Medium Risk Regular Savings?

Discussion

I'm looking to save about £1,500 pcm but not really interested in 4% cash ISA type of investment. I'm not looking for high risk where I could lose it all so was wondering about some sort of (for example from position of ignorance) Vanguard ETF where they are managing the savings across a range of companies but really have no idea.

So I'd love 6%+ medium risk + not tied away for any period of time.

Any suggestions? Many thanks.

So I'd love 6%+ medium risk + not tied away for any period of time.

Any suggestions? Many thanks.

Scarletpimpofnel said:

I'm looking to save about £1,500 pcm but not really interested in 4% cash ISA type of investment. I'm not looking for high risk where I could lose it all so was wondering about some sort of (for example from position of ignorance) Vanguard ETF where they are managing the savings across a range of companies but really have no idea.

So I'd love 6%+ medium risk + not tied away for any period of time.

Any suggestions? Many thanks.

Various providers have ranges of multi asset funds which are aligned to different levels of risk.So I'd love 6%+ medium risk + not tied away for any period of time.

Any suggestions? Many thanks.

The likes of AJ Bell, Blackrock, Barclays Wealth, L&G, Royal London, Columbia Threadneedle etc etc have ranges that typically go;

Cautious - Conservative - Balanced - Moderately Adventurous - Adventurous.

You probably want a balanced fund (aligning with your medium risk), and may consider spreading your risk across a couple.

Scarletpimpofnel said:

So I'd love 6%+ medium risk + not tied away for any period of time.

Medium risk to me says you could still be down 10% at any given point if the markets spook. It’s a really strange time at the moment with very high valuations and a loose cannon us president.I mention this because you say not tied away for any period of time. While you can withdraw a medium risk investment at any time you should really be thinking if you need it within 5 years. If so or you don’t think you could stomach being notionally down 10% medium risk might not be for you.

Scarletpimpofnel said:

So I'd love 6%+ medium risk + not tied away for any period of time.

Yes that would be rather nice

In addition to the above which is all sensible stuff remember investments are not the same as investments they will go down as well as up.

These are ranges so worst case to best case but perhaps have a look at this and see what you think your appetite and tolerance for loss might be.

b hstewie said:

hstewie said:

hstewie said: Yes that would be rather nice

In addition to the above which is all sensible stuff remember investments are not the same as investments they will go down as well as up.

These are ranges so worst case to best case but perhaps have a look at this and see what you think your appetite and tolerance for loss might be.

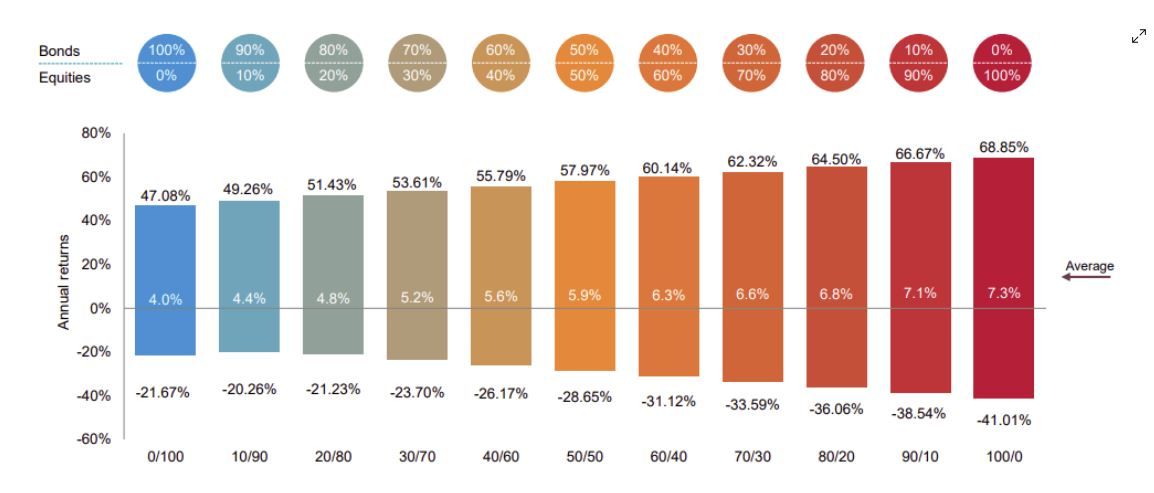

I'm not sure I understand that? Take the first column. It seems to suggest that 100% bonds only could give a 40%+gain or a 20%+ loss? I thought bonds were a fixed return? Am I reading it right? Thanks.In addition to the above which is all sensible stuff remember investments are not the same as investments they will go down as well as up.

These are ranges so worst case to best case but perhaps have a look at this and see what you think your appetite and tolerance for loss might be.

Scarletpimpofnel said:

I'm not sure I understand that? Take the first column. It seems to suggest that 100% bonds only could give a 40%+gain or a 20%+ loss? I thought bonds were a fixed return? Am I reading it right? Thanks.

It's showing the historical range of returns you could get with a mix of investments from 100% bonds through to 100% stocks.So it's not that you should only see those returns it's highlighting the average return (the middle line) and the extremes that have been seen of both loss and gain.

