Investing £200k for £500/month income?

Discussion

As a starting point for researching how to achieve a £500/month income from and investment of £200k I've been playing around on GhatGTP to see what it says

I'm considering an option like this to top up my pension when I retire next year, bridging the 12yr gap from retiring at age 55 and receiving state pension age 67. Does this seem accurate enough to start doing further research, or a load of complete codswallop?

1. Global equity income 35% (£70,000)

Vanguard FTSE All-World High Dividend Yield UCITS ETF

Yield: ~3.2%?Income: ~£2,240

Core growth + dividends

2. Bonds 25% (£50,000)

Vanguard Global Bond Index Fund Hedged

Yield: ~2.5%?Income: ~£1,250

Stability + smoother ride

3. Property (REITs) 20% (£40,000)

iShares UK Property UCITS ETF

Yield: ~4.5%?Income: ~£1,800

Higher income + inflation hedge

4. Infrastructure 20% (£40,000)

Greencoat UK Wind

Yield: ~5 6%?Income: ~£2,200

Reliable, often inflation-linked income

Total income

Estimated income: ~£7,500/year

That s about £625/month

How you use it

Take £500/month

Withdraw: £6,000/year

Leave ~£1,500 surplus invested

I'm considering an option like this to top up my pension when I retire next year, bridging the 12yr gap from retiring at age 55 and receiving state pension age 67. Does this seem accurate enough to start doing further research, or a load of complete codswallop?

1. Global equity income 35% (£70,000)

Vanguard FTSE All-World High Dividend Yield UCITS ETF

Yield: ~3.2%?Income: ~£2,240

Core growth + dividends

2. Bonds 25% (£50,000)

Vanguard Global Bond Index Fund Hedged

Yield: ~2.5%?Income: ~£1,250

Stability + smoother ride

3. Property (REITs) 20% (£40,000)

iShares UK Property UCITS ETF

Yield: ~4.5%?Income: ~£1,800

Higher income + inflation hedge

4. Infrastructure 20% (£40,000)

Greencoat UK Wind

Yield: ~5 6%?Income: ~£2,200

Reliable, often inflation-linked income

Total income

Estimated income: ~£7,500/year

That s about £625/month

How you use it

Take £500/month

Withdraw: £6,000/year

Leave ~£1,500 surplus invested

Edited by The Gauge on Saturday 18th April 17:49

£500 per month fixed or index linked for the next 12 years?

Gross or net of any taxes?

An investment of £126,000 into UK government gilt TR38 will pay you guaranteed fixed gross interest of £3000 every 6 months (ie. £500 pm) until maturity in 2038 when you get roughly £126k back.

Gross or net of any taxes?

An investment of £126,000 into UK government gilt TR38 will pay you guaranteed fixed gross interest of £3000 every 6 months (ie. £500 pm) until maturity in 2038 when you get roughly £126k back.

Edited by LeoSayer on Saturday 18th April 18:19

It largely depends on what your attitude to risk is. Looking at the yields is all very well, but how would you feel if the value of the underlying capital dropped?

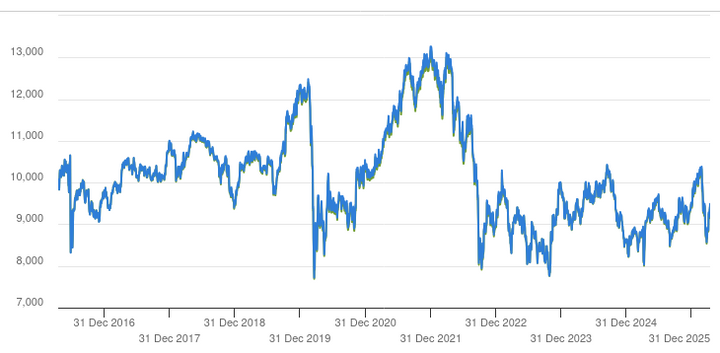

Take a look at the last ten years' performance for that property ETF, for example. It suggests that you'll have to strap yourself in, because it's going to be a bumpy ride.

By comparison, for an (almost) risk-free experience, you can currently get a five-year fixed-rate savings bond at 4.58% that pays interest monthly. The risk is inflation erosion.

