Does my Vanguard need tidying up?

Discussion

forest172 said:

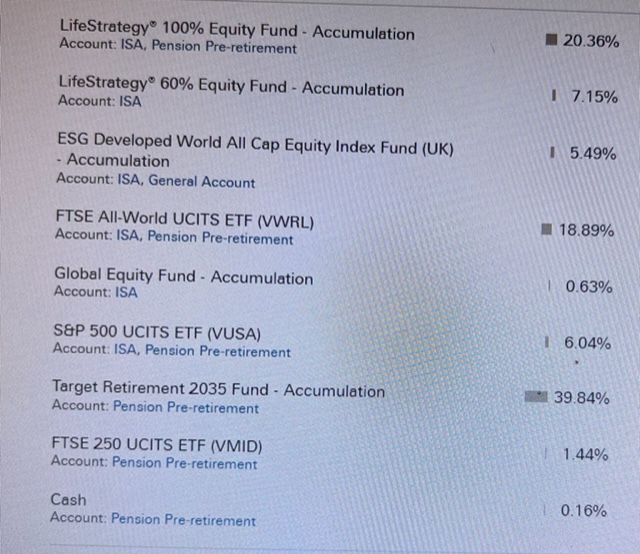

Here are my investments and I feel it`s messy. But does it matter? Would you guys switch them and keep them more simple?

Just stating the obvious- you might want to see what the glide path for Target dated 2035 is. The very small holdings, personally don't see the point. What matters really is your risk profile/appetite for a bit of risk. Most of your holdings are Funds of funds/trackers so there will be plenty of overlap. The LS 100 may be at odds with your LF 60. It's a personal preference. I see the US outperforming the UK by some margin.

Whether you "need" to tidy it up is debatable but I looking at the list I don't get what the plan is so that might be useful.

LifeStrategy suggests you've thought about risk.

Target Retirement suggests you've thought about the date you need the funds for.

VWRL suggests you've thought about broad global exposure.

Then the remnants all look very random and there look to be different accounts (ISA, pension pre-retirement etc.)

LifeStrategy suggests you've thought about risk.

Target Retirement suggests you've thought about the date you need the funds for.

VWRL suggests you've thought about broad global exposure.

Then the remnants all look very random and there look to be different accounts (ISA, pension pre-retirement etc.)

forest172 said:

ok, I`m ok with risk.

So more US weighted how would you correct this? Happy to swap 2035 out to something else. Obviously I`d do it slowly and a bit at a time because I`ve seen brilliant gains again recently

Any Global index will naturally be tilted towards the US given their companies comprise 65-70% of the entire pools. Some trackers exclude the UK (6%?). LF 60 is more an income fund-something you would look at in retirement and I would wager than Vanguards strategy for TD 2035 would plonk assets into this sort of profile at 3-5 years out. You might be seeking more capital growth this far out? It's your callSo more US weighted how would you correct this? Happy to swap 2035 out to something else. Obviously I`d do it slowly and a bit at a time because I`ve seen brilliant gains again recently

Edited by forest172 on Saturday 13th August 11:32

b hstewie said:

hstewie said:

hstewie said: Whether you "need" to tidy it up is debatable but I looking at the list I don't get what the plan is so that might be useful.

LifeStrategy suggests you've thought about risk.

Target Retirement suggests you've thought about the date you need the funds for.

VWRL suggests you've thought about broad global exposure.

Then the remnants all look very random and there look to be different accounts (ISA, pension pre-retirement etc.)

I treat it all as pension really inc. the ISA. I`m 46LifeStrategy suggests you've thought about risk.

Target Retirement suggests you've thought about the date you need the funds for.

VWRL suggests you've thought about broad global exposure.

Then the remnants all look very random and there look to be different accounts (ISA, pension pre-retirement etc.)

Suppose I just looked at some other funds when I put cash in and decided it`d be good to see how they do.

Without hijacking, I have a vanguard cash isa, predominantly in vls60. Having used it to get exposure to equities my perception of risk has changed (I am 31, so plenty of years to allow the investment to grow). Is it possible to transfer this over to a vls80 or do I have to sell out then buy back in as it were - would this affect my annual isa allowance?

bhstewie said:

hstewie said: Whether you "need" to tidy it up is debatable but I looking at the list I don't get what the plan is.

Agreed.Job 1 - Identify what you're trying to achieve.

Job 2 - Decide whether the portfolio is right for that and, if not, adjust to suit.

Or if you simply want fewer holdings that achieve that target the same objective, adjust to suit.

bmwmike said:

VWRL is an income tracker. I can't find an equivalent accumulator priced in GBP anyone know one? Needs to be an ETF as they are cheaper to hold for me

I believe 'VWRP' is the acc version of VWRL however only available on certain platforms e.g: it's on AJBELL but Vanguard UK don't offer it on their platform. Personally I hold VEVE on AJBELL for a cheap Dev world Global Equities ETF and FTSE Global All CAP fund on Vanguard.Edit: doh, just realised you asked for a 'Gbp' priced tracker, VWRP is USD so disregard

Edited by VR99 on Saturday 13th August 18:13

Edited by VR99 on Saturday 13th August 19:49

Gassing Station | Finance | Top of Page | What's New | My Stuff