Will the plan work to turn generation rent into buy?

Discussion

Groat said:

C70R said:

The late 90s and early 00s were an absolute shambles for BTL mortgages....... it was truly the wild west.

What makes you think that?The husband told me that buying that house was the worst financial mistake he had ever made.

Oakey said:

Here you go, ones just popped up today. He's a scaffolder, she's 19 and a part time student and they've just bought their first home for £160k.

https://www.mirror.co.uk/money/young-couple-spend-...

I note that it is literally newsworthy that it has happened though. https://www.mirror.co.uk/money/young-couple-spend-...

I'm pleased for them, but the article also doesn't really go into where the deposit money came from. They'd have needed what - £30k deposit and you'd still be capped at 3.5x your annual income?

Edited by anonymous-user on Saturday 10th April 13:24

Oakey said:

Her mum being Investment Director for an investment fund and her dad operating his 150yr old wholesale bakery business probably helped...

Honestly. I'm surprised also that house prices in Dundee are so high, sign of the times? £160k for a 2-bedroom house in a city with a £23-25k average wage. Biggy Stardust said:

I bought a wreck with potential. It was cheap because absolutely nobody wanted it. Many people don't recognise an opportunity because it comes disguised as hard work.

This morning was spent drilling & fixing inside the house. This afternoon was spent shovelling large amounts of stone. Tomorrow will be just like yesterday- painting.

This is how I afford the place I live in. If others feel that this sort of thing is either beneath them or too much effort then I have zero sympathy for them.

How much did the house cost (compared to its value) and how much will it cost to restore it?This morning was spent drilling & fixing inside the house. This afternoon was spent shovelling large amounts of stone. Tomorrow will be just like yesterday- painting.

This is how I afford the place I live in. If others feel that this sort of thing is either beneath them or too much effort then I have zero sympathy for them.

Lloyds, NatWest, Santander, Barclays, HSBC UK and Virgin Money all announce 5% government backed mortgages.

https://www.dailymail.co.uk/news/article-9471187/M...

Wonder what the interest rate is going to be?

https://www.dailymail.co.uk/news/article-9471187/M...

Wonder what the interest rate is going to be?

Joey Deacon said:

Lloyds, NatWest, Santander, Barclays, HSBC UK and Virgin Money all announce 5% government backed mortgages.

https://www.dailymail.co.uk/news/article-9471187/M...

Wonder what the interest rate is going to be?

Would be interesting to see because they have been given free reign to set the interest. My guess is anywhere from 3-4%. Optimistic I know. https://www.dailymail.co.uk/news/article-9471187/M...

Wonder what the interest rate is going to be?

austinsmirk said:

It’d never work. How would you police it ? I work in social housing. Rents are tuppence. Seriously £72 a week for a one bed flat. About £85 to £120 a week for a house. No bonds. No deposits.

We write off £2.5 m a year in uncollected rent. I wouldn’t care but only 50% even have full/ part to pay. It’s accepted as the nature of the business you take these losses to help the most vulnerable

As someone else who has worked in social housing for many years, I can absolutely confirm the above, but also add that it isn't just the rental properties that fall into arrears and ultimately eviction.We write off £2.5 m a year in uncollected rent. I wouldn’t care but only 50% even have full/ part to pay. It’s accepted as the nature of the business you take these losses to help the most vulnerable

I have witnessed many cases of people failing to pay the small rental amount on their Shared Ownership homes, and ultimately have lost their homes. These are homes that people have taken out mortgages on.

You can do everything you possibly can to advise people in the strongest possible terms that they are about to lose their rental property or shared ownership property due to their arrears situation, and the situation will not improve.

As Austinsmirk says, we are talking about significant numbers of people who can't even manage £80-100 a week and go on to lose their homes.

Edited by anonymous-user on Monday 19th April 10:25

austinsmirk said:

just to expand on this our sector is rigorous when it comes to debt enforcement. and its not a case of letting people get away with it- there are massive income teams helping and assisting people get what they are due income wise, help them budget, help with advise on best energy deals.............you can get attachments from their benefits to clear debt off..

don't forget this is all interest free- unlike when you bounce on your mortgage payment.

