Taking NHS pension early

Discussion

Part of my pension is covered under the "95" pension, final salary based, best of previous 2 years. I can take it from 60 with no penalty, from 50 with penalties.

Rest of my pension is the 2017 pension, this will run from 2022 until I retire, (or take it early), can't take without penalties until government retirement age (67 for me).

I'm 50 this year and considering taking my 95 pension then, as a retire and return, so no drop in pay or hours.

Things to consider: -

Talk of retire and return being stopped.

For the last 11 months I've been on a higher band, likely this will drop from 01/04/25

The penalties for taking at 50 are only receiving 68.2% of pension and 84.5% of lump sum.

I would take max lump sum, invest bulk between myself and wife in ISA's, confident that would then exceed loss in 10 years (appreciate some risk)

For the loss in pension, if I add 10 years extra pension I make it 23 years from 60 before as a total amount paid I'm worse off.

Mortgage will be paid off in 7 years, won't touch that as below 2%

Also fair chance pension will rise at a better % than pay over next 10 years (not expecting / hoping for a promotion or significant pay rise).

Make sense to take now to those of you wiser than I?

Rest of my pension is the 2017 pension, this will run from 2022 until I retire, (or take it early), can't take without penalties until government retirement age (67 for me).

I'm 50 this year and considering taking my 95 pension then, as a retire and return, so no drop in pay or hours.

Things to consider: -

Talk of retire and return being stopped.

For the last 11 months I've been on a higher band, likely this will drop from 01/04/25

The penalties for taking at 50 are only receiving 68.2% of pension and 84.5% of lump sum.

I would take max lump sum, invest bulk between myself and wife in ISA's, confident that would then exceed loss in 10 years (appreciate some risk)

For the loss in pension, if I add 10 years extra pension I make it 23 years from 60 before as a total amount paid I'm worse off.

Mortgage will be paid off in 7 years, won't touch that as below 2%

Also fair chance pension will rise at a better % than pay over next 10 years (not expecting / hoping for a promotion or significant pay rise).

Make sense to take now to those of you wiser than I?

Your final salary for the 95 scheme will be best year of last 3 so you could wait a while longer rather than jump early. Going at 50 will be a big hit as you say, if you can stretch that to say 53?

You'll also be into some decent tax potentially with your pension plus part time earnings, that's the only downside I imagine.

Edit to add, I thought that 55 was the earliest you can take the 95 scheme unless special circumstances, might be worth checking that out.

You'll also be into some decent tax potentially with your pension plus part time earnings, that's the only downside I imagine.

Edit to add, I thought that 55 was the earliest you can take the 95 scheme unless special circumstances, might be worth checking that out.

Edited by 200Plus Club on Friday 7th March 11:46

200Plus Club said:

Your final salary for the 95 scheme will be best year of last 3 so you could wait a while longer rather than jump early. Going at 50 will be a big hit as you say, if you can stretch that to say 53?

You'll also be into some decent tax potentially with your pension plus part time earnings, that's the only downside I imagine.

Edit to add, I thought that 55 was the earliest you can take the 95 scheme unless special circumstances, might be worth checking that out.

Can retire at 50 if you joined the NHS 1995 PS before April 2006, thereafter early retirement from age 55yearsYou'll also be into some decent tax potentially with your pension plus part time earnings, that's the only downside I imagine.

Edit to add, I thought that 55 was the earliest you can take the 95 scheme unless special circumstances, might be worth checking that out.

Edited by 200Plus Club on Friday 7th March 11:46

The 95 scheme is based on best 12 months in the last 3 years, so you can wait a couple of years and save a few percent of reduction.

With regards the reduction by taking the 95 early; the overall amount you get is the same as if you stayed to 60 but your getting it for longer. I cant remember what age post 60 it balances out - something like 80??

You can continue to build 2015 pension if tou retire and return or partially retire.

Be aware that receiving pension and your existing salary may push you into another tax zone. Of course you could reduce your hours and improve your work/life balance whilst not impacting your income.

I did this a few years ago at 53. So four day week and increased income but building a a bit more pension for when i stop work altogether

With regards the reduction by taking the 95 early; the overall amount you get is the same as if you stayed to 60 but your getting it for longer. I cant remember what age post 60 it balances out - something like 80??

