Where to stick 25k for 18 months

Discussion

Had what (to me) is a faily decent sum of money recently due to a few things going very well and im after advice as where to stick it...

In total, it is 40k and realistically, I'm looking to spend 5k of it in bits and peices over the next year, 10k to sit in my business account to create a bit more liquidity, remove the need for my overdraft facilities (been slowly working it down so that I can work all in the black, and im finally there)

That leaves me with 25k which me and the Mrs have decided can go towards a house deposit when we start looking in 18 months (along with anymore we save in that time) so in the interim, i'm after advice as to where would be the best place to stick 25k for a year and a half to 2 years that would produce the best return.

Normally, my attitude to risk, is fairly good, I take those kind of decisions with my business daily, but since this money is savings for bricks and mortar my attitude is a lot more conservative as by that time it may be for a larger family than 2

TIA!

In total, it is 40k and realistically, I'm looking to spend 5k of it in bits and peices over the next year, 10k to sit in my business account to create a bit more liquidity, remove the need for my overdraft facilities (been slowly working it down so that I can work all in the black, and im finally there)

That leaves me with 25k which me and the Mrs have decided can go towards a house deposit when we start looking in 18 months (along with anymore we save in that time) so in the interim, i'm after advice as to where would be the best place to stick 25k for a year and a half to 2 years that would produce the best return.

Normally, my attitude to risk, is fairly good, I take those kind of decisions with my business daily, but since this money is savings for bricks and mortar my attitude is a lot more conservative as by that time it may be for a larger family than 2

TIA!

Craikeybaby said:

If it is going to be for your first house deposit, I would look into one of the help to buy/life ISAs, as the government top it when used for a house deposit.

This is a good shout, you'll get a small bonus from the GVT and the safety of a basic ISA...albeit your interest rate before the bonus will probably be less than inflation!As your attitude to risk is good, why not select a decent fund. Just Google the top 10 bought funds in 2016 and they have all done well.

One of the most popular is Fundsmith which has grown:

1 year - 32.53%

3 years - 77.30%

5 years - 110.76%

The fund size is £8.2 bn.

Terry Smith the fund manager who runs the fund invested a further £115m of his own money in September last year. Let's be honest if you didn't have total faith in it, whether you were the fund manager or anyone else, you wouldn't invest such a large sum.

Whilst past performance is of course no guarantee of future performance the underlying investments are very good.

You could of course diversify so as to not put all your eggs in one basket and choose two or three funds and spread your risk.

One of the most popular is Fundsmith which has grown:

1 year - 32.53%

3 years - 77.30%

5 years - 110.76%

The fund size is £8.2 bn.

Terry Smith the fund manager who runs the fund invested a further £115m of his own money in September last year. Let's be honest if you didn't have total faith in it, whether you were the fund manager or anyone else, you wouldn't invest such a large sum.

Whilst past performance is of course no guarantee of future performance the underlying investments are very good.

You could of course diversify so as to not put all your eggs in one basket and choose two or three funds and spread your risk.

Stuart1961 said:

As your attitude to risk is good, why not select a decent fund. Just Google the top 10 bought funds in 2016 and they have all done well.

One of the most popular is Fundsmith which has grown:

1 year - 32.53%

3 years - 77.30%

5 years - 110.76%

The fund size is £8.2 bn.

Terry Smith the fund manager who runs the fund invested a further £115m of his own money in September last year. Let's be honest if you didn't have total faith in it, whether you were the fund manager or anyone else, you wouldn't invest such a large sum.

Whilst past performance is of course no guarantee of future performance the underlying investments are very good.

You could of course diversify so as to not put all your eggs in one basket and choose two or three funds and spread your risk.

So, with an 18-month timescale (and presumably a low risk tolerance, given the planned purpose of the £25k) you'd advocate buying into equity-type risks at close to top of the market?One of the most popular is Fundsmith which has grown:

1 year - 32.53%

3 years - 77.30%

5 years - 110.76%

The fund size is £8.2 bn.

Terry Smith the fund manager who runs the fund invested a further £115m of his own money in September last year. Let's be honest if you didn't have total faith in it, whether you were the fund manager or anyone else, you wouldn't invest such a large sum.

Whilst past performance is of course no guarantee of future performance the underlying investments are very good.

You could of course diversify so as to not put all your eggs in one basket and choose two or three funds and spread your risk.

Still, I guess at least it's not £20k watches that are being suggested like last time....

