Windscreen Claims WILL Affect Your NCD

Discussion

graham22 said:

The point being missed here is that by using one national supplier, the insurer only has to make one payment a month (at a discounted cost) rather than to many differing invoices etc - unfortunately it's the ways of big companies who are being forced to cut costs by comparisom websites (OK better savings could be made elsewhere but that's not the point of this thread).

Another factor is Autoglass only do windscreens. As a broker I've seen windscreen invoices from garages who don't do windscreens coincedently when their customer has recently had an unexpected mechanical repair or MoT bill. I've also seen invoices from independent glass replacement companies for work that's never been done - no inspection of broken glass = nice little earner for customer & glass co.

In nearly 30 years of driving I've had 1 windscreen and 2 chip repairs yet I see customers with several breakages over a short period.

I do feel that ultimately this will benefit the smaller local repairers.

Can't argue with any of that TBF. Another factor is Autoglass only do windscreens. As a broker I've seen windscreen invoices from garages who don't do windscreens coincedently when their customer has recently had an unexpected mechanical repair or MoT bill. I've also seen invoices from independent glass replacement companies for work that's never been done - no inspection of broken glass = nice little earner for customer & glass co.

In nearly 30 years of driving I've had 1 windscreen and 2 chip repairs yet I see customers with several breakages over a short period.

I do feel that ultimately this will benefit the smaller local repairers.

There are all sorts of issues which ever way you look at it. Ultimately, the way things are, the bottom line is cost. By imposing limits, or capping payouts to non-approved repairers means they [the insurers] can benefit from the average invoice value their nominated supplier gives them under their agreement.

For all the smaller companies who state they're 'insurance approved', they're not. They are bound by some very badly written (and biased) terms and conditions set out by the insurance company's nominated supplier [cough]a company also owned by the same parent company as their nominated supplier[/cough] to whom they are contracted to, acting as a price comparator using a supplier invoice control program ( "SICP" ) under the 'trading name' of Glasscare (owned by Belron, who also own Autoglass) or windscreen invoice control system ( "WICS" ) operated by Nationwide Network Services (who also run Nationwide Motorglass) and 'Quick Quote' which is operated by the same people behind National Windscreens... you get the picture!

Not only are these smaller companies helping the larger companies get away with murder, they're providing them with work (yes, these non-approved supplier invoices can be 'billed on' for a commission/fee!) they are also contributing to their own demise.

BorkFactor said:

I had my windscreen replaced by Bell and called up before hand asking them if I was to hypothetically claim for a windscreen, would it affect my no claims? I was told no, it had no bearing on it at all.

Come renewal time I put my details in on their website without mentioning it and the price was identical, so for the Admiral group at least it doesn't do anything.

So many contrasting accounts. I've spoken to over a dozen people over the last few months, all of whom were insured with Admiral. Thy all stated that a glass claim had some bearing on their renewal. By contrast, many said there was no change whatsover. Come renewal time I put my details in on their website without mentioning it and the price was identical, so for the Admiral group at least it doesn't do anything.

crossy67 said:

graham22 said:

I've also seen invoices from independent glass replacement companies for work that's never been done - no inspection of broken glass = nice little earner for customer & glass co.

I've owned my own small independent windscreen company and worked for a few others, including Autoglass. Whilst working at other indies I have never, never seen anything billed that wasn't fitted or done. On the other hand whilst at Autoglass I have also never seen bills being issued for parts not used but I have on a daily basis seen parts being used that were not needed to up the branch turnover and earn the management staff a better bonus.If you believe national companies to be squeaky clean you need to look into Auto Windscreens, a few years back they got been caught doing exactly what you claim indies have done but being national they were able to do it on a national scale.

kuro said:

I phoned hastings and they told me ncd would be unaffected

This may not be the case in this instance, but it is worth noting that when calling an insurer in the event of a glass claim, there may be a specific number to call, or an option to select at the automated switchboard. Your call does not always go to the insurer. If/when this happens, the person answering the call will usually answer that dedicated line with, 'hello glass line' or something similar. This may give you the impression you're talking to your insurer...

CoolHands said:

there doesn't seem to be a default answer for this, but: are the autoglass etc screens as good quality as oem or not? Is there any noticeable difference.

