Low Valuation - Insurance write off

Discussion

porterpainter said:

If you wanted your car insured for a particular amount, you should have bought a policy with an agreed value for the vehicle. Yes it will cost more, but it avoids this sort of issue.

No help to the OP right now I guess, but maybe for when you take out future insurance for a car you deem to be much better than average.

+1No help to the OP right now I guess, but maybe for when you take out future insurance for a car you deem to be much better than average.

if someone has a extraordinary car relative to the market, then an agreed value policy needs to be considered.

Not what you want to hear OP, but it's a simple truth.

Hope you get it sorted regardless.

MarkGolf said:

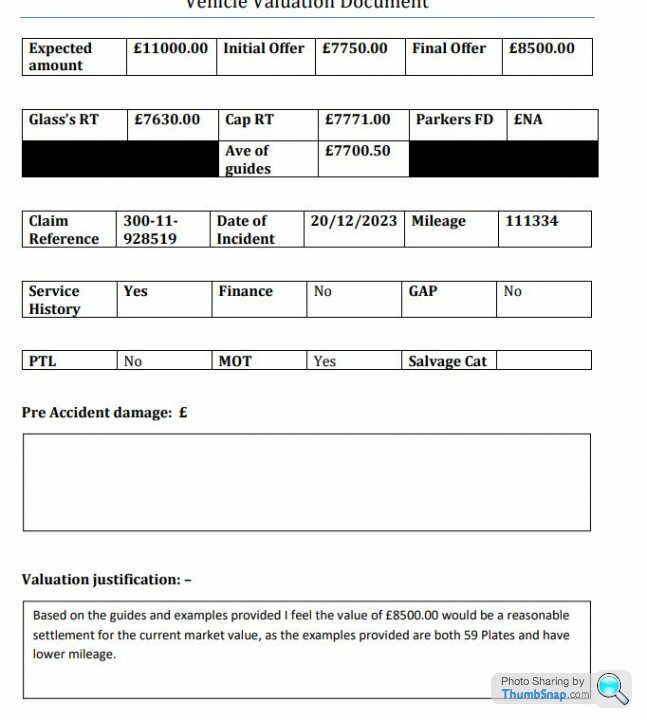

I just noticed an attachment on the email sent.

Please see below

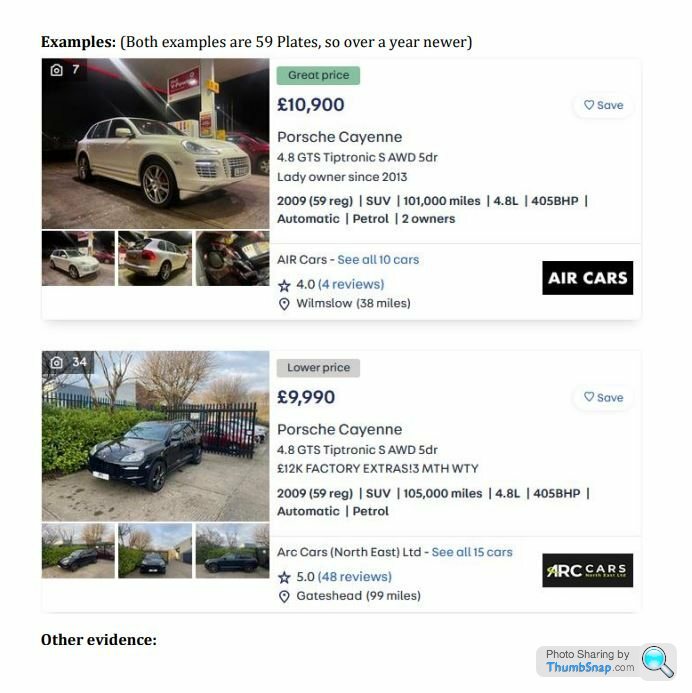

The have based it on those being a 59 plate, regardless of their condition, the black one is a dog and autotrader even states is it £1.3k under the average value.

The white one has also been reduced in price since my screenshot, aren't they meant to take the value at time of accident, which was before christmas, so not fair to use a reduced price now?

