AML - Stock Market Listing

Discussion

oilit said:

I saw an article recently which suggested that if the younger Stroll gets kicked out/gets bored/takes up monopoly from the f1 that Stroll senior will want to offload the whole lot.

It wasn’t clear if that mean the whole F1 team or the whole of AM ….

It wasn’t clear if that mean the whole F1 team or the whole of AM ….

Trying to apply logic to this;

1. - LS must be more interested in his privately owned Formula One team, than the AML road cars business.

2. - If he does sell the race team, why would he then want to continue as Chairman of AML ?

I cannot think of a reason.

AstonV said:

This guy can really spew a line of horse manure.

We must admit though, that many AML share buyers seem to believe every word.

This is revealed on the share chat forums and by the share price increases following his statements.

Do you think the, 'We don't need money' comment, might have been on the wrong side of any stock exchange rules?

Public statements by directors, which within just a few months are seen to be incorrect, are at one extreme most unfortunate and at the other end ...........

Last year Lawrence Stroll was reported to have said, "This company will be cash-flow positive in 2023."

Interesting, we will find out next March.

That comment excited share buyers, because positive cash flow has hardly ever been achieved at AML. As for the 'billions of Formula One views' benefiting AM sales, well unfortunately, no sign yet in the published sales numbers.

Q3 Results.

Everything going really well.

Continued strong demand across existing and new product lines; the recently launched DB12 is driving reappraisal of Aston Martin with order book now extending to Q2 2024.

DBX orders also extending into 2024, as it continues to establish itself as the benchmark in the ultra-luxury SUV segment with over 25% market share in key markets.

Message from LS;

"Our 110th anniversary year continues to be a fantastic one for the Company, and we are delighted with the strategic and financial progress we have made during the first nine months of 2023. Our volumes, pricing, gross margins and EBITDA are showing strong improvement and we are delivering an accelerated industrial turnaround.

- Hide this in the small print.

Only lost £117 million in Q3 and debt is £749,900,000

'In line with the announcement in July, our objective is to repay the second lien in full. During November, we will be redeeming 50% of the outstanding second lien notes and beyond that, we intend to undertake a fulsome refinancing exercise during the first half of 2024'.

(Click images to enlarge)

I have just realised an interesting point.

AML no longer publish retail sales, however for the UK we can see the figures, because the DVLA provide new registration numbers.

2023 (to 30th September), the UK wholesale numbers increased, whereas the new registrations decreased.

Does that mean the dealer stock has increased ?

Edited by Jon39 on Wednesday 1st November 08:32

The share chat rooms can be places for amusement.

Some posters are presumably day traders trying to influence share prices, others are mischievous and some think they know about investing, but clearly need far more practical experience.

Posts after the AML Q3 Results announcement, but before the Stock Market opened.

Here is a post after stock market trading began.

AML share price 185.7p down 15%.

I don't expect AML want these figures to be compared, but it is all publicly published information so there we are.

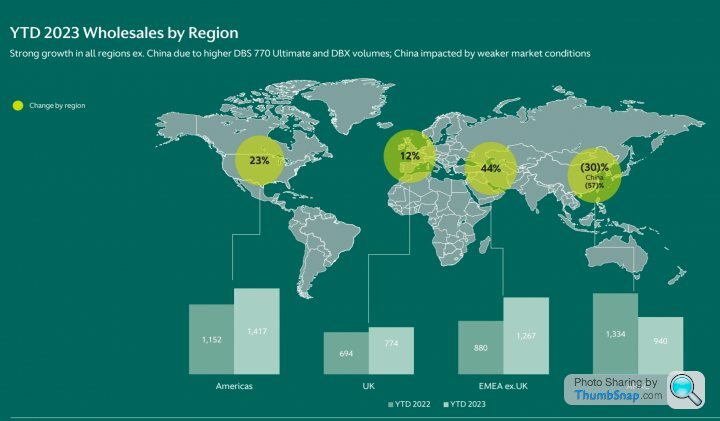

UNITED kINGDOM

YTD 2023 (to 30th September) Wholesales;

2022 = 694

2023 = 774

(per AML)

UNITED KINGDOM

YTD 2023 (to 30th September) New Aston Martin Registrations;

2022 = 834

2023 = 784

(per DVLA)

What does this tell us?

In 2022 (to Q3) 140 (20%) more Aston Martins were registered for the first time, than Aston Martin sold to their UK dealers.

In 2023 (to Q3) 10 more Aston Martins were registered for the first time, than Aston Martin sold to their UK dealers.

This is where the guessing starts.

Dealer stock levels presumably reduced during 2022, whereas the balance was close this year.