I'd also consider what type of income (dividends vs. savings interest) suits your personal income tax situation better. Or is another solution likely to be more tax efficient (e.g. buying gilts directly)?

Take a look at the last ten years' performance for that property ETF, for example. It suggests that you'll have to strap yourself in, because it's going to be a bumpy ride.

By comparison, for an (almost) risk-free experience, you can currently get a five-year fixed-rate savings bond at 4.58% that pays interest monthly. The risk is inflation erosion.

I'd also consider what type of income (dividends vs. savings interest) suits your personal income tax situation better. Or is another solution likely to be more tax efficient (e.g. buying gilts directly)?

Couple of ideas.

1/ Switch global bonds for UK gilts - an intermediate gilt ETF like VGOV (approx +4.6%). Gilts are a little more volatile than the global fund but the income is higher - just my personal opinion but I don't think you need to diversify too much with IG bonds. You want the higher 'income' - just choose a fund to suit your duration.

2/ Look at FTSE U.K. Equity Income Index Fund (VUKEIII) (approx +4.0%)

3/ Might be worth watching this vid - "Smart investors use these investments for income - here’s how"

https://www.youtube.com/watch?v=-zjtrTa9ODc

https://www.theaic.co.uk/income-finder/dividend-he...

1/ Switch global bonds for UK gilts - an intermediate gilt ETF like VGOV (approx +4.6%). Gilts are a little more volatile than the global fund but the income is higher - just my personal opinion but I don't think you need to diversify too much with IG bonds. You want the higher 'income' - just choose a fund to suit your duration.

2/ Look at FTSE U.K. Equity Income Index Fund (VUKEIII) (approx +4.0%)

3/ Might be worth watching this vid - "Smart investors use these investments for income - here’s how"

https://www.youtube.com/watch?v=-zjtrTa9ODc

https://www.theaic.co.uk/income-finder/dividend-he...

STRC (preferred equity) currently pays 11.5% (, annually paid mthly - soon to switch to 2x a mth) paid as a return of capital so no CGT to pay til the original principle has been fully 'covered' by the div's received. If you're not a believer in bitcoin and believe BTC will go to zero - then it's a non-starter. If you're not in that camp, might be worth some research & allocation. It's aim is to be pegged as close to $100 as poss, so tends to trade between 100.01 and 99 - although with them moving to 2 div payment days per mth, i'd imagine it'll stay adjacent to it's 'peg'. In rough terms, with the fluctuation in FX - worst month was a .67p per share, and last mths was .70; £20k'ish yields £170'ish a mth.

Quantum State said:

NS&I Guaranteed Income Bonds for a year at 4%

£200k @4% return would give me £550/m after tax (20%).I realise inflation would eat away at any gains but by topping up my pension this way the benefit to me would be ensuring I never have to work again if I choose not to. If I choose to return to work then I can reinvest the capital elsewhere.

I guess the decision to make is whether I want to have some element of risk for the chance of a higher return.

The Gauge said:

Quantum State said:

NS&I Guaranteed Income Bonds for a year at 4%

£200k @4% return would give me £550/m after tax (20%).I realise inflation would eat away at any gains but by topping up my pension this way the benefit to me would be ensuring I never have to work again if I choose not to. If I choose to return to work then I can reinvest the capital elsewhere.

I guess the decision to make is whether I want to have some element of risk for the chance of a higher return.

Quantum State said:

Ahh yes sorry I don t pay tax !

No worries, even after tax I still get the £500/m I need

The NS&I Guaranteed fixed return 12 month bond is nice and simple, but I'll keep researching gilts as I don't fully understand them yet, as in secondary markets and predicting future inflation etc.

LeoSayer said:

£500 per month fixed or index linked for the next 12 years?

Gross or net of any taxes?

An investment of £126,000 into UK government gilt TR38 will pay you guaranteed fixed gross interest of £3000 every 6 months (ie. £500 pm) until maturity in 2038 when you get roughly £126k back.

£200k would buy approximately 164000 Newcastle building society PIBS returning 8% or just over £13k a year. Gross or net of any taxes?

