Discussion

sidicks said:

AMDBSTony said:

This has worked for me very well which is why I say what I say - there are obvious conditions like location but we've cracked that.

What supports your statement?

The basic definition of 'very low risk' in connection with investments...What supports your statement?

Choose correct area - houses let out - low risk in my experience

ISA's - up and down but generally up - higher risk than property but still lowish risk.

Sorry but your argument still hasnt much substance IMO.

Edited by AMDBSTony on Friday 26th August 09:02

AMDBSTony said:

sidicks said:

AMDBSTony said:

This has worked for me very well which is why I say what I say - there are obvious conditions like location but we've cracked that.

What supports your statement?

The basic definition of 'very low risk' in connection with investments...What supports your statement?

Choose correct area - houses let out - low risk in my experience

ISA's - up and down but generally up - higher risk than property but still lowish risk.

Sorry but your argument still hasnt much substance IMO.

Edited by AMDBSTony on Friday 26th August 09:02

- Highly illiquid = risky.

- Single asset, not diversified = risky.

- Non-guaranteed yield = risky. (You can pretend that the yield is guaranteed but that's a simple lie - often you can't rent nose-to-tail, rental yields fall).

- Capital at risk = risky. (Laughable "houses always go up" arguments are only made by total muppets.)

- Hidden costs = risky. (Transaction costs: legal, agents, stamp duty then eventually - new kitchen, wear and tear, new windows, roof, painting... everyone forgets these.)

- High tax = just crap asset allocation.

Just because you have one example of "low risk in my experience" sadly won't really give much credibility against centuries of economic and financial principle.

Having said all that property COULD be a reasonable part of a portfolio but not 100% of it.

Sadly with 100k that's going to be tough to do.

walm said:

AMDBSTony said:

sidicks said:

AMDBSTony said:

This has worked for me very well which is why I say what I say - there are obvious conditions like location but we've cracked that.

What supports your statement?

The basic definition of 'very low risk' in connection with investments...What supports your statement?

Choose correct area - houses let out - low risk in my experience

ISA's - up and down but generally up - higher risk than property but still lowish risk.

Sorry but your argument still hasnt much substance IMO.

Edited by AMDBSTony on Friday 26th August 09:02

- Highly illiquid = risky.

- Single asset, not diversified = risky.

- Non-guaranteed yield = risky. (You can pretend that the yield is guaranteed but that's a simple lie - often you can't rent nose-to-tail, rental yields fall).

- Capital at risk = risky. (Laughable "houses always go up" arguments are only made by total muppets.)

- Hidden costs = risky. (Transaction costs: legal, agents, stamp duty then eventually - new kitchen, wear and tear, new windows, roof, painting... everyone forgets these.)

- High tax = just crap asset allocation.

Just because you have one example of "low risk in my experience" sadly won't really give much credibility against centuries of economic and financial principle.

Having said all that property COULD be a reasonable part of a portfolio but not 100% of it.

Sadly with 100k that's going to be tough to do.

Really not bothered how others invest, thats up to them. All i am saying is that in my experience, which is fairly extensive, this has served me well and pays very very well. The value of the properties have also increased very significantly.

Compared to 'safer' options like ISA's and the like, the above out performs beyond belief.

Nobody will ever convince me otherwise but i am not saying that my way is the best way......its just my way that has served me very well in the past and means that i am afforded the luxury of being able to do other things - like choosing not to work!!

Go figure!

This is my last post on this matter as like everything else on PH there are always many differences of opinions which is fine, i just have better things to do than get mixed up in pointless discussions.

walm said:

Your opinion is sadly wrong and is in direct contradiction to even the most basic of risk management principles.

- Highly illiquid = risky.

- Single asset, not diversified = risky.

- Non-guaranteed yield = risky. (You can pretend that the yield is guaranteed but that's a simple lie - often you can't rent nose-to-tail, rental yields fall).

- Capital at risk = risky. (Laughable "houses always go up" arguments are only made by total muppets.)