Most of the new registration cars would be retail sales, but some would be;

1. Dealer demonstrators (wholesales, but not retails).

2. Aston Martin must register new cars for their own use eg. staff cars; press cars; development cars, so presumably these cars would not be counted as wholesales (sales to dealers).

There we are. Some numbers, but probably does not tell us much about the business.

China figures showed a dramatic fall of 57%. AML once had great hopes for that export market.

The DBX 3 litre straight six was offered for sale in China. Has anyone heard any more about that model?

I think the 3 litre engine capacity, placed the car in a much more favourable tax bracket.

RL17 said:

One article today says just 6,700 DB12s to be sold this year (down from 7,000).

Assume this is total vehicles including DBX?

Assume this is total vehicles including DBX?

Yes that is correct, Reg.

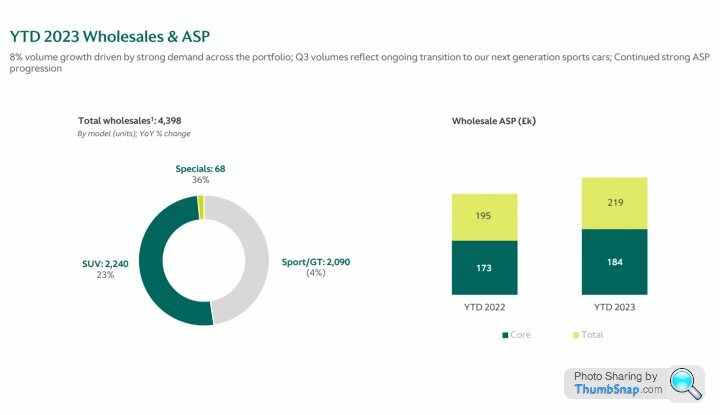

Number of sales (wholesale) 2023 year to 30th September

Sports/GTs ..... = 2090

Specials ......... = ... 90

SUVs ............. = 2240

Total .............. = 4398 ( therefore average per quarter = 1466 )

AML Guidance for full year 2023

Wholesales Growth to c.6,700 units (revised from c.7,000 units)

Therefore need 2302 in the final quarter to achieve the revised target.

Link to the 2023 Quarter 3 Presentation, where you can find greater detail.

https://www.astonmartin.com/-/media/corporate/docu...

RL17 said:

Telegraph!

Some early evening amusement - looking for any more mistakes in the article.

(Might be a slight delay before opening.)

https://archive.ph/8EprH

TELEGRAPH VERSION

'This marks a setback for the company’s billionaire owner Lawrence Stroll who has been attempting to turn the business around.'

MR STROLL VERSION

"We have rebuilt this iconic company, transforming it into an ultra-luxury brand, with a portfolio of highly desirable, performance-driven cars. The company has delivered a major turnaround since the Yew Tree Consortium’s initial investment three years ago."

TELEGRAPH

'Chief executive Amedeo Felisa hailed the “exceptional demand” for the DB12 but said that “given the slight delays in the initial production ramp-up we have marginally updated our volume expectations for the year”.'

AMENDMENT

'Chief executive Amedeo Felisa. "Mr. Stroll told me to say, I hail the exceptional demand

for the DB12 ...... continues

At 77 years of age, I need to go slower these days (cannot keep up with Mick Jagger, 80 years old), which explains why I used the hesitant words slight delays and marginally updated. -

Edited by Jon39 on Thursday 2nd November 19:34

SSO said:

Jon39 said:

28,352,273 new ordinary shares issued to a Lucid subsidiary on Monday.

In theory, more shares in issue means each existing share becomes worth less, but there was not much difference at the close of trading.

I read your Q3 review SSO. Thanks for taking the time to prepare that.

I thought one of your Comments people were rather unkind (probably someone who believes every word LS says), by saying something about you 'knocking this Company'.

Having studied the entire business history of Bamford and Martin and Aston Martin, I consider your AML reviews to be accurate and factual.

The Stroll statement listeners seem to think, that after 110 years of continually selling a relatively modest number of cars and always spending more than earnings, that steady profitability is suddenly going to happen.

I am sure that you know SSO, that the best business era for AML was during and just after, the Ford ownership period. The DB7 then the popular VH range of three core models, enormously increased the annual sales numbers. Record production was achieved in 2007 with 7281 sports cars (no DBX then). That figure has never been exceeded.

Mostly single figure £millions pre-tax profits were reported from 2000 to 2010 (£57m in 2006), but those were somewhat inflated because the accounts reveal new model development costs being repaid by Ford. I assume that Ford also paid for preparing Bloxham for DB7 production and for construction of the new Gaydon factory.