You can continue to build 2015 pension if tou retire and return or partially retire.

Be aware that receiving pension and your existing salary may push you into another tax zone. Of course you could reduce your hours and improve your work/life balance whilst not impacting your income.

I did this a few years ago at 53. So four day week and increased income but building a a bit more pension for when i stop work altogether

Edited by sawman on Saturday 8th March 08:54

Edited by sawman on Saturday 8th March 09:16

sawman said:

The 95 scheme is based on best 12 months in the last 3 years, so you can wait a couple of years and save a few percent of reduction.

With regards the reduction by taking the 95 early; the overall amount you get is the same as if you stayed to 60 but your getting it for longer. I cant remember what age post 60 it balances out - something like 80??

You can continue to build 2015 pension if tou retire and return or partially retire.

Be aware that receiving pension and your existing salary may push you into another tax zone. Of course you could reduce your hours and improve your work/life balance whilst not impacting your income.

I did this a few years ago at 53. So four day week and increased income but building a a bit more pension for when i stop work altogether

]

This is my plan and most people I know like me. Do the maths with quotes from NHS BSA at aged 54 and/or 56 and or 58.With regards the reduction by taking the 95 early; the overall amount you get is the same as if you stayed to 60 but your getting it for longer. I cant remember what age post 60 it balances out - something like 80??

You can continue to build 2015 pension if tou retire and return or partially retire.

Be aware that receiving pension and your existing salary may push you into another tax zone. Of course you could reduce your hours and improve your work/life balance whilst not impacting your income.

I did this a few years ago at 53. So four day week and increased income but building a a bit more pension for when i stop work altogether

]

Plan to fully exit before 60.

The trouble is, the whole workforce is so f

ked off, everyone over 50 is actively planning to leave.

ked off, everyone over 50 is actively planning to leave.Imaginethe largest employer in the world, losing all it's most experienced and productive 50 yr olds, all the GPs, all the senior medics etc, leaving up to a decade early.

At aged 51 (ish) you are the most efficient, productive and valuable to the NHS.

Work to 67..... forget about it. The environment is a meat grinder now.

A total disaster.

The_Doc said:

This is my plan and most people I know like me. Do the maths with quotes from NHS BSA at aged 54 and/or 56 and or 58.

Plan to fully exit before 60.

The trouble is, the whole workforce is so fked off, everyone over 50 is actively planning to leave.

Imaginethe largest employer in the world, losing all it's most experienced and productive 50 yr olds, all the GPs, all the senior medics etc, leaving up to a decade early.

At aged 51 (ish) you are the most efficient, productive and valuable to the NHS.

Work to 67..... forget about it. The environment is a meat grinder now.

A total disaster.

Completely agree, and thats before you consider the farce that faces the foundation docs looking at taking jobs in starbucks because they cant get a training post… probably fodder for another thread in NP&EPlan to fully exit before 60.

The trouble is, the whole workforce is so f

ked off, everyone over 50 is actively planning to leave.Imaginethe largest employer in the world, losing all it's most experienced and productive 50 yr olds, all the GPs, all the senior medics etc, leaving up to a decade early.

At aged 51 (ish) you are the most efficient, productive and valuable to the NHS.

Work to 67..... forget about it. The environment is a meat grinder now.

A total disaster.

CoolHands said:

Don’t know about nhs but pls check as with teacherspensions if you take the FS pension early you must also take the career average pension you’ve built up so far at the same time ie early and is reduced by greater amount as its early from 67 rather than early from 60 like the FS

Good point - probably needs fact checking, but my understanding is that you can't take the 2015 more than 13 years before your NPA - so 54 for most folks. but if you retire and return you can still contribute to 2015 on your return to workAlso if you havent taken 95 benefits by age 60 you are loosing cash, as it its not backdated

CoolHands said:

Don’t know about nhs but pls check as with teacherspensions if you take the FS pension early you must also take the career average pension you’ve built up so far at the same time ie early and is reduced by greater amount as its early from 67 rather than early from 60 like the FS

Totally different schemes and the career average can be frozen till 67. Interesting thread

How do you find out the % drop of taking the pension early ie at 50?

