Joining employers Aviva Pension Scheme

Discussion

Anyone able to comment on how good/bad the Aviva My Future Long Term Growth S6 pension plan is please?

My 19yr old son was about 1yr into his mechanical engineering apprenticeship and has just been enrolled into his employers pension. His salary is just short of £15k and from the paperwork he's just received I've established the following..

Employee contributions @3% (£39 gross) - I'm encouraging him to increase this to take advantage of employer contributions

Employer contributions £23

Annual Fund Charge - 0.3%

Additional Yearly Charge - 0%

Fund Manager Expense Charge - 0%

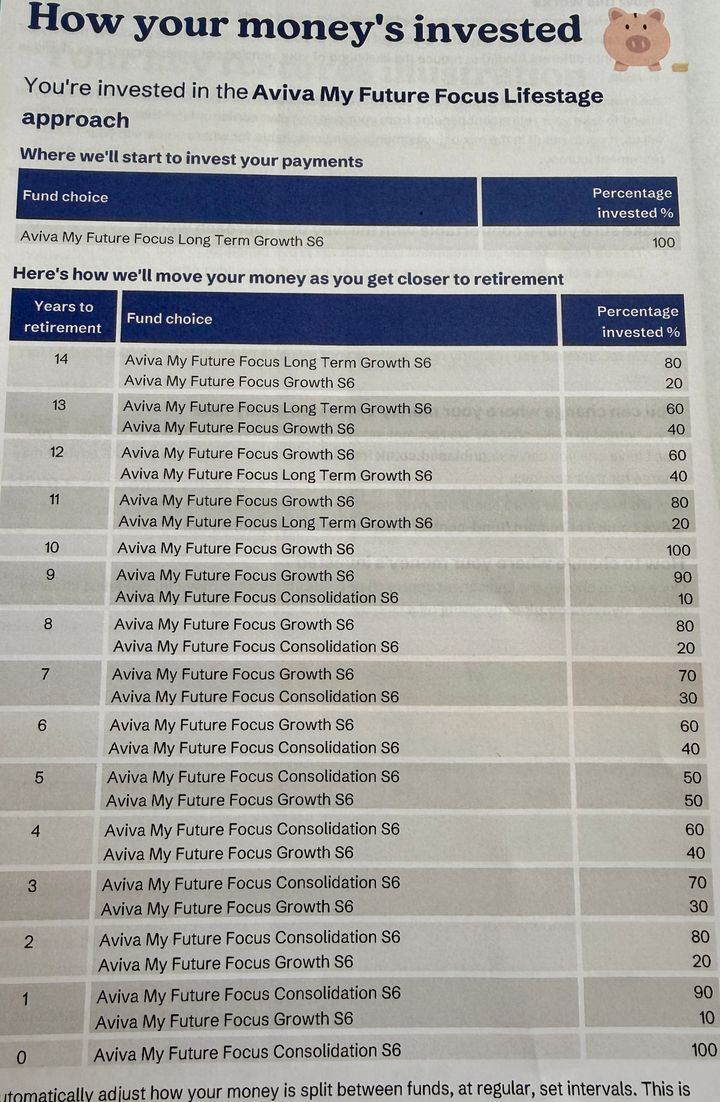

Here's how Aviva invest his money....

My 19yr old son was about 1yr into his mechanical engineering apprenticeship and has just been enrolled into his employers pension. His salary is just short of £15k and from the paperwork he's just received I've established the following..

Employee contributions @3% (£39 gross) - I'm encouraging him to increase this to take advantage of employer contributions

Employer contributions £23

Annual Fund Charge - 0.3%

Additional Yearly Charge - 0%

Fund Manager Expense Charge - 0%

Here's how Aviva invest his money....

The Gauge said:

Anyone able to comment on how good/bad the Aviva My Future Long Term Growth S6 pension plan is please?

My 19yr old son was about 1yr into his mechanical engineering apprenticeship and has just been enrolled into his employers pension.

At that age / investing horizon, I think my advice would be to put as much in as he can - At least to always take the "free money" / employer matched amount. My 19yr old son was about 1yr into his mechanical engineering apprenticeship and has just been enrolled into his employers pension.

