How do I pay Tax on interest

Discussion

This is going to be very new to me so be gentle !

I’ve stuck a decent amount into NS&I bonds a few weeks ago ( joint account ) and have a few other bits scattered around in various accounts.

When will I have to declare the interest to HMRC is it next April ?

I also intend to stop working beginning of March I’m guessing this will complicate things ?

Would I be best to just spend a couple of hundred quid at least in this first year when I’m working then not working with an accountant to sort it for me ?

I’ve stuck a decent amount into NS&I bonds a few weeks ago ( joint account ) and have a few other bits scattered around in various accounts.

When will I have to declare the interest to HMRC is it next April ?

I also intend to stop working beginning of March I’m guessing this will complicate things ?

Would I be best to just spend a couple of hundred quid at least in this first year when I’m working then not working with an accountant to sort it for me ?

stuthemongoose said:

You’d have to do a self assessment for the tax year Apr 2024 to Apr 2025, which would need to be filed by end Jan 2025.

You have, IIRC, up to 2k you don’t need to declare, but you’ll need a Self assessment if over that!

The filing deadline for the 2024/25 Self Assessment tax returns is 31 January 2026.You have, IIRC, up to 2k you don’t need to declare, but you’ll need a Self assessment if over that!

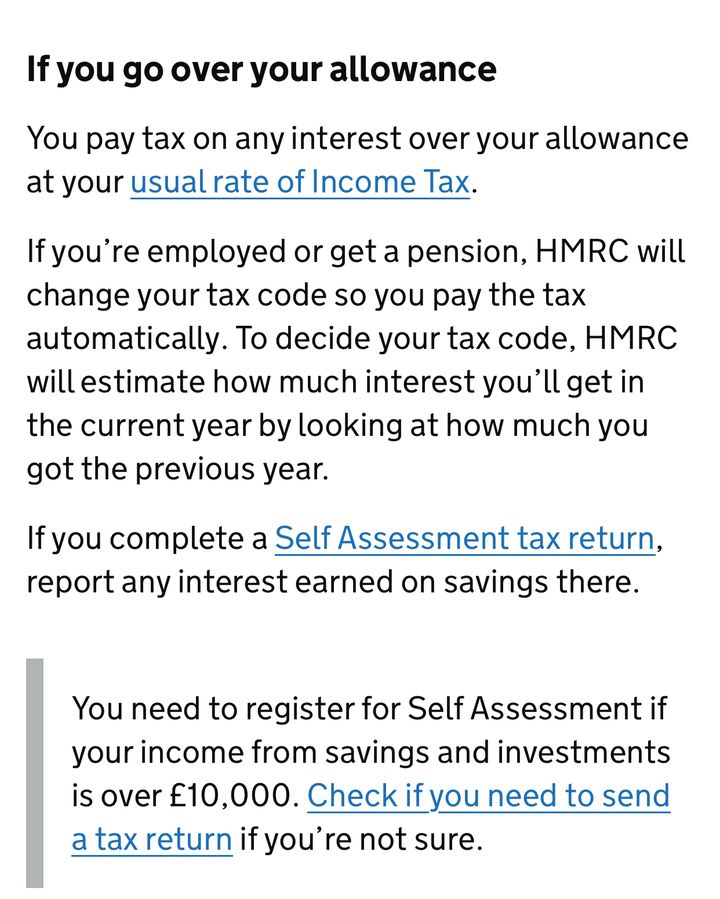

If person pays tax under PAYE, HMRC MAY alter your tax coding to try and collect any additional tax payable on interest. However, do not assume that they will do this as they don’t always make the right connection between information they receive from third parties and the actual tax payer.

If you fail to pay the tax on the interest, it will always be your fault.

Eric Mc said:

The filing deadline for the 2024/25 Self Assessment tax returns is 31 January 2026.

If person pays tax under PAYE, HMRC MAY alter your tax coding to try and collect any additional tax payable on interest. However, do not assume that they will do this as they don’t always make the right connection between information they receive from third parties and the actual tax payer.