Yes there is a difference. OEM is the best available, no question. Even the ones made by the same glass manufacturer will show differences in quality and/or hardware. In some (rare examples) the OEM (car manufacturer logo) is removed for the aftermarket distributors. http://www.glasstecpaul.com/windscreen-manufacture...

LoonR1 said:

Glassman said:

This may not be the case in this instance, but it is worth noting that when calling an insurer in the event of a glass claim, there may be a specific number to call, or an option to select at the automated switchboard. Your call does not always go to the insurer.

If/when this happens, the person answering the call will usually answer that dedicated line with, 'hello glass line' or something similar. This may give you the impression you're talking to your insurer...

You know glass, I know insurance. The only insurer that I'm aware of where a glass claim affects your NCD and / or premium is Swiftcover, nobody else cares. If/when this happens, the person answering the call will usually answer that dedicated line with, 'hello glass line' or something similar. This may give you the impression you're talking to your insurer...

One thing is clear (looking at it from a consumer POV) is that this subject is not made clear by the insurers. Just like the matter of approved/nominated/preferred repairers isn't made clear before inception. Using words and terms like, 'windscreen cover is unlimited' is not good enough if the (hard to find) smallprint stipulates an addendum, "as long as our nominated repairer is used".

LoonR1 said:

Glassman said:

LoonR1 said:

The premium will always rise after a claim as your risk has increased.

...except for windscreen/glass claims, is that right? Or...sampsan said:

I used Autoglass, rang for a quote as was going to pay myself. That will be £175 sir, great please complete the work.

On the day of the works, fitter turned up with paperwork. He suggested that I could claim on my insurance and without thinking signed the forms and work was completed. Didn't think much more of it.

Some time later received a letter from my insurance company stating they had received a invoice from Autoglass and I was not covered for Windscreen therefore please find enclosed the invoice to pay directly.

No issues, my fault and should have checked the policy.

Then........ noticed the Autoglass invoice to the insurance company was not the £175 quoted but had risen to £480.

Following this had a major fall out with them where they denied the quote and refused to reduce the costs, this got silly with me telling them to come and remove the windscreen and take it away. Anyway eventually agreed on a reasonable amount but have never dealt with people so aggressive and unwilling to say anything apart from give me your money.

So lessons learnt.... they rip off insurance companies and always get a quote in writing.

Are you sure it was Autoglass, and not the Camorra? On the day of the works, fitter turned up with paperwork. He suggested that I could claim on my insurance and without thinking signed the forms and work was completed. Didn't think much more of it.

Some time later received a letter from my insurance company stating they had received a invoice from Autoglass and I was not covered for Windscreen therefore please find enclosed the invoice to pay directly.

No issues, my fault and should have checked the policy.

Then........ noticed the Autoglass invoice to the insurance company was not the £175 quoted but had risen to £480.

Following this had a major fall out with them where they denied the quote and refused to reduce the costs, this got silly with me telling them to come and remove the windscreen and take it away. Anyway eventually agreed on a reasonable amount but have never dealt with people so aggressive and unwilling to say anything apart from give me your money.

So lessons learnt.... they rip off insurance companies and always get a quote in writing.

LoonR1 said:

Glassman said:

LoonR1 said:

excuse me for trying to correct the ill -informed and simply incorrect stuff being posted on this thread.

Can we see some facts please? It seems most insurers don't like putting any of this stuff in writing. The thread title can be disproven via policy booklets.

addey said:

I am with Swiftcover and have a chip on my windscreen - if I claim what is the effect on my premium?

No idea. Ask them, there are literally thousands of rating factors all of which will interact to produce your premium. LoonR1 said:

And to bring some closure I've quoted your opening post below. It's clear that you have chosen Hastings Direct as the prompt for this whole thread over 4 years ago. Here's the Hastings booklet

http://www.hastingsdirect.com/documents/Policy_doc...

Section 8 page 25

http://www.hastingsdirect.com/about-us/news/100726.htmlhttp://www.hastingsdirect.com/documents/Policy_doc...

Section 8 page 25

Glassman said:

Hastings Direct are reported to be revising their policies to include a few interesting changes, one stands out quite clearly: "windscreen claims will affect no claims discounts and excesses will be doubled if policyholders choose their own repairer." This is to enable HD to offer drivers a 'no frills comprehensive car insurance policy to help cut motoring costs.

