Best time to put money into ISA?

Discussion

I have never had an ISA before.

Say I had £20k to put into a cash ISA, should I do it in March or after 5 April?

I'm a little confused, ISAs only seem to last twelve months (before dropping to a lower rate) so is that twelve months from 6 April 2025 to 5 April 2026?

I have noticed that ISA interest rates are dropping slightly after 5 April 2025, from where they are now.

I definitely like easy access, one never knows what emergency is round the corner.

Say I had £20k to put into a cash ISA, should I do it in March or after 5 April?

I'm a little confused, ISAs only seem to last twelve months (before dropping to a lower rate) so is that twelve months from 6 April 2025 to 5 April 2026?

I have noticed that ISA interest rates are dropping slightly after 5 April 2025, from where they are now.

I definitely like easy access, one never knows what emergency is round the corner.

Surely you’d want to put it in before the end of the current tax year. As you can only pay a maximum of £20k into ISAs per year (you can pay into both a cash and a stocks & shares ISA within the £20k limit), if you leave it until April you will have missed out on any opportunity to add in further funds if they become available

595Heaven said:

Surely you’d want to put it in before the end of the current tax year. As you can only pay a maximum of £20k into ISAs per year (you can pay into both a cash and a stocks & shares ISA within the £20k limit), if you leave it until April you will have missed out on any opportunity to add in further funds if they become available

Thanks for the reply, so say I pay in 20k on 1 March 2025, do I get twelve months interest, payable 1 March 2026?So say I manage to save 10k during 2026, should I get another ISA on 6 April and start saving into that?

I am a lower rate tax payer.

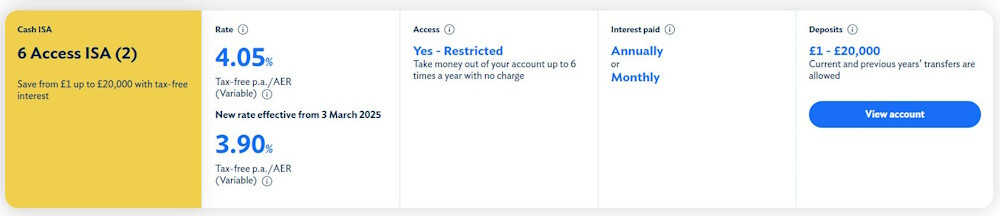

As you can see from this example from Coventry Building Society, the rates are dropping for 2026 (actually from 3 March 2025).

Put it in now as then you will have the benefit of another £20k allowance for the next tax year.

Most initial fixed rates last a year but you can then transfer to another ISA with whatever decent rates are available then. By transferring from one ISA to another you retain the allowance for that year - if you withdraw the money and then want to put money back into an ISA you are limited by whatever of your £20k allowance you have left that year.

Most initial fixed rates last a year but you can then transfer to another ISA with whatever decent rates are available then. By transferring from one ISA to another you retain the allowance for that year - if you withdraw the money and then want to put money back into an ISA you are limited by whatever of your £20k allowance you have left that year.

If you haven't had an ISA before, or have not paid anything into one (of any type) this tax year, then put it in an ISA as soon as possible (i.e. this tax year) and you can then add more to it if you want (or are able) next tax year.

Many cash ISAs are one-year fixed (slightly higher) rate that then drop a little at the end of the one year term - but they remain an ISA and you can transfer them to a new deal/fixed term immediately (in fact most ISA providers will write to you/email you to encourage you to do this), or you could leave them there and start a new ISA.

So, for example if you open one tomorrow (25th Feb) you pay in £20K, on April 6th, you pay in another £20K.

On 24th Feb 2026 you now have an ISA containing £40K plus some interest (probably in the region of £1,800) which has reached the end of its fixed term, and moves to a lower rate - but it is still an ISA.

You can then leave that ~£42K in where it is (a lower performing ISA) or transfer it to a new fixed rate ISA starting with ~£42K in it. You would not be able to pay in any more until 6th April 2026 though, at which point you could add another £20K, or start a totally new ISA with someone else (and not pay any more into the original - just earn interest) - the reason for this might be if you have over £85K in your ISA and want to ensure that you are covered by FSCS if your ISA provider were to go bust.

This is a quite good summary here: https://www.moneysupermarket.com/savings/cash-isas...

Many cash ISAs are one-year fixed (slightly higher) rate that then drop a little at the end of the one year term - but they remain an ISA and you can transfer them to a new deal/fixed term immediately (in fact most ISA providers will write to you/email you to encourage you to do this), or you could leave them there and start a new ISA.

