Insurance companies now refusing to quote for East London

Discussion

creampuff said:

I'm just back from a holiday in a developed, western country. It was quite refreshing just to be able to drive any car while I was there, because the car was already insured and any driver driving it is standard. Infact it's been standard in every country I've been to, except the UK.

You can buy that insurance here, but it’s expensive due to the legal framewthats in place in the U.K. few other countries have such a claimant biased legal culture.

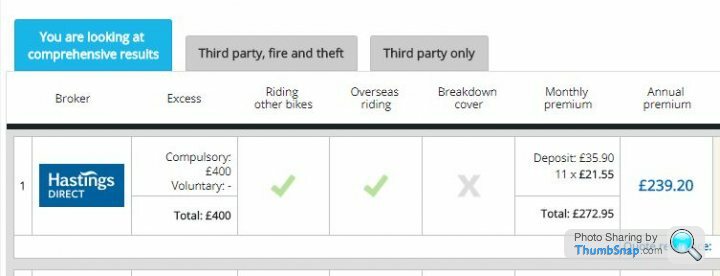

As a SW London resident I can recommend BeMoto. Their pricing has been very competitive for me and after mentioning the magic words 44Teeth a few extras were added FOC.

I've been speaking with them this week and they did mention that a couple of underwriters have now pulled out of the London/M25 area market

Best of luck with the renewal.

I've been speaking with them this week and they did mention that a couple of underwriters have now pulled out of the London/M25 area market

Best of luck with the renewal.

sjtscott said:

Some really really bad premiums there sorry to hear that

At least you have the MCE option too like myself even if its not an ideal choice.

I've always been of the opinion that an MCE policy is just a piece of paper that says "Certificate of Motor Insurance" on it, and that it makes you car appear on ASKMID. Serves no other purpose.At least you have the MCE option too like myself even if its not an ideal choice.

sjtscott said:

I posted to the new thread (about London insurance) but basically ended up having to go with MCE without any other realistic choice to keep it reasonable at just sub £400 FComp. The excess of £1k+ effectively makes it total loss/write off use only now.

I’ve mentioned insuring your excess before, but it seemed to pass everyone by. I’ll have another go. You can insure your excess with a few companies. This one covers up to £1000 for under £40 for the year. It will only cover one claim as the cover stops once the figure has been hit, but you can start another immediately if neededhttps://www.bestpricefs.co.uk/car-excess-insurance

I have no connection whatsoever to this company, other than I buy their legal expenses cover, as it covers all my vehicles at a lower cost than each insurer wants per vehicle.

cmaguire said:

anonymous said:

[redacted]

No, I'm suggesting that very occasional trips wouldn't constitute commuting in my book.Would you have the same attitude to a trackday ? I only do it once a year, on a nice day, I know I'm not covered but can you pay anyhow ??

Not sure any of us would get far ...

dibblecorse said:

No, but it would in the eyes of the insure, commuting is by definition travelling to and from work, makes no odd whether you did the journey once or one hundred times in the year, if thats what you were doing and didn't have the cover they don't need to pay out.

Would you have the same attitude to a trackday ? I only do it once a year, on a nice day, I know I'm not covered but can you pay anyhow ??

Not sure any of us would get far ...

.Would you have the same attitude to a trackday ? I only do it once a year, on a nice day, I know I'm not covered but can you pay anyhow ??

Not sure any of us would get far ...

Totally different scenario so a daft analogy.

A rare trip to work is probably less likely to end in tears than a rideout on a Sunday.

It's so low risk I wouldn't care a less. If you're pushing the technicality bit then if the worst happened on that very rare journey to work then I wouldn't admit to taking it to work if asked.

Then again I wouldn't be posting on here asking if it was alright to drive an untaxed vehicle for an MOT, or worry about whether it was OK to take a vehicle without an MOT for a test ride.

It didn't bother me 25 years ago and it isn't going to bother me now, whatever the Stasi say.

There are way too many people worried about trivial stuff these days.

So - for the simple of mind like myself - is it just the theft part of the insurance that’s putting the costs up/ resulting in refusals to cover?

So if the worst happens and I can’t find anyone to cover an ungaraged bike at a reasonable price, I could sell the nice(ish) bike, buy a cheapo one and insure 3rd party only cover if necessary?

So if the worst happens and I can’t find anyone to cover an ungaraged bike at a reasonable price, I could sell the nice(ish) bike, buy a cheapo one and insure 3rd party only cover if necessary?

anonymous said:

[redacted]

Thanks also for sharing the link Gavia will take a look, didn't pass me by just getting the main policy sorted first was the priority.Seriously went through the paperwork from MCE with a fine tooth comb so many things just not quite right but I have a recorded conversation explaining to me why the date I passed my UK license was some random date and couldn't be corrected. States no mods but I have them declared - explanation they only want to know about perf enhancing mods. Despite repeated attempts they still weren't listing the triumph factory key immobiliser I told them about but still listed it as 'unspecified' on security devices. I do have that finally showing correctly.

Suggest anyone double triple checks their MCE policy docs!!!

Edited by sjtscott on Saturday 27th January 02:00

The wording of the theft around the house has been around for quite a few years. It use to be a doubling of the excess, but as people abused the garage “Discount” and claimed to have one when they didn’t this is the insurers way of trying to eradicate that. A bike jacking would be an interesting test of it though.

I’m trying to recall the underwriter with that clause who started it RSA, or ERS spring to mind.

Declaring mods doesn’t make you an idiot. It’s personal choice and I personally wouldn’t, but you’re probably being more right than me.

I’m trying to recall the underwriter with that clause who started it RSA, or ERS spring to mind.

Declaring mods doesn’t make you an idiot. It’s personal choice and I personally wouldn’t, but you’re probably being more right than me.

I'm with principal and don't pay any premium on my mods, it's probably the map declaration that did for you. In my experience declaring the mods is usually free but in a claim they will only ever restore with OEM so it only ever works as a way for them to avoid paying out rather than protect any investment. With my Yamaha repair (non fault) I managed to swap the OEM exhaust for the akropovic paying the extra 25 quid difference to the garage.

anonymous said:

[redacted]

Thanks for the info however I'm sticking with MCE for now - principle were adamant without a garage and with commuting added + mods declared they couldn't get less than the circa £700 i.e. high 600s FComp they quoted me after I asked them to try better the £900 they first came back with. Its the map+can i.e. a perf enhancement which is whats doubled the premium not the can by itself I'd suggest. I'm always asked if I have any perf enhancing mods which I don't.

anonymous said:

[redacted]

I'm not sure how they'd ever tell it had been mapped unless your bike is new enough that a dealer would know this? The question MCE asked for comparison are any of your mods performance enhancing - no is the accurate response. They said they will cover any mods that don't enhance performance. They specifically called out turbos or superchargers lol But for non perm enhancing mods will only replace with manufacturer parts in the event of a claim - had that statement from other insurers too.

Gassing Station | Biker Banter | Top of Page | What's New | My Stuff