Car finance - hidden commission payments

Discussion

phpe said:

sugerbear said:

Thanks. Two more claims going in then :-) Trying to find details of when I purchased them is going to be fun as it was back in 2010!

Do a subject access request to the finance companies for historical records about you.https://ico.org.uk/for-the-public/your-right-to-ge...

FamousPheasant said:

Extracting as much money out of a customer while keeping said customer happy (be that a business or an individual) for the benefit of their employer - and often themselves via commission - is the primary function of every salesperson, everywhere - in every industry. There is nothing scummy about that.

And that was an argument the bank made in the judgement - section 236 www.financial-ombudsman.org.uk/decision/DRN-418828... but that argument was dismissed.The issue is that the car dealer isn't the business 'selling' the product - the finance - that is being 'sold' by the bank.

The car dealer is acting as a broker for the person receiving the finance, selecting from a range of products to that which best meets the needs of the individual, and the issue was that the broker was incentivised by the bank to treat the recipient unfairly.

The bank in this case was fully prepared to lend to the individual at 2.49% and pay the broker a fee of around £150. However the bank told the broker that if it increased that rate up to 5.5% then it would pay the broker a higher discretionary commission.

As soon as the bank did that then the broker ceased to have any interest in what was best for the person receiving the finance and simply told them that the best rate they could achieve was 5.5% - and that simply wasn't true.

It is the conflict of interest of the broker created by the bank and the discretionary commission if they inflated the interest rate that is the problem, not that the broker earned a commission.

Honourable Dead Snark said:

Update from Martin Lewis on Twitter:

‘In the first 3 days:-

- 463,750 complaint letters now generated

- 40% likely to have had the hidden commission

- Typical expected pay-back £1,100

So a conservative predicted £204million total’

Across multiple finance companies it isnt very much. ‘In the first 3 days:-

- 463,750 complaint letters now generated

- 40% likely to have had the hidden commission

- Typical expected pay-back £1,100

So a conservative predicted £204million total’

OddCat said:

So existing brokers go bust because they broke the rules - sad for them, but the industry will just adapt around it and perhaps will stick to the rules this time.PF62 said:

OddCat said:

So existing brokers go bust because they broke the rules - sad for them, but the industry will just adapt around it and perhaps will stick to the rules this time.Caddyshack said:

PF62 said:

OddCat said:

So existing brokers go bust because they broke the rules - sad for them, but the industry will just adapt around it and perhaps will stick to the rules this time.Caddyshack said:

PF62 said:

OddCat said:

So existing brokers go bust because they broke the rules - sad for them, but the industry will just adapt around it and perhaps will stick to the rules this time.No one broke any rules at the time.

It’s subsequently been deemed unfair practice and potentially they are now looking to retroactively punish.

I wonder about the legality of that, are the FCA above the law.

I mentioned earlier, it would be like doing 50mph on a 50 limit road, a week later its changed to a 30mph limit and they then try and charge you with speeding for the previous week.

And as I also said, the current regime that the FCA put in place in 2021 and is still current, isn’t really all that different.

Stupot123 said:

Caddyshack said:

PF62 said:

OddCat said:

So existing brokers go bust because they broke the rules - sad for them, but the industry will just adapt around it and perhaps will stick to the rules this time.No one broke any rules at the time.

It’s subsequently been deemed unfair practice and potentially they are now looking to retroactively punish.

I wonder about the legality of that, are the FCA above the law.

I mentioned earlier, it would be like doing 50mph on a 50 limit road, a week later its changed to a 30mph limit and they then try and charge you with speeding for the previous week.

And as I also said, the current regime that the FCA put in place in 2021 and is still current, isn’t really all that different.

PF62 said:

The rules that the brokers and the banks broke existed before 2021. It is just that in 2021 they put their foot down and actively stopped the abuse, but it didn't mean that the behaviour before 2021 was within the rules.

Don’t agree. It’s the way the industry operated. No one was doing anything wrong at the time.It’s subsequently been deemed wrong, and they are potentially going to backdate punishment, which doesn’t seem right.

And I’ll mention again, what they have changed it to now, is almost as bad. In the future I’d almost guarantee that will be deemed unethical too. Will they then decide to punish that too, even although it’s deemed acceptable today?

Stupot123 said:

PF62 said:

The rules that the brokers and the banks broke existed before 2021. It is just that in 2021 they put their foot down and actively stopped the abuse, but it didn't mean that the behaviour before 2021 was within the rules.

Don’t agree. It’s the way the industry operated. No one was doing anything wrong at the time.It’s subsequently been deemed wrong, and they are potentially going to backdate punishment, which doesn’t seem right.

And I’ll mention again, what they have changed it to now, is almost as bad. In the future I’d almost guarantee that will be deemed unethical too. Will they then decide to punish that too, even although it’s deemed acceptable today?

