Intelligent Money - your investment questions answered

Discussion

renmure said:

A dog walker. Just what we need.

The last one didn't come back

I'm not sure whether the little guy sat on hom him or if the two land-sharks did that barky bitey thing.

What a beast Jim! Land sharks is pretty spot on too, ours lost her first baby tooth a few days ago and it looked like a shark tooth!.The last one didn't come back

I'm not sure whether the little guy sat on hom him or if the two land-sharks did that barky bitey thing.

42 adult teeth still to come!

Re SDLT, the 3% additional surcharge still applies if you own more than one property on completion and are not replacing your main residence. So it's 3% up to £500,000 and then business as usual above there.

There are some other caveats where it may or may not apply and rules around married couples being treated as one unit (so no putting a BTL solely in the wife's name because she's not named on the deeds of the main residence) etc

I should put a little "risk warning" here and say I'm a mortgage adviser and not a tax adviser but that is my understanding of stamp duty taxation per experience.

There are some other caveats where it may or may not apply and rules around married couples being treated as one unit (so no putting a BTL solely in the wife's name because she's not named on the deeds of the main residence) etc

I should put a little "risk warning" here and say I'm a mortgage adviser and not a tax adviser but that is my understanding of stamp duty taxation per experience.

GR_TVR said:

The stamp duty holiday (unfortunately) only applies to the "normal" rate table and the additional property rate of 3% still applies.

E.g. a second home or BTL worth £500k would incur the 3% additional property stamp duty of £15k, but you would save the £15k of "normal" stamp duty.

Every day is a school day! E.g. a second home or BTL worth £500k would incur the 3% additional property stamp duty of £15k, but you would save the £15k of "normal" stamp duty.

Note to self, stay away from things you don't fully know about...

JulianPH said:

Thanks!

After 6,500 posts I honestly don't remember if it has been asked before! A quick chat with Nik (nik.burrows@intelligentmoney.com) will give you everything you need to know.

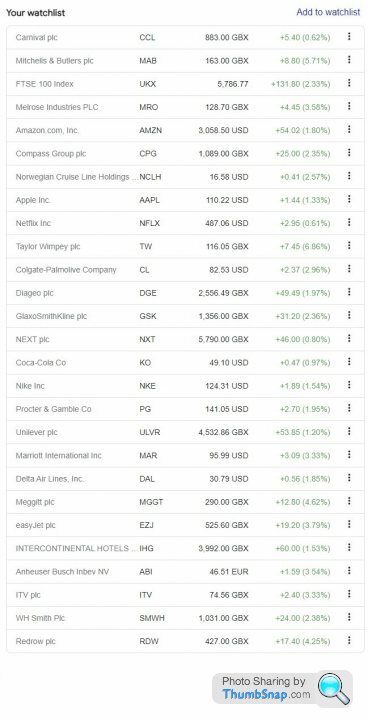

Basically, if you hold them in a personal CREST account everything is in your name, but this can be expensive. If you hold them through a nominee they are still your legal property, but the costs can be significantly lower. Most companies hand out any perks to shareholders regardless of how you hold them and your nominee broker will also be holding them through CREST on your behalf.

Cheers

Julian

I sent Nik an email this morning....but I think there was quite a lot to answer After 6,500 posts I honestly don't remember if it has been asked before! A quick chat with Nik (nik.burrows@intelligentmoney.com) will give you everything you need to know.

Basically, if you hold them in a personal CREST account everything is in your name, but this can be expensive. If you hold them through a nominee they are still your legal property, but the costs can be significantly lower. Most companies hand out any perks to shareholders regardless of how you hold them and your nominee broker will also be holding them through CREST on your behalf.

Cheers

Julian

I have a general question about money in trust.

My father in law passed away recently and left some money to my son. This will be in the form of proceeds from the sale of his house when his partner no longer wants to live in it (probably a long way off) and some compensation money as he died from a cancer related to inhaling asbestos.

