Base Rate Forecast

Discussion

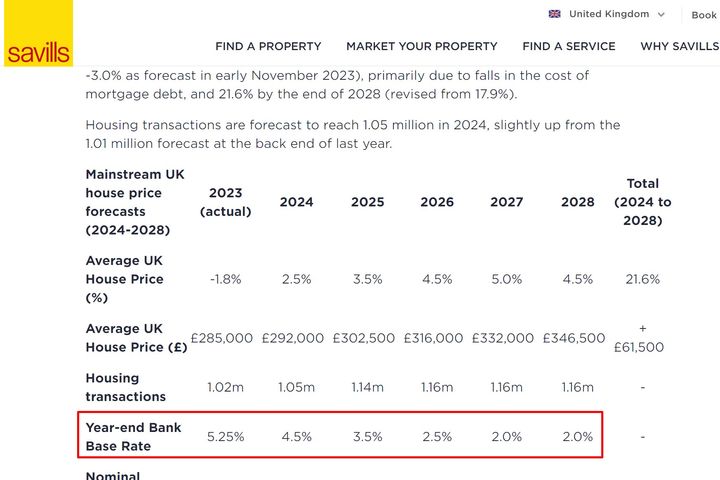

The below base rate forecast is from Savills.

I need to remortage from a 5 year fixed that is ending this year so not sure whether to go fixed or variable. The former gives certainty. The latter (if the forecasts below are to be believed) will save money. But with Labour in power who knows what catastrophes the economy could face with the BoE then stepping in... much as they did when the Tories were in power under Liz Truss!

What would you do? ....

I need to remortage from a 5 year fixed that is ending this year so not sure whether to go fixed or variable. The former gives certainty. The latter (if the forecasts below are to be believed) will save money. But with Labour in power who knows what catastrophes the economy could face with the BoE then stepping in... much as they did when the Tories were in power under Liz Truss!

What would you do? ....

The BoE isn't going to cut the base rate unless there's a reason to.

It's the one big tool in their toolbox that they can whip out when the s t hits the fan (see COVID, the 2008 crash, etc).

t hits the fan (see COVID, the 2008 crash, etc).

No way are they going to undermine their own ability to react to shocks by letting the base rate drift down like that.

Base rate of less than 4 or 5% isn't normal. That's abnormal and an emergency condition.

It's the one big tool in their toolbox that they can whip out when the s

t hits the fan (see COVID, the 2008 crash, etc).No way are they going to undermine their own ability to react to shocks by letting the base rate drift down like that.

Base rate of less than 4 or 5% isn't normal. That's abnormal and an emergency condition.

I work within the analytics industry and have designed a number of forecasting programs for very large multi-nationals. They are a useful tool for some things but I wouldn't bet my own money on the accuracy of a base rate forecast being pedalled by an estate agency with a vested interest in painting a rosy picture of the future.

I could go into all of the reasons that their forecast will be complete tripe but the long and short of it is, it's a gamble on whether or not you should fix your mortgage and you should do whatever suits your appetite for risk. They might go down (and probably will see a modest decline in the "short term") but could just as easily go up in the next 5 years. Liz Truss, Russia, Covid etc etc were all *fairly* unpredictable and any other black swan event could easily happen at any time.

I could go into all of the reasons that their forecast will be complete tripe but the long and short of it is, it's a gamble on whether or not you should fix your mortgage and you should do whatever suits your appetite for risk. They might go down (and probably will see a modest decline in the "short term") but could just as easily go up in the next 5 years. Liz Truss, Russia, Covid etc etc were all *fairly* unpredictable and any other black swan event could easily happen at any time.

currently in the same position, do I fix for five years at 4.88% or 2 years at 5.48%? The difference in monthly payments is about £75 a month

I currently overpay by 10% a year, so I am tempted by the 5 year fix and pay off 20% at the lower rate. Rates would need to fall by a decent amount after two years to make it more cost effective to remortgage at a (hopefully) lower rate after 2 years and take the pain of the higher rate for the first two years.

I change my mind from day to day, whatever happens it will be wrong though.