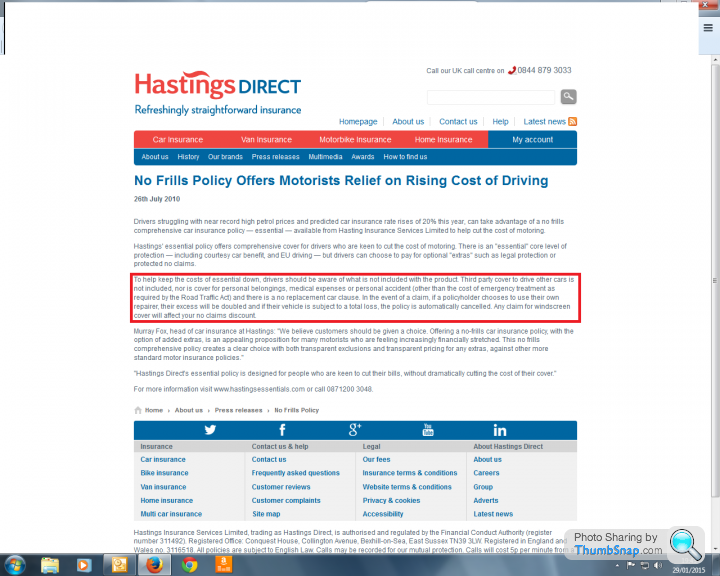

Furthermore, Equity Red Star, Fortis and NIG are to withdraw from personal lines, ie, private motor insurance (according to a broker in London). These are the type of policies that are bread and butter to a lot of brokers; with price online sales and price comparison websites it's a tough business for the motor insurance broker. But it's not just the guys in the broker world, with these changes to Key Facts and underwriters pulling out of motor insurance, is this the industry stepping sideways?

For the policyholder (with HD) this means (in the event of a windscreen claim) you will go with who we tell you to, or you get your wallet spanked.

Furthermore, Equity Red Star, Fortis and NIG are to withdraw from personal lines, ie, private motor insurance (according to a broker in London). These are the type of policies that are bread and butter to a lot of brokers; with price online sales and price comparison websites it's a tough business for the motor insurance broker. But it's not just the guys in the broker world, with these changes to Key Facts and underwriters pulling out of motor insurance, is this the industry stepping sideways?

For the policyholder (with HD) this means (in the event of a windscreen claim) you will go with who we tell you to, or you get your wallet spanked.

LoonR1 said:

Can you please show me your staff salaries please, otherwise you're just proving to me that you pay below minimum wage.

About as related to the subject as the relationship between NCD and loading premiums following a glass claim. At the time of starting the thread, the statement in the OP was pretty bang on and true. You claim to debunk the claim the title of this thread, but a) you confirm there's at least one insurer who will frig a PH's NCD following a glass claim, and b) Hastings Direct state this which, at the time was true. No date confusion, and link with corresponding date/timestamp provided.

Others have stated that there may be a premium issue subsequent to a glass claim; again, Hastings (from the link you very kindly provided) state in Section 9:

"No-claim discount

"If you have protected no-claims discount, there is no guarantee that your premium will not increase".

Yet you're digging your heels in stating that the insurers are 'not bothered' by glass claims. In another post you say a 'claim' is a perceived risk, etc...

I'm just trying to understand which part(s) are correct. References are always good back up. What I pay, whether I pay; to whom I pay has no relevance whatsoever.

LoonR1 said:

Can I come into your business and get all the details of how you make money please. I'll takenit to your competitors and see how long survive.

Will a glass claim affect NCD? Not with all insurers. OK then, will my premium rise as a result of a glass claim. IOW, is there a claw-back, or are the insurers hiding behind the NCD thing but will still hike up the premium under a different guise etc etc? It's this bit that most people think is true and some are presenting themselves as case examples. You say this is b

ks. A simple bit of evidence will suffice. Nothing to do with margins, profit, inside leg measurements or anything else. What's so secretive about it? Does a windscreen claim mean mine premium will go up as a result. You say no. Others say yes. They have the premium (and their insurer's words to back it up). You go all stush about it.

ks. A simple bit of evidence will suffice. Nothing to do with margins, profit, inside leg measurements or anything else. What's so secretive about it? Does a windscreen claim mean mine premium will go up as a result. You say no. Others say yes. They have the premium (and their insurer's words to back it up). You go all stush about it.

Gassing Station | General Gassing | Top of Page | What's New | My Stuff