Most people focus on the upside but if you've only ever saved money where your capital is 100% safe it can come as a bit of a shock when that an investments can lose money.

It's not intended to scare you it's intended to make you think about your appetite for volatility

colin79666 said:

If you are taking risk then it’s investing not saving.

& that is key.OP, you will only get around 4% if you are ‘saving’. NS&I bonds, cash ISAs, Premium Bonds.

Nothing wrong with that, & pretty important for your “emergency funds” budget.

Beyond that, you are investing.

You can always go for a “low risk” fund as described above.

Actually one of the best “reliable” investments we have is Kuflink - a P2P lending business

Weirdly, we only have a tiny sum invested - it is P2P & therefore technically quite high risk - but it has been rolling along nicely for several years - we ought to put more in it.

I see they have almost 400M invested & have had zero investor losses to date.

Scarletpimpofnel said:

I'm not sure I understand that? Take the first column. It seems to suggest that 100% bonds only could give a 40%+gain or a 20%+ loss? I thought bonds were a fixed return? Am I reading it right? Thanks.

You might be confusing savings bonds and investment bonds. Investment bonds are fixed interest but the value of the bond can go up and down. Sheepshanks said:

Scarletpimpofnel said:

I'm not sure I understand that? Take the first column. It seems to suggest that 100% bonds only could give a 40%+gain or a 20%+ loss? I thought bonds were a fixed return? Am I reading it right? Thanks.

You might be confusing savings bonds and investment bonds. Investment bonds are fixed interest but the value of the bond can go up and down. bhstewie said:

hstewie said: It's showing the historical range of returns you could get with a mix of investments from 100% bonds through to 100% stocks.

So it's not that you should only see those returns it's highlighting the average return (the middle line) and the extremes that have been seen of both loss and gain.

Most people focus on the upside but if you've only ever saved money where your capital is 100% safe it can come as a bit of a shock when that an investments can lose money.

It's not intended to scare you it's intended to make you think about your appetite for volatility

Ok thanks. I appreciate your effort in educating me.So it's not that you should only see those returns it's highlighting the average return (the middle line) and the extremes that have been seen of both loss and gain.

Most people focus on the upside but if you've only ever saved money where your capital is 100% safe it can come as a bit of a shock when that an investments can lose money.

It's not intended to scare you it's intended to make you think about your appetite for volatility

At one level the remarkably simple answer is to have,

50% Savings

50% Investments

or whatever % suits your mood.

Personally I consider "cash ISA" to be a waste of potentially bigger tax free returns, especially in a world where everyone is allowed a certain amount of tax free interest each year in any event (i.e. outside an ISA).

50% Savings

50% Investments

or whatever % suits your mood.

Personally I consider "cash ISA" to be a waste of potentially bigger tax free returns, especially in a world where everyone is allowed a certain amount of tax free interest each year in any event (i.e. outside an ISA).

Scarletpimpofnel said:

Ok thanks. I appreciate your effort in educating me.

If you want to do something simple and I think sensible, I think you'd do worse than look at opening an ISA and drop some money in something like Vanguard LifeStrategy 60 and get used to just seeing a small amount float up and down.The nice thing about what you're doing which is investing regularly and without an initial lump sum is you're not rocking up with £500K and a big decision to make.

There will be similar options that are cheaper there will be similar options that have given better returns and there will be be similar options that have given worse returns.

You can overthink to the Nth degree but it's simple and I think you should end up there or there about for a "balanced" risk profile.

Scarletpimpofnel said:

So I'd love 6%+ medium risk + not tied away for any period of time.

I'd suggest that the bit in bold re time period needs some consideration before switching from saving to investing. Anything involving equities should be a medium- to long-term commitment, really. If you know that you'll need access to your funds in a couple of years, then sticking to savings is probably going to be a less stressful experience.

As an illustration, Vanguard LS60 has been mentioned. It's an excellent fund if it suits your needs and risk appetite. However, as the attached five-year price graph shows, its value doesn't rise steadily and consistently over time.

C69 said:

I'd suggest that the bit in bold re time period needs some consideration before switching from saving to investing.

Anything involving equities should be a medium- to long-term commitment, really. If you know that you'll need access to your funds in a couple of years, then sticking to savings is probably going to be a less stressful experience.

As an illustration, Vanguard LS60 has been mentioned. It's an excellent fund if it suits your needs and risk appetite. However, as the attached five-year price graph shows, its value doesn't rise steadily and consistently over time.

Yes I take your point thanks. I need to think more about the bit in bold, realistically how long will I leave this saved up/invested for???Anything involving equities should be a medium- to long-term commitment, really. If you know that you'll need access to your funds in a couple of years, then sticking to savings is probably going to be a less stressful experience.

As an illustration, Vanguard LS60 has been mentioned. It's an excellent fund if it suits your needs and risk appetite. However, as the attached five-year price graph shows, its value doesn't rise steadily and consistently over time.

Scarletpimpofnel said:

Yes I take your point thanks. I need to think more about the bit in bold, realistically how long will I leave this saved up/invested for???

You can sell funds pretty much whenever you want.The thing to remember is that you may be selling at a loss and when you sell it can take a few days to clear to be "cash" you can withdraw - but the money isn't usually locked away.

Gassing Station | Finance | Top of Page | What's New | My Stuff