As for “subsequently” being deemed wrong - well duh! That’s how breaking the rules works - you break the rules and then you are subsequently investigated and when it is confirmed you did then that breach is dealt with.

PF62 said:

The industry may have operated in that way, but that doesn’t mean it operated within the rules - or are you claiming that the references the regulator is quoting are made up by them. If so that’s a strong allegation.

As for “subsequently” being deemed wrong - well duh! That’s how breaking the rules works - you break the rules and then you are subsequently investigated and when it is confirmed you did then that breach is dealt with.

Ok, what rule was broken, what year was that rule introduced and what year are you applying it to? They are looking at 2007-2021, if that helps.As for “subsequently” being deemed wrong - well duh! That’s how breaking the rules works - you break the rules and then you are subsequently investigated and when it is confirmed you did then that breach is dealt with.

Stupot123 said:

Ok, what rule was broken, what year was that rule introduced and what year are you applying it to?

Have a read as it is all detailed here - www.financial-ombudsman.org.uk/decision/DRN-418828...But since this has been posted multiple times I guess you won’t.

Edited by PF62 on Friday 9th February 22:47

PF62 said:

Stupot123 said:

Ok, what rule was broken, what year was that rule introduced and what year are you applying it to?

Have a read as it is all detailed here - www.financial-ombudsman.org.uk/decision/DRN-418828...PPi gave a nice boost as people didn’t pay the compo off what they owed, they bought stuff with it.

I suspect retail will be in for a boost of the £200m compo.

PF62 said:

Have a read as it is all detailed here - www.financial-ombudsman.org.uk/decision/DRN-418828...

But since this has been posted multiple times I guess you won’t.

I’ve read both the rulings many times, the answer to the question I asked isn’t in there?But since this has been posted multiple times I guess you won’t.

Edited by PF62 on Friday 9th February 22:47

The CONC rules that it refers to look to be current, yet being applied retrospectively, which is the bit I don’t understand.

Edited by Stupot123 on Friday 9th February 23:04

Stupot123 said:

I’ve read both the rulings many times, the answer to the question I asked isn’t in there?

The CONC rules that it refers to look to be current, yet being applied retrospectively, which is the bit I don’t understand.

You have been misled by the annotation in the FCA handbook that indicates CONC 4.5.3 was a new rule introduced on 28/01/2021 when in fact there had been a previous CONC 4.5.3 rule which had been in place since 2014 that covered this case - The CONC rules that it refers to look to be current, yet being applied retrospectively, which is the bit I don’t understand.

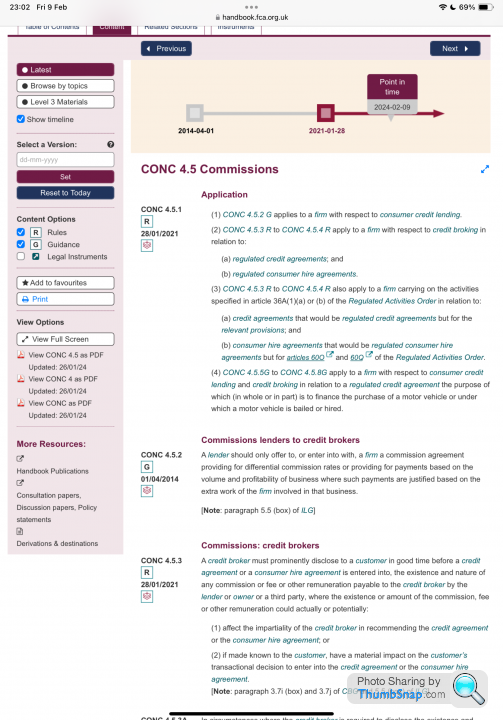

www.handbook.fca.org.uk/handbook/CONC/4/5.html?dat...

FCA said:

A credit broker must disclose to a customer in good time before a credit agreement or a consumer hire agreement is entered into, the existence of any commission or fee or other remuneration payable to the credit broker by the lender or owner or a third party in relation to a credit agreement or a consumer hire agreement, where knowledge of the existence or amount of the commission could actually or potentially:

(1) affect the impartiality of the credit broker in recommending a particular product; or

(2) have a material impact on the customer's transactional decision.

The FCA considered that the discretionary commission given to the broker for pushing the rate up to 5.5% when they knew the customer had already been accepted at 2,5% affected their impartiality.(1) affect the impartiality of the credit broker in recommending a particular product; or

(2) have a material impact on the customer's transactional decision.

Also had the customer been informed that they were only being sold the 5.5% rate because of the commission and that they had been accepted at 2.5% then they wouldn’t have agreed to the deal.

Edited by PF62 on Saturday 10th February 08:33

Gassing Station | Finance | Top of Page | What's New | My Stuff