Do I need to pay Capital Gains tax?

Discussion

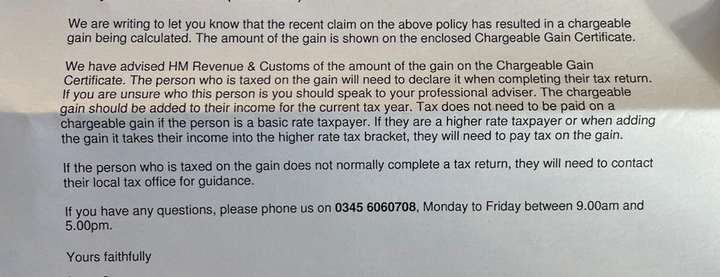

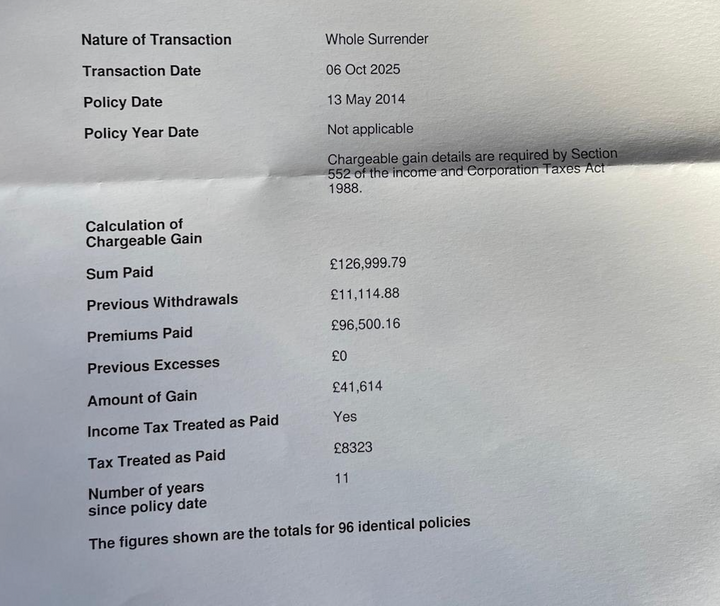

Before I engage with a professional can anyone suggest if any tax is due on this Canada Life Loan Trust investment of my late mothers please, and if so what type of tax - capital gains tax, income tax etc?

Last year after mum died I cashed in the Loan Trust that she had set up to try and exclude some of her estate from Inheritance Tax. Her three children were the beneficiaries and I shared the money out accordingly. However I then received this letter from Canada Life and I'm not sure if any tax is due.

I was assuming capital gains tax as it mentions chargeable gains, but it also states that tax doesn't need to be paid if I/we are basic rate tax payers (which I am), suggesting it's income tax. It also states that tax has been treated as paid???

If any tax due, is this on all the monies received as a one off payment, or it it spread across all three beneficiaries depending on their personal tax status?

Last year after mum died I cashed in the Loan Trust that she had set up to try and exclude some of her estate from Inheritance Tax. Her three children were the beneficiaries and I shared the money out accordingly. However I then received this letter from Canada Life and I'm not sure if any tax is due.

I was assuming capital gains tax as it mentions chargeable gains, but it also states that tax doesn't need to be paid if I/we are basic rate tax payers (which I am), suggesting it's income tax. It also states that tax has been treated as paid???

If any tax due, is this on all the monies received as a one off payment, or it it spread across all three beneficiaries depending on their personal tax status?

Jesus, that's clear as mud!

I'd say it's capital gains as that is generally added to your income. No idea why it suggests that basic rate tax payers don't need to pay it. If you add your share to your income would that push you into the higher rate bracket?

I think you also get a £3k CGT allowance to take off?

I'd ring that number, explain your situation and ask them if they can shed more light on it.

