Consumer debt hit an all-time high last year

Discussion

youngsyr said:

Granfondo said:

youngsyr said:

1) Thanks for the list. What's the level of debt across those types and how much impact would a 1% increase in interest rates have?

2) I wasn't implying anything, you brought up 2009 as having record bankruptcies in a discussion about an interest rate rise "screwing millions", I pointed out that 2009 saw interest rate cuts and asked you what your point is - you still haven't clarified.

3) So again, what's your point - are you saying that fixed term lending at 0% doesn't exist?

1)Those figures aren't readily available to the public but the "absence of evidence isn't evidence of absence or some other drivel!2) I wasn't implying anything, you brought up 2009 as having record bankruptcies in a discussion about an interest rate rise "screwing millions", I pointed out that 2009 saw interest rate cuts and asked you what your point is - you still haven't clarified.

3) So again, what's your point - are you saying that fixed term lending at 0% doesn't exist?

2)You were looking for data about bankruptcies and I gave them and you extrapolated from that that interest rate reduction causes bankruptcy!

"Screwed"???

3)lots of people believe the Loch Ness monster exists but try catching it!

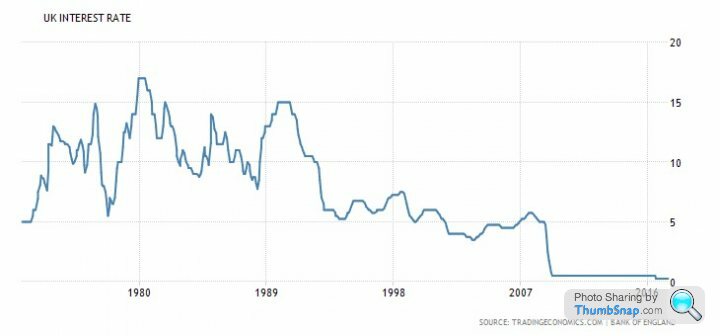

The point everyone with an ounce of intelligence can see is that the more interest rises the more people will suffer and no I don't have any data but looking back through history it seems plausible!

this graph only proves one thing,that anyone who thinks that high interest rates can't happen and are basing borrowings as some kind of investment might come unstuck!

this graph only proves one thing,that anyone who thinks that high interest rates can't happen and are basing borrowings as some kind of investment might come unstuck! Be lucky!

This report from last year [edit - see links at bottom] would suggest 8.2 million UK adults are classed as over indebted. I found it among the research archives of the Money Advice Service which can be found here.

I've only skimmed through it so am not sure how well that 8.2m figure correlates to the number of people who'd be hurt by a rate rise. I also note that they had to do a survey then extrapolate the results, which would suggest that hard figures on how borrowing is spread between households may be quite hard to come by.

MAS report - https://masassets.blob.core.windows.net/cms/files/...

MAS technical report - https://masassets.blob.core.windows.net/cms/files/...

I've only skimmed through it so am not sure how well that 8.2m figure correlates to the number of people who'd be hurt by a rate rise. I also note that they had to do a survey then extrapolate the results, which would suggest that hard figures on how borrowing is spread between households may be quite hard to come by.

MAS report - https://masassets.blob.core.windows.net/cms/files/...

MAS technical report - https://masassets.blob.core.windows.net/cms/files/...

Edited by Tartan Pixie on Thursday 29th June 18:47

Expect younger is up to his ne k in debt without a. are in the World. Seen and heard of so many people who overstretched themselves and then have the rug pulled from under them.

In the 80's/90's we had people buying houses with 100% mortgages, the gamble was that the house price would rise at a faster rate than the loan debt

In the 80's/90's we had people buying houses with 100% mortgages, the gamble was that the house price would rise at a faster rate than the loan debt

Edited by crankedup on Thursday 29th June 19:02

Edited by crankedup on Thursday 29th June 19:03

crankedup said:

Expect younger is up to his ne k in debt without a. are in the World. Seen and heard of so many people who overstretched themselves and then have the rug pulled from under them.

In the 80's/90's we had people buying houses with 100% mortgages, the gamble was that the house price would rise at a faster rate than the loan debt

Why are you attacking the person making the argument, rather than the argument itself?In the 80's/90's we had people buying houses with 100% mortgages, the gamble was that the house price would rise at a faster rate than the loan debt

Edited by crankedup on Thursday 29th June 19:02

Edited by crankedup on Thursday 29th June 19:03

Seems pretty clear to me that if you can borrow £XXX at 0% and stick it in the bank earning 2%, then it's a no brainer that you would do so. The bank is paying you to hold their money for them.

That situation is more than possible now, it wasn't possible in the 80s and 90s.

So, why are people tyring to use 30 year old data as proof that people are doomed today?

Tartan Pixie]This report from last year [edit - see links at bottom said:

would suggest 8.2 million UK adults are classed as over indebted. I found it among the research archives of the Money Advice Service which can be found here.

I've only skimmed through it so am not sure how well that 8.2m figure correlates to the number of people who'd be hurt by a rate rise. I also note that they had to do a survey then extrapolate the results, which would suggest that hard figures on how borrowing is spread between households may be quite hard to come by.

MAS report - https://masassets.blob.core.windows.net/cms/files/...

MAS technical report - https://masassets.blob.core.windows.net/cms/files/...

Thanks, that's interesting reading. Unfortunately it doesn't touch on sensitivity to interest rates at all.I've only skimmed through it so am not sure how well that 8.2m figure correlates to the number of people who'd be hurt by a rate rise. I also note that they had to do a survey then extrapolate the results, which would suggest that hard figures on how borrowing is spread between households may be quite hard to come by.

MAS report - https://masassets.blob.core.windows.net/cms/files/...

MAS technical report - https://masassets.blob.core.windows.net/cms/files/...

Edited by Tartan Pixie on Thursday 29th June 18:47

youngsyr said:

Why are you attacking the person making the argument, rather than the argument itself?

Seems pretty clear to me that if you can borrow £XXX at 0% and stick it in the bank earning 2%, then it's a no brainer that you would do so. The bank is paying you to hold their money for them.

That situation is more than possible now, it wasn't possible in the 80s and 90s.

So, why are people tyring to use 30 year old data as proof that people are doomed today?

Two questions, if I may? Seems pretty clear to me that if you can borrow £XXX at 0% and stick it in the bank earning 2%, then it's a no brainer that you would do so. The bank is paying you to hold their money for them.

That situation is more than possible now, it wasn't possible in the 80s and 90s.

So, why are people tyring to use 30 year old data as proof that people are doomed today?

I'd be fascinated to know how old you are. I'm guessing early-mid twenties?

I'm even more fascinated to learn about these 2% interest rate bank accounts please!?

Ari said:

youngsyr said:

Why are you attacking the person making the argument, rather than the argument itself?

Seems pretty clear to me that if you can borrow £XXX at 0% and stick it in the bank earning 2%, then it's a no brainer that you would do so. The bank is paying you to hold their money for them.

That situation is more than possible now, it wasn't possible in the 80s and 90s.

So, why are people tyring to use 30 year old data as proof that people are doomed today?

Two questions, if I may? Seems pretty clear to me that if you can borrow £XXX at 0% and stick it in the bank earning 2%, then it's a no brainer that you would do so. The bank is paying you to hold their money for them.

That situation is more than possible now, it wasn't possible in the 80s and 90s.

So, why are people tyring to use 30 year old data as proof that people are doomed today?

I'd be fascinated to know how old you are. I'm guessing early-mid twenties?

I'm even more fascinated to learn about these 2% interest rate bank accounts please!?

As for 2% interest rate bank accounts, I can do better than that: how about a 3% one?

http://www.tescobank.com/current-accounts/

There are monthly savings accounts currently available that offer up to 5%.

Ari said:

youngsyr said:

Why are you attacking the person making the argument, rather than the argument itself?

Seems pretty clear to me that if you can borrow £XXX at 0% and stick it in the bank earning 2%, then it's a no brainer that you would do so. The bank is paying you to hold their money for them.

That situation is more than possible now, it wasn't possible in the 80s and 90s.

So, why are people tyring to use 30 year old data as proof that people are doomed today?

Two questions, if I may? Seems pretty clear to me that if you can borrow £XXX at 0% and stick it in the bank earning 2%, then it's a no brainer that you would do so. The bank is paying you to hold their money for them.

That situation is more than possible now, it wasn't possible in the 80s and 90s.

So, why are people tyring to use 30 year old data as proof that people are doomed today?

I'd be fascinated to know how old you are. I'm guessing early-mid twenties?

I'm even more fascinated to learn about these 2% interest rate bank accounts please!?

Maybe they are working as a charity?

Granfondo said:

Ari said:

youngsyr said:

Why are you attacking the person making the argument, rather than the argument itself?

Seems pretty clear to me that if you can borrow £XXX at 0% and stick it in the bank earning 2%, then it's a no brainer that you would do so. The bank is paying you to hold their money for them.

That situation is more than possible now, it wasn't possible in the 80s and 90s.

So, why are people tyring to use 30 year old data as proof that people are doomed today?

Two questions, if I may? Seems pretty clear to me that if you can borrow £XXX at 0% and stick it in the bank earning 2%, then it's a no brainer that you would do so. The bank is paying you to hold their money for them.

That situation is more than possible now, it wasn't possible in the 80s and 90s.

So, why are people tyring to use 30 year old data as proof that people are doomed today?

I'd be fascinated to know how old you are. I'm guessing early-mid twenties?

I'm even more fascinated to learn about these 2% interest rate bank accounts please!?

Maybe they are working as a charity?

Are you honestly saying that it's impossible to borrow money at 0% and invest it in a current account offering 3% interest, despite the fact that I've linked on this very thread the credit card providers and bank accounts which will let you do precisely this?

Do you need me to spell it out for you on how to do it???

youngsyr said:

Granfondo said:

Ari said:

youngsyr said:

Why are you attacking the person making the argument, rather than the argument itself?

Seems pretty clear to me that if you can borrow £XXX at 0% and stick it in the bank earning 2%, then it's a no brainer that you would do so. The bank is paying you to hold their money for them.

That situation is more than possible now, it wasn't possible in the 80s and 90s.

So, why are people tyring to use 30 year old data as proof that people are doomed today?

Two questions, if I may? Seems pretty clear to me that if you can borrow £XXX at 0% and stick it in the bank earning 2%, then it's a no brainer that you would do so. The bank is paying you to hold their money for them.

That situation is more than possible now, it wasn't possible in the 80s and 90s.

So, why are people tyring to use 30 year old data as proof that people are doomed today?

I'd be fascinated to know how old you are. I'm guessing early-mid twenties?

I'm even more fascinated to learn about these 2% interest rate bank accounts please!?

Maybe they are working as a charity?

Are you honestly saying that it's impossible to borrow money at 0% and invest it in a current account offering 3% interest, despite the fact that I've linked on this very thread the credit card providers and bank accounts which will let you do precisely this?

Do you need me to spell it out for you on how to do it???

But as I said "be lucky!"

youngsyr said:

Seriously?

Are you honestly saying that it's impossible to borrow money at 0% and invest it in a current account offering 3% interest, despite the fact that I've linked on this very thread the credit card providers and bank accounts which will let you do precisely this?

Do you need me to spell it out for you on how to do it???

On balances up to 3k with £750 a month going in and 3 dd coming outAre you honestly saying that it's impossible to borrow money at 0% and invest it in a current account offering 3% interest, despite the fact that I've linked on this very thread the credit card providers and bank accounts which will let you do precisely this?

Do you need me to spell it out for you on how to do it???

Best you can do is use a CC for the full 3k so you need 3k spare to clear that when it falls due

If you are lucky you might bag £90 a year if you dont need to dig into it.

Of course- this is similar to the Santander 1,2,3 and the TSB whatever it is iffering 3% - plenty of clever people spent a long time figuring out how to offer these without ending up with runaway interest payments

What I wonder if whether the the levels they max out at are indicative of the bank's risk appetite or analysis of the max funds the average customer will have.... Is 3k is the most they think the average customer can lay their hands on - probably including any CC offers out there in the market. After all they have all that data of the average current, savings, ISA account across their banking client base. They will probably have the best CC offers too. They know more than us. Perhaps 3k is what they deem the upper limit the above average customer can possibly hit

menousername said:

On balances up to 3k with £750 a month going in and 3 dd coming out

Best you can do is use a CC for the full 3k so you need 3k spare to clear that when it falls due

If you are lucky you might bag £90 a year if you dont need to dig into it.

Of course- this is similar to the Santander 1,2,3 and the TSB whatever it is iffering 3% - plenty of clever people spent a long time figuring out how to offer these without ending up with runaway interest payments

What I wonder if whether the the levels they max out at are indicative of the bank's risk appetite or analysis of the max funds the average customer will have.... Is 3k is the most they think the average customer can lay their hands on - probably including any CC offers out there in the market. After all they have all that data of the average current, savings, ISA account across their banking client base. They will probably have the best CC offers too. They know more than us. Perhaps 3k is what they deem the upper limit the above average customer can possibly hit

Can you just pay £3k into your current account from a 0% credit card without incurring costs?Best you can do is use a CC for the full 3k so you need 3k spare to clear that when it falls due

If you are lucky you might bag £90 a year if you dont need to dig into it.

Of course- this is similar to the Santander 1,2,3 and the TSB whatever it is iffering 3% - plenty of clever people spent a long time figuring out how to offer these without ending up with runaway interest payments

What I wonder if whether the the levels they max out at are indicative of the bank's risk appetite or analysis of the max funds the average customer will have.... Is 3k is the most they think the average customer can lay their hands on - probably including any CC offers out there in the market. After all they have all that data of the average current, savings, ISA account across their banking client base. They will probably have the best CC offers too. They know more than us. Perhaps 3k is what they deem the upper limit the above average customer can possibly hit

menousername said:

youngsyr said:

Seriously?

Are you honestly saying that it's impossible to borrow money at 0% and invest it in a current account offering 3% interest, despite the fact that I've linked on this very thread the credit card providers and bank accounts which will let you do precisely this?

Do you need me to spell it out for you on how to do it???

On balances up to 3k with £750 a month going in and 3 dd coming outAre you honestly saying that it's impossible to borrow money at 0% and invest it in a current account offering 3% interest, despite the fact that I've linked on this very thread the credit card providers and bank accounts which will let you do precisely this?

Do you need me to spell it out for you on how to do it???

Best you can do is use a CC for the full 3k so you need 3k spare to clear that when it falls due

If you are lucky you might bag £90 a year if you dont need to dig into it.

Of course- this is similar to the Santander 1,2,3 and the TSB whatever it is iffering 3% - plenty of clever people spent a long time figuring out how to offer these without ending up with runaway interest payments

What I wonder if whether the the levels they max out at are indicative of the bank's risk appetite or analysis of the max funds the average customer will have.... Is 3k is the most they think the average customer can lay their hands on - probably including any CC offers out there in the market. After all they have all that data of the average current, savings, ISA account across their banking client base. They will probably have the best CC offers too. They know more than us. Perhaps 3k is what they deem the upper limit the above average customer can possibly hit

They're financial dinosaurs who mentally still live in the 80s.

youngsyr said:

Granfondo said:

Does anyone know if you can get 0% interest money out of a credit card?

Really, if you don't know the answer to this, or ways around it, I'd advise staying out of discussions on consumer debt. Edited by Granfondo on Thursday 29th June 21:17

Granfondo said:

youngsyr said:

Granfondo said:

Does anyone know if you can get 0% interest money out of a credit card?

Really, if you don't know the answer to this, or ways around it, I'd advise staying out of discussions on consumer debt. You know there's this wonderful source of information, with billions of articles explaining almost everything, and it's available at your fingertips. You don't even need to leave your seat to access it. Its called "the internet", you might have heard of it?

youngsyr said:

Granfondo said:

youngsyr said:

Granfondo said:

Does anyone know if you can get 0% interest money out of a credit card?

Really, if you don't know the answer to this, or ways around it, I'd advise staying out of discussions on consumer debt. You know there's this wonderful source of information, with billions of articles explaining almost everything, and it's available at your fingertips. You don't even need to leave your seat to access it. Its called "the internet", you might have heard of it?

Granfondo said:

youngsyr said:

Granfondo said:

youngsyr said:

Granfondo said:

Does anyone know if you can get 0% interest money out of a credit card?

Really, if you don't know the answer to this, or ways around it, I'd advise staying out of discussions on consumer debt. You know there's this wonderful source of information, with billions of articles explaining almost everything, and it's available at your fingertips. You don't even need to leave your seat to access it. Its called "the internet", you might have heard of it?

Likewise anyone else who doesn't know.

Your education isn't my responsibility.

Gassing Station | News, Politics & Economics | Top of Page | What's New | My Stuff