Assuming from other comments you can ‘leave’ or still grow the career average pension until 68 (in my case) or take 10 years early with a % reduction

For context I started in 2003, I’m a Band 9 A4C will be top of band in 2027 so unless I move to a VSM post I’ve maxed out my pay (with significant graft and stress along the way) and I’m 45. So would be 50 in 2030 with the last 3 years at max earnings (so 12mths of the last 3 easily covered)

Applying your percentages I would be happily retired at 50 on that income and then start doing short term contracts to up my salary to current levels. But I don’t need that income, I could easily survive on the lower % pension, as I will be mortgage free by then also.

Interesting prospect and as another poster said, why we are in such crisis as the over 50 workforce just disappears or moves to agency/short term work

How do you find out the % drop of taking the pension early ie at 50?

Assuming from other comments you can ‘leave’ or still grow the career average pension until 68 (in my case) or take 10 years early with a % reduction

For context I started in 2003, I’m a Band 9 A4C will be top of band in 2027 so unless I move to a VSM post I’ve maxed out my pay (with significant graft and stress along the way) and I’m 45. So would be 50 in 2030 with the last 3 years at max earnings (so 12mths of the last 3 easily covered)

Applying your percentages I would be happily retired at 50 on that income and then start doing short term contracts to up my salary to current levels. But I don’t need that income, I could easily survive on the lower % pension, as I will be mortgage free by then also.

Interesting prospect and as another poster said, why we are in such crisis as the over 50 workforce just disappears or moves to agency/short term work

Dadof2 said:

Interesting thread

How do you find out the % drop of taking the pension early ie at 50?

Assuming from other comments you can ‘leave’ or still grow the career average pension until 68 (in my case) or take 10 years early with a % reduction

For context I started in 2003, I’m a Band 9 A4C will be top of band in 2027 so unless I move to a VSM post I’ve maxed out my pay (with significant graft and stress along the way) and I’m 45. So would be 50 in 2030 with the last 3 years at max earnings (so 12mths of the last 3 easily covered)

Applying your percentages I would be happily retired at 50 on that income and then start doing short term contracts to up my salary to current levels. But I don’t need that income, I could easily survive on the lower % pension, as I will be mortgage free by then also.

Interesting prospect and as another poster said, why we are in such crisis as the over 50 workforce just disappears or moves to agency/short term work

read this leaflet - should have all the details: https://www.nhsbsa.nhs.uk/sites/default/files/2019...How do you find out the % drop of taking the pension early ie at 50?

Assuming from other comments you can ‘leave’ or still grow the career average pension until 68 (in my case) or take 10 years early with a % reduction

For context I started in 2003, I’m a Band 9 A4C will be top of band in 2027 so unless I move to a VSM post I’ve maxed out my pay (with significant graft and stress along the way) and I’m 45. So would be 50 in 2030 with the last 3 years at max earnings (so 12mths of the last 3 easily covered)

Applying your percentages I would be happily retired at 50 on that income and then start doing short term contracts to up my salary to current levels. But I don’t need that income, I could easily survive on the lower % pension, as I will be mortgage free by then also.

Interesting prospect and as another poster said, why we are in such crisis as the over 50 workforce just disappears or moves to agency/short term work

The other motivating factory for me is that I’ve only just got away with not paying tax on the value of my pension (contributions and growth) being above the annual limit, as the limit has gone up. Any revision to this figure (downwards) would bring me into paying more income tax. Or even if static at £60k it might mean I hit that before I’m 60 (I imagine so), so taking it at 50 and 58 for the average scheme and contracting for those 8 years for a few months a year would seem like the best approach

Interesting, will still have to think about the maths of swapping my 996 for a 458 Spider in all of this of course 🤭

Interesting, will still have to think about the maths of swapping my 996 for a 458 Spider in all of this of course 🤭

The_Doc said:

The trouble is, the whole workforce is so fked off, everyone over 50 is actively planning to leave

Bit of an exaggeration ked off, everyone over 50 is actively planning to leave

Only those who can afford it will leave in their 50s and realistically that’s only going to be those at or near the top of the NHS.

