Which ftse tracker?

Discussion

FWIW said:

I'd like to add a ftse tracking fund to my portfolio so that I maximise my diversification.

I'm thinking ftse 250 rather than 100. How should I choose which one? Or would I be better with some other fund?

I'd prefer to deal with HL to keep my investments together.

1) if you just want a tracker then price should the most important factor.I'm thinking ftse 250 rather than 100. How should I choose which one? Or would I be better with some other fund?

I'd prefer to deal with HL to keep my investments together.

2) 'better' in what way?

I was considering this http://www.hl.co.uk/funds/fund-discounts,-prices--...

But there are so many to choose from! http://www.hl.co.uk/funds/index-tracker-funds/view...

But there are so many to choose from! http://www.hl.co.uk/funds/index-tracker-funds/view...

sidicks said:

1) if you just want a tracker then price should the most important factor.

Ginge R said:

Don't forget tracking error, too. There are some cheap dogs out there.

Whilst buying a low-cost tracker can be a good option it's not as simple as might be expected. Ginge is correct to draw your attention to tracking error. If you look at returns from index tracking funds, many of them underperform the indices they track. This underperformance - which results from the replication strategies employed - can more than erode the impact of price differentials.

It is hard to assess what the tracking error for a given fund might be on a prospective basis, especially with a broader index like the 250.

My view is that the specialist houses with deeper resources (Vanguard is a prime example) are more likely to be deliver accurate tracking in the long run, so perhaps start there whilst keeping one eye on costs.

WindyCommon said:

Whilst buying a low-cost tracker can be a good option it's not as simple as might be expected.

Ginge is correct to draw your attention to tracking error. If you look at returns from index tracking funds, many of them underperform the indices they track. This underperformance - which results from the replication strategies employed - can more than erode the impact of price differentials.

It is hard to assess what the tracking error for a given fund might be on a prospective basis, especially with a broader index like the 250.

My view is that the specialist houses with deeper resources (Vanguard is a prime example) are more likely to be deliver accurate tracking in the long run, so perhaps start there whilst keeping one eye on costs.

It's a fair point, but tracking error can work for or against you! Ginge is correct to draw your attention to tracking error. If you look at returns from index tracking funds, many of them underperform the indices they track. This underperformance - which results from the replication strategies employed - can more than erode the impact of price differentials.

It is hard to assess what the tracking error for a given fund might be on a prospective basis, especially with a broader index like the 250.

My view is that the specialist houses with deeper resources (Vanguard is a prime example) are more likely to be deliver accurate tracking in the long run, so perhaps start there whilst keeping one eye on costs.

I would agree that focussing on an established name at reasonable cost is likely to be better than an unknown manager at the lowest cost!

sidicks said:

It's a fair point, but tracking error can work for or against you!

I would agree that focussing on an established name at reasonable cost is likely to be better than an unknown manager at the lowest cost!

Interestingly, tracking error nearly always works against investors in practice. When I last analysed the dataset for FTSE100 index trackers, only a couple of them outperformed the index over any period longer than 12 months. I suspect that this is an inevitable consequence of implementation (specifically trading) costs which are not today disclosed as components of the OCF.I would agree that focussing on an established name at reasonable cost is likely to be better than an unknown manager at the lowest cost!

Of course when tracking error works for you, the quants involved will look to re-christen it as "implementation efficiencies arising from their class-leading model"...

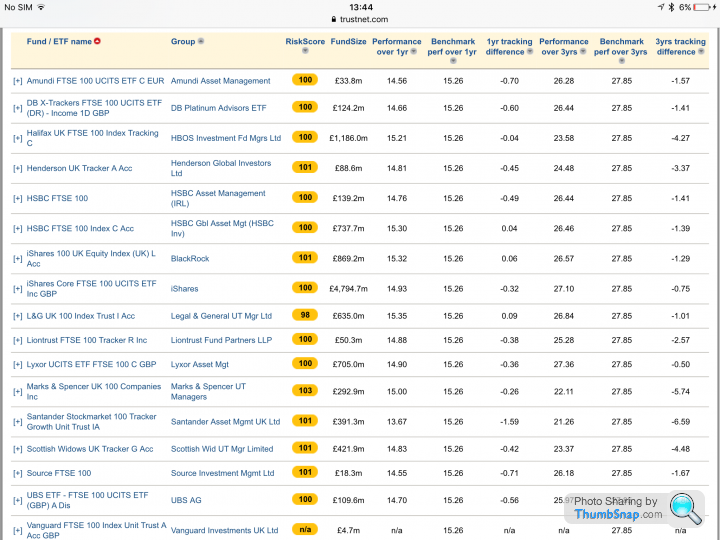

Added: take a look at the last column of the table below...