I'd say it's capital gains as that is generally added to your income. No idea why it suggests that basic rate tax payers don't need to pay it. If you add your share to your income would that push you into the higher rate bracket?

I think you also get a £3k CGT allowance to take off?

I'd ring that number, explain your situation and ask them if they can shed more light on it.

I think that's probably right, some of these investment products deliver "capital gains" which are actually taxed as income.

The reporting obligation for CGT requires gains over £3,000 to be reported whether or not there's any tax payable. That's what they're telling you. You could give them a call to check.

The reporting obligation for CGT requires gains over £3,000 to be reported whether or not there's any tax payable. That's what they're telling you. You could give them a call to check.

There's a guide here: https://www.canadalife.co.uk/investments/guide-to-...

Seems to say the gain is treated as income. not a capital gain.

I guess recipients could be liable for more tax if the gain tips them into a higher tax bracket.

Seems to say the gain is treated as income. not a capital gain.

I guess recipients could be liable for more tax if the gain tips them into a higher tax bracket.

Pre-death growth is not subject to CGT.

You only calculate CGT if the asset increases in value after the date of death and is subsequently sold.

Imagine having to pay CGT and also IHT.

Nobody would even bother starting a business, or invest in anything trying to achieve independence.

Return to stone age living.

I hear that Ed Milliband now wants all underfloor heating to be disconnected.

Has he got solar panels on his house yet, or using a bicycle for transport?

Probably not. "Just do as I say."

The Roman's had underfloor heating.

Would living in pre-Roman times, be any more comfortable than the Stone Age?

I don't even know how to hunt animals for food, so cannot see me being able to survive very long.

The Gauge said:

Last year after mum died I cashed in the Loan Trust that she had set up to try and exclude some of her estate from Inheritance Tax. Her three children were the beneficiaries and I shared the money out accordingly. However I then received this letter from Canada Life and I'm not sure if any tax is due.

Not Capital Gains. Chargeable events occur on life insurance policies when certain things happen e.g. the death of the person whose life was insured.If in doubt, contact Canada Life to clarify whether or not the tax has been treated as already paid (although the letter does make this clear).

You mention Loan Trust - was this policy held in your late mother's name, or in a trust?

Edited by C69 on Friday 3rd July 12:37

Jon39 said:

Imagine having to pay CGT and also IHT.

Nobody would even bother starting a business, or invest in anything trying to achieve independence.

Return to stone age living.

R.

Jon39 said:

Pre-death growth is not subject to CGT.

You only calculate CGT if the asset increases in value after the date of death and is subsequently sold.

Imagine having to pay CGT and also IHT.

Nobody would even bother starting a business, or invest in anything trying to achieve independence.

Return to stone age living.

I hear that Ed Milliband now wants all underfloor heating to be disconnected.

Has he got solar panels on his house yet, or using a bicycle for transport?

Probably not. "Just do as I say."

The Roman's had underfloor heating.

Would living in pre-Roman times, be any more comfortable than the Stone Age?

I don't even know how to hunt animals for food, so cannot see me being able to survive very long.

So...much....misinformation...

Better not to comment like you know if you don't know.

A professional would immediately tell you that it was an onshore investment bond. The gains are subject to income tax, there's also top slicing relief if relevant.

Being a loan trust any growth was outside the estate for IHT purposes. The loan amount still belonged to your mother, the point of which is to give her access to that money if she needed it. That would need to be included in her assets, less any repayments she might have taken before her death.

Onshore bonds pay ongoing tax at effectively basic rate. Therefore, if the chargeable gain is within the basic rate band there's no further income tax to pay.

Sounds like you might already have cocked up when you encashed it. If the encashment occurred in the same tax year as her death then the chargeable gain is against the settlor (your mum) and needs to go on her final self assessment. If it was in a later tax year then the gain is on the trustees at trustee rates, which are 45%. You'll have to pay the extra 25%, as 20% has already been paid.

