How far will house prices fall [volume 4]

Discussion

V6Alfisti said:

Also I am not sure where the 5x came from, but I think the latest figures show the average is 5.5x in the cheapest area (North East) and 13x in South East.

I guess it's from one of those "how much you can borrow" calculators, where you find that mortgage provider who wants to take a risk. Chris Type R said:

Chris Type R said:

Down the road from us:

Added to RM 13 Nov 2016 at £3,750,000 - http://www.rightmove.co.uk/property-for-sale/prope...

Relisted 20 Oct 2017 at £2,500,000 - http://www.rightmove.co.uk/property-for-sale/prope...

Post revival.... now up for auction, guide price £1,250,000 - https://www.rightmove.co.uk/property-for-sale/prop...Added to RM 13 Nov 2016 at £3,750,000 - http://www.rightmove.co.uk/property-for-sale/prope...

Relisted 20 Oct 2017 at £2,500,000 - http://www.rightmove.co.uk/property-for-sale/prope...

Which is probably closer to realistic.

Today's news seems to be centering around Foxton's losses due to the faltering London market.

Interesting Deloitte article here as well

http://blogs.deloitte.co.uk/mondaybriefing/2018/07... particularly "A standard measure of affordability compares house prices to rents and to incomes relative to long-term averages. At £226,351 the average UK house is almost eight times median annual earnings. The OECD estimates that UK housing is 29% overvalued against incomes and 41% overvalued against rents."

Interesting Deloitte article here as well

http://blogs.deloitte.co.uk/mondaybriefing/2018/07... particularly "A standard measure of affordability compares house prices to rents and to incomes relative to long-term averages. At £226,351 the average UK house is almost eight times median annual earnings. The OECD estimates that UK housing is 29% overvalued against incomes and 41% overvalued against rents."

Matt p said:

Ouch, 29% over valued?. Doubt we will ever see that sort of reduction in prices it’ll be a bloodbath. However stranger things have happened I guess so who knows.

Overvalued compared to incomes. Thats not the same. Foreign investors dont have 'incomes' which means its pointless. Not only locals can buy. Matt p said:

Ouch, 29% over valued?. Doubt we will ever see that sort of reduction in prices it’ll be a bloodbath. However stranger things have happened I guess so who knows.

Well the reduction from late 1989 was around 20-25% or more .... I can remember the pain after my first house purchase.

Which equates to approx 25-30% overvalue.

Somehow I doubt there will be a 25% correction this time though.

p1stonhead said:

Overvalued compared to incomes. Thats not the same. Foreign investors dont have 'incomes' which means its pointless. Not only locals can buy.

Yes but as with most things there are multiple levers at play.Foreign investment has tangibly reduces, as FI typically requires confidence in a market or suitable reward for risk, whilst we currently have an uncertain political/economic future, a wobbly pound. Add into this the opening up of pandora's box by revealing the names of foreign investors which have a rather less honest looking source of funds, and interest rates starting to creep up globally.

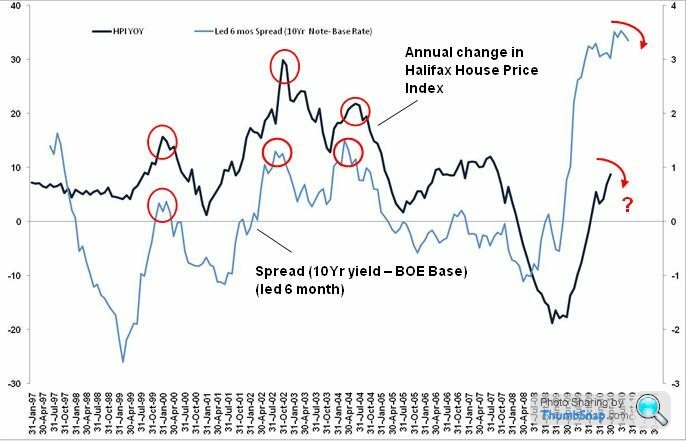

We all know that as soon as interest rates reach a normal average, house prices definitely will not be maintained.

As I can see it, FI has more risk, less to negative reward....if I was FI right now, I wouldn't be buying property to flip/keep empty like many did in the past and no doubt made some great returns. I would be looking at other countries, or investment vehicles.

Adding to this if you follow Henry Pryor on Twitter, he often has a number of EA's responding to his post. One recently said that they had seen a significant drop in Chinese/Russian interest and other regions had picked up slightly in response but foreign interest was down by at least 50%...rather significant.