Hmm...

sidicks said:

Ahbefive said:

Buy a car that doesn't depreciate and enjoy it for 18months. Pointless having no enjoyment out of it by sitting it in the bank. YOLO

Which cars a) don't depreciate (guaranteed), b) have zero bid-offer spread and c) zero running costs?I have 3 cars currently that are doing no depreciating at all, one even appreciating.

sidicks said:

Craikeybaby said:

If it is going to be for your first house deposit, I would look into one of the help to buy/life ISAs, as the government top it when used for a house deposit.

Good advice!The help to buy ISA - Government bonus only on the first £12K, and you can't chuck a big chunk into it, I don't know what the maximums are but it's a lot less than normal ISA, and then you're supposed to save a regular amount per month. You only get the bonus when you go to buy a house so if you don't buy a house with it you won't get owt.

Life ISA - similar to the above, £4k a year limit and you can't get at it until your 50 unless you buy a house with it. Bonus is paid annually so you're hung up on when you buy your house if you want to get the bonus.

They're designed for long term savings or a way of middle class parents tax efficiently putting away for kids in the long run, not as a place to stash cash for a year.

£25k for 18months of so and you require immediate access to the cash? I'd split it into two standard ISAs between you and your mrs and invest in some sort of reasonable risk fund, or split it between some world index tracking fund and an emerging markets tracker. Not risk free over that period of time though.

sidicks said:

So, with an 18-month timescale (and presumably a low risk tolerance, given the planned purpose of the £25k) you'd advocate buying into equity-type risks at close to top of the market?

Still, I guess at least it's not £20k watches that are being suggested like last time....

Hmm...

Without a crystal ball neither you, nor I or anyone else knows that it is the top of the market.Still, I guess at least it's not £20k watches that are being suggested like last time....

Hmm...

As mentioned past performance is no guarantee of the future and I did suggesting spreading the risk.

No risk would be NS&I, e.g. Premium Bonds.

Low risk would be a building society account paying a paltry return.

Medium to High risk will be funds depending upon which fund(s) you select.

I have a considerable sum invested into Fundsmith and continue to add a four figure sum to it every month. In the last two years my profit from Fundsmith has bought me a Group B Homologation Peugeot 205 T16, which has itself increased in value by 30% since I have owned it. So I would have recommended a classic car but then someone will no doubt will tell me that the classic car market is also close to the top of the market.

What you invest in all depends upon your risk appetite is and no two people have the same appetite.

The question to ask yourself is:

"Would I be prepared to lose a substantial part of my investment if the market crashed in the 18 month period ?"

If the answer is no then a fund is not for you !

Stuart1961 said:

Without a crystal ball neither you, nor I or anyone else knows that it is the top of the market.

As mentioned past performance is no guarantee of the future and I did suggesting spreading the risk.

No risk would be NS&I, e.g. Premium Bonds.

Low risk would be a building society account paying a paltry return.

Medium to High risk will be funds depending upon which fund(s) you select.

I have a considerable sum invested into Fundsmith and continue to add a four figure sum to it every month. In the last two years my profit from Fundsmith has bought me a Group B Homologation Peugeot 205 T16, which has itself increased in value by 30% since I have owned it. So I would have recommended a classic car but then someone will no doubt will tell me that the classic car market is also close to the top of the market.

What you invest in all depends upon your risk appetite is and no two people have the same appetite.

The question to ask yourself is:

"Would I be prepared to lose a substantial part of my investment if the market crashed in the 18 month period ?"

If the answer is no then a fund is not for you !

My paltry understanding of investing options based on 3 months of furious research after setting up my SIPP is that Funds like Terry Smiths and Woodfords that have large amounts of money invested in a small number of very high performance companies do better in bear markets, I have some money in both and over the last 4 months of bull market in the UK, World and US indices they've been out performed but in general if you look at the charts they will outperform the trackers if and when we tip the top of this current growth spurt. As mentioned past performance is no guarantee of the future and I did suggesting spreading the risk.

No risk would be NS&I, e.g. Premium Bonds.

Low risk would be a building society account paying a paltry return.

Medium to High risk will be funds depending upon which fund(s) you select.

I have a considerable sum invested into Fundsmith and continue to add a four figure sum to it every month. In the last two years my profit from Fundsmith has bought me a Group B Homologation Peugeot 205 T16, which has itself increased in value by 30% since I have owned it. So I would have recommended a classic car but then someone will no doubt will tell me that the classic car market is also close to the top of the market.

What you invest in all depends upon your risk appetite is and no two people have the same appetite.

The question to ask yourself is:

"Would I be prepared to lose a substantial part of my investment if the market crashed in the 18 month period ?"

If the answer is no then a fund is not for you !

That's not to say Fundsmith or Woodford won't crash - but they won't crash at anywhere near the rate of the general index. But they are at severe risk of one company i.e Microsoft, Apple, Alphabet... having a complete nightmare year (which is a pretty small risk from where I'm sat)

Thanks for your replies!