- Hidden costs = risky. (Transaction costs: legal, agents, stamp duty then eventually - new kitchen, wear and tear, new windows, roof, painting... everyone forgets these.)

- High tax = just crap asset allocation.

Just because you have one example of "low risk in my experience" sadly won't really give much credibility against centuries of economic and financial principle.

Having said all that property COULD be a reasonable part of a portfolio but not 100% of it.

Sadly with 100k that's going to be tough to do.

It's probably unlikely on a £70k property anyone soon, but there's the possibility of CGT on the sale of a letting too. I agree, as part of a diversified portfolio, there's lots of merit in the idea, but to provide income for a pensioner with the possibility of changing needs? It's difficult to justify. - Highly illiquid = risky.

- Single asset, not diversified = risky.

- Non-guaranteed yield = risky. (You can pretend that the yield is guaranteed but that's a simple lie - often you can't rent nose-to-tail, rental yields fall).

- Capital at risk = risky. (Laughable "houses always go up" arguments are only made by total muppets.)

- Hidden costs = risky. (Transaction costs: legal, agents, stamp duty then eventually - new kitchen, wear and tear, new windows, roof, painting... everyone forgets these.)

- High tax = just crap asset allocation.

Just because you have one example of "low risk in my experience" sadly won't really give much credibility against centuries of economic and financial principle.

Having said all that property COULD be a reasonable part of a portfolio but not 100% of it.

Sadly with 100k that's going to be tough to do.

Does her pension increase with inflation? If it does then pick one of the investment options that will give her a near immediate return. If her pension does not increase with inflation then I would suggest not drawing down on the cash for a few years as she will become increasingly dependant on the extra cash later on. Every penny left in the investment for as long as possible will mean more money later.

AMDBSTony said:

I have many examples of this, not just one. This extends to commercial offices as well as domestic but seeing as we were discussing only £100k i thought i would keep it relevant to that amount.

Really not bothered how others invest, thats up to them. All i am saying is that in my experience, which is fairly extensive, this has served me well and pays very very well. The value of the properties have also increased very significantly.

None of which has anything to do with risk!Really not bothered how others invest, thats up to them. All i am saying is that in my experience, which is fairly extensive, this has served me well and pays very very well. The value of the properties have also increased very significantly.

AMDBSTony said:

Compared to 'safer' options like ISA's and the like, the above out performs beyond belief.

An ISA is just a tax-efficient wrapper - it is neither safe nor risky. That depends on the underlying investment exposure.AMDBSTony said:

Nobody will ever convince me otherwise but i am not saying that my way is the best way......its just my way that has served me very well in the past and means that i am afforded the luxury of being able to do other things - like choosing not to work!!

Go figure!

This is my last post on this matter as like everything else on PH there are always many differences of opinions which is fine, i just have better things to do than get mixed up in pointless discussions.

No-one is saying that your proposal could not work or is inappropriate, just that it is (blatantly) not "very low risk", particularly given the circumstances presented by the OP!Go figure!

This is my last post on this matter as like everything else on PH there are always many differences of opinions which is fine, i just have better things to do than get mixed up in pointless discussions.

AMDBSTony said:

Over time houses have only gone up not down - low risk in my books.

Choose correct area - houses let out - low risk in my experience

ISA's - up and down but generally up - higher risk than property but still lowish risk.

Nonsense! Sounds like you don't really understand what an ISA is!Choose correct area - houses let out - low risk in my experience

ISA's - up and down but generally up - higher risk than property but still lowish risk.

AMDBSTony said:

Sorry but your argument still hasnt much substance IMO.

Sorry, but you clearly don't understand 'risk'!Simpo Two said:

Would the tax benefits of an ISA (whatever investment is in it) mitigate some of risk, in that gains are greater? Hence a greater upside but the same downside. Or is 'risk' calculated simply on the investments within it?

I don't think so.Risk here is measured to the objectives of the OP:

"Where best to invest the £100,000 to provide her with an income top up each month, with easy access to funds when needed."

Investing in an asset that provides no guaranteed income, which could actually require cash outflows at some point in the future and which is highly illiquid is highly risky for the OP.