Totally agree that includes Consultants, GPs and the like though.

I’m 8B and can’t afford to go before 60, unless inheritance comes my way. By that point I’d have 36 years pension contributions.

The_Doc said:

Yeah, good point.

I'll rephrase, all the doctors that can, are planning to leave..

Literally all my friends that are doctors and qualified in the 90s are taking to their advisors and such

What would it take to keep you? Genuine question.I'll rephrase, all the doctors that can, are planning to leave.

. Literally all my friends that are doctors and qualified in the 90s are taking to their advisors and such

My wife works in the NHS and will be retired by 50 if she can and I know some of the answers. But what would it take to keep you?

I'm a realist and I realise some are quitting because they can. Many others will have to keep on chugging on and I'm sure you're the same as her and don't like just walking.

The_Doc said:

Literally all my friends that are doctors and qualified in the 90s are taking to their advisors and such

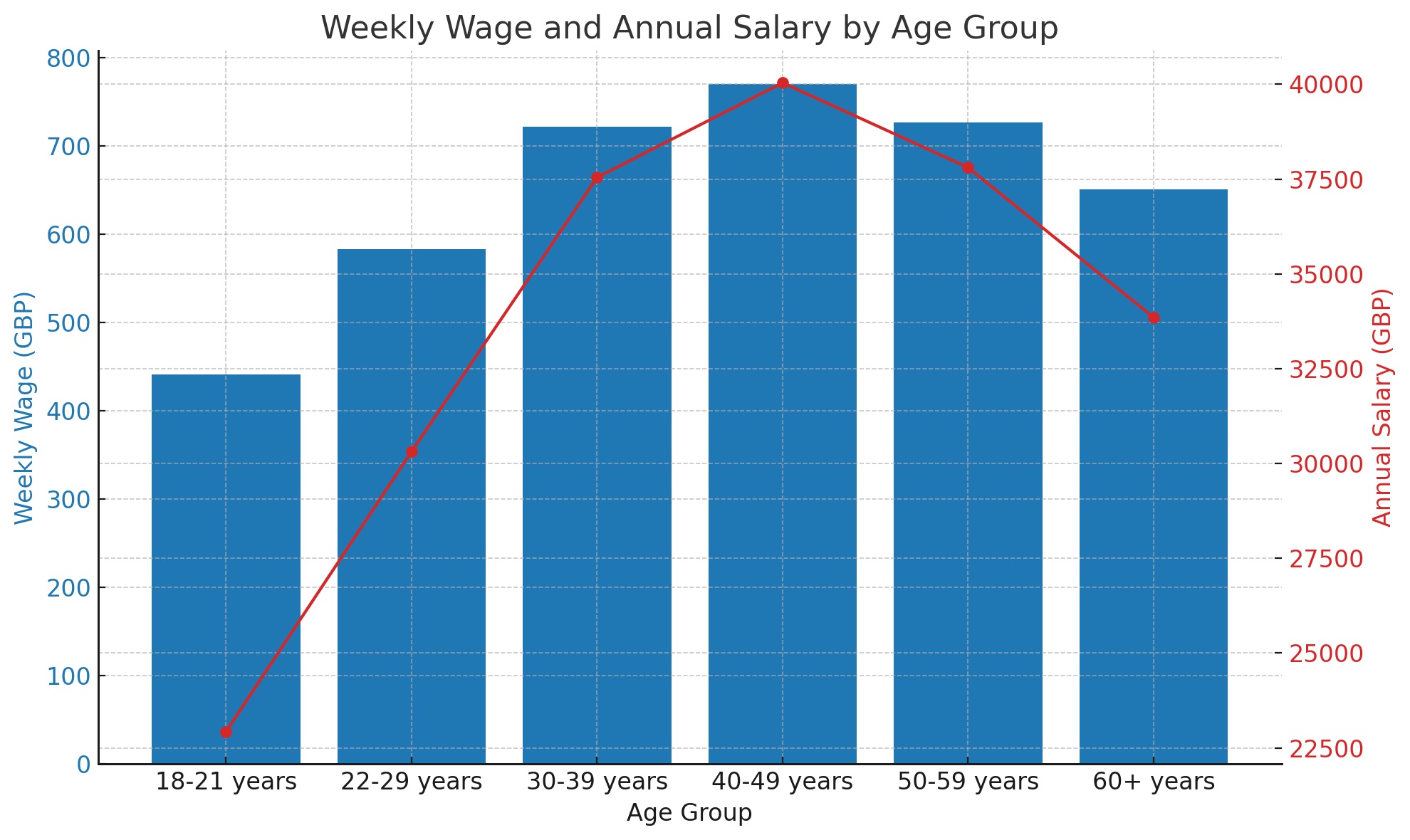

I think well over 3/4, may be even 4/5 of doctors in VSM positions in our organisation are probably over 50, and very few show signs of moving on. 60 seems to the magical age, and many than are back at work the next day. Though clearly that's probably a biased view given I'm up at 6:30am on a Sunday finishing off a board paper . Though from what I understand nationally (internationally??) peak earnings is between 40-50 and than it tails off. I presume that isn't because people become less effective, more likely all of us get older earning money becomes less of a priority. Given there are more and more LTFT in the medical workforce, I suspect that graph will shift more and more to the left.

Edited by gangzoom on Sunday 9th March 06:42

cheesejunkie said:

The_Doc said:

Yeah, good point.

I'll rephrase, all the doctors that can, are planning to leave..

Literally all my friends that are doctors and qualified in the 90s are taking to their advisors and such

What would it take to keep you? Genuine question.I'll rephrase, all the doctors that can, are planning to leave.

. Literally all my friends that are doctors and qualified in the 90s are taking to their advisors and such

My wife works in the NHS and will be retired by 50 if she can and I know some of the answers. But what would it take to keep you?

I'm a realist and I realise some are quitting because they can. Many others will have to keep on chugging on and I'm sure you're the same as her and don't like just walking.

One that my organisation doesn't ask me !