If you fail to pay the tax on the interest, it will always be your fault.

As the OP says it's a joint account I guess he's going to have to declare for both him and his wife if he wants to split the tax.If person pays tax under PAYE, HMRC MAY alter your tax coding to try and collect any additional tax payable on interest. However, do not assume that they will do this as they don’t always make the right connection between information they receive from third parties and the actual tax payer.

If you fail to pay the tax on the interest, it will always be your fault.

When and why did they make the change from deducting basic rate tax at source to paying the interest gross?

I appreciate that we now get a £1k tax free allowance, but it was so much simpler for a basic rate taxpayer under the old system.

I have quite a few small sums in savings accounts, making use of the higher rates paid on "regular saver" accounts, plus 3 current accounts and an ISA. Total savings around £30k.

It's a real pain getting all the figures together for self assessment.

No tax due last year, but not that far off.

I appreciate that we now get a £1k tax free allowance, but it was so much simpler for a basic rate taxpayer under the old system.

I have quite a few small sums in savings accounts, making use of the higher rates paid on "regular saver" accounts, plus 3 current accounts and an ISA. Total savings around £30k.

It's a real pain getting all the figures together for self assessment.

No tax due last year, but not that far off.

clockworks said:

When and why did they make the change from deducting basic rate tax at source to paying the interest gross?

I appreciate that we now get a £1k tax free allowance, but it was so much simpler for a basic rate taxpayer under the old system.

I have quite a few small sums in savings accounts, making use of the higher rates paid on "regular saver" accounts, plus 3 current accounts and an ISA. Total savings around £30k.

It's a real pain getting all the figures together for self assessment.

No tax due last year, but not that far off.

Because the vast majority of people don’t need to pay it any more, it’s far better not to tax the earned interest, and let the minority declare it on an annual return. I appreciate that we now get a £1k tax free allowance, but it was so much simpler for a basic rate taxpayer under the old system.

I have quite a few small sums in savings accounts, making use of the higher rates paid on "regular saver" accounts, plus 3 current accounts and an ISA. Total savings around £30k.

It's a real pain getting all the figures together for self assessment.

No tax due last year, but not that far off.

Narcisus said:

I’ve stuck a decent amount into NS&I bonds a few weeks ago ( joint account ) and have a few other bits scattered around in various accounts.

Re. the NS&I bonds, it depends on what type they are, as iirc some just pay interest at maturity, so for those you'd only have to declare the interest for the tax year in which they mature e.g. if you bought a 3 year bond that only paid interest at maturity in tax year 2027-28, then you'd only have to declare the interest in that tax year.When you know you are going to go over your tax free interest allowance for a particular tax year, tell HMRC. It is quite likely that they will not put you on self-assessment i.e. completing a tax return, but will collect the interest information directly from the banks themselves and calculate the tax for you in the autumn following the end of the tax year. This can be a good and a bad thing - good as they do the work, bad if they get the numbers wrong as they have in my case

trevalvole said:

Narcisus said:

I’ve stuck a decent amount into NS&I bonds a few weeks ago ( joint account ) and have a few other bits scattered around in various accounts.

Re. the NS&I bonds, it depends on what type they are, as iirc some just pay interest at maturity, so for those you'd only have to declare the interest for the tax year in which they mature e.g. if you bought a 3 year bond that only paid interest at maturity in tax year 2027-28, then you'd only have to declare the interest in that tax year.When you know you are going to go over your tax free interest allowance for a particular tax year, tell HMRC. It is quite likely that they will not put you on self-assessment i.e. completing a tax return, but will collect the interest information directly from the banks themselves and calculate the tax for you in the autumn following the end of the tax year. This can be a good and a bad thing - good as they do the work, bad if they get the numbers wrong as they have in my case

trevalvole said:

Re. the NS&I bonds, it depends on what type they are, as iirc some just pay interest at maturity, so for those you'd only have to declare the interest for the tax year in which they mature e.g. if you bought a 3 year bond that only paid interest at maturity in tax year 2027-28, then you'd only have to declare the interest in that tax year.

