Beginners Portfolio Advice

Discussion

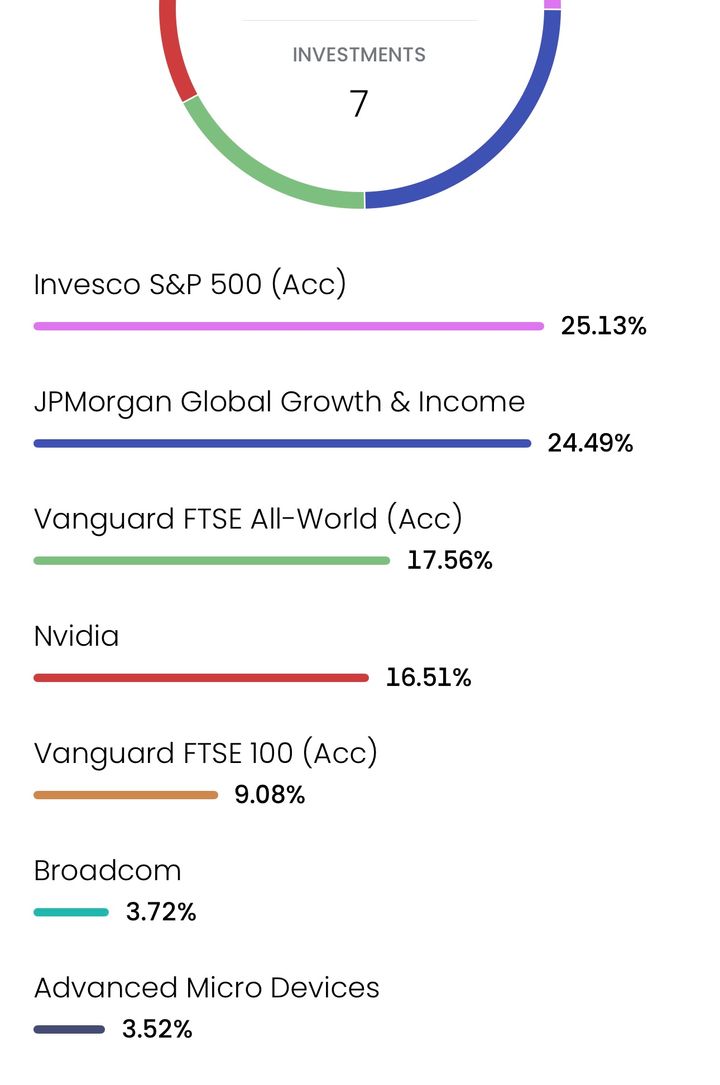

I’ve been dabbling with Trading212 for a few months now to mostly* good success especially of late by topping up in the recent dip

Despite this I’m under no illusion I’ve been lucky and don’t intend to carry on trading this way, the money that’s in is there for the long haul and I intend on adding to this monthly

My intention is to get rid of the single stocks due to my risk profile but need some advice on where to distribute the funds, it’s not a significant amount (circa £10k further to invest)

Despite this I’m under no illusion I’ve been lucky and don’t intend to carry on trading this way, the money that’s in is there for the long haul and I intend on adding to this monthly

My intention is to get rid of the single stocks due to my risk profile but need some advice on where to distribute the funds, it’s not a significant amount (circa £10k further to invest)

brianb said:

I’ve been dabbling with Trading212 for a few months now to mostly* good success especially of late by topping up in the recent dip

Despite this I’m under no illusion I’ve been lucky and don’t intend to carry on trading this way, the money that’s in is there for the long haul and I intend on adding to this monthly

My intention is to get rid of the single stocks due to my risk profile but need some advice on where to distribute the funds, it’s not a significant amount (circa £10k further to invest)

The FTSE All World is nearly 63% invested in the USA, so you would have a significant exposure to the S&P500 index just through that.Despite this I’m under no illusion I’ve been lucky and don’t intend to carry on trading this way, the money that’s in is there for the long haul and I intend on adding to this monthly

My intention is to get rid of the single stocks due to my risk profile but need some advice on where to distribute the funds, it’s not a significant amount (circa £10k further to invest)

So unless you want to overweight to S&P500 you could just hold the All World alone to cover your equity allocation and sell everything else.

You don't say how old you are, which might influence if you want some allocation to bonds.

It intrigues me, that by owning several different funds, would you have investments in the same companies several times?

I did not start with the strategy that I have been using for 35 years, but eventually realised that owning portions of successful large businesses and holding long-term is the best way. The theory favours that and also it suites me because the minimum amount of effort is needed with few portfolio changes. It is sometimes said, short-term is gambling, long-term is investing.

Dividend income. In theory, it is better for a good business never to pay out dividends. The money can grow more within the business. However, many investors like to receive dividends, to use as regular income. They can form a significant part of overall investment returns. The odd thing though when you think about it, the shareholders already own the cash being paid to them. The company has a lower value, because the cash has been distributed.

If you have not already watched them, look on YouTube for Berkshire Hathaway Annual General Meetings. A lengthy watch so set aside enough time. You will be learning from Warren Buffett, probably the most successful business investor ever. Interestingly, he realised far more quickly than me, that long-term gets the compounding going, provided that the business is a good one. You will hear him sometime talk about diversification, because almost all of his own money is invested in only one company. His explanation being, if you know that you have ownership in three of the best businesses at the top of the league and you want to invest more money, then why then put it into a business in say 34th place. It makes no sense.

Stick to the rules Brian. The first two, only use money that you will not need and never invest using leverage (debt). You will learn others.

Good luck.

Edited by Jon39 on Friday 16th August 17:37

Jon39 said:

It intrigues me, that by owning several different funds, would you have investments in the same companies several times?

I did not start with the strategy that I have been using for 35 years, but eventually realised that owning portions of successful large businesses and holding long-term is the best way. The theory favours that and also it suites me because the minimum amount of effort is needed with few portfolio changes. It is sometimes said, short-term is gambling, long-term is investing.

Dividend income. In theory, it is better for a good business never to pay out dividends. The money can grow more within the business. However, many investors like to receive dividends, to use as regular income. They can form a significant part of overall investment returns. The odd thing though when you think about it, the shareholders already own the cash being paid to them. The company has a lower value, because the cash has been distributed.

If you have not already watched them, look on YouTube for Berkshire Hathaway Annual General Meetings. A lengthy watch so set aside enough time. You will be learning from Warren Buffett, probably the most successful business investor ever. Interestingly, he realised far more quickly than me, that long-term gets the compounding going, provided that the business is a good one. You will hear him sometime talk about diversification, because almost all of his own money is invested in only one company. His explanation being, if you know that you have ownership in three of the best businesses at the top of the league and you want to invest more money, then why then put it into a business in say 34th place. It makes no sense.

Stick to the rules Brian. The first two, only use money that you will not need and never invest using leverage (debt). You will learn others.

Good luck.

Edited by Jon39 on Friday 16th August 17:37

But my advice to younger self would probably be to just keep buying a global tracker to hold until you start nearing retirement, and then maybe shift to a more income focussed portfolio - dividends, fund distributions and bond coupons - in your 50s or whatever.

WayOutWest said:

For the record I'm much more geared to dividend income now, and my own portfolio is far from just an All-World index tracker - which only yields a paltry 1.54% - much like the S&P500.

But my advice to younger self would probably be to just keep buying a global tracker to hold until you start nearing retirement, and then maybe shift to a more income focussed portfolio - dividends, fund distributions and bond coupons - in your 50s or whatever.

Where the heck do you get that an all-world index tracker only yields 1.54%?But my advice to younger self would probably be to just keep buying a global tracker to hold until you start nearing retirement, and then maybe shift to a more income focussed portfolio - dividends, fund distributions and bond coupons - in your 50s or whatever.

https://curvo.eu/backtest/en/market-index/ftse-all... shows a CAGR over 9%

For the long term, a global tracker makes a huge amount of sense

Check the logic given on the simple Lars video at https://kroijer.com

Jon39 said:

If you have not already watched them, look on YouTube for Berkshire Hathaway Annual General Meetings. A lengthy watch so set aside enough time. You will be learning from Warren Buffett, probably the most successful business investor ever. Interestingly, he realised far more quickly than me, that long-term gets the compounding going, provided that the business is a good one. You will hear him sometime talk about diversification, because almost all of his own money is invested in only one company. His explanation being, if you know that you have ownership in three of the best businesses at the top of the league and you want to invest more money, then why then put it into a business in say 34th place. It makes no sense.

Buffett also said:"In my view, for most people, the best thing to do is own the S&P 500 index fund”.