At the risk of just having a mega-winge, I'll state some answers. They may be quite location specific but my friends across the country say the same.

I only have surgeon friends now, we don't keep friends

Many of the answers represent the reasons why surgeons are leaving the NHS to go 100% private, a big loss.

Lack of control - I know how to work productively and fast, but the organisation is incapable of enabling this.

Perpetual cost saving exercises - Its been 25 years in the NHS, and I've never been anywhere that has enough money, we are constantly being told to save money. For 25 years. Cutting back on things for ever.

An unmanaged constant wave of work breaking on your head. Unmanaged, unreasonable work demands. Lots of work is fine, but being pummelled by the surf the whole time is not nice.

Never have enough beds, we never have the beds we need, we now park our patient in fire exits on the ward, not in bed areas.

Unmotivated and apathetic staff. - Not all of them, there are terrific staff out there, but this place/system grinds you down, then they leave.

Pay erosion, its still down 22% in 10 years. Why am I 22% less valuable? I did exams every 3 years between the ages of 7 and 34. Undervalued.

Management/Board level that isn't on the same planet as the rest of the hospital They are workplace aliens.

Wading through mud with a mud rainstorm on your head.

is chapter 1.....

Go into 100% private practice, take back control of all of that and treat more people.

I'm not doing this.

I too got up at 0630 to go to work this am, I work 1 in 6 weekends, no probs with this, I like being a doctor.

But man its hard.

Oh and don't even start me on the Annual Allowance thing.

I have dropped sessions and curtailed my career progression because of this government idiotic s

tshow tax.Read that back. Less people treated to avoid a £40k tax bill for the overtime. My numbers. ish

gangzoom said:

The_Doc said:

Literally all my friends that are doctors and qualified in the 90s are taking to their advisors and such

I think well over 3/4, may be even 4/5 of doctors in VSM positions in our organisation are probably over 50, and very few show signs of moving on. 60 seems to the magical age, and many than are back at work the next day. Though clearly that's probably a biased view given I'm up at 6:30am on a Sunday finishing off a board paper . I'd like to retire and return, maybe in mid 50s, but come back on 20-40% hours. Give up on all management, teaching, supervision work. Just be a serf.

What a total waste, It took me so long to train to get here.

Gassing Station | Finance | Top of Page | What's New | My Stuff