And to then pick whichever fund is most aligned to either "the world" or "the riskiest" depending on attitude to risk - And to try and make sure that the chosen fund option has fund management charges of c~0.3% or lower

It looks on the surface that this one meets those requirements, so it's unlikely to be a move he regrets in the future

Great to be enrolled at that age, both my lads had to wait until aged 22. Fortunately, both took my advice to pay in as much as they had to, to get the maximum employer contributions. My eldest had to up from 3% to 6% for get 6% from his employer, but my youngest pays 8% to get 13% from his employer !!!

Of course the 6% is only 4.8% after tax and the 8% is only 6.4%

Of course the 6% is only 4.8% after tax and the 8% is only 6.4%

That fund appears to be a 'default' life styling fund (de-risking as you get older).

These tend to play it safe.

If it was me, I would swap it for a global equities fund and come back to it when he's in his 50s.

Definitely make sure the contributions are upped to maximise employer contributions too.

These tend to play it safe.

If it was me, I would swap it for a global equities fund and come back to it when he's in his 50s.

Definitely make sure the contributions are upped to maximise employer contributions too.

superpp said:

That fund appears to be a 'default' life styling fund (de-risking as you get older).

These tend to play it safe.

If it was me, I would swap it for a global equities fund and come back to it when he's in his 50s.

Definitely make sure the contributions are upped to maximise employer contributions too.

I'm not entirely sure which type of companies are included in Aviva's 'My Future Focus Long Term Growth' and 'My Future Focus Growth' plans. I'm guessing the former is shares, and the latter is bonds? But which shares and bonds?These tend to play it safe.

If it was me, I would swap it for a global equities fund and come back to it when he's in his 50s.

Definitely make sure the contributions are upped to maximise employer contributions too.

He's onboard with upping his contributions, just need to see how this affects his employers contributions.

I'm going to ask him to speak to his employer about the possibilities of moving it to a Global Index Fund, something like the Vanguard VAFTGAG, but maybe he'll be restricted to an Aviva product? Do employers often allow such a move, or are they normally a one trick pony?

Edited by The Gauge on Friday 10th April 12:09

Many companies will only pay into their approved scheme.

You should be able to move the money around to your chosen funds within the Aviva scheme, but will be restricted to whatever funds they allow.

If the employer won't increase their contributions in line with your son's then I'd question whether he'd be better off saving into an ISA rather than the pension.

You should be able to move the money around to your chosen funds within the Aviva scheme, but will be restricted to whatever funds they allow.

If the employer won't increase their contributions in line with your son's then I'd question whether he'd be better off saving into an ISA rather than the pension.

Nicetobenice said:

Many companies will only pay into their approved scheme.

You should be able to move the money around to your chosen funds within the Aviva scheme, but will be restricted to whatever funds they allow.

If the employer won't increase their contributions in line with your son's then I'd question whether he'd be better off saving into an ISA rather than the pension.

He would still get the tax benefit from paying into the pension, even if the employer doesn't match the uprate on payments.You should be able to move the money around to your chosen funds within the Aviva scheme, but will be restricted to whatever funds they allow.

If the employer won't increase their contributions in line with your son's then I'd question whether he'd be better off saving into an ISA rather than the pension.

It's always a good idea for him to be paying into short and medium term products too, such as an ISA to build up a house deposit fund with government top up and a cash savings account for short term goals and safety nets.

Get in these habits now and it will serve him well for life. Even if it's small amounts at this stage due to his low income.

732NM said:

He would still get the tax benefit from paying into the pension, even if the employer doesn't match the uprate on payments.

It's always a good idea for him to be paying into short and medium term products too, such as an ISA to build up a house deposit fund with government top up and a cash savings account for short term goals and safety nets.

Get in these habits now and it will serve him well for life. Even if it's small amounts at this stage due to his low income.

This is true but also he's paying basic rate tax on a small amount of income.It's always a good idea for him to be paying into short and medium term products too, such as an ISA to build up a house deposit fund with government top up and a cash savings account for short term goals and safety nets.

Get in these habits now and it will serve him well for life. Even if it's small amounts at this stage due to his low income.

He will pay tax on the way out when he takes his pension

I agree that it's good to get into these habits

TwigtheWonderkid said:

Great to be enrolled at that age, both my lads had to wait until aged 22. Fortunately, both took my advice to pay in as much as they had to, to get the maximum employer contributions. My eldest had to up from 3% to 6% for get 6% from his employer, but my youngest pays 8% to get 13% from his employer !!!

