PCP - is the monthly payment negotiable?

Discussion

Sounds like a stupid question, according to the thread title? However, I wanted to ask, why do car salesmen/authorised dealers ask you whether you have a monthly payment in mind?

I thought it was an automated calculation, i.e. you are financing £20,000 with 11.9% interest over 48 months.

Are they just alluding to the number of months? That's the only variable from what I can see?

Thanks all.

I thought it was an automated calculation, i.e. you are financing £20,000 with 11.9% interest over 48 months.

Are they just alluding to the number of months? That's the only variable from what I can see?

Thanks all.

The price dictates the monthlies.

I've just bought on PCP and used the firms online calculator to figure out that my deposit and p/x would land me at 318 a month over 4 years. I went to the salesman with my deposit and px and said I need this figure to be 300 a month, he knocked a bit of the car and gave a bit more for my PX and everyone was happy.

I've just bought on PCP and used the firms online calculator to figure out that my deposit and p/x would land me at 318 a month over 4 years. I went to the salesman with my deposit and px and said I need this figure to be 300 a month, he knocked a bit of the car and gave a bit more for my PX and everyone was happy.

They have a bit more leeway to 'adjust' monthly payments without actually reducing the price of the car. The agreed overall price has, of course, the most influence on the monthly payments but deposit, length of deal and annual mileage allowance also have an influence and can be used by the salesman to reduce your monthly payment without affecting the sale price.

They may have some leeway on interest rate too but this is more often than not fixed by the financer as is the 'balloon' payment.

Always start a negotiation with the actual price of the car and don't be lead in to discussing monthlies until you have a figure you are happy with.

They may have some leeway on interest rate too but this is more often than not fixed by the financer as is the 'balloon' payment.

Always start a negotiation with the actual price of the car and don't be lead in to discussing monthlies until you have a figure you are happy with.

Because if you say you want to pay xyz monthly, then they'll suggest a deposit increase, remove a service pack or something, extend the PCP timeframe etc to get to the monthly. Which is fine, as long as they don't pretend they're doing you a deal if they're not actually reducing the price.

Always make sure you know what you're borrowing, if you need to sell mid term for any reason then those cheap monthlies at high interest but with an inflated balloon payment could be an issue.

Always make sure you know what you're borrowing, if you need to sell mid term for any reason then those cheap monthlies at high interest but with an inflated balloon payment could be an issue.

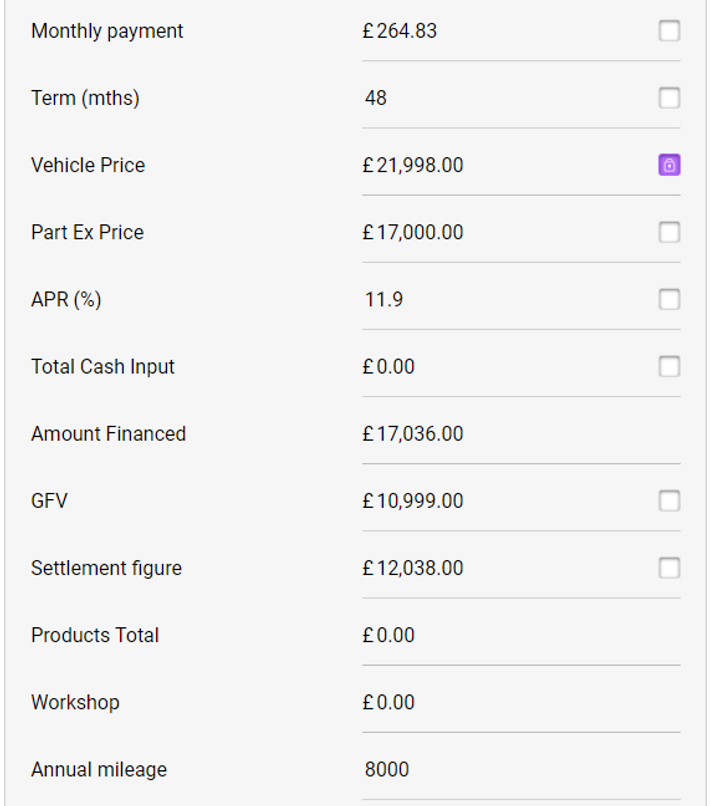

Cheers everyone for your advice so far. Just another quick one from me. Am I looking at this all wrong? With reference to the attached draft illustration, one of the ways I have been assessing it is by looking at the amount being financed (£17,000), subtracting the final balloon payment (£11,000), which results in an amount of £6,000.

As a check, I am then taking the monthly payment of £265, multiplied by 48 months, so I pay £12,720 over 4 years. That's more than double the £6,000 above. With the interest of course it will be more than £6k, but not 100% more...?

Another way of looking at it - £12,720 + £11,000 (balloon) = £23,720. Which is £6,720 in interest. It seems a bit steep??