So, for example if you open one tomorrow (25th Feb) you pay in £20K, on April 6th, you pay in another £20K.

On 24th Feb 2026 you now have an ISA containing £40K plus some interest (probably in the region of £1,800) which has reached the end of its fixed term, and moves to a lower rate - but it is still an ISA.

You can then leave that ~£42K in where it is (a lower performing ISA) or transfer it to a new fixed rate ISA starting with ~£42K in it. You would not be able to pay in any more until 6th April 2026 though, at which point you could add another £20K, or start a totally new ISA with someone else (and not pay any more into the original - just earn interest) - the reason for this might be if you have over £85K in your ISA and want to ensure that you are covered by FSCS if your ISA provider were to go bust.

This is a quite good summary here: https://www.moneysupermarket.com/savings/cash-isas...

ISA is a tax wrapper available for each tax year.

In the OP's example he would get tax free interest for one month, then have a further allowance so he could roll the ISA over into next tax year with one month's interest thus having a slightly larger amount for the upcoming new tax year.

However, far better returns could be won by buying into a S&S ISA!

There is a very small chance that Rachel Thieves, after stealing my WFA and having a minor fiddle with pensions may decide to look at ISA's, most likely to discourage cash ISA's in favour of S&A ISA's.

In the OP's example he would get tax free interest for one month, then have a further allowance so he could roll the ISA over into next tax year with one month's interest thus having a slightly larger amount for the upcoming new tax year.

However, far better returns could be won by buying into a S&S ISA!

There is a very small chance that Rachel Thieves, after stealing my WFA and having a minor fiddle with pensions may decide to look at ISA's, most likely to discourage cash ISA's in favour of S&A ISA's.

Senex said:

I have never had an ISA before.

Say I had £20k to put into a cash ISA, should I do it in March or after 5 April?

I'm a little confused, ISAs only seem to last twelve months (before dropping to a lower rate) so is that twelve months from 6 April 2025 to 5 April 2026?

I have noticed that ISA interest rates are dropping slightly after 5 April 2025, from where they are now.

I definitely like easy access, one never knows what emergency is round the corner.

Hopefully it is clearer from the other threads, but it might help to think of it as follows:Say I had £20k to put into a cash ISA, should I do it in March or after 5 April?

I'm a little confused, ISAs only seem to last twelve months (before dropping to a lower rate) so is that twelve months from 6 April 2025 to 5 April 2026?

I have noticed that ISA interest rates are dropping slightly after 5 April 2025, from where they are now.

I definitely like easy access, one never knows what emergency is round the corner.

Savings accounts are like pots: you put money into the pot, and the bank pays you interest. Some pots are easy access, some are fixed term. A fixed term/fixed rate savings account pays (say) 4% for one year, then the pot becomes (usually) an easy access pot paying much less interest. You can move money around between pots, subject to the rules of the account - e.g., you usually can't move money out of a fixed term account before the term ends.

ISAs are just particular types of savings account pots. Just as with other types of accounts/pots, there are easy access accounts and fixed term accounts. Interest earned is tax free. You can move money between pots, just as between non-ISA pots. However, (and this is simplifying things a bit) you can only move money from ISA pots to other ISA pots (not to non-ISA pots) otherwise the interest will then be taxable.

You can put up to £20k from a non-ISA pot into an ISA pot each tax year. Once money is in an ISA pot, you can keep it in an ISA pot (doesn't have to be the same one) forever, if you wish.

You can have multiple ISA pots running at the same time - for example, you might put this year's £20k in a 2-year fixed rate ABC bank ISA account; next year, you could put £20k into a 2-year fixed rate XYZ bank ISA account.

Senex said:

595Heaven said:

Surely you’d want to put it in before the end of the current tax year. As you can only pay a maximum of £20k into ISAs per year (you can pay into both a cash and a stocks & shares ISA within the £20k limit), if you leave it until April you will have missed out on any opportunity to add in further funds if they become available

Thanks for the reply, so say I pay in 20k on 1 March 2025, do I get twelve months interest, payable 1 March 2026?Senex said:

So say I manage to save 10k during 2026, should I get another ISA on 6 April and start saving into that?