I used to run the cities homeless services for years: I've seen it from the other end of people losing their homes. A very common thing that used to occur was people buying their "council" house- obviously discounted. they'd get all sorts of shady mortgages to do so, managing to prove income. you'd look at people who utterly failed to pay promptly and on time, forever, somehow getting mortgages.

they wouldn't get a mortgage for £50k to buy it, they'd go for £100k for "home improvements".

you could literally do a check list of where the £50k went- holiday to disney, massive RV, pair of dirt bikes, pick up truck/4 x 4, deck/stone clad every inch of the house..................... but the bank wants paying don't they, with interest unlike their previous landlord.

so re-possessions would kick in. they'd be back asking for a free house.....................

funnily enough, if you can get a nice social housing prop and all you ever have to pay is £85 a week for life- its repaired and maintained for free for you------------ you could have a lovely quite wealthy life if that's what and where you wanted to live in. people think its all estates- its not. but those rural village homes are harder and harder to find these days.

Absolutely.don't forget this is all interest free- unlike when you bounce on your mortgage payment.

I used to run the cities homeless services for years: I've seen it from the other end of people losing their homes. A very common thing that used to occur was people buying their "council" house- obviously discounted. they'd get all sorts of shady mortgages to do so, managing to prove income. you'd look at people who utterly failed to pay promptly and on time, forever, somehow getting mortgages.

they wouldn't get a mortgage for £50k to buy it, they'd go for £100k for "home improvements".

you could literally do a check list of where the £50k went- holiday to disney, massive RV, pair of dirt bikes, pick up truck/4 x 4, deck/stone clad every inch of the house..................... but the bank wants paying don't they, with interest unlike their previous landlord.

so re-possessions would kick in. they'd be back asking for a free house.....................

funnily enough, if you can get a nice social housing prop and all you ever have to pay is £85 a week for life- its repaired and maintained for free for you------------ you could have a lovely quite wealthy life if that's what and where you wanted to live in. people think its all estates- its not. but those rural village homes are harder and harder to find these days.

As for the bit I highlighted in bold. This is very true. I have worked for a couple of housing associations who had quite a lot of nice stock in stunning rural locations. Small developments of 8 or 10 cottage style houses in really upmarket little villages etc.

Some providers still have fairly active development programs in nice rural areas.

A friend of mine just managed to get a house-swap for his Mum, from some dodgy part of Essex to a stunning village in Cumbria, and into a lovely house. It's hers for the rest of her life as long as she keeps paying £80 a week, and she will never have to worry about any repair bills. All she has to do is decorate it internally and keep it tidy.

InitialDave said:

Not declaring rental income for tax sounds like a good way to get yourself a severe legal and financial buggering.

My wife was obsessed with doing things by the book when she had a BTL, and rightly so, but a couple of her work colleagues had a BTL each, and they were practically mocking her for declaring it. One of them went round every month and collected the rent in cash, and the other just had a separate bank account for collecting the rent.Neither of them thought HMRC would ever find out, or be particularly interested. "All I'm doing is renting my old house. It's no one else business. I pay tax on my salary. This isn't a salary" etc.

Must be tens of thousands, or hundreds of thousands, of people across the country doing the same.

We all know that HMRC are steadily ending all manner of loopholes and blindspots, and no doubt after Covid they will be under instruction from the government to go after everyone they can. It would not surprise me if they had a big push on undeclared BTL.

Edited by anonymous-user on Monday 19th April 12:46

Nationwide announce first time buyer 5.5 times salary mortgage as long as you fix for five years.

https://www.dailymail.co.uk/money/mortgageshome/ar...

https://www.dailymail.co.uk/money/mortgageshome/ar...

Sycamore said:

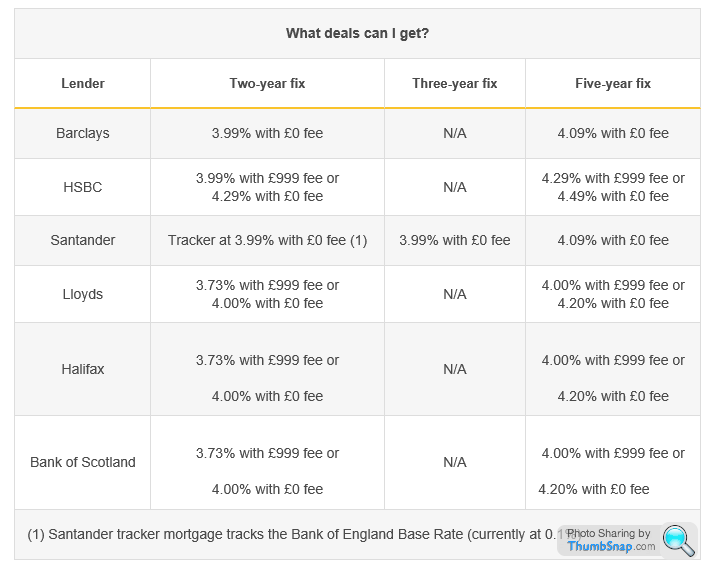

Overview of 5% mortgages available as of them being released yesterday.

https://www.moneysavingexpert.com/mortgages/new-mo...

It mentions the top mortgage available with 10% is around 2.99% interest.

So an extra 1% really if using 5%.

Ouch, as someone who got a 1.54% mortgage with Natwest with a 20% deposit last year, these figures seem incredibly high.https://www.moneysavingexpert.com/mortgages/new-mo...

It mentions the top mortgage available with 10% is around 2.99% interest.

So an extra 1% really if using 5%.

I assume the reality is going to be that looking past the headline "5% deposit" these mortgages are going to be unaffordable for a large percentage of the people they are aimed at.

okgo said:

The thing is, the 600k thing is aimed at London. Where that will buy you a nice 2 bed, or a total s tehole of a house somewhere. These people will all easily be able to afford the payment, as for a couple they'll be used to paying 1k each for a room already/1800-2k for a alright 1 bed somewhere. So I do think there will be a fair few going at the top end. Obviously finding 30 grand is still a fair amount, but it's within the reach of BOMAD/your more saving oriented 28 year a lot more than 60 is.

tehole of a house somewhere. These people will all easily be able to afford the payment, as for a couple they'll be used to paying 1k each for a room already/1800-2k for a alright 1 bed somewhere. So I do think there will be a fair few going at the top end. Obviously finding 30 grand is still a fair amount, but it's within the reach of BOMAD/your more saving oriented 28 year a lot more than 60 is.

But yes, those rates are grim.

Slim pickings near me, but lets assume a couple borrow the maximum allowed and go for something like this.tehole of a house somewhere. These people will all easily be able to afford the payment, as for a couple they'll be used to paying 1k each for a room already/1800-2k for a alright 1 bed somewhere. So I do think there will be a fair few going at the top end. Obviously finding 30 grand is still a fair amount, but it's within the reach of BOMAD/your more saving oriented 28 year a lot more than 60 is.But yes, those rates are grim.

https://www.rightmove.co.uk/properties/104484818#/

They need the £30K deposit so borrow £570K with Halifax at 3.73% over a 25 year repayment mortgage.

I make that £2924.35 a month........

InitialDave said:

austinsmirk said:

Joey Deacon said:

Slim pickings near me, but lets assume a couple borrow the maximum allowed and go for something like this.

https://www.rightmove.co.uk/properties/104484818#/

They need the £30K deposit so borrow £570K with Halifax at 3.73% over a 25 year repayment mortgage.

I make that £2924.35 a month........

That’s hilarious. A house so small that you can sit on the sofa on the l.room and kick the front door shut without getting up. https://www.rightmove.co.uk/properties/104484818#/

They need the £30K deposit so borrow £570K with Halifax at 3.73% over a 25 year repayment mortgage.

I make that £2924.35 a month........

Joking aside you need a hell of a job to buy that. And it’s utterly utterly dreadful and miserable. Can you imagine the last 12 mths of lockdown living in that for what, nearly £3k a mth in mortgage.

But that’s the twist isn’t it. Bonkers wages required to live in a home the rest of the UK might put up with as a first time buyer home for a few years. Say you can afford it, what on earth do you do next when you want an average sized house ?

To put that in perspective I bought a 3 bedroom detached house with garage and drive as a BTL four years ago in Hampshire for not much more than that. It's about a 45 minute drive outside of where we are now.

It is mental, I don't know how the majority of people afford it as £1 million doesn't even get you off street parking. Yet I see lots of couples in their 30s putting the children into the brand new Range Rover after having lunch in an expensive restaurant.

Gassing Station | News, Politics & Economics | Top of Page | What's New | My Stuff