Holding funds outside of UK - Vanguard?

Discussion

I have a (perhaps unwarranted?!) nervousness about having all of my savings and investments held within the UK system (even my US tech shares are in a Freetrade S&S ISA), and am wondering whether I should have a portion invested outside of the UK. What would be the easiest way to do this…does a Vanguard S&P500 or Global fund give that comfort? For context, probably talking £80-100k invested outside the UK system. I have a couple of EIS investments but everything else is currently in ISAs, UK savings and premium bonds - and I worry that’s not diversified enough.

Second question - if passive non-UK funds make sense, there look to be platforms (eg InvestEngine) that are cheaper than direct (eg Vanguard). Any recommendations for 1 vs the other?

Thanks in advance.

Second question - if passive non-UK funds make sense, there look to be platforms (eg InvestEngine) that are cheaper than direct (eg Vanguard). Any recommendations for 1 vs the other?

Thanks in advance.

Edited by johnnyBv8 on Thursday 19th December 13:39

Jackals said:

Why are you nervous about having your assets within the UK system? If you move your assets offshore this can be expensive and you could be liable for a different set of tax rules unless I've misunderstood your question?

I just feel from a risk perspective that it’s perhaps healthy to spread assets not just across asset types but also countries. As I say, perhaps unnecessary Your post is very confusing. Do you want to have investments in non-UK securities? You have this with the US tech shares, S&P 500 fund etc OR do you want some of your assets to be in custody outside of the UK? If it‘s the latter, the only place amenable to offshore banking in Europe that I can think of and that would be a safer bet from whatever you are worried about would be Switzerland and no reputable institution there is going to be interested in less than half a million (and the proper ones 10 times that minimum these days) - it‘s just not worth the hassle.

What are you worried about? Asset confiscation? That‘s pretty much a literal doomsday scenario IMO

What are you worried about? Asset confiscation? That‘s pretty much a literal doomsday scenario IMO

You'll create a load of paperwork and expose yourself to greater risk by holding assets offshore. One of the key benefits of investing via UK entities is that you get to resolve disputes through the English legal system and you get all the consumer protection of a Brit.

There can be tax advantages from off-shoring assets. If that was what you were trying to achieve, it could make sense.

The risk of UK companies and markets underperforming is a different thing and you can easily choose to invest in overseas companies by buying funds that are listed in the UK but are just wrappers for investments in those overseas companies. Investing in overseas firms via unit trusts or whatever gives you an easy way of getting diversification and options for the amount of foreign exchange risk you want to carry.

There can be tax advantages from off-shoring assets. If that was what you were trying to achieve, it could make sense.

The risk of UK companies and markets underperforming is a different thing and you can easily choose to invest in overseas companies by buying funds that are listed in the UK but are just wrappers for investments in those overseas companies. Investing in overseas firms via unit trusts or whatever gives you an easy way of getting diversification and options for the amount of foreign exchange risk you want to carry.

Edited by ATG on Thursday 19th December 18:04

ATG said:

You'll create a load of paperwork and expose yourself to greater risk by holding assets offshore. One of the key benefits of investing via UK entities is that you get to resolve disputes through the English legal system and you get all the consumer protection of a Brit.

There can be tax advantages from off-shoring assets. If that was what you were trying to achieve, it could make sense.

This! There can be tax advantages from off-shoring assets. If that was what you were trying to achieve, it could make sense.

Unless its Elon money, its more of a likely (expensive) option than any benefit it might bring.

Without addressing the validity of your concerns, many funds and ETFs sold in the UK (e.g. Vanguard ones) are managed by an Irish subsidiary and use an Irish depositary. The flip side to your concerns is that there's no Irish equivalent to the FSCS for funds/ETFs, though I understand that the protection offered by the FSCS for funds/ETFs is probably fairly limited.

Ok, thanks all. It wasn’t asset confiscation per se, but certainly government intervention. You look at the proportion of people in the UK that live beyond their means and have no savings (and I genuinely don’t mean those for whom saving is impossible), and have to wonder whether there has to be some form of wealth correction against those that have saved, in a country that is quickly moving down the world wealth rankings. But from the responses here it sounds like it isn’t a valid concern! Thanks anyway - I may still look at Vanguard from a diversified portfolio perspective.