An investment of £126,000 into UK government gilt TR38 will pay you guaranteed fixed gross interest of £3000 every 6 months (ie. £500 pm) until maturity in 2038 when you get roughly £126k back.

Edited by LeoSayer on Saturday 18th April 18:19

Slightly higher risk than government gilts though.

hodjie said:

We have an investment with Prufund , organised by hsbc wealth management & you can take a 5 % monthly payment tax free , which would get you more then what you want .

Per month and of the original investment quantum or a regular withdrawal monthly up to 5% of any “growth “ ?I have some IIB ‘s which work in a similar fashion but they are limited to 4% annual withdrawals of the original investment ( you can carry over any unused percentages to the following year and so on ).

alscar said:

hodjie said:

We have an investment with Prufund , organised by hsbc wealth management & you can take a 5 % monthly payment tax free , which would get you more then what you want .

Per month and of the original investment quantum or a regular withdrawal monthly up to 5% of any growth ?I have some IIB s which work in a similar fashion but they are limited to 4% annual withdrawals of the original investment ( you can carry over any unused percentages to the following year and so on ).

Mr Pointy said:

alscar said:

hodjie said:

We have an investment with Prufund , organised by hsbc wealth management & you can take a 5 % monthly payment tax free , which would get you more then what you want .

Per month and of the original investment quantum or a regular withdrawal monthly up to 5% of any growth ?I have some IIB s which work in a similar fashion but they are limited to 4% annual withdrawals of the original investment ( you can carry over any unused percentages to the following year and so on ).

Mr Pointy said:

What sort of investments are these & what is an IIB? Not paying tax on any growth is interesting.

International Investment Bonds - Dublin. There is tax due on growth but the original ( my money anyway ) can be withdrawn each year tax free.

Comes with “ free “ Life Insurance.

My point ( maybe expressed badly ) is that a withdrawal

allowance of 5% monthly of the original capital won’t last very long !

C69 said:

If they're talking about onshore or offshore investment bonds, then the 5% annual withdrawal is technically 'tax deferred' rather than 'tax free'.

The 5% of original investment if taken is technically tax free but should really be called tax not applicable as it’s simply your original investment monies being taken. The Gauge said:

As a starting point for researching how to achieve a £500/month income from and investment of £200k I've been playing around on GhatGTP to see what it says

I'm considering an option like this to top up my pension when I retire next year, bridging the 12yr gap from retiring at age 55 and receiving state pension age 67. Does this seem accurate enough to start doing further research, or a load of complete codswallop?

1. Global equity income 35% (£70,000)

Vanguard FTSE All-World High Dividend Yield UCITS ETF

Yield: ~3.2%?Income: ~£2,240

Core growth + dividends

2. Bonds 25% (£50,000)

Vanguard Global Bond Index Fund Hedged

Yield: ~2.5%?Income: ~£1,250

Stability + smoother ride

3. Property (REITs) 20% (£40,000)

iShares UK Property UCITS ETF

Yield: ~4.5%?Income: ~£1,800

Higher income + inflation hedge

4. Infrastructure 20% (£40,000)

Greencoat UK Wind

Yield: ~5 6%?Income: ~£2,200

Reliable, often inflation-linked income

Total income

Estimated income: ~£7,500/year

That s about £625/month

How you use it

Take £500/month

Withdraw: £6,000/year

Leave ~£1,500 surplus invested

I'm going to do something not too dissimilar. My observations are the yield on that iShares REIT ETF is low relative to what you can get on 2 or 3 of the higher yielding big name individual REITs (e.g. Land Securities, British Land) which are over 6%. The fees on that iShares ETF may seem low but it is on top of the REITs held within it.I'm considering an option like this to top up my pension when I retire next year, bridging the 12yr gap from retiring at age 55 and receiving state pension age 67. Does this seem accurate enough to start doing further research, or a load of complete codswallop?