So by his logic, "Both examples are over a year newer" - So in a years time you expect them to have depreciated another 20-30%? lol! Where is the logic

Sorry but there is no chance anyone would have my car on the market for £8.5k or even accept that little for it, no way!

I still have not replied but trying to compile something..

Before I saw the above, I had written this;

I hope this email finds you well. I appreciate your efforts in assessing the valuation for my 2008 Porsche Cayenne GTS following the recent accident. However, after careful consideration and market research, I believe that the offered value of £8,500 does not accurately reflect the true market value of my vehicle at time of accident.

I have attached evidence of recent online listings for similar models, which I do not appear in the same condition or as well optioned, which consistently show a market value well above the offered amount. My car has been meticulously maintained, has a full service history, and is in immaculate condition, factors that contribute significantly to its overall value. I cannot purchase a similar vehicle for the amount you are offering.

I kindly request a thorough review of the valuation, taking into account the provided evidence again. I believe a fair and equitable settlement should be in line with the current market value for my vehicle.

If necessary, I am prepared to escalate this matter to the Financial Ombudsman Service for a third-party review. I trust that we can reach a mutually agreeable resolution before considering such steps.

I look forward to your prompt attention to this matter and a revised valuation that accurately reflects the fair market value of my vehicle.

Thank you for your understanding and cooperation.

Sincerely,

AT's price guide is easy to skew with a rare car. Please see below

The have based it on those being a 59 plate, regardless of their condition, the black one is a dog and autotrader even states is it £1.3k under the average value.

The white one has also been reduced in price since my screenshot, aren't they meant to take the value at time of accident, which was before christmas, so not fair to use a reduced price now?

So by his logic, "Both examples are over a year newer" - So in a years time you expect them to have depreciated another 20-30%? lol! Where is the logic

Sorry but there is no chance anyone would have my car on the market for £8.5k or even accept that little for it, no way!

I still have not replied but trying to compile something..

Before I saw the above, I had written this;

I hope this email finds you well. I appreciate your efforts in assessing the valuation for my 2008 Porsche Cayenne GTS following the recent accident. However, after careful consideration and market research, I believe that the offered value of £8,500 does not accurately reflect the true market value of my vehicle at time of accident.

I have attached evidence of recent online listings for similar models, which I do not appear in the same condition or as well optioned, which consistently show a market value well above the offered amount. My car has been meticulously maintained, has a full service history, and is in immaculate condition, factors that contribute significantly to its overall value. I cannot purchase a similar vehicle for the amount you are offering.

I kindly request a thorough review of the valuation, taking into account the provided evidence again. I believe a fair and equitable settlement should be in line with the current market value for my vehicle.

If necessary, I am prepared to escalate this matter to the Financial Ombudsman Service for a third-party review. I trust that we can reach a mutually agreeable resolution before considering such steps.

I look forward to your prompt attention to this matter and a revised valuation that accurately reflects the fair market value of my vehicle.

Thank you for your understanding and cooperation.

Sincerely,

Edited by MarkGolf on Friday 19th January 11:34

Edited by MarkGolf on Friday 19th January 11:38

We often discuss car values on here and people keep ignoring valuation guides and paying well over what valuation guides say the car is worth.

Like the position your are in just now the overinflated advertised prices aren't taken into consideration by the insurance company. They will look at the valuation guides.

I've never understood why insurance companies can used these 'guides' as their source for valuations...aren't the guides linked to trade-in prices, not what Joe Bloggs can buy a car for? Surely the answer to the OP issue is to settle somewhere in between their initial valuation [based on these BS guides] and the perhaps inflated dealer prices?

Driver101 said:

AT's price guide is easy to skew with a rare car.

We often discuss car values on here and people keep ignoring valuation guides and paying well over what valuation guides say the car is worth.

Like the position your are in just now the overinflated advertised prices aren't taken into consideration by the insurance company. They will look at the valuation guides.