The car idea...I have an MX5 for the weekend at the moment and have just had a 5 series a few months ago for work and comfort. If another car appeared at the moment the mrs would have a fit, no amount of explaining it would make her understand its not just for me to play around in

I like the idea of splitting between me and the Mrs in an ISA, I already have one that I pay a tiny amount into so will have to check what I have left for this year.

Going to have a look into the funds this evening, so far I have stayed away from funds as any spare cash I had that wasn't meant for somewhere else got reinvested into the business, as explained thats not required now though like it was.

The car idea...I have an MX5 for the weekend at the moment and have just had a 5 series a few months ago for work and comfort. If another car appeared at the moment the mrs would have a fit, no amount of explaining it would make her understand its not just for me to play around in

I like the idea of splitting between me and the Mrs in an ISA, I already have one that I pay a tiny amount into so will have to check what I have left for this year.

Going to have a look into the funds this evening, so far I have stayed away from funds as any spare cash I had that wasn't meant for somewhere else got reinvested into the business, as explained thats not required now though like it was.

MarshPhantom said:

Buy Euros or Dollars.

I did do some trading a few years ago but it didnt go too well to be honest, still have the account open but when I started losing more then I won I stopped investing once I got back down to the break-even point. It's something I have been meaning to return to once I had a bit more knowledge and experience but have never had the time to pick back up.

FredClogs said:

...That's not to say Fundsmith or Woodford won't crash - but they won't crash at anywhere near the rate of the general index...

Fred - even with your considered qualification that's a stretch too far I'm afraid. The funds/strategies to which you refer are fantastic examples of active management that have delivered long term outperformance for holders. However, their structure - particularly the concentration to which you refer - does mean that there are conditions under which drawdowns could exceed those of broad indices. Holders should be aware of this.WindyCommon said:

FredClogs said:

...That's not to say Fundsmith or Woodford won't crash - but they won't crash at anywhere near the rate of the general index...

Fred - even with your considered qualification that's a stretch too far I'm afraid. The funds/strategies to which you refer are fantastic examples of active management that have delivered long term outperformance for holders. However, their structure - particularly the concentration to which you refer - does mean that there are conditions under which drawdowns could exceed those of broad indices. Holders should be aware of this.Anyone who takes financial advice from me is a penis anyway and deserves all they lose

I only read these pages and occasionally interlude my opinions to aid my own confirmation bias.

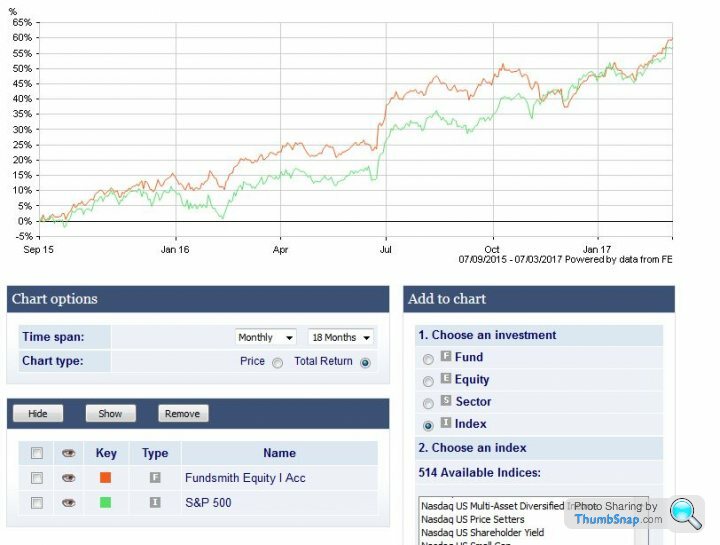

As an illustration of what I meant though this is the Fundsmith vs SP500 chart from the last 18 months (which is the time frame under discussion)

You'll see the dips in the index do correspond to a slightly smaller dip in the managed fund, Dec 2015, Feb 2016, June 2016, Nov 2016 each dip in the index leading to a widening margine to fundsmith as dips a little less and recovers a little quicker and then for some unknown (to me) reason fundsmith tanked on it's arse in Nov/Dec 2016 (suspect more due £/$ as it holds mostly US stock) and hasn't regained the gap to the index through the bull period...

The wider 5 year picture does show Fundsmith only really outperformed the index slightly 2012 to 2015 it was only the year 2015 that fundsmith strode ahead, during the flat/bear market 2015 to 2016.

But Gordon Gecko I am not, I accept.

Gassing Station | Finance | Top of Page | What's New | My Stuff