1. Global equity income 35% (£70,000)

Vanguard FTSE All-World High Dividend Yield UCITS ETF

Yield: ~3.2%?Income: ~£2,240

Core growth + dividends

2. Bonds 25% (£50,000)

Vanguard Global Bond Index Fund Hedged

Yield: ~2.5%?Income: ~£1,250

Stability + smoother ride

3. Property (REITs) 20% (£40,000)

iShares UK Property UCITS ETF

Yield: ~4.5%?Income: ~£1,800

Higher income + inflation hedge

4. Infrastructure 20% (£40,000)

Greencoat UK Wind

Yield: ~5 6%?Income: ~£2,200

Reliable, often inflation-linked income

Total income

Estimated income: ~£7,500/year

That s about £625/month

How you use it

Take £500/month

Withdraw: £6,000/year

Leave ~£1,500 surplus invested

Edited by The Gauge on Saturday 18th April 17:49

I have a couple of infrastructure investment trusts. Picking just one adds a bit of concentration risk, particularly if Reform have a bad impact on windfarms or the management of the trust is poor. I have held Greencoat previously but not at present.

There are plenty of Dividend Hero investment trusts, and a couple of global equity ETFs to cover number 1 that offer higher yields than that Vanguard FTSE All-World High Dividend Yield, although I do hold VHYL in amongst the mix.

On bonds, with your approx 12 year horizon you could probably do fine snapping up individual gilts such as T41F, locking in a juicy 5.25% at current price with no fees

https://www.hl.co.uk/shares/shares-search-results/...

Admittedly all of the above is a bit of a faff to do for smaller portfolios (you might only have £10k-£20k in each holding), but for me the goal is to blend a combination of high current yields with some element of dividend growth or inflation indexation (hence REITs/infrastructure) for inflation protection. There is almost always a compromise between the two.

I think my current portfolio yield is at least 5.25%, probably a bit more.

I've added in some high yield bond stuff and even option based income ETFs to boost current yield a bit. I don't even care too much about NAV decay with them but it has to be balanced with the growers.

Actually this popped up in my feed today regarding 5 assets, I thought it was a reasonable overview

https://www.youtube.com/watch?v=mqDoGZ8BPc4

And just highlights how crap BTL property has become in comparison. I've had to help a relative who is sick of earning about 2% net yield by the time you take into account fixing boilers, showers, pet damage, tenants not paying, etc. The new laws coming in on the 1st May aren't going to help, although the coming landlord exodus could at least be good for first time buyers. But that deserves a thread of its own.

Edited by WayOutWest on Monday 20th April 16:31

Some useful replies, thanks.

As for gilts, help me understand them please...

1) They are called gilts because originally the edges of the document were guilted gold?

2) They come about because the government want to borrow some (your) money

3) You lend the government some money fro an agreed term and they pay you a fixed rate of interest (called coupons) throughout the term, and then hand your original stake back

4) You can buy them on the Primary market (when the government first announce them being available), or you can buy them on the Secondary market which is when the original owner decide to sell them on

5) You can sell them on to other buyers at any time, and the new buyer then owns them as you once did and receives the coupons, but part of the agreed term will have already passed so they won't have as long to wait for the (your) original stake back

6) Various factors such as changes in inflation affect whether you might want to sell them on, or buy on secondary market.

Whether you'd want to buy on primary or secondary market, the why you'd want to sell them seems a bit confusing to me at this stage, whereas bonds are quite straight forward in my head.

As for gilts, help me understand them please...

1) They are called gilts because originally the edges of the document were guilted gold?

2) They come about because the government want to borrow some (your) money

3) You lend the government some money fro an agreed term and they pay you a fixed rate of interest (called coupons) throughout the term, and then hand your original stake back

4) You can buy them on the Primary market (when the government first announce them being available), or you can buy them on the Secondary market which is when the original owner decide to sell them on

5) You can sell them on to other buyers at any time, and the new buyer then owns them as you once did and receives the coupons, but part of the agreed term will have already passed so they won't have as long to wait for the (your) original stake back

6) Various factors such as changes in inflation affect whether you might want to sell them on, or buy on secondary market.

Whether you'd want to buy on primary or secondary market, the why you'd want to sell them seems a bit confusing to me at this stage, whereas bonds are quite straight forward in my head.

Edited by The Gauge on Monday 20th April 21:17

Gassing Station | Finance | Top of Page | What's New | My Stuff