Edited by WindyCommon on Tuesday 8th August 14:00

From memory, L&G used to be pretty good when it came to tracking error and price with the FTSE.

Edited to say I've just seen the table above - Santander and M&S (which used to be provided by M&G, not sure if this is still the case) are absolutely shocking - but I have a feeling their 1% annual fee contributes massively to this!

Edited to say I've just seen the table above - Santander and M&S (which used to be provided by M&G, not sure if this is still the case) are absolutely shocking - but I have a feeling their 1% annual fee contributes massively to this!

Edited by JulianPH on Tuesday 8th August 16:36

WindyCommon said:

sidicks said:

NickCQ said:

Plus income from stock lending...

Yes, that's how most tracker funds offset their trading costs, I think?Black Rock, Vanguard Group and Fidelity Investments lend, and lend heavily. Most others do, I'm not sure in what capacity of class, though. Black Rock especially, makes a significant sum. The bugbear has always been that it should be the shareholders of the fund who should be rewarded, and not the fund manager's balance sheet.

Ginge R said:

Black Rock, Vanguard Group and Fidelity Investments lend, and lend heavily. Most others do, I'm not sure in what capacity of class, though. Black Rock especially, makes a significant sum. The bugbear has always been that it should be the shareholders of the fund who should be rewarded, and not the fund manager's balance sheet.

GingeAre you sure it's not the fund's shareholders that get the benefit of that stock lending? The fund manager's balance should be entirely separate (unless they also own units in the fund).

No, I'm pretty certain that the vast majority went to the manager. Some may have gone back into the pot, but certainly it was a disproportionately small amount. That was my understanding (particularly in regard to Black Rock) although it was quite a few years ago, and I'm quite happy to be corrected in the event my memory is stuffed.

Edit: Some context from 2013. Things may have changed?

http://citywire.co.uk/wealth-manager/news/pension-...

Edit 2: And more, from 2011. As I said, things may have changed now.

https://www.theguardian.com/business/2011/aug/31/s...

Edit: Some context from 2013. Things may have changed?

http://citywire.co.uk/wealth-manager/news/pension-...

Edit 2: And more, from 2011. As I said, things may have changed now.

https://www.theguardian.com/business/2011/aug/31/s...

Edited by Ginge R on Wednesday 9th August 09:24

Edited by Ginge R on Wednesday 9th August 09:30

Ginge R said:

No, I'm pretty certain that the vast majority went to the manager. Some may have gone back into the pot, but certainly it was a disproportionately small amount. That was my understanding (particularly in regard to Black Rock) although it was quite a few years ago, and I'm quite happy to be corrected in the event my memory is stuffed.

Edit: Some context from 2013. Things may have changed?

http://citywire.co.uk/wealth-manager/news/pension-...

Edit 2: And more, from 2011. As I said, things may have changed now.

https://www.theguardian.com/business/2011/aug/31/s...

Those articles appear to suggest that 60-65% went to the shareholders and the balance went to the manager in lieu of charging actual fees for the lending process.Edit: Some context from 2013. Things may have changed?

http://citywire.co.uk/wealth-manager/news/pension-...

Edit 2: And more, from 2011. As I said, things may have changed now.

https://www.theguardian.com/business/2011/aug/31/s...

Edited by Ginge R on Wednesday 9th August 09:24

Edited by Ginge R on Wednesday 9th August 09:30

Which is quite different than 'the vast majority' going to the fund manager!

sidicks said:

Ginge R said:

Black Rock, Vanguard Group and Fidelity Investments lend, and lend heavily. Most others do, I'm not sure in what capacity of class, though. Black Rock especially, makes a significant sum. The bugbear has always been that it should be the shareholders of the fund who should be rewarded, and not the fund manager's balance sheet.

GingeAre you sure it's not the fund's shareholders that get the benefit of that stock lending? The fund manager's balance should be entirely separate (unless they also own units in the fund).

It's an area fraught with regulatory and PR risk, so many managers simply don't bother even if they have the correct prospectus powers.

sidicks said:

Those articles appear to suggest that 60-65% went to the shareholders and the balance went to the manager in lieu of charging actual fees for the lending process.

Which is quite different than 'the vast majority' going to the fund manager!

You're quite correct, it was c40%. What remains unclear is whether or not, when lending to another fund within its own stable, the fund manager also collected arrangement/brokerage fees. If that was the case, we might assume that amount was higher - in what amount, I don't know (I don't imagine anyone does, hence my caveat). In these days of piercing political and regulatory scrutiny, you'd be a brave fund manager to try it - i.e, just because you can do it, doesn't mean you should.Which is quite different than 'the vast majority' going to the fund manager!

Gassing Station | Finance | Top of Page | What's New | My Stuff