St. James' Place - a review…

Discussion

b hstewie said:

hstewie said:

hstewie said:Halitosis said:

I work in the industry and honestly think SJP are spinning some very tenuous tales on the Assets Under Management (AUM) front by describing themselves as the largest in the UK (by trying to differentiate "Wealth" Manager from "Asset" Manager). SJP don't even make it into the UK's top 10 Asset Managers by AUM. BlackRock Investment Management (UK) had £847 billion according to their 2020 accounts, and I believe L&G and Standard Life/Aberdeen (or whatever they call themselves these days) are even larger.

Regardless, as others have stated, AUM is legally ring-fenced, so if the firm goes under the clients' assets are preserved

Is it because SJP class it as customers money with them directly v a lot of institutional money i.e. at a legal level my money is with IWEB or whoever even if I've invested it in a BlackRock product?Regardless, as others have stated, AUM is legally ring-fenced, so if the firm goes under the clients' assets are preserved

GT3Manthey said:

CharlesElliott said:

The 1.6% is just one fee though - for advice.

If you are investing in SJP funds, you are also paying higher fees as part of the fund investment than you would be with a lot of other funds, including (in all likelihood) the funds that SJP are investing you in.

The investment industry - not just SJP - has layers and layers of fees and you need to see the whole picture.

I’m only really concerned at the returns net to me regardless of who it is If you are investing in SJP funds, you are also paying higher fees as part of the fund investment than you would be with a lot of other funds, including (in all likelihood) the funds that SJP are investing you in.

The investment industry - not just SJP - has layers and layers of fees and you need to see the whole picture.

But I can see both sides. I MIGHT be able to fix an electrical issue with my boat, but it would take time and still might not work so I'd rather pay someone to do it for me.

Simpo Two said:

I'm a 'bottom line' person too. But if you can invest in the same or equivalent funds at a lower cost, your bottom line will be higher. Penny saved penny earned and all that. The only losers will be the guys in the middle hoovering a living out of your wealth while you take the risk for them.

But I can see both sides. I MIGHT be able to fix an electrical issue with my boat, but it would take time and still might not work so I'd rather pay someone to do it for me.

To an extent, I'm a bottom line person (for example I own Fundsmith rather than Vanguard's world equity tracker).But I can see both sides. I MIGHT be able to fix an electrical issue with my boat, but it would take time and still might not work so I'd rather pay someone to do it for me.

However, I think its presently particularly risky to make decisions because we're satisfied with a bottom line performance, as we're looking back at over a decade of pretty exceptional equity returns, so our recency bias makes us prone to feeling the top line return that is generating that bottom line will continue indefinitely. Imagine a generally flat market for 5 years where you see your portfolio value steadily falling to pay the management fee.

I've encountered quite a few quasi-competent professionals in my life - to use your metaphor, I'd worry about a careless electrical fault causing the boat to burn down to the waterline, and electrical circuits really aren't that complicated.

xeny said:

However, I think its presently particularly risky to make decisions because we're satisfied with a bottom line performance, as we're looking back at over a decade of pretty exceptional equity returns, so our recency bias makes us prone to feeling the top line return that is generating that bottom line will continue indefinitely. Imagine a generally flat market for 5 years where you see your portfolio value steadily falling to pay the management fee.

Market performance is one thing. As you say it can be up, stagnant or down. But if someone is in the middle taking a fee whatever the eventuality, then all three options are worse.Looking at my IM dashboard - there are others but that's the quickest to check - everything is saggy at present. Let's hope this isn't the beginning of a continued decline.

xeny said:

I'd worry about a careless electrical fault causing the boat to burn down to the waterline, and electrical circuits really aren't that complicated.

Can you start tomorrow?

GT3Manthey said:

Derek Chevalier said:

That implies you've paid more than one lot of initial fees. Are you being charged for regular/ad-hoc contributions as well as on the initial money invested?

So my ongoing fees annually are 1.6% for everything including new investments. I appreciate this is more than others charge however I’ve been happy with my returns and advice/tax advice received.

I appreciate others self manage pensions but I’m too busy to deal with it all plus I’m concerned that a transfer now elsewhere might not work out

Derek Chevalier said:

That's relatively cheap if it's for their pensions (which are typically more than ISA on an ongoing basis but don't incur the 5% (explicit) initial). Typically I've seen a tad over 2% including transaction cost with the adviser getting 0.5% of that.

That's horrific if you bung it into a compound interest calculator.Are they offering more than a SIPP would in product/functionality terms?