As I've said above, aren't the 'valuation guides' an unfair source of prices, as they aren't an indication of the price a punter would have to pay to buy said car? How are insurance companies allowed to use the guides in this way?We often discuss car values on here and people keep ignoring valuation guides and paying well over what valuation guides say the car is worth.

Like the position your are in just now the overinflated advertised prices aren't taken into consideration by the insurance company. They will look at the valuation guides.

BUG4LIFE said:

I've never understood why insurance companies can used these 'guides' as their source for valuations...aren't the guides linked to trade-in prices, not what Joe Bloggs can buy a car for? Surely the answer to the OP issue is to settle somewhere in between their initial valuation [based on these BS guides] and the perhaps inflated dealer prices?

There's usually more than one price in the guide, so it will show Trade/Retail/Private or similar.I don't know which of these the insurers use, but I'd guess the Private one is inbetween the Trade and Retail prices.

mmm-five said:

BUG4LIFE said:

I've never understood why insurance companies can used these 'guides' as their source for valuations...aren't the guides linked to trade-in prices, not what Joe Bloggs can buy a car for? Surely the answer to the OP issue is to settle somewhere in between their initial valuation [based on these BS guides] and the perhaps inflated dealer prices?

There's usually more than one price in the guide, so it will show Trade/Retail/Private or similar.I don't know which of these the insurers use, but I'd guess the Private one is inbetween the Trade and Retail prices.

In the Porsche forum I asked for someone to value my brothers Porsche so he could get an agreed valuation policy. In the event of it being stolen/written off there's no arguments. Another friend has a multi car policy with Admiral which he appreciates is 'market value' but has just bought a £25k vintage VW camper which isn't on the multi car but instead a desperate agreed value policy with a different insurer.

MarkGolf said:

Checked policy. valuation should be "up to market value at time of incident"

Hmmm...the full term in ours, with LV= says:"Market value: the cost of replacing your car with the same make, model and specification. Age, mileage and condition will be taken into account. We’ll ask an engineer for advice, use motor trade guides and other sources to determine the market value at the time of the accident or loss. We’ll consider the amount you could have reasonably got for your car if you sold it immediately before the accident, loss or theft and not the price you paid for it."

So it's somewhat contradictory as first it talks about replacing the car, then goes on to talk the value if you sold it.

Different scale to your issue, but in practice this is what happened when daughter's LV insured car was written off - and it's interesting as it was super-easy car to value. It was a Golf Twist which all had the same spec, was sold in large numbers but only for a short time.

When it was written off LV said they looked at values in Autotrader and offered £4995. I looked, and there were 35 for sale with both mean and median prices were £5995. The one that was £4995 was the cheapest, and the photo had the screen showing £5995. It was also 200 miles away and LV say they should at cars within 50 miles.

We’d owned the Golf from new, and it had recently had quite a lot spent on it – cambelt (would have been due on all those Golf Twists but few mentioned it), new pads & discs and new CrossClimate tyres. Insurer just dismissed all that as normal maintenance. However they didn’t seem to pick up on ours having done 70 something K miles when most listed were mid-30’s. Most had had a couple of owners.

They came back and offered £5495. I still felt £5995 would have been the right value but they absolutely wouldn’t budge.

Edited by Sheepshanks on Friday 19th January 16:54

Sheepshanks said:

"Market value: the cost of replacing your car with the same make, model and specification. Age, mileage and condition will be taken into account. We’ll ask an engineer for advice, use motor trade guides and other sources to determine the market value at the time of the accident or loss. We’ll consider the amount you could have reasonably got for your car if you sold it immediately before the accident, loss or theft and not the price you paid for it."

I'm not an insurance company basher, but wording such as the above gets my goat. It's not a definition of market value that the man on the Clapham omnibus would accept.1 Cost of replacing your car with same make, model and spec. Not same age and mileage - fundamental points in ascertaining market value

2 Age etc will be taken into account - meaningless

3 Get advice, use guides - doesn't say they will stick to them, just get advice from those sources

4 Consider sale price - what possible relevance does that have.

I can only conclude that they are actually stating they intend to low-ball the amount which in many cases they seem to go on to do.

Hey ho

Bert

Sheepshanks said:

Hmmm...the full term in ours, with LV= says:

"Market value: the cost of replacing your car with the same make, model and specification. Age, mileage and condition will be taken into account. We’ll ask an engineer for advice, use motor trade guides and other sources to determine the market value at the time of the accident or loss. We’ll consider the amount you could have reasonably got for your car if you sold it immediately before the accident, loss or theft and not the price you paid for it."

So it's somewhat contradictory as first it talks about replacing the car, then goes on to talk the value if you sold it.

Different scale to your issue, but in practice what happened when daughter's LV insured car was written off - and it's interesting as it was super-easy car to value. It was a Golf Twist which all had the same spec, was sold in large numbers but only for a short time.

When it was written off LV said they looked at values in Autotrader and offered £4995. I looked, and there were 35 for sale with both mean and medial prices of £5995. The one that was £4995 was the cheapest, and the photo had the screen showing £5995. It was also 200 miles away and LV say they should at cars within 50 miles.

We’d owned the Golf from new, and it had recently had quite a lot spent on it – cambelt (would have been due on all those Golf Twists but few mentioned it), new pads & discs and new CrossClimate tyres. Insurer just dismissed all that as normal maintenance. However they didn’t seem to pick up on ours having done 70 something K miles when most listed were mid-30’s. Most had had a couple of owners.

They came back and offered £5495. I still felt £5995 would have been the right value but they absolutely wouldn’t budge.

Exactly, those LV T&C's make so sense...the 'person' isn't looking to sell a car, they need to buy/replace the one that's just been written-off!!!!"Market value: the cost of replacing your car with the same make, model and specification. Age, mileage and condition will be taken into account. We’ll ask an engineer for advice, use motor trade guides and other sources to determine the market value at the time of the accident or loss. We’ll consider the amount you could have reasonably got for your car if you sold it immediately before the accident, loss or theft and not the price you paid for it."

So it's somewhat contradictory as first it talks about replacing the car, then goes on to talk the value if you sold it.

Different scale to your issue, but in practice what happened when daughter's LV insured car was written off - and it's interesting as it was super-easy car to value. It was a Golf Twist which all had the same spec, was sold in large numbers but only for a short time.

When it was written off LV said they looked at values in Autotrader and offered £4995. I looked, and there were 35 for sale with both mean and medial prices of £5995. The one that was £4995 was the cheapest, and the photo had the screen showing £5995. It was also 200 miles away and LV say they should at cars within 50 miles.

We’d owned the Golf from new, and it had recently had quite a lot spent on it – cambelt (would have been due on all those Golf Twists but few mentioned it), new pads & discs and new CrossClimate tyres. Insurer just dismissed all that as normal maintenance. However they didn’t seem to pick up on ours having done 70 something K miles when most listed were mid-30’s. Most had had a couple of owners.

They came back and offered £5495. I still felt £5995 would have been the right value but they absolutely wouldn’t budge.

Good luck with fighting it OP.

Unfortunately as many have said usually with insurance if it's over anywhere from 50-90% of the value that counts as a write off in a lot of t's and c's. Not to mention they always under play anything anyway.

Neighbour had his BMW pinched off the drive. Cheapest match (model, trim, visible extras, mileage) on the market at the time was £22k.

They gave him £16k and got taken to the Ombudsman, which after like 3 more months of not having a car or the money got him another £2k.

Unfortunately as many have said usually with insurance if it's over anywhere from 50-90% of the value that counts as a write off in a lot of t's and c's. Not to mention they always under play anything anyway.

Neighbour had his BMW pinched off the drive. Cheapest match (model, trim, visible extras, mileage) on the market at the time was £22k.

They gave him £16k and got taken to the Ombudsman, which after like 3 more months of not having a car or the money got him another £2k.

Incredible that they get away with this, simply because we are all forced to pay it.

Thanks again for the input here, I am slowly editing my reply.

If I accepted their £8,500, I could get back into a 2008 Cayenne GTS, just one with 43k more miles (154k) and I seriously doubt it's condition and maintenance is anywhere close to mine.

I'll be sending that example in and see how they turn that around.

.

Thanks again for the input here, I am slowly editing my reply.

If I accepted their £8,500, I could get back into a 2008 Cayenne GTS, just one with 43k more miles (154k) and I seriously doubt it's condition and maintenance is anywhere close to mine.

I'll be sending that example in and see how they turn that around.

.

MarkGolf said:

Incredible that they get away with this, simply because we are all forced to pay it.

Thanks again for the input here, I am slowly editing my reply.

If I accepted their £8,500, I could get back into a 2008 Cayenne GTS, just one with 43k more miles (154k) and I seriously doubt it's condition and maintenance is anywhere close to mine.

I'll be sending that example in and see how they turn that around.

.

They'd probably justify their current offer by expecting you to be able to haggle 10% off that without even trying...same as with any other car for sale.Thanks again for the input here, I am slowly editing my reply.

If I accepted their £8,500, I could get back into a 2008 Cayenne GTS, just one with 43k more miles (154k) and I seriously doubt it's condition and maintenance is anywhere close to mine.

I'll be sending that example in and see how they turn that around.

.

My argument to insurers has always been that I always buy from a franchised dealer, and thus my cost to replace is higher as I don't trust independent/private sellers, and am not interested in haggling.

When I was doing my renewals this year, some of the companies let you tick a 'market value' box and completed it for you. But you could opt out and put your own value in. I assume this 'manual' value has some effect on your premium...otherwise why bother offering it? But in some cases the automatic value these insurers filled in, based on my reg alone, was as much as 30% different (e.g. lowest said £10k, highest said £14.5k).

MarkGolf said:

Incredible that they get away with this, simply because we are all forced to pay it.

Thanks again for the input here, I am slowly editing my reply.

If I accepted their £8,500, I could get back into a 2008 Cayenne GTS, just one with 43k more miles (154k) and I seriously doubt it's condition and maintenance is anywhere close to mine.

I'll be sending that example in and see how they turn that around.

.

HPI valuation thinks that car is worth £5350-5700 for a private sale. Thanks again for the input here, I am slowly editing my reply.

If I accepted their £8,500, I could get back into a 2008 Cayenne GTS, just one with 43k more miles (154k) and I seriously doubt it's condition and maintenance is anywhere close to mine.

I'll be sending that example in and see how they turn that around.

.

£6130-6620 for a dealer sale.

Screenshot/save all the adverts now and write down all your points as to why you think your car is valued what you think it is. You can ask your insurance company to get an independent assessor involved and if that doesn't work out there's always the Ombudsman you can complain to.

I had a write off a year ago, ended up getting the valuation I wanted minus £500 after going through the Ombudsman. This was £12k more than their final offer and £20k more than their initial one! And I also received a nice 8% annualised interest on top of that £12k

Main thing is to not lose any sleep over it, if it's very obvious that the valuation should be higher then the Ombudsman should side with you. To give you an idea of timescale, it took 6 months from complaint to payout in my case.

I had a write off a year ago, ended up getting the valuation I wanted minus £500 after going through the Ombudsman. This was £12k more than their final offer and £20k more than their initial one! And I also received a nice 8% annualised interest on top of that £12k

Main thing is to not lose any sleep over it, if it's very obvious that the valuation should be higher then the Ombudsman should side with you. To give you an idea of timescale, it took 6 months from complaint to payout in my case.

MarkGolf said:

Even though it has 43k more miles and they were keen to point out 2 cars having 5 and 11k lower miles?

They will just focus on the asking price and having already offered you more than that will simply advise you to therefore take their offer and buy it !Negotiation on a range needs to give both sides somewhere to end up with that arguably they are both happy with.

If that car was say on at £9,450 then including that with your letter with the £8,500 offer in mind MIGHT see a final counter offer at say £9,000.

Obviously including cars for sale at higher than that would help more.

Cracking cars though incidentally - my wife’s was an 09 model and owned from new with air , pdcc and most importantly sports exhaust.

Gassing Station | Speed, Plod & the Law | Top of Page | What's New | My Stuff