When you know you are going to go over your tax free interest allowance for a particular tax year, tell HMRC. It is quite likely that they will not put you on self-assessment i.e. completing a tax return, but will collect the interest information directly from the banks themselves and calculate the tax for you in the autumn following the end of the tax year. This can be a good and a bad thing - good as they do the work, bad if they get the numbers wrong as they have in my case

HMRC currently has no mechanism for collecting tax on interest directly from banks and building societies. The old "basic rate tax deduction at source" system was closed around ten years ago.When you know you are going to go over your tax free interest allowance for a particular tax year, tell HMRC. It is quite likely that they will not put you on self-assessment i.e. completing a tax return, but will collect the interest information directly from the banks themselves and calculate the tax for you in the autumn following the end of the tax year. This can be a good and a bad thing - good as they do the work, bad if they get the numbers wrong as they have in my case

They may need to bring it back but at the moment it's not an option.

Eric Mc said:

HMRC currently has no mechanism for collecting tax on interest directly from banks and building societies. The old "basic rate tax deduction at source" system was closed around ten years ago.

They may need to bring it back but at the moment it's not an option.

How much are your mates rates Eric ? They may need to bring it back but at the moment it's not an option.

Will you be taking a pension when you stop working or doing some other paid work?

If so the “horse’s mouth” says they’ll just claw back tax owed via your tax code…

https://www.gov.uk/apply-tax-free-interest-on-savi...

If so the “horse’s mouth” says they’ll just claw back tax owed via your tax code…

https://www.gov.uk/apply-tax-free-interest-on-savi...

The problem with "clawing back tax" through tax codes is that HMRC tend to claw back LAST YEAR'S tax in THIS YEAR's tax code. That's because the third party (in this case the banks) can only provide the necessary interest information to HMRC AFTER the tax year has ended. So you will always be a year behind with paying the tax on the interest you earned.

HMRC sometimes GUESS what the interest in the current tax year is - in which case they will guess wrongly and you will, by default, pay tax on the wrong amount of interest. HMRC then try to correct matters by fiddling with yoir tax code. As a result, people will be getting multiple tax codes in any given tax year as HMRC TRY to gets it right (which they won't).

Playing catch-up by adjusting tax codes can get very messy.

HMRC sometimes GUESS what the interest in the current tax year is - in which case they will guess wrongly and you will, by default, pay tax on the wrong amount of interest. HMRC then try to correct matters by fiddling with yoir tax code. As a result, people will be getting multiple tax codes in any given tax year as HMRC TRY to gets it right (which they won't).

Playing catch-up by adjusting tax codes can get very messy.

Eric Mc said:

HMRC currently has no mechanism for collecting tax on interest directly from banks and building societies. The old "basic rate tax deduction at source" system was closed around ten years ago.

They may need to bring it back but at the moment it's not an option.

Why was that system removed?They may need to bring it back but at the moment it's not an option.

The Chancellor introduced a new additional tax allowance of £1,000 specifically to cover interest earned in bank and building society accounts. Prior to this, interest did not have any specific allowance allocated to it. The only allowance a peson got was their normal Personal Tax Allowance which covers their overall income from all sources.

As interest rates were very low, even people with large deposits were earning low amounts of interest and were not exceeding this interest allowance.

The banks took the opportunity to stop deducting tax at source as it was an administrative hassle ( and cost - of course) for them.

In the last couple of years, interest rates have risen and even modest savings are generating more than £1,000 in annual interest - so many more people suddenly are finding that they need to pay tax on that interest.

As interest rates were very low, even people with large deposits were earning low amounts of interest and were not exceeding this interest allowance.

The banks took the opportunity to stop deducting tax at source as it was an administrative hassle ( and cost - of course) for them.

In the last couple of years, interest rates have risen and even modest savings are generating more than £1,000 in annual interest - so many more people suddenly are finding that they need to pay tax on that interest.

Edited by Eric Mc on Tuesday 17th September 08:19

Gassing Station | Finance | Top of Page | What's New | My Stuff