As a check, I am then taking the monthly payment of £265, multiplied by 48 months, so I pay £12,720 over 4 years. That's more than double the £6,000 above. With the interest of course it will be more than £6k, but not 100% more...?

Another way of looking at it - £12,720 + £11,000 (balloon) = £23,720. Which is £6,720 in interest. It seems a bit steep??

Prisoner 24601 said:

Sounds like a stupid question, according to the thread title? However, I wanted to ask, why do car salesmen/authorised dealers ask you whether you have a monthly payment in mind?

I thought it was an automated calculation, i.e. you are financing £20,000 with 11.9% interest over 48 months.

Are they just alluding to the number of months? That's the only variable from what I can see?

Thanks all.

Depends on how they ask it too. If at the beginning they ask what monthly payments you are looking for and you say £200. They then are trying to work out which model spec you’re going to get. They can then also show you the £210 or £240 higher spec cars, look what you can have for o boy an extra £5 a week! I thought it was an automated calculation, i.e. you are financing £20,000 with 11.9% interest over 48 months.

Are they just alluding to the number of months? That's the only variable from what I can see?

Thanks all.

dave123456 said:

It likely is that high.

Thanks Dave.This leads me back to one of my options, which is, take a personal loan of £12,000 and pay the balloon amount of £12k. That leaves me with a car which is valued at circa £17k. I am perfectly happy with my current car, I could keep it, maintain it and own it for another 5+ years. I'm not a petrolhead and have 'shed' leanings, although not full on 'shedding'.

I will check some quotes for personal loans and see what the interest amount is on those. I am torn on what is the best route to take overall.

Prisoner 24601 said:

Cheers everyone for your advice so far. Just another quick one from me. Am I looking at this all wrong? With reference to the attached draft illustration, one of the ways I have been assessing it is by looking at the amount being financed (£17,000), subtracting the final balloon payment (£11,000), which results in an amount of £6,000.

As a check, I am then taking the monthly payment of £265, multiplied by 48 months, so I pay £12,720 over 4 years. That's more than double the £6,000 above. With the interest of course it will be more than £6k, but not 100% more...?

Another way of looking at it - £12,720 + £11,000 (balloon) = £23,720. Which is £6,720 in interest. It seems a bit steep??

A a rough an ready i would look at it like this.As a check, I am then taking the monthly payment of £265, multiplied by 48 months, so I pay £12,720 over 4 years. That's more than double the £6,000 above. With the interest of course it will be more than £6k, but not 100% more...?

Another way of looking at it - £12,720 + £11,000 (balloon) = £23,720. Which is £6,720 in interest. It seems a bit steep??

The GFV of £11k is there fore the 4 years, therefore 11,000 * 11.9% * 4 years is £5,236

The differential between the £17k and £11k is paid (assume equally) over the 4 years, therefore over the 4 years your average balance is £6,000/2 or £3,000. The 3,000 * 11.9% * 4 years is £1,428

therefore rough total of £5,236 + £1,428 is ~ $6,664 in interest.

you should be able to get a much better pcp rate from any high st bank

Prisoner 24601 said:

Cheers everyone for your advice so far. Just another quick one from me. Am I looking at this all wrong? With reference to the attached draft illustration, one of the ways I have been assessing it is by looking at the amount being financed (£17,000), subtracting the final balloon payment (£11,000), which results in an amount of £6,000.

As a check, I am then taking the monthly payment of £265, multiplied by 48 months, so I pay £12,720 over 4 years. That's more than double the £6,000 above. With the interest of course it will be more than £6k, but not 100% more...?

Another way of looking at it - £12,720 + £11,000 (balloon) = £23,720. Which is £6,720 in interest. It seems a bit steep??

It's a high amount because you are also paying interest on the balloon amount at 11.9% over the 4 year term.As a check, I am then taking the monthly payment of £265, multiplied by 48 months, so I pay £12,720 over 4 years. That's more than double the £6,000 above. With the interest of course it will be more than £6k, but not 100% more...?

Another way of looking at it - £12,720 + £11,000 (balloon) = £23,720. Which is £6,720 in interest. It seems a bit steep??

R500K said:

Prisoner 24601 said:

Cheers everyone for your advice so far. Just another quick one from me. Am I looking at this all wrong? With reference to the attached draft illustration, one of the ways I have been assessing it is by looking at the amount being financed (£17,000), subtracting the final balloon payment (£11,000), which results in an amount of £6,000.

As a check, I am then taking the monthly payment of £265, multiplied by 48 months, so I pay £12,720 over 4 years. That's more than double the £6,000 above. With the interest of course it will be more than £6k, but not 100% more...?

Another way of looking at it - £12,720 + £11,000 (balloon) = £23,720. Which is £6,720 in interest. It seems a bit steep??

A a rough an ready i would look at it like this.As a check, I am then taking the monthly payment of £265, multiplied by 48 months, so I pay £12,720 over 4 years. That's more than double the £6,000 above. With the interest of course it will be more than £6k, but not 100% more...?