"The trick is not to pick the right company. The trick is to essentially buy all the big companies through the S&P 500 and to do it consistently and to do it in a very, very low-cost way”.

For me S&P ETF. 90% ish.

The rest is either in a handful of single stocks when I see the PE get favourable or cash for dips. One replaces the other.

I also trade, but thats a very different game.

Investing is hold and play the long game. The longer you can hold the better you will do.

As others have said, just don't hold the same investments in different accounts / funds its pretty much pointless especially if the fees are different.

Go with the lowest cost.

The rest is either in a handful of single stocks when I see the PE get favourable or cash for dips. One replaces the other.

I also trade, but thats a very different game.

Investing is hold and play the long game. The longer you can hold the better you will do.

As others have said, just don't hold the same investments in different accounts / funds its pretty much pointless especially if the fees are different.

Go with the lowest cost.

b hstewie said:

hstewie said:

hstewie said: A sensible starting point would be a dumb cheap global tracker.

Think about your appetite for risk.

What would you do in a serious downturn. Would you want to buy more of it, or would you panic and sell?

The answer to that might push you down the risk ladder.

Think about your appetite for risk.

What would you do in a serious downturn. Would you want to buy more of it, or would you panic and sell?

The answer to that might push you down the risk ladder.

A very important point Mr. Stewie, for all beginners to consider.

I can still remember a few people who had applied for a privitisation issue, but before they received their shares, there was a huge stock market crash. They were shocked and said they would never invest in stock markets ever again.

There was indeed a huge percentage fall around the world in just a few days, but the irony was, there was a prompt partial recovery and the UK market finished that year higher than it had begun. A reasonable overall result therefore, with a buying opportunity included (which I did not realise at that time though).

It of course takes time to accumulate investing experience, but as you suggest above, having the right temperament is so important.

Worrying and losing sleep when downturns occur is not good, so perhaps best not to become involved.

For example, this chart shows my weekly losses and gains so far this year. How would a new investor sleep on Friday night, after losing money (on paper) that week? It happens continually. To always use money that is not needed is vital, because you will never become a forced seller.

( Only corporate action changes to the portfolio. )

As experience is gained, a serious market downturn can become an opportunity. They seldom occur though. In my time of investing they have only happened in 1987; 2000 (dot com bust); 2009 (global crash); 2020 (pandemic). There were bargains to be purchased on those occasions, but imagine having to be a brave buyer, when everyone appears to be selling. Adding to your existing holdings seems safest, because you already have experience of those businesses and therefore it is easier to recognise that the prices are attractive. Herd activity can sometimes be observed at those times. Interestingly, the October 1987 crash was huge news at the time, but look on a long-term market chart now and you can hardly even see a blip on the trace.

Edited by Jon39 on Sunday 18th August 17:07

gotoPzero said:

For me S&P ETF. 90% ish.

Do you ever worry about lack of diversification e.g: US markets go through a prolonged downturn. I hold VUSA in one of my investment accounts but sometimes wonder why I don't just hold a similar cheap S&P500 ETF or fund in my SIPP rather than a Global Equities tracker. It would be a bet on US markets continuing to outperform RoW but with a 15+ years horizon to retirement it may work out ok....or not!brianb said:

I’ve been dabbling with Trading212 for a few months now to mostly* good success especially of late by topping up in the recent dip

Despite this I’m under no illusion I’ve been lucky and don’t intend to carry on trading this way, the money that’s in is there for the long haul and I intend on adding to this monthly

My intention is to get rid of the single stocks due to my risk profile but need some advice on where to distribute the funds, it’s not a significant amount (circa £10k further to invest)

Just two things to highlight: Despite this I’m under no illusion I’ve been lucky and don’t intend to carry on trading this way, the money that’s in is there for the long haul and I intend on adding to this monthly

My intention is to get rid of the single stocks due to my risk profile but need some advice on where to distribute the funds, it’s not a significant amount (circa £10k further to invest)

First, when you look at companies, including those contained within trackers, do consider that you might have more exposure to (or concentration of) foreign exchange risk than you first realise.

Also be very aware of fees, especially on platform that don’t appear to charge you commission. There is no free lunch in the financial services industry and it’s easy to make platforms offering things like “commission free” more than pay their way by giving punters crappy bid/offer spreads, loading up the fx charges, etc…

Gassing Station | Finance | Top of Page | What's New | My Stuff