Funds dropping!

Discussion

Mr Pointy said:

Derek Chevalier said:

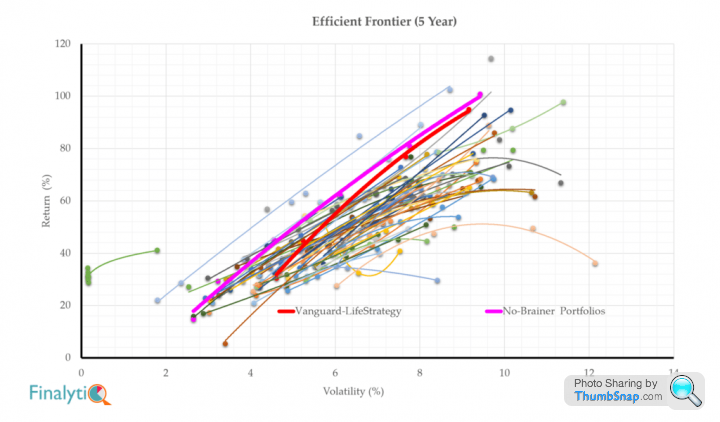

As one of the comments to that article points out those graphs are only looking at 3 & 5 years in the present bullish market. If it was over 20 years it might be a bit more convincing that they were capturing true long term performance?

Of course they need a snappy conclusion to sell the book for £499/£4999.

Derek Chevalier said:

Interesting stuff will check it out when I have a minute. Intuitively I don’t doubt that there is a ‘price’ to be paid for the convenience of LSNickCQ said:

Derek Chevalier said:

Interesting stuff will check it out when I have a minute. Intuitively I don’t doubt that there is a ‘price’ to be paid for the convenience of LS98elise said:

JulianPH said:

They all do that sometimes, sir!

Markets are falling, so funds will fall with them, some more than others though.

Just seems to be a big drop recently, bigger than the markets. That said they have risen well over the past few years so you have to expect the odd big fall.Markets are falling, so funds will fall with them, some more than others though.

My purely passive ones are all down though.

Derek Chevalier said:

Peter Lynch

With all my funds except for smithson you have to agree to buy or sell at the price set at the next midday price after your instruction is placed.So the price can obviously vary from the day before.

Smithson let's you deal instantly so you know the price.

Maybe if you have a broker you can tell them to deal if the price suits,I use apps to buy and these dont have that function.

b hstewie said:

hstewie said:

hstewie said: Which funds?

Lindsell Train Global Equity fund is down around 10% since the beginning of September.

Bad news perhaps for anyone that invested recently with a short term outlook:

https://www.ftadviser.com/investments/2019/10/02/l...

Has the bubble burst?

bhstewie said:

hstewie said:98elise said:

A spread of some of the usual suspects LTGE, Fundsmith etc.

Fundsmith is pretty much 70% US exposure so you'll have taken a hit on the dollar as the pound has gained with a no-deal Brexit looking less likely.As I said there have been a few days where you look at global stock exchanges or individual company shares and they're green, but the pound gaining means you're in the red just due to currency.

bhstewie said:

hstewie said:98elise said:

A spread of some of the usual suspects LTGE, Fundsmith etc.

Fundsmith is pretty much 70% US exposure so you'll have taken a hit on the dollar as the pound has gained with a no-deal Brexit looking less likely.As I said there have been a few days where you look at global stock exchanges or individual company shares and they're green, but the pound gaining means you're in the red just due to currency.

EDIT -

just found the following:

"Say you want to buy $150 of US stock as a UK investor. Your British pounds are converted into those dollars at a rate of £100 for $150 (way back in 2015). Now, let’s say the value of the company itself doesn’t move an inch for four years: your shares are still worth $150. Sorry!

But in that time, the pound also declines: you can now exchange $150 for £125. That means your $150 of stock is now worth 25% more pounds than in the past (equally, if the pound rises in this scenario, your $150 investment will be worth less than you paid for it initially).

So even though the underlying value of the investment itself didn’t move at all, the currency move meant that its relative value in pounds made you money."