I am going to renew with the same provider and can do it online. I have until September to decide, current thinking is if rates fall next week and the mortgage rate goes down, lock in a five year deal at (hopefully) 4.63% (assuming rates fall 0.25%)

I currently overpay by 10% a year, so I am tempted by the 5 year fix and pay off 20% at the lower rate. Rates would need to fall by a decent amount after two years to make it more cost effective to remortgage at a (hopefully) lower rate after 2 years and take the pain of the higher rate for the first two years.

I change my mind from day to day, whatever happens it will be wrong though.

I am going to renew with the same provider and can do it online. I have until September to decide, current thinking is if rates fall next week and the mortgage rate goes down, lock in a five year deal at (hopefully) 4.63% (assuming rates fall 0.25%)

As far as I can see the world and his Mum have been predicting interest rate cuts since the first rise the other year. Yes it may have happened a tiny bit in Europe but I see that heading back up soon. At best you will get a token 0.25% before Christmas, but don't see any more than that over the next 5 years or so, as historically it has always been around 5 or 6%.

LowTread said:

The BoE isn't going to cut the base rate unless there's a reason to.

It's the one big tool in their toolbox that they can whip out when the st hits the fan (see COVID, the 2008 crash, etc).

No way are they going to undermine their own ability to react to shocks by letting the base rate drift down like that.

Base rate of less than 4 or 5% isn't normal. That's abnormal and an emergency condition.

I tend to agree. There seems to be a pretty widespread belief that the BoE will reduce base rates down just because that's where they were before...but if the BoE's remit is to keep inflation at or around 2%, and it is at or around 2% when base rates are at 5-ish%, which looks to be a plausible scenario, then why would they cut them much? I'd also be very sceptical about a forward base rate projection from an estate agent, who would very much like people to think 'That £500k house looks a bit pricey at 5% rates, but they'll be back to 2% in a few years so it'll be alright if I buy it now'. I'm sure I'll be corrected if I've got this wrong, but I'm pretty sure gilt forward curves don't suggest that a fall back to 2% base rates is likely in the next five years? It's the one big tool in their toolbox that they can whip out when the s

t hits the fan (see COVID, the 2008 crash, etc).No way are they going to undermine their own ability to react to shocks by letting the base rate drift down like that.

Base rate of less than 4 or 5% isn't normal. That's abnormal and an emergency condition.

ARHarh said:

As far as I can see the world and his Mum have been predicting interest rate cuts since the first rise the other year. Yes it may have happened a tiny bit in Europe but I see that heading back up soon. At best you will get a token 0.25% before Christmas, but don't see any more than that over the next 5 years or so, as historically it has always been around 5 or 6%.

Hmm, I think something will break and force rate cuts. By design, of course. I’ll be rolling the dice in October and taking a tracker. Just as people are saying that we shouldn’t expect rates much below 5% because of historical precedent, precedent exists for very low long term interest rates- see Japan. Post-industrial island nation, aging spendthrift population, disenfranchised navel-gazing youth who aren’t having enough children, high utility and commodity prices, shortage of affordable property, lifetime mortgages etc etc…

Japanification is a thing, and a warning of what happens if you don’t have enough people to support the retired.

Japanification is a thing, and a warning of what happens if you don’t have enough people to support the retired.

Edited by Hustle_ on Tuesday 11th June 15:13

Sarnie said:

People shouldn't follow financial advice given by an Estate Agent.

Couldn't have said it better. Very difficult to predict interest rates in 12 months time, let alone 5 years. Far too many assumptions, which make the outcome quite unreliable.

If it was me, I'd go for a 2 year variable/tracker.

esuuv said:

An estate agent predicting long term low interest rates.........and people actually take notice of it........seriously?

The source is Oxford Economics - https://www.oxfordeconomics.com/service-category/r...What source would you suggest?

Some really good helpful comments above many thanks (shame PH always attracts some sarky unhelpful types).

The consensus seems to be that rates might drop a small amount over the next year or so but don't expect much. So a 5 year fix would probably suit me based on that and my risk aversion.

Thanks again all.

The consensus seems to be that rates might drop a small amount over the next year or so but don't expect much. So a 5 year fix would probably suit me based on that and my risk aversion.

Thanks again all.

Gassing Station | Finance | Top of Page | What's New | My Stuff