Your issue with offshoring your wealth because you are concerned about some sort of redistribution, wealth tax, whatever, is that most places where I’d feel comfortable having my assets has signed up to AEOI (Automatic Exchange of Information), so they’d still inform HMRC.

I mean do you really want to put your money in any of these places?

From ChatGPT

The **Automatic Exchange of Information (AEOI)** is a global initiative aimed at enhancing tax transparency and preventing tax evasion. Countries that participate in AEOI are obligated to share financial account information of foreign account holders with tax authorities in the account holders' home countries. This is typically done under the **Common Reporting Standard (CRS)**, established by the OECD.

However, not all jurisdictions comply with the AEOI standards. While many offshore banking centres have adopted the AEOI framework, some have not signed on or have delayed their participation. These jurisdictions may either have resisted implementing AEOI or might not yet have been formally included in the global framework.

Some well-known offshore banking centres that have historically been either **non-compliant or not fully participating in AEOI** (as of the latest available data) include:

I mean do you really want to put your money in any of these places?

From ChatGPT

The **Automatic Exchange of Information (AEOI)** is a global initiative aimed at enhancing tax transparency and preventing tax evasion. Countries that participate in AEOI are obligated to share financial account information of foreign account holders with tax authorities in the account holders' home countries. This is typically done under the **Common Reporting Standard (CRS)**, established by the OECD.

However, not all jurisdictions comply with the AEOI standards. While many offshore banking centres have adopted the AEOI framework, some have not signed on or have delayed their participation. These jurisdictions may either have resisted implementing AEOI or might not yet have been formally included in the global framework.

Some well-known offshore banking centres that have historically been either **non-compliant or not fully participating in AEOI** (as of the latest available data) include:

- # 1. **United States**

- # 2. **Panama**

- # 3. **Belize**

- # 4. **Vanuatu**

- # 5. **The Cook Islands**

- # 6. **The Marshall Islands**

- # 7. **Nauru**

- # 8. **Seychelles**

- # Other Jurisdictions

- # Conclusion

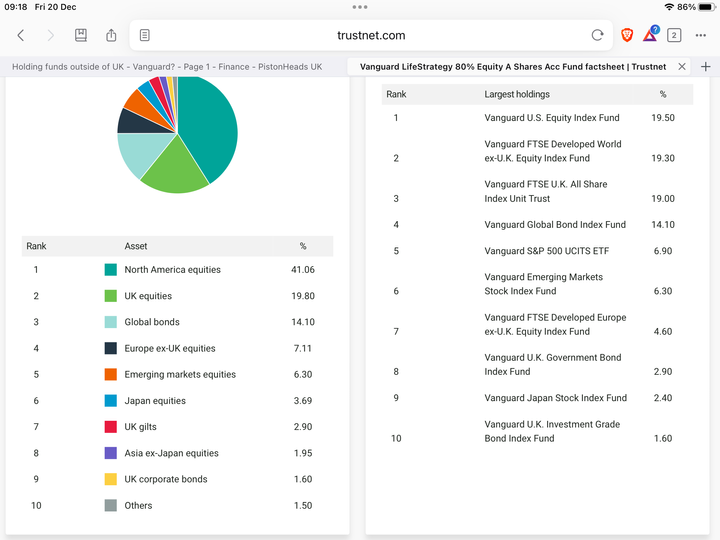

In 2017, I decided to stop looking for Global needles and bet on the haystack with Vanguard LifeStrategy 80. https://www.trustnet.com/factsheets/o/acdt/vanguar...

This is their current geographical and asset spread?

It is angst-free and so simple with a consolidated tax certificate for the tax-man, last time I checked it had done about 17% this year. Our ISAs are there as well.

Being old, we keep a decent chunk in cash deposits to see to our likely immediate needs for about 3-years, so combined, it is relatively low-risk.

This is their current geographical and asset spread?

It is angst-free and so simple with a consolidated tax certificate for the tax-man, last time I checked it had done about 17% this year. Our ISAs are there as well.

Being old, we keep a decent chunk in cash deposits to see to our likely immediate needs for about 3-years, so combined, it is relatively low-risk.

Gassing Station | Finance | Top of Page | What's New | My Stuff