So i get that. If you are buying direct microsoft or google denoted in $ which is then converted to £ as we buy and sell or receive dividends in $ - but how would that affect shares denominated in £? Is that because they earn $? Or funds like fundsmith - is that simply as they hold lots of american stocks that are now worth more or less actual £? Or is it to do with demand for the fund from US investors would be less as the exchange rate makes it more expensive? Or both?

Edited by trowelhead on Tuesday 22 October 23:01

Edited by trowelhead on Tuesday 22 October 23:03

Yep, I’ve taken a cold shower on LT Global Equity (among others) over the past few weeks. I take the view that there will be ups and downs, which is why you have to see equities as a long-term investment.

Higher volatility, higher risk, but over the long term should generate higher returns.

Higher volatility, higher risk, but over the long term should generate higher returns.

Looks like I got out just in time

I was always running the risk, seeing as though my investments were always meant to be held for a maximum of 3 years... Cashed out early (regardless of market conditions) after ~18 months to use as a deposit for my first house.

I'll be opening a standard S&S ISA to try and do the same again once I have adjusted to the adult life of paying a mortgage/bills and work out how much I can invest per month. Let's hope the aforementioned fund prices stay low until I'm back

I was always running the risk, seeing as though my investments were always meant to be held for a maximum of 3 years... Cashed out early (regardless of market conditions) after ~18 months to use as a deposit for my first house.

I'll be opening a standard S&S ISA to try and do the same again once I have adjusted to the adult life of paying a mortgage/bills and work out how much I can invest per month. Let's hope the aforementioned fund prices stay low until I'm back

95JO said:

Looks like I got out just in time

I was always running the risk, seeing as though my investments were always meant to be held for a maximum of 3 years... Cashed out early (regardless of market conditions) after ~18 months to use as a deposit for my first house.

I'll be opening a standard S&S ISA to try and do the same again once I have adjusted to the adult life of paying a mortgage/bills and work out how much I can invest per month. Let's hope the aforementioned fund prices stay low until I'm back

Well, any dip is a buying opportunity!I was always running the risk, seeing as though my investments were always meant to be held for a maximum of 3 years... Cashed out early (regardless of market conditions) after ~18 months to use as a deposit for my first house.

I'll be opening a standard S&S ISA to try and do the same again once I have adjusted to the adult life of paying a mortgage/bills and work out how much I can invest per month. Let's hope the aforementioned fund prices stay low until I'm back

.....although knowing where were are on the "dip curve" is always the interesting challenge.....let's just hope it isn't a "dip cliff" !!

mikeiow said:

Well, any dip is a buying opportunity!

.....although knowing where were are on the "dip curve" is always the interesting challenge.....let's just hope it isn't a "dip cliff" !!

The financial news, signals, forecasts, political situation (both her and US) etc etc are so confusing at the moment. I haven't got too long to go to retirement and find myself a bit paralysed as to what to do......although knowing where were are on the "dip curve" is always the interesting challenge.....let's just hope it isn't a "dip cliff" !!

Sheepshanks said:

The financial news, signals, forecasts, political situation (both her and US) etc etc are so confusing at the moment. I haven't got too long to go to retirement and find myself a bit paralysed as to what to do.

Key is to ignore short term noise - commonly known as financial p**n  There's always some crisis in the news - they thrive on it. What ratings would a "good news" channel get?

There's always some crisis in the news - they thrive on it. What ratings would a "good news" channel get? https://www.investopedia.com/terms/f/financialporn...

Think about what your long term goals and objectives are and build a plan around that.

Sheepshanks said:

The financial news, signals, forecasts, political situation (both her and US) etc etc are so confusing at the moment. I haven't got too long to go to retirement and find myself a bit paralysed as to what to do.

Well, I am in the same position as you.....actually in the process of 'crystallising' one lump from my Aviva fund (from an LTA perspective, the dip is a good thing , should that be a concern!)I assume you mean you have more in DC pensions than DB?

My view is that although, like you, I may not have long to go to retire, that retirement will itself (hopefully!) be a lengthy 20-30+ year period....so my logic ought to be similar to that I had 20 years ago.

(eta - this is pretty well what Derek said whilst I was typing!)

"What was that logic?", I hear you ask!

