on their website, top spec AWD model with 575hp came in at £109k, with lots of options. I think it’s hard to justify a new Vantage at circa £30/40k on top of that. Anyway, we are all guilty of a bit of thread creep here......stock price -2% today, currently around 565p.....happy hunting!

Best Regards

Minglar

And there in lies a big part of the problem. We have said it before, but AML have got the pricing of the new Vantage wrong. Early adopting is rarely a good idea on any new product, especially one that is priced too highly. I’ve driven the new car and liked many aspects of it. However, the cost to change at the time was eye watering, and in my opinion, not worth it. So it’s easy to see why people now think that the lower pricing and the deals available may overcome some of the other issues. I was looking at the new F-Type today just out of curiosity. New build on their website, top spec AWD model with 575hp came in at £109k, with lots of options. I think it’s hard to justify a new Vantage at circa £30/40k on top of that. Anyway, we are all guilty of a bit of thread creep here......stock price -2% today, currently around 565p.....happy hunting!

Best Regards

Minglar

Quarterly said:

I bought one on exactly this deal last week, have say I'm very impressed with the way it drives. What interests me is how AM are going to sell cars in the future when they do deals like this, I mean who would pay full price now? Its like going to Pizza Express without a voucher code.

Put a link up to the deal and I’ll accept it’s true.

Gassing Station | Aston Martin | Top of Page | What's New | My Stuff