A rocky road for 110 years, but what a survivor!

Every time that more money was/is required (2024 next top-up), it magically appears.

Everyone has always known Aston Martin for beautiful and exciting cars and don't worry about the money.

Edited by Jon39 on Wednesday 8th November 17:42

Ghini said:

PIF is now the second largest shareholder after Stroll / Yewtree consortium. Most people seem to think Geely is the main contender to take over AML. On the other hand PIF increased their holding via the Lucid tech deal and they are also involved in Strolls F1 team so they could take over both.

It seems to me that Stroll set up two parties with deep pockets and a conflict of interest against each other.

What is your take on this?

It seems to me that Stroll set up two parties with deep pockets and a conflict of interest against each other.

What is your take on this?

Car maker, or Investment fund?

People might feel a car manufacturer would be the best owner.

Thinking about that though, Daimler's purchase of Chrysler did not go well.

There must be many other similar examples.

Geely's purchase of Volvo does seem to be successful.

When Ford owned Aston Martin, they provided money and production engineering guidance, but otherwise we are told, kept at 'arms length, for AML to do Aston Martiny things. That worked really well (for Aston Martin, although must have been expensive for Ford).

InvestIndustrial is an investment fund and we remember what happened there.

At present LS seems to be able to continually raise more money from shareholders, so no requirement for additional financial support.

It is when the bonds mature and need refinancing that it might be awkward. When the present bond debt was arranged, general interest rates were at historic lows, but even then, AML had to pay 10% interest. What might the interest rate be next time and will lenders be willing to lend ?

LTP said:

... This is why the VH cars have magnesium die-castings for the door inner structure ... - ... the latest cars have deep-drawn aluminium pressings, plus some extrusions and brackets, thus avoiding some of the bimetallic corrosion that plagued the bottom edges of doors on early VH cars. And the cost of die-casting tooling.

Ford also provided Engineering Standards, sign-off to which was mandatory (unless you're Volvo) and access to the parts bin, of course.

IMHO Aston needs an automotive big brother, not another bunch of money men who know the cost of everything and the value of nothing.

Ford also provided Engineering Standards, sign-off to which was mandatory (unless you're Volvo) and access to the parts bin, of course.

IMHO Aston needs an automotive big brother, not another bunch of money men who know the cost of everything and the value of nothing.

Yes, an automotive big brother who acts in the same way as Ford did, ie. does not interfere with the Aston Martin creativity and specialness. A big brother would not derive any financial benefit (in fact must be prepared for the opposite), but perhaps might be satisfied with the image association.

You refer to 'early VH cars'. Up to what year would that have been, when the change was introduced ?

I don't think I can remember complaints on PH, about corrosion on the bottom edges of doors.

KevinBird said:

Looks like the software issues on the DB12 preventing deliveries, has now hit the share price. It’s under 200 this morning

No worries though.

If Mr. Stroll mentions cash flow positive in 2024 H1, that should help.

Mind you, if I can remember correctly, that was 'promised' for 2023 Q4.

If they can somehow persuade the accountants to regard the, 'and intend to undertake a fulsome refinancing exercise during H1 2024' as cashflow, then it might be achieveable.

Some of the AML shares short-term gamblers, who post on share chat forums, regard cash flow positive and EBITDA just as good as profit in the bank, so they might start buying the shares again. They have an interesting system; buy, then try to encourage the next person to pay more. Sometimes it works. -

Ghini said:

IR: "The reference to “fulsome refinancing exercise" made at the Q3 results on 1 November 2023 was in relation to a review of the entire stack of 1st and 2nd Lien Debt. We will carry out a full review in 1H24 in order to optimise the debt structure of the Group over the medium term."

Yes. There is now a track record with some of their statements, making us confused about what they mean. There could probably be quite a debate, about what is intended by the word fulsome. Enormous perhaps ?

I remember during one of cash raising exercises, where AML said, 'up to 50% will be used to pay down debt'.

That sentence was in a very lengthy prospectus and I did not notice the words, 'up to'. Later I could not understand why so little of the money raised, had been used to redeem debt, but subsequently realised it was 'up to' 50%. I was taken in as the perfect investor, mistakenly thinking that reducing debt was serious.

In reality, for a business that continually spends more than it earns, keeping back as much as possible from each cash raise, ensures the business expenses cash lasts longer.

Interesting how some people repeatedly seem to believe that each new model is about to make the Company profitable for the first time.

It is fun for us when a new model is in prospect. Spy shots are discovered and discussion takes place about what is going to be unