PCP / Purchase Mileage Advice Needed

Discussion

Hi All,

I’ve asked this question in the Car Buying forum, but I’m after some broader advice.

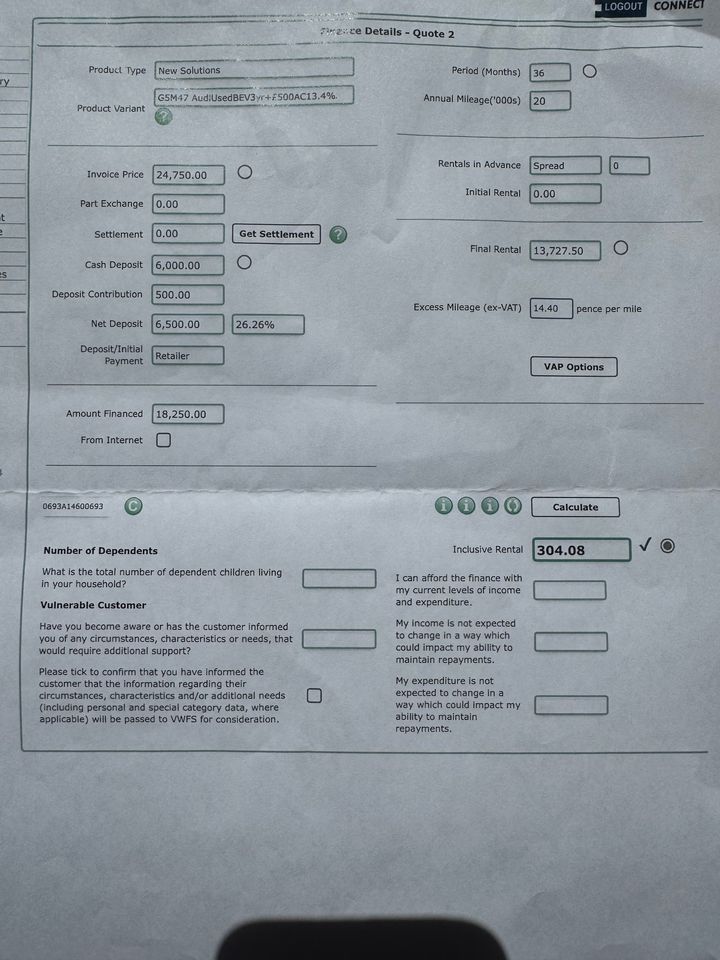

My wife does around 17k miles annually, so we are looking to make the move to electric, and have found two approved used Q4 Audi eTrons we like, from an Audi main dealer. Both similar age, and we are looking at 6k down, and £304 per month over 36-months, with a 13.7k balloon payment at the end of the term. In our mind this looks very attractive, as her current car has cost 5k in the last two years to maintain, and she also spends £300+ a month on diesel.

Are we missing anything else to consider?

However, the main point we are stuck on is, one car has 25k miles, however the other has 45k miles, and a much more attractive spec, such as pan roof, colour and full leather interior. When we questioned the impact of the mileage on the agreement, the salesman said zero, as the end value is predetermined, you run the car, and give it back after three years. In my mind, this makes sense, unless we either want to end the contract early, or have expensive issues relating to the higher mileage in the last year?

I’ve asked this question in the Car Buying forum, but I’m after some broader advice.

My wife does around 17k miles annually, so we are looking to make the move to electric, and have found two approved used Q4 Audi eTrons we like, from an Audi main dealer. Both similar age, and we are looking at 6k down, and £304 per month over 36-months, with a 13.7k balloon payment at the end of the term. In our mind this looks very attractive, as her current car has cost 5k in the last two years to maintain, and she also spends £300+ a month on diesel.

Are we missing anything else to consider?

However, the main point we are stuck on is, one car has 25k miles, however the other has 45k miles, and a much more attractive spec, such as pan roof, colour and full leather interior. When we questioned the impact of the mileage on the agreement, the salesman said zero, as the end value is predetermined, you run the car, and give it back after three years. In my mind, this makes sense, unless we either want to end the contract early, or have expensive issues relating to the higher mileage in the last year?

That's a very expensive deal - I make it around £6,000 in interest on a £25.000 car.

You are borrowing £18k, why not look at a bank loan? You should be able to get around 6.5% over 5 years which works out at around £350 per month. That would save you around £3,000 in interest, and if you wanted to get out after 3 years you'd only owe around £5,500, the car would be worth considerably more.

In terms of your question, the mileage in your agreement is just the maximum you can return the car with at the end of the term if you want to hand it back. So, if you bought the 45,000 mile car and agreed a 3 year deal with 20k p/annum allowance, you could return the car with anything up to 105,000 miles. This is only relevant if you intend to hand the car back at the end of the term, if you want to change early then the car is worth whatever the current market value is, and hopefully this will be more than the settlement on your agreement.

You are borrowing £18k, why not look at a bank loan? You should be able to get around 6.5% over 5 years which works out at around £350 per month. That would save you around £3,000 in interest, and if you wanted to get out after 3 years you'd only owe around £5,500, the car would be worth considerably more.

In terms of your question, the mileage in your agreement is just the maximum you can return the car with at the end of the term if you want to hand it back. So, if you bought the 45,000 mile car and agreed a 3 year deal with 20k p/annum allowance, you could return the car with anything up to 105,000 miles. This is only relevant if you intend to hand the car back at the end of the term, if you want to change early then the car is worth whatever the current market value is, and hopefully this will be more than the settlement on your agreement.

Nothing to add here other than to say that before you sign on the line, take a serious look at the Enyaq.

I've driven both the Enyaq and the Q4 extensively, and the Enyaq is a better car in pretty much every way (including, unusually, in interior trim quality). The Q4 seems to borrow too much of its interior from the A3.

I've driven both the Enyaq and the Q4 extensively, and the Enyaq is a better car in pretty much every way (including, unusually, in interior trim quality). The Q4 seems to borrow too much of its interior from the A3.

Thanks all, the only thing I would add, is they are giving a very attractive trade-in value on our car, plus an additional second year warranty, both of which have a combined value to us of around 4k.

I believe the additional year warranty comes as standard with PCP.

Overall we like the hassle free dealing with Audi offers. Any negotiation advice on what I could request?

I believe the additional year warranty comes as standard with PCP.

Overall we like the hassle free dealing with Audi offers. Any negotiation advice on what I could request?

Edited by AudiSport on Monday 28th April 15:33

AudiSport said:

Thanks all, the only thing I would add, is they are giving a very attractive trade-in value on our car, plus an additional second year warranty, both of which have a combined value to us of around 4k.

I believe the additional year warranty comes as standard with PCP.

Overall we like the hassle free dealing with Audi offers. And negotiation advice on what I could request?

Pop your reg in here and make sure it really is attractive.I believe the additional year warranty comes as standard with PCP.

Overall we like the hassle free dealing with Audi offers. And negotiation advice on what I could request?

https://www.arnoldclark.com/sell-my-car

Would you buy the car at the end of the agreement or buy it? If you'd hand it back I'd ask them to recalculate the mileage at your wifes current annual mileage of 17k rather than 20k as that should make the final value higher, reducing your monthly cost. Of course, if you're going to buy it at the end then it only makes a small difference in the total you'll pay.

As others have said the interest amount seems very high for a relatively small loan, something like 20.5% AER? Even discounting the loan interest of £5,924 by £2,500 for the trade in offer you're left paying £3,424 in interest when you could finance it on a say 6% loan over 3 years for £1,700 interest?

As others have said the interest amount seems very high for a relatively small loan, something like 20.5% AER? Even discounting the loan interest of £5,924 by £2,500 for the trade in offer you're left paying £3,424 in interest when you could finance it on a say 6% loan over 3 years for £1,700 interest?

Nothing of any intelligence to add really, just my thoughts on the option.

You don't say the age of the cars but I am guessing 2 years old as only a year left on the warranty (or 60K whichever comes first), then Audi will give you another year for buying approved used, I guess adding another 20k miles (but I can't see and would be nervous it isn't lower for an older car). Out of your 36 month term that leaves you with at least a year uncovered... I'm guessing batteries and major electrical beyond that probably 8 years 100k.

So you buy the 47k miles Q4 at 2 years old you could be out of warranty in year 2 of ownership, worse before 5 years is up you could be out of battery warranty leaving you potentially with a £13k paperweight. To get the GFV you'd have to return it working (so repair or pay).

It's certainly close, the gamble for me is; do you for sure want to be in battery warranty at the end of ownership or not?

Being prudent, I'd probably go with the lower mileage car as I might cry if I had to pay £13k for nothing at the end. That being said I hate used APR percentages especially on EV's as a lot of manufacturers have some very low APR deals on new but then again I'm not having to consider 20k miles a year which is a fair bit.