Assuming there was also a younger life assured on the bond, such that it didn't automatically mature when your mum died, then you could have assigned the bond to the three beneficiaries before encashment. Then the gains would have been split and assessed on each of the three of you, possibly resulting in no more income tax if you were all in basic rate. Top slicing could also have been used, but cannot if it's trustee tax.

Always get advice FIRST if you're unsure.

Better not to comment like you know if you don't know.

A professional would immediately tell you that it was an onshore investment bond. The gains are subject to income tax, there's also top slicing relief if relevant.

Being a loan trust any growth was outside the estate for IHT purposes. The loan amount still belonged to your mother, the point of which is to give her access to that money if she needed it. That would need to be included in her assets, less any repayments she might have taken before her death.

Onshore bonds pay ongoing tax at effectively basic rate. Therefore, if the chargeable gain is within the basic rate band there's no further income tax to pay.

Sounds like you might already have cocked up when you encashed it. If the encashment occurred in the same tax year as her death then the chargeable gain is against the settlor (your mum) and needs to go on her final self assessment. If it was in a later tax year then the gain is on the trustees at trustee rates, which are 45%. You'll have to pay the extra 25%, as 20% has already been paid.

Assuming there was also a younger life assured on the bond, such that it didn't automatically mature when your mum died, then you could have assigned the bond to the three beneficiaries before encashment. Then the gains would have been split and assessed on each of the three of you, possibly resulting in no more income tax if you were all in basic rate. Top slicing could also have been used, but cannot if it's trustee tax.

Always get advice FIRST if you're unsure.

Edited by PistonHead007 on Friday 3rd July 15:07

The Leaper said:

Jon39 said:

Imagine having to pay CGT and also IHT.

Nobody would even bother starting a business, or invest in anything trying to achieve independence.

Return to stone age living.

R.

Louise Haigh, a close ally of Mr Burnham and former Transport Secretary, recently argued in an essay that any review of the tax system should "at a minimum" include reform of the CGT uplift on death.

Even if they don't apply it to the family home it would apply to any other properties such as BTLs or holiday homes. There is a scenario where for a lot of boomers CGT is the only reason they are still holding onto their BTLs. This would precipitate a selloff to either avoid higher CGT rates in advance (talk of equalising with income tax rates), or just get on and pay it now and avoid all the Renters Rights Act risks and liabilities if you are going to get clobbered for CGT on top of IHT anyway.

Edited by WayOutWest on Friday 3rd July 15:15

ChrisH72 said:

I can't imagine why anyone would set up something so complicated in the first place. If you want to gift money just do it.

Because it allows you to keep access to some money, whilst accruing growth on it outside of your estate.However, chances are she could probably just have kept a bit and done a straight gift. Which is a lot simpler.

PistonHead007 said:

ChrisH72 said:

I can't imagine why anyone would set up something so complicated in the first place. If you want to gift money just do it.

Because it allows you to keep access to some money, whilst accruing growth on it outside of your estate.However, chances are she could probably just have kept a bit and done a straight gift. Which is a lot simpler.

Ours are Offshore.

Sheepshanks said:

We've done them because we had quite a lot of unsheltered cash and didn't want to give big amounts of money to our kids immediately, but wanted the 7yr IHT clock to start ticking.

Ours are Offshore.

If you've done a loan trust there is no 7 year clock. The original sum is still owed to you and therefore within your estate. The growth is immediately accruing outside of your estate. Should you later decide to gift the amount on loan then that would need 7 years to pass before it falls outside of your estate.Ours are Offshore.

PistonHead007 said:

If you've done a loan trust there is no 7 year clock. The original sum is still owed to you and therefore within your estate. The growth is immediately accruing outside of your estate. Should you later decide to gift the amount on loan then that would need 7 years to pass before it falls outside of your estate.

Off the top of my head I'm not sure what the Trust's exact name is but its specific purpose is as I described.Gassing Station | Finance | Top of Page | What's New | My Stuff