Partly - live for fun - get out there & do stuff, enjoy the growing family, have FUN!!

Partly - I don't really understand markets, but I do understand they go down, then they go up (I work in IT, not finance, so not an advisor!!)

The difference in retirement is that one is not in a great position to "buy on the dips" and keep adding to investments to average in.

To alleviate that, maybe one should take the TFLS and trickle it back into markets over time (okay, perhaps via ISAs, not pensions), trying to replicate that regular paying pattern.

Maybe one should keep a chunk of it in cash (perhaps even the oft-criticised premium bonds) to be able to live off at times of poor markets in order to allow them to recover.

None of us have a crystal ball

I've spent too long on my own 'planning spreadsheet' (I imagine many here have!) - tries to give you the ability to model income desires against fund/pension growth over many years, allowing for different pensions (eg state) kicking in at different points, allowing you to play with imaginary fund growth, or indeed throw in some dips to see "what if".

It is very much a "work in progress", but has given me a decent handle on how things could pan out!

If you/anyone want a sanitised version of my spreadsheet to look at, message me your email - I'd welcome any feedback (had some already from folk on a couple of forums!)

When US stocks priced in USD drop in price and the GBP goes up vs. USD it amplifies the relative drop of the USD priced asset.

Hence why it's good to keep a range of funds.

As the drop and/or GBP increases think of it as an offer price or 10% discount and you are buying more units.

If the UK crashes out of the EU GBP will drop and the relative price of funds will rocket.

A 5% raise in GBP vs a 5% drop in USD priced units will leave you able to buy 10% more for your money.

Strong domestic currency is good for buying foreign currency assets.

Hence why it's good to keep a range of funds.

As the drop and/or GBP increases think of it as an offer price or 10% discount and you are buying more units.

If the UK crashes out of the EU GBP will drop and the relative price of funds will rocket.

A 5% raise in GBP vs a 5% drop in USD priced units will leave you able to buy 10% more for your money.

Strong domestic currency is good for buying foreign currency assets.

mikeiow said:

I assume you mean you have more in DC pensions than DB?

I do have a DC pension but I'm leaving that alone as it's switched into whatever it's final phase is called as I near retirment.It's everything else - I've got money with Fundsmith which has obviously performed remarkably well over the last few years, and some other finds which are OK but not spectacular. The bad thing we've (in both my and wife's names) done is built up chunky amounts in cash ISAs - but everytime I think about doing something with them, some calamity hits us (personally)!

Sheepshanks said:

mikeiow said:

I assume you mean you have more in DC pensions than DB?

I do have a DC pension but I'm leaving that alone as it's switched into whatever it's final phase is called as I near retirement.It's everything else - I've got money with Fundsmith which has obviously performed remarkably well over the last few years, and some other finds which are OK but not spectacular. The bad thing we've (in both my and wife's names) done is built up chunky amounts in cash ISAs - but everytime I think about doing something with them, some calamity hits us (personally)!

Must admit, I actively took my DC pension OUT of the 'glidepath' to retirement about 15 years ago - I could see mine (Aviva) ended up mostly in cash, effectively losing money out to inflation, & the bond elements are still rated as "risk 5' by them. I have moved some towards those anyway....

Like I said above, I understand the mental anguish about approaching retirement....BUT that is just the start of a lengthy time (hopefully!!), during which there is that need for the funds to continue to grow. Of course there is the risk of them diving at some point....but for me, it is a view on a 30+ year timeframe of investment.

We have a reasonable amount in cash ISAs, which (perhaps like you!) I view as a mistake - hindsight & all that - but I figure they can form monies that could be easily accessed during any downturn to let other S&S funds/pensions climb back.

Good luck with your choices!

As Mike has highlighted, most pension glide paths phases you into low volatility holdings as you get closer to retirement.

This was historically done on the basis you were going to buy an annuity.

If you are intending to use your fund to draw down an income this can be exactly the wrong place to be, as your money needs to keep working for you.

This was historically done on the basis you were going to buy an annuity.

If you are intending to use your fund to draw down an income this can be exactly the wrong place to be, as your money needs to keep working for you.

Gassing Station | Finance | Top of Page | What's New | My Stuff