We often find that there is a lack of understanding about what and who SJP are.

They aren't true IFAs in a way that most people presume. Instead they have a range of their own products which they will try and sell you to fit your circumstances. They are a product business not a service industry. Sometimes those products might be right, but note that they are promoting their own products, what they don't do is find the very best product for your circumstances and sell you that one.

You can get a true service from other large suppliers like Tilney etc who will look at whole of market.

They aren't true IFAs in a way that most people presume. Instead they have a range of their own products which they will try and sell you to fit your circumstances. They are a product business not a service industry. Sometimes those products might be right, but note that they are promoting their own products, what they don't do is find the very best product for your circumstances and sell you that one.

You can get a true service from other large suppliers like Tilney etc who will look at whole of market.

bhstewie said:

hstewie said: Are they offering more than a SIPP would in product/functionality terms?

There's some tax efficiency "advice" (quotes as I'm not sure if it is technically advised or not), periodic face to face visits, hand holding if the market looks scary, and product advice from their range of products. Ladies depending on portfolio size get different sized bunches of flowers. I don't know what men get.CharlesElliott said:

The 1.6% is just one fee though - for advice.

If you are investing in SJP funds, you are also paying higher fees as part of the fund investment than you would be with a lot of other funds, including (in all likelihood) the funds that SJP are investing you in.

The investment industry - not just SJP - has layers and layers of fees and you need to see the whole picture.

You can see the (pension) fees hereIf you are investing in SJP funds, you are also paying higher fees as part of the fund investment than you would be with a lot of other funds, including (in all likelihood) the funds that SJP are investing you in.

The investment industry - not just SJP - has layers and layers of fees and you need to see the whole picture.

https://www.sjp.co.uk/charges/transaction-costs

https://www.sjp.co.uk/charges/transaction-costs

For pension it's 1.5% (of which the adviser gets 0.5%) plus fund and transaction charges on top. Typrically 2% + transaction costs.

I recall there are some legacy pension products where the adviser gets 0.25% which brings the overall cost down by 0.25%

PugwasHDJ80 said:

You can get a true service from other large suppliers like Tilney etc who will look at whole of market.

This Tilney?https://citywire.co.uk/new-model-adviser/news/reve...

PugwasHDJ80 said:

We often find that there is a lack of understanding about what and who SJP are.

They aren't true IFAs in a way that most people presume. Instead they have a range of their own products which they will try and sell you to fit your circumstances. They are a product business not a service industry. Sometimes those products might be right, but note that they are promoting their own products, what they don't do is find the very best product for your circumstances and sell you that one.

You can get a true service from other large suppliers like Tilney etc who will look at whole of market.

Very true although in reality, a firm like Tilley won't actually be much different as they may have access to the whole of market but they will typically only be using a small part of that as their 'proffered' list. They won't be conducting research on all, just a few and the regulatory environment and their PI insurance will steer them to stick to 'favourites'. They aren't true IFAs in a way that most people presume. Instead they have a range of their own products which they will try and sell you to fit your circumstances. They are a product business not a service industry. Sometimes those products might be right, but note that they are promoting their own products, what they don't do is find the very best product for your circumstances and sell you that one.

You can get a true service from other large suppliers like Tilney etc who will look at whole of market.

The real difference is that the IFA has no control over the cost of those investments whereas the the real benefit of only selling your own in house products is that you can not only bury wider fees within the spread of each product but you can also cash in on slippage during execution! On top of that, you're also the fund manager but with no third party customers to query either the activity/turnover or the execution costs.

What this means is that if you take a publicly listed fund that is open to the whole market you have to be transparent and competitive. So your spread, technically your dealing charge is kept tiny because of you widen it out you lose flow to your competition. Likewise, if you buy and sell within your fund you will also need to be transparent. Finally, your execution costs are almost nothing as you will be exchange members but also have super competitive clearing. And finally you have no ability to slip the price on any fills. Conversely, if you run your funds in house and restrict them only to in house end customers almost none of this applies.

In that scenario you have the clear potential for a bandit's charter. First of all your bid and offer isn't defined by competitive market forces which means you can widen it out and capture a chunky commission that no one sees. You can even potentially slip the fills to make that even wider, clipping a penny on the execution adds a huge amount to the bottom line. Inside the fund you can then do a bit of churning, a bit of unnecessary buying and selling to generate comms. At the same time you can mark up your internal fund dealing costs so as to have an unreported commission flow. All these charges just clip the end performance to the customer. Instead of them banking 10% they get 8% as you've snuck 2% of additional, non transparent charges into your model.