See my example in the previous post. Your ISA will likely span two tax years and you can put up to £20K in per tax year. You also do not need to do it on one go - you could make your savings into the ISA directly (i.e. monthly payment) as long as you do not exceed the £20K annual allowance in each of the tax years. 1st March 2026 you could either open a new ISA with a higher interest rate and transfer the balance from the old one to the new one (this does not count towards the £20K annual limit) or open an entirely new one and keep it separate from the old one (note - if you had already paid in £20K in 2025-2026 you might need to wait until 6th April 2026 to do this as most providers require you to actually add some money when opening a new ISA if you are not transferring an old one into it).Senex said:

I am a lower rate tax payer.

As you can see from this example from Coventry Building Society, the rates are dropping for 2026 (actually from 3 March 2025).

Your tax rate makes little difference to an ISA - the only thing it does mean is that you will have a higher tax free allowance on a "normal" bank account (£1,000) - so if you don't get more than £1,000 in interest then you don't really "need" an ISA, but if your salary is likely to grow and you have a long term plan for the money (e.g. retirement fund/house purchase) then it does make sense to get it into the tax free wrapper.As you can see from this example from Coventry Building Society, the rates are dropping for 2026 (actually from 3 March 2025).

Just as an aside, some ISA providers will allow you to make withdrawals and later replace that money within the same tax year, but not all, so you will need to review if access to the money is something you might need to consider when choosing.

Edited by TriumphStag3.0V8 on Monday 24th February 22:51

ferret50 said:

ISA is a tax wrapper available for each tax year.

In the OP's example he would get tax free interest for one month, then have a further allowance so he could roll the ISA over into next tax year with one month's interest thus having a slightly larger amount for the upcoming new tax year.

However, far better returns could be won by buying into a S&S ISA!

There is a very small chance that Rachel Thieves, after stealing my WFA and having a minor fiddle with pensions may decide to look at ISA's, most likely to discourage cash ISA's in favour of S&A ISA's.

Two points:In the OP's example he would get tax free interest for one month, then have a further allowance so he could roll the ISA over into next tax year with one month's interest thus having a slightly larger amount for the upcoming new tax year.

However, far better returns could be won by buying into a S&S ISA!

There is a very small chance that Rachel Thieves, after stealing my WFA and having a minor fiddle with pensions may decide to look at ISA's, most likely to discourage cash ISA's in favour of S&A ISA's.

1. Yes, you can make much better returns in a S&S ISA, however you *could* also lose money.

2. It's much more than a small chance Rachel will come after cash ISAs. I would expect it to be a certainty that something will be changed.

Thank you for all the replies. Very helpful.

Right, I see now. For some reason I thought the max you could ever have in any ISA was 20k, but I see now, that's per year.

So I can open a 20k ISA in March and keep adding savings (estimated £500 per month) into it during 25-26 tax year, got it.

Fixed rate ISAs are very attractive but I can't live with not being able to get at my money if the roof blows off my house or something.

As for S&S ISAs, I just don't have the bottle for that game. Low risk, medium risk, high risk....any sentence involving my money that contains the word "risk" and I'm out

If Rachel Thieves does go after cash ISAs, surely that will only be for new accounts? If I get my 20k in now, I'll be OK?

Right, I see now. For some reason I thought the max you could ever have in any ISA was 20k, but I see now, that's per year.

So I can open a 20k ISA in March and keep adding savings (estimated £500 per month) into it during 25-26 tax year, got it.

Fixed rate ISAs are very attractive but I can't live with not being able to get at my money if the roof blows off my house or something.

As for S&S ISAs, I just don't have the bottle for that game. Low risk, medium risk, high risk....any sentence involving my money that contains the word "risk" and I'm out

If Rachel Thieves does go after cash ISAs, surely that will only be for new accounts? If I get my 20k in now, I'll be OK?

Senex said:

Thank you for all the replies. Very helpful.

Right, I see now. For some reason I thought the max you could ever have in any ISA was 20k, but I see now, that's per year.

Correct - you can ADD up to £20K per tax yearRight, I see now. For some reason I thought the max you could ever have in any ISA was 20k, but I see now, that's per year.

Senex said:

So I can open a 20k ISA in March and keep adding savings (estimated £500 per month) into it during 25-26 tax year, got it.

Correct. It will be the same account and you should not need to do anything other than pay into it.Senex said:

Fixed rate ISAs are very attractive but I can't live with not being able to get at my money if the roof blows off my house or something.