Another way of looking at it - £12,720 + £11,000 (balloon) = £23,720. Which is £6,720 in interest. It seems a bit steep??

The GFV of £11k is there fore the 4 years, therefore 11,000 * 11.9% * 4 years is £5,236

The differential between the £17k and £11k is paid (assume equally) over the 4 years, therefore over the 4 years your average balance is £6,000/2 or £3,000. The 3,000 * 11.9% * 4 years is £1,428

therefore rough total of £5,236 + £1,428 is ~ $6,664 in interest.

you should be able to get a much better pcp rate from any high st bank

Prisoner 24601 said:

R500K said:

Prisoner 24601 said:

Cheers everyone for your advice so far. Just another quick one from me. Am I looking at this all wrong? With reference to the attached draft illustration, one of the ways I have been assessing it is by looking at the amount being financed (£17,000), subtracting the final balloon payment (£11,000), which results in an amount of £6,000.

As a check, I am then taking the monthly payment of £265, multiplied by 48 months, so I pay £12,720 over 4 years. That's more than double the £6,000 above. With the interest of course it will be more than £6k, but not 100% more...?

Another way of looking at it - £12,720 + £11,000 (balloon) = £23,720. Which is £6,720 in interest. It seems a bit steep??

A a rough an ready i would look at it like this.As a check, I am then taking the monthly payment of £265, multiplied by 48 months, so I pay £12,720 over 4 years. That's more than double the £6,000 above. With the interest of course it will be more than £6k, but not 100% more...?

Another way of looking at it - £12,720 + £11,000 (balloon) = £23,720. Which is £6,720 in interest. It seems a bit steep??

The GFV of £11k is there fore the 4 years, therefore 11,000 * 11.9% * 4 years is £5,236

The differential between the £17k and £11k is paid (assume equally) over the 4 years, therefore over the 4 years your average balance is £6,000/2 or £3,000. The 3,000 * 11.9% * 4 years is £1,428

therefore rough total of £5,236 + £1,428 is ~ $6,664 in interest.

you should be able to get a much better pcp rate from any high st bank

Finance may be convenient but it is very rarely cheap.

As mentioned above, perhaps a bank loan as alternative or see what the deals are on new cars.

Prisoner 24601 said:

Thank you R500K - when you say much better rate elsewhere, I presume that means, 11.2% in lieu of 11.9%; but doesn't really shift the needle in the overall analysis. It still doesn't strike me as being a particularly great deal for the consumer.

Using your price data, halifax, for example, are currently offering 7.9% so a third less interest charge. Makes it more palatable and i am sure there are others out there that might have slightly better rates. Total payable would be £20.8k over the termPrisoner 24601 said:

dave123456 said:

It likely is that high.

Thanks Dave.This leads me back to one of my options, which is, take a personal loan of £12,000 and pay the balloon amount of £12k. That leaves me with a car which is valued at circa £17k. I am perfectly happy with my current car, I could keep it, maintain it and own it for another 5+ years. I'm not a petrolhead and have 'shed' leanings, although not full on 'shedding'.

I will check some quotes for personal loans and see what the interest amount is on those. I am torn on what is the best route to take overall.

If you don’t, don’t. The cost of interest and depreciation make this sort of thing a lifetime crippler to financial freedom.

A lot of things to unpick here

1. Monthly payment is dictated by a number of variables - deposit, term, rate, annual mileage that is then linked to the balloon (GFV)

2. You pay interest on the GFV, but no capital

(a) You pay capital and interest on the remaining balance after deposits/contributions etc

3. Yes, it's likely that you'll pay that much back in interest as the rate is high

4. You will be protected from negative equity, but only if you keep the car for the full term

5. You can pay the balloon at the end and keep the car

6. You can trade the car in and change at any point before the term is up. Your annual mileage in this scenario is irrelevant, as the car will be valued with whatever mileage you've done versus your settlement figure at that point.

7. You can terminate your agreement once you have paid back 50% of the total amount payable. This is not half your payments as it includes half the interest on the GFV

Probably some things that I've missed as well

1. Monthly payment is dictated by a number of variables - deposit, term, rate, annual mileage that is then linked to the balloon (GFV)

2. You pay interest on the GFV, but no capital

(a) You pay capital and interest on the remaining balance after deposits/contributions etc

3. Yes, it's likely that you'll pay that much back in interest as the rate is high

4. You will be protected from negative equity, but only if you keep the car for the full term

5. You can pay the balloon at the end and keep the car

6. You can trade the car in and change at any point before the term is up. Your annual mileage in this scenario is irrelevant, as the car will be valued with whatever mileage you've done versus your settlement figure at that point.

7. You can terminate your agreement once you have paid back 50% of the total amount payable. This is not half your payments as it includes half the interest on the GFV

Probably some things that I've missed as well

Edited by Dimebars on Friday 5th July 15:11

Gassing Station | Car Buying | Top of Page | What's New | My Stuff