Of course the 6% is only 4.8% after tax and the 8% is only 6.4%

What do you mean by “after tax” ? Of course the 6% is only 4.8% after tax and the 8% is only 6.4%

My company use Aviva and the standard fund our pensions are put in is the Future Focus Growth S6, im not sure how that compares to the Long term growth one youre sons starting in.

Its pretty simple on the app and website to look at all the funds available and risk levels and choose something different.

I moved 50% of mine into 2 other riskier funds and over the last 4 or 5 years they have done better than the original. However hard trump has tried to cock it up.

Its pretty simple on the app and website to look at all the funds available and risk levels and choose something different.

I moved 50% of mine into 2 other riskier funds and over the last 4 or 5 years they have done better than the original. However hard trump has tried to cock it up.

All info here

https://www.aviva.co.uk/business/workplace-pension...

Nothing wrong with it at his age but, there may be better funds to invest in.

Info on other funds here

https://www.fundslibrary.co.uk/FundsLibrary.Brande...

https://www.aviva.co.uk/business/workplace-pension...

Nothing wrong with it at his age but, there may be better funds to invest in.

Info on other funds here

https://www.fundslibrary.co.uk/FundsLibrary.Brande...

Nicetobenice said:

Many companies will only pay into their approved scheme.

You should be able to move the money around to your chosen funds within the Aviva scheme, but will be restricted to whatever funds they allow.

If the employer won't increase their contributions in line with your son's then I'd question whether he'd be better off saving into an ISA rather than the pension.

No way.You should be able to move the money around to your chosen funds within the Aviva scheme, but will be restricted to whatever funds they allow.

If the employer won't increase their contributions in line with your son's then I'd question whether he'd be better off saving into an ISA rather than the pension.

SIPP would be the sensible alternative, especially if 40%+ tax payer - the income tax relief gains are huge.

fat80b said:

At that age / investing horizon, I think my advice would be to put as much in as he can - At least to always take the "free money" / employer matched amount.

I always thought this, take the employer contributions seems like a no brainer.However I just did some rough calculations and if I got 10% annual returns on a SIPP and 5% on the employer pension after 30 years I'd be 61% better off with the SIPP. So I think it depends on how good the fund options are on the employer pension and the employer contribution %.

Edited to add it's only after 18 years and £100k that the SIPP overtakes the employer pension. By then I would have left and moved the employer pension into the SIPP anyway.

A few years ago, in a previous job someone opted out of a final salary scheme. I would have told her she is crazy opting out, but she was a horrible person.

Edited by Josemartinez on Friday 10th April 14:38

Josemartinez said:

A few years ago, in a previous job someone opted out of a final salary scheme. I would have told her she is crazy opting out, but she was a horrible person.

Someone I know opted out of a very very good final salary public sector pension, and instead remortgaged and bought 2 x rental houses.He gave up a receiving a future annual pension at age 55 of around £23k with a lump sum of £170k

I thought he was mad to do so, but I suppose time will tell.

Edited by The Gauge on Friday 10th April 15:39

The Gauge said:

superpp said:

That fund appears to be a 'default' life styling fund (de-risking as you get older).

These tend to play it safe.

If it was me, I would swap it for a global equities fund and come back to it when he's in his 50s.

Definitely make sure the contributions are upped to maximise employer contributions too.

I'm going to ask him to speak to his employer about the possibilities of moving it to a Global Index Fund, something like the Vanguard VAFTGAG, but maybe he'll be restricted to an Aviva product? Do employers often allow such a move, or are they normally a one trick pony?These tend to play it safe.

If it was me, I would swap it for a global equities fund and come back to it when he's in his 50s.

Definitely make sure the contributions are upped to maximise employer contributions too.

Edited by The Gauge on Friday 10th April 12:09

Went through similar with my son a couple of years back and he told me earlier this year his fund took a marked upturn following the changes.

The Gauge said:

Someone I know opted out of a very very good final salary public sector pension, and instead bought 2 x rental houses.

He gave up a receiving a future annual pension at age 55 of around £23k with a lump sum of £170k

I thought he was mad to do so, but I suppose time will tell.

Hm maybe he was right. He gave up a receiving a future annual pension at age 55 of around £23k with a lump sum of £170k

I thought he was mad to do so, but I suppose time will tell.

This lady would have been contributing 5% of her salary which would have been around £1400 a year Seems like a good deal, £1400 a year for a local government final salary pension.

Gassing Station | Finance | Top of Page | What's New | My Stuff