Consider something like a limited access ISA - for example Nationwide allow up to 3 withdrawals without impacting the interest rate, which is only 0.1% less than their "do not touch for a year" ISA.Senex said:

As for S&S ISAs, I just don't have the bottle for that game. Low risk, medium risk, high risk....any sentence involving my money that contains the word "risk" and I'm out

Agreed, I have a small amount in a S&S as a self managed plaything that I am "willing" to lose, but the bulk is in cash ISAs. Some people will just use a managed portfolio offering - but there is still the chance of losing money in that (and paying for the privilege). Cash ISAs are the safe bet.Senex said:

If Rachel Thieves does go after cash ISAs, surely that will only be for new accounts? If I get my 20k in now, I'll be OK?

One would hope and expect so, yes (although I would say new allowances rather than new accounts). Get the money in the tax free wrapper now and hopefully Rachel's next masterclass in economics will only be to limit how much more you can add to it each year. TriumphStag3.0V8 said:

Two points:

1. Yes, you can make much better returns in a S&S ISA, however you *could* also lose money.

2. It's much more than a small chance Rachel will come after cash ISAs. I would expect it to be a certainty that something will be changed.

A 'flexible' ISA is a good starting point for an ISA virgin, allows one to pull cash out if needed and can be replaced within the same tax year.1. Yes, you can make much better returns in a S&S ISA, however you *could* also lose money.

2. It's much more than a small chance Rachel will come after cash ISAs. I would expect it to be a certainty that something will be changed.

I did this last summer, I had solar panels placed on my garage roof on a 'fit now, pay in 6 months' basis, as I was sure a holiday property would sell in time.....it did'nt, by a gap of a week or so...

so I 'borrowed ' from the ISA, I was also able to place the returned funds in a better producing fund but that is another risk to consider!

so I 'borrowed ' from the ISA, I was also able to place the returned funds in a better producing fund but that is another risk to consider!Regarding the delightful Rachel, producing a Budget that would encourage growth rather than placing punative burdens on employers would go down very well!

Fiddling with pensions and ISA's does nothing to boost growth. Stealing WFA just simply removed money from the economy.

Just to note you can get much better rates than the quoted Coventry account, I usually peruse this list from time to time (first post on page 1);

https://forums.moneysavingexpert.com/discussion/40...

Personally we have a couple of Chip Cash ISA's (also a Investengine S&S ISA in a 'world' tracker - SPDR MSCI World (SWLD), consider one for longer term savings).

https://forums.moneysavingexpert.com/discussion/40...

Personally we have a couple of Chip Cash ISA's (also a Investengine S&S ISA in a 'world' tracker - SPDR MSCI World (SWLD), consider one for longer term savings).

Worth knowing that cash over the long term isn’t a risk free option. Inflation is your enemy there.

Emergency money is typically separate from longer term savings which is what many use their ISA allowance for given its generous tax free growth potential. Your pension is likely invested in stocks..

Emergency money is typically separate from longer term savings which is what many use their ISA allowance for given its generous tax free growth potential. Your pension is likely invested in stocks..

okgo said:

Worth knowing that cash over the long term isn’t a risk free option. Inflation is your enemy there.

Yes, I can see that but as things currently stand, inflation is 3% and cash ISA returns 4-5% so that's inflation sorted, no?okgo said:

Emergency money is typically separate from longer term savings which is what many use their ISA allowance for given its generous tax free growth potential. Your pension is likely invested in stocks..

Yes, so I understand. I'm pretty new at this savings game and I realise that If i put my savings in an ISA I will need to build a separate emergency fund, I have £20k saved over the last 3 years or so that I need to shove in an ISA soon, and I hope to add to that this year. I am aiming at saving 500 per month this year so perhaps half in the ISA and half in the emergency fund. How does that sound? I'll tell you something about becoming a saver, it doesn't half make one tight, I'm starting to resent things like Christmas, so come December it's 'Oh well, no savings this month then Grr'

I don't really see a need to separate Emergency fund and savings. I just don't see that much that could happen that you'd need to completely clear out.

Worth having a bit of cash on hand but I happily use that same pot to book a holiday, buy a watch or in an emergency, buy a washing machine.

Even just relying on credit cards will see you through a month. If it does turn out to be something significant, just take it from your cash ISA, even if 'fixed' you can still get that money back. It just seems a waste to be to have an extra fund sat not really doing anything.

Worth having a bit of cash on hand but I happily use that same pot to book a holiday, buy a watch or in an emergency, buy a washing machine.

Even just relying on credit cards will see you through a month. If it does turn out to be something significant, just take it from your cash ISA, even if 'fixed' you can still get that money back. It just seems a waste to be to have an extra fund sat not really doing anything.

Gassing Station | Finance | Top of Page | What's New | My Stuff