What you can easily create is a system which benignly sucks out unreported fees. You could completely replicate a Fundsmith product but deal on a wider spread and manage with inflated execution costs. You can even do a bit of churning such as switching BP for Shell. You could even look to combat the underperformance by adopting a bit more risk to compensate but the better mechanism is to apply a PR and marketing layer and enhanced systems to retain clients. Ultimately, so long as your returns are roughly in line with the market the end customer who isn't aware of these hidden charges won't even be bothered.

A less scrupulous player could rip the arse out of a retail client base via a closed shop mechanism. Their own salesmen wouldn't even know.

“Broker Bestinvest’s “Spot the Dog” study, which names and shames funds that return substantially less than their benchmarks, found wealth manager St James’s Place and fund groups Jupiter and Abrdn had the highest number of poorly performing funds.”

https://www.telegraph.co.uk/investing/funds/worst-...

https://www.telegraph.co.uk/investing/funds/worst-...

Amazing the rigorous "no name and shame" policy doesn't seem to apply to industries that don't advertise their products on ponds.

Express an opinion on a used car dealer? Post deleted. Express a similar opinion about a financial adviser that doesn't advertise on the same platform... quelle surprise!

By no means is this a criticism of this discussion - I'm no fan of SJP or their products. I just don't like censorship that is detrimental to the community a platform is supposed to serve.

Express an opinion on a used car dealer? Post deleted. Express a similar opinion about a financial adviser that doesn't advertise on the same platform... quelle surprise!

By no means is this a criticism of this discussion - I'm no fan of SJP or their products. I just don't like censorship that is detrimental to the community a platform is supposed to serve.

Last year my return with SJP was 7.2% net to me so after fees.

By comparison the return on my ISA’s with NatWest currently stands at around 2.5%.

I don’t think it’s all bad and every fund will have good and bad times.

Some of the funds that posted 17% returns when the market bounced may have equally given up those gains when a big downturn happened if they were in heavily leveraged funds.

By comparison the return on my ISA’s with NatWest currently stands at around 2.5%.

I don’t think it’s all bad and every fund will have good and bad times.

Some of the funds that posted 17% returns when the market bounced may have equally given up those gains when a big downturn happened if they were in heavily leveraged funds.

GT3Manthey said:

Last year my return with SJP was 7.2% net to me so after fees.

By comparison the return on my ISA’s with NatWest currently stands at around 2.5%.

I don’t think it’s all bad and every fund will have good and bad times.

Some of the funds that posted 17% returns when the market bounced may have equally given up those gains when a big downturn happened if they were in heavily leveraged funds.

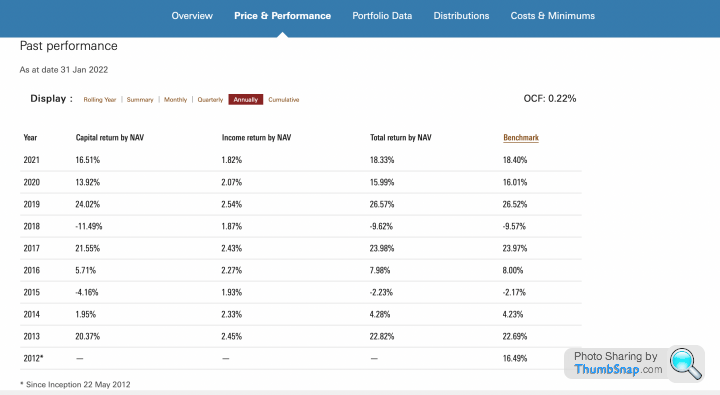

Just an example, but what a simple low-cost (0.37%) global etf would of returned. Easy as 1,2,3, to set up. By comparison the return on my ISA’s with NatWest currently stands at around 2.5%.

I don’t think it’s all bad and every fund will have good and bad times.

Some of the funds that posted 17% returns when the market bounced may have equally given up those gains when a big downturn happened if they were in heavily leveraged funds.

dingg said:

Isa is just the wrapper, its the investment contained in the wrapper that counts

Indeed…what is the actual investment, that is the question!Medium risk low cost index trackers did around that mark…& slightly higher risk (eg, IM80 or IM100) exceeded that, even though the figures here include the rather poor Jan22! Vanguard numbers easily found here

Gassing Station | Finance | Top of Page | What's New | My Stuff