You don't need more than half a brain to see that!

To my mind, tax efficiency simply allows the OP to achieve (marginally) higher income for the same amount of risk.

Edited by sidicks on Friday 26th August 10:39

drainbrain said:

walm said:

...Having said all that property COULD be a reasonable part of a portfolio but not 100% of it….

Why do you think that? (Would have thought the Duke of Westminster's a pretty obvious topical example of why it's nonsense)He is almost a complete exception (although I don't know, I strongly suspect he will have been far more diversified than you think).

Multi-billion family offices (which I know a fair bit about) don't put all their eggs in one basket.

They diversify.

Because it's the NUMBER ONE rule of risk management.

drainbrain said:

Yes! Yes! Those 'managers' who 'manage' to make the poor punter not much more than the poor punter would 'make' by keeping his hard-earned in a box under his bed!

ESPECIALLY them!

As usual with you, a total lack of understanding of what I do, what 'managers' do and the topic under discussion.ESPECIALLY them!

An idiot's hatrick!

Anything to add to the thread apart from poorly directed snipes in my direction?

drainbrain said:

sidicks said:

You mean the guy who is paid to manage investment 'risk' for other people?

Yes! Yes! Those 'managers' who 'manage' to make the poor punter not much more than the poor punter would 'make' by keeping his hard-earned in a box under his bed!ESPECIALLY them!

What are your qualifications and experience?

One guy managing a successful portfolio of BTLs in the greatest housing boom in history doesn't really make a great case I am afraid.

walm said:

Just read my previous post.

He is almost a complete exception (although I don't know, I strongly suspect he will have been far more diversified than you think).

Multi-billion family offices (which I know a fair bit about) don't put all their eggs in one basket.

They diversify.

Because it's the NUMBER ONE rule of risk management.

What on earth is stop a property investor owning a portfolio which contains a whole spectrum of risk within it? You would agree, I take it, that there are very high risk properties and very low risk ones (and everything in between). So why shouldn't a property portfolio form 100% of a retirement plan?He is almost a complete exception (although I don't know, I strongly suspect he will have been far more diversified than you think).

Multi-billion family offices (which I know a fair bit about) don't put all their eggs in one basket.

They diversify.

Because it's the NUMBER ONE rule of risk management.

drainbrain said:

What on earth is stop a property investor owning a portfolio which contains a whole spectrum of risk within it? You would agree, I take it, that there are very high risk properties and very low risk ones (and everything in between). So why shouldn't a property portfolio form 100% of a retirement plan?

Well that's better than the just one single property originally suggested.But you are (obviously) HUGELY exposed to a single asset class (maybe two if you separate commercial/resi).

This means that when the government changes the stamp duty rules you can take a massive hit.

In 2008 you would be crushed (on capital).

Perhaps the most important thing is that with any sizeable portfolio you need to WORK to keep it generating all that lovely yield.

Lots of people genuinely want to retire, not keep on top of their portfolio.

Lastly, the vast majority of people are already massively exposed to property since they tend to live in a property that they own.

(Obviously not the OP's mum.)

So adding a further exposure to the same asset class adds to the risk by definition.

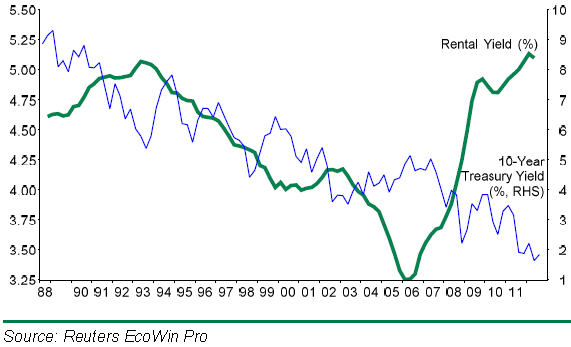

Here's the UK rental yield... safe as houses.

Edited by walm on Friday 26th August 10:38

Gassing Station | Finance | Top of Page | What's New | My Stuff