You don't say the age of the cars but I am guessing 2 years old as only a year left on the warranty (or 60K whichever comes first), then Audi will give you another year for buying approved used, I guess adding another 20k miles (but I can't see and would be nervous it isn't lower for an older car). Out of your 36 month term that leaves you with at least a year uncovered... I'm guessing batteries and major electrical beyond that probably 8 years 100k.

So you buy the 47k miles Q4 at 2 years old you could be out of warranty in year 2 of ownership, worse before 5 years is up you could be out of battery warranty leaving you potentially with a £13k paperweight. To get the GFV you'd have to return it working (so repair or pay).

It's certainly close, the gamble for me is; do you for sure want to be in battery warranty at the end of ownership or not?

Being prudent, I'd probably go with the lower mileage car as I might cry if I had to pay £13k for nothing at the end. That being said I hate used APR percentages especially on EV's as a lot of manufacturers have some very low APR deals on new but then again I'm not having to consider 20k miles a year which is a fair bit.

Yikes

That's very expensive

If you took at bank loan over 60 months, my bank is currently offering 5.9% you'd pay £350 per month on £18250 .. after 3 years you'd owe £8k before early settlement rebate rather than £13747

So you pay £46 pm more (£1656) over three years but you are nearly £6k below the GMFV at 3 yrs

Which gives you your £6k deposit back

IMHO PCP only really works on new with very low finance rates and big discounts

Have you had a quote on a new one, it might not be much different ?

That's very expensive

If you took at bank loan over 60 months, my bank is currently offering 5.9% you'd pay £350 per month on £18250 .. after 3 years you'd owe £8k before early settlement rebate rather than £13747

So you pay £46 pm more (£1656) over three years but you are nearly £6k below the GMFV at 3 yrs

Which gives you your £6k deposit back

IMHO PCP only really works on new with very low finance rates and big discounts

Have you had a quote on a new one, it might not be much different ?

Edited by Earthdweller on Monday 28th April 16:48

the deal name suggests it's 13.4% apr which is a bit bonkers.

I can understand the trade-in deal but i think in the end you _could_ sell the car privately for similar amount and save yourself the interest.

in the end to answer your original question, the mileage over agreed value only matter s if you 're returning the car and then you're paying 14.4p/mile.

so if you return the car with 21000 miles rather than 20000 you pay them £1440 at the end.

you can only terminate PCP early after you've paid 50% of the value (excluding any deposit contribution, or at least that's my deal on bmw finance)

I can understand the trade-in deal but i think in the end you _could_ sell the car privately for similar amount and save yourself the interest.

in the end to answer your original question, the mileage over agreed value only matter s if you 're returning the car and then you're paying 14.4p/mile.

so if you return the car with 21000 miles rather than 20000 you pay them £1440 at the end.

you can only terminate PCP early after you've paid 50% of the value (excluding any deposit contribution, or at least that's my deal on bmw finance)

AudiSport said:

Thanks guys, the car is indeed 2-years old. We plan to just give it back after the 3-years.

Your wife does a lot of miles which makes it tough. In all honesty though I'd probably look at something with a better warranty, Kia maybe? Then a year or two old around the £20-£25k mark and go bank loan to keep the APR down.Although you do have to work hard to offset the £2.5k premium on your trade in they are offering. Does sound like a big difference though they aren't usually that generous...

Certainly sounds like your wife needs something reliable though and covered so it doesn't cost a ton in the next three or so years.

cvega said:

the deal name suggests it's 13.4% apr which is a bit bonkers.

I can understand the trade-in deal but i think in the end you _could_ sell the car privately for similar amount and save yourself the interest.

in the end to answer your original question, the mileage over agreed value only matter s if you 're returning the car and then you're paying 14.4p/mile.

so if you return the car with 21000 miles rather than 20000 you pay them £1440 at the end.

you can only terminate PCP early after you've paid 50% of the value (excluding any deposit contribution, or at least that's my deal on bmw finance)

Don't you mean £144?I can understand the trade-in deal but i think in the end you _could_ sell the car privately for similar amount and save yourself the interest.

in the end to answer your original question, the mileage over agreed value only matter s if you 're returning the car and then you're paying 14.4p/mile.

so if you return the car with 21000 miles rather than 20000 you pay them £1440 at the end.

you can only terminate PCP early after you've paid 50% of the value (excluding any deposit contribution, or at least that's my deal on bmw finance)

Gassing Station | Car Buying | Top of Page | What's New | My Stuff