My brother in law in executing the will and said he would put the money in to trust for my son. This is fine but I was wondering how much influence I could have over this in so far as I would like it invested rather than sitting in premium bonds or similar for the next 16 years.

Has anyone done anything similar or is this something that is frowned upon?

My father in law passed away recently and left some money to my son. This will be in the form of proceeds from the sale of his house when his partner no longer wants to live in it (probably a long way off) and some compensation money as he died from a cancer related to inhaling asbestos.

My brother in law in executing the will and said he would put the money in to trust for my son. This is fine but I was wondering how much influence I could have over this in so far as I would like it invested rather than sitting in premium bonds or similar for the next 16 years.

Has anyone done anything similar or is this something that is frowned upon?

Edited by KTF on Tuesday 3rd November 16:08

KTF said:

I have a general question about money in trust.

My father in law passed away recently and left some money to my son. This will be in the form of proceeds from the sale of his house when his partner no longer wants to live in it (probably a long way off) and some compensation money as he died from a cancer related to inhaling asbestos.

My brother in law in executing the will and said he would put the money in to trust for my son. This is fine but I was wondering how much influence I could have over this in so far as I would like it invested rather than sitting in premium bonds or similar for the next 16 years.

Has anyone done anything similar or is this something that is frowned upon?

Presumably the executors are the trustees?My father in law passed away recently and left some money to my son. This will be in the form of proceeds from the sale of his house when his partner no longer wants to live in it (probably a long way off) and some compensation money as he died from a cancer related to inhaling asbestos.

My brother in law in executing the will and said he would put the money in to trust for my son. This is fine but I was wondering how much influence I could have over this in so far as I would like it invested rather than sitting in premium bonds or similar for the next 16 years.

Has anyone done anything similar or is this something that is frowned upon?

Edited by KTF on Tuesday 3rd November 16:08

Would they be willing to appoint you as a trustee?

KTF said:

I have a general question about money in trust.

My father in law passed away recently and left some money to my son. This will be in the form of proceeds from the sale of his house when his partner no longer wants to live in it (probably a long way off) and some compensation money as he died from a cancer related to inhaling asbestos.

My brother in law in executing the will and said he would put the money in to trust for my son. This is fine but I was wondering how much influence I could have over this in so far as I would like it invested rather than sitting in premium bonds or similar for the next 16 years.

Has anyone done anything similar or is this something that is frowned upon?

Sorry to hear that Peter and my best wishes to you and you wife.My father in law passed away recently and left some money to my son. This will be in the form of proceeds from the sale of his house when his partner no longer wants to live in it (probably a long way off) and some compensation money as he died from a cancer related to inhaling asbestos.

My brother in law in executing the will and said he would put the money in to trust for my son. This is fine but I was wondering how much influence I could have over this in so far as I would like it invested rather than sitting in premium bonds or similar for the next 16 years.

Has anyone done anything similar or is this something that is frowned upon?

Edited by KTF on Tuesday 3rd November 16:08

Nik is advanced qualified in taxation and trusts, so can go over all of this with you.

Please give me a shout if you need anything else, but Nik knows more about this than I do.

JulianPH said:

Sorry to hear that Peter and my best wishes to you and you wife.

Nik is advanced qualified in taxation and trusts, so can go over all of this with you.

Please give me a shout if you need anything else, but Nik knows more about this than I do.

Thanks Julian. I will drop Nick an email about this as I would like my son to get the ‘best’ out of this windfall rather than it sit in an instant access account. Nik is advanced qualified in taxation and trusts, so can go over all of this with you.

Please give me a shout if you need anything else, but Nik knows more about this than I do.

Had a chat with NHS pensions today. I recently left the NHS so wanted to transfer my pension into a SIPP but apparently they dont allow it as people were being silly and investing in dodgy Gold Mines or something?

Have you (IM) ever had an NHS pension transferred over for you to manage?

Thanks.

Have you (IM) ever had an NHS pension transferred over for you to manage?

Thanks.

Gassing Station | Finance | Top of Page | What's New | My Stuff