This isn't just London/UK specific, many global hot property markets are falling back ... in fact https://moneyweek.com/house-prices-arent-just-slip...

"Prices in Sydney fell by 4.5% in the second quarter, while prices in Melbourne slipped too.

Australia is far from alone. Hot global markets everywhere are slowing down. Canada is another good example.

And now we’re seeing it happen in the US as well. As Bloomberg reports: “The US housing market – particularly in cutthroat areas like Seattle, Silicon Valley and Austin, Texas – appears to be headed for the broadest slowdown in years.”

The number of home sales (of existing homes as opposed to new builds) fell in June for the third month in a row. New builds are selling at the slowest pace in eight months.

Meanwhile, the inventory of unsold homes – the amount of supply on the sidelines – is rising again. Prices in May were up by 6.4% year-on-year (so a lot stronger than in the UK, for example), but that’s the smallest annual gain since 2017 – and over the last three months, prices have risen at their slowest rate since 2012."

Edited by V6Alfisti on Monday 30th July 15:20

V6Alfisti said:

p1stonhead said:

Overvalued compared to incomes. Thats not the same. Foreign investors dont have 'incomes' which means its pointless. Not only locals can buy.

We all know that as soon as interest rates reach a normal average, house prices definitely will not be maintained.ten years is 'normal' in my book. Its certainly been a much longer constant rate than ever before. Doesnt that count as 'normal'?

P.S - im playing devils advocate. But I dont think it will be above say 2% base rate in the coming ten years either. No one has a crystal ball however.

Edited by p1stonhead on Monday 30th July 15:40

turbobloke said:

V6Alfisti said:

We all know that as soon as interest rates reach a normal average, house prices definitely will not be maintained.

Some questions if I may. Do we all have operational Mk I crystal balls meaning we all really do know?!

What's normal, and when will it be reached?

However, the implications of even a modest rate rise could lead to big collapses in house prices and, in turn, consumer confidence and unemployment.

Neither option is very attractive and with rates where they have been for 10 years there is little room to work with. It's a pretty ugly situation and the easiest "solution" to switch back on the printing presses only serves to put further strain on Sterling.

Of course none of us have a crystal ball but if I did, whatever I see before us looks pretty grey and stormy.

Edited by Shnozz on Monday 30th July 17:14

turbobloke said:

Some questions if I may.

Do we all have operational Mk I crystal balls meaning we all really do know?!

What's normal, and when will it be reached?

I know you are playing devils advocate but ... of course not, but we do have the benefit of history and correlation.Do we all have operational Mk I crystal balls meaning we all really do know?!

What's normal, and when will it be reached?

I thought it was common knowledge to know that assets increase when money is cheap, when money isn't cheap the reverse happens, then add fuel to the fire when people see an asset value flying and fear of being priced out...until it reaches such a point where either a buyer cannot afford it or the surrounding fuel starts to dissipate. A bubble.

Noticed any trends with investment assets like classic cars, watches and houses in recent years?

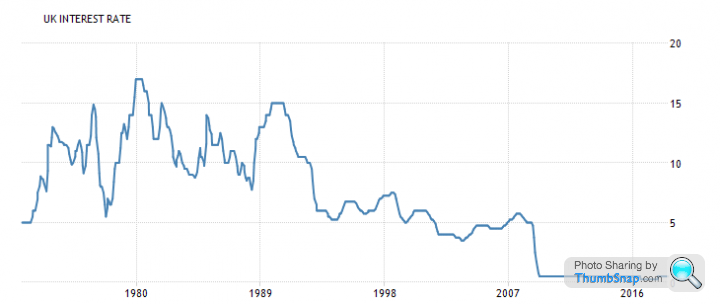

Normal - Certainly not anywhere in the 0-2% range, at no point between 1975 and 2008 did interest rates drop below 3.5% until we had the global crisis which led to today's state of affairs. It is not a coincidence that house values of gone up so much on a pretty much global scale with a few exceptions.

The average over that same period was about 7% but even taking away some of the higher interest rates over that period, I think it's fair to say that even the lowest base rate of 3.5% is not an unreasonable place to be. You didn't think 0.5% was going to last/normal?

Edited by V6Alfisti on Monday 30th July 17:16

Shnozz said:

Of course none of us have a crystal ball but if I did, whatever I see before us looks pretty grey and stormy.

Absolutely and history supports a number of those fears, I cannot comprehend anyone with knowledge thinking it will be the status quo when the cost of borrowing goes up against a back drop of the highest salary to house value disparities in recorded history.Even with all the QE, HTB e.t.c the market in large parts of London are falling over itself. That doesn't take imagination, its happening right now.

V6Alfisti said:

turbobloke said:

Some questions if I may.

Do we all have operational Mk I crystal balls meaning we all really do know?!

What's normal, and when will it be reached?

I know you are playing devils advocate but ... of course not, but we do have the benefit of history and correlation.Do we all have operational Mk I crystal balls meaning we all really do know?!

What's normal, and when will it be reached?

Economics 101 to know that assets increase when money is cheap, when money isn't cheap the reverse happens.

Noticed any trends with investment assets like classic cars, watches and houses in recent years?

Normal - Certainly not anywhere in the 0-2% range, at no point between 1975 and 2008 did interest rates drop below 3.5% until we had the global crisis which led to today's state of affairs.

The average over that same period was about 7% but even taking away some of the higher interest rates over that period, I think it's fair to say that even the lowest base rate of 3.5% is not an unreasonable place to be. You didn't think 0.5% was going to last/normal?

Edited by V6Alfisti on Monday 30th July 17:05

p1stonhead said:

I think the main point is that the government isn’t going to allow rates to go up to a point such as 7% where it would bankrupt half the country who have ever known the interest rates we’ve had for ten years. They’ll do anything to stop that happening. No government wants to be within 1000 years of being in power when such a thing occurred.

That's why my crystal ball said a figure half that, but certainly not overnight. However in all seriousness the loan values as a proportion of salary are so much higher now, even modest 0.25% increases are making people think twice, as I suspect many expected house prices to keep on rising and rates to stay super low for many more years to afford the monthlies.

V6Alfisti said:

p1stonhead said:

I think the main point is that the government isn’t going to allow rates to go up to a point such as 7% where it would bankrupt half the country who have ever known the interest rates we’ve had for ten years. They’ll do anything to stop that happening. No government wants to be within 1000 years of being in power when such a thing occurred.

That's why my crystal ball said a figure half that, but certainly not overnight. However in all seriousness the loan values as a proportion of salary are so much higher now, even modest 0.25% increases are making people think twice, as I suspect many expected house prices to keep on rising and rates to stay super low for many more years to afford the monthlies.

p1stonhead said:

V6Alfisti said:

p1stonhead said:

Overvalued compared to incomes. Thats not the same. Foreign investors dont have 'incomes' which means its pointless. Not only locals can buy.

We all know that as soon as interest rates reach a normal average, house prices definitely will not be maintained.ten years is 'normal' in my book. Its certainly been a much longer constant rate than ever before. Doesnt that count as 'normal'?

tannhauser said:

p1stonhead said:

V6Alfisti said:

p1stonhead said:

Overvalued compared to incomes. Thats not the same. Foreign investors dont have 'incomes' which means its pointless. Not only locals can buy.

We all know that as soon as interest rates reach a normal average, house prices definitely will not be maintained.ten years is 'normal' in my book. Its certainly been a much longer constant rate than ever before. Doesnt that count as 'normal'?

Anyone on a 20 year mortgage would be more than half through on these ‘unsustainable’ rates if they secured it ten years ago.

You can fix right now for 5 years at under 2% and 10 years at under 3%. A 2.7% (available to me right now) ten year fix could get me within 4 years of finishing my mortgage and i would be 45 having never experienced any BOE rates above 0.5% as a homeowner.

Rates will not go up past 2% BOE for at least 5 years IMO

Again - see my previous comment about partially playing devils advocate.

Edited by p1stonhead on Monday 30th July 18:50

p1stonhead said:

tannhauser said:

p1stonhead said:

V6Alfisti said:

p1stonhead said:

Overvalued compared to incomes. Thats not the same. Foreign investors dont have 'incomes' which means its pointless. Not only locals can buy.

We all know that as soon as interest rates reach a normal average, house prices definitely will not be maintained.ten years is 'normal' in my book. Its certainly been a much longer constant rate than ever before. Doesnt that count as 'normal'?

Anyone on a 20 year mortgage would be more than half through on these ‘unsustainable’ rates if they secured it ten years ago.

You can fix right now for 5 years at under 2% and 10 years at under 3%. A 2.7% (available to me right now) ten year fix could get me within 4 years of finishing my mortgage and i would be 45 or with a bit of overpaying would clear it easily.

Rates will not go up past 2% BOE for at least 5 years IMO

Edited by p1stonhead on Monday 30th July 18:48

Low odds.

Gassing Station | News, Politics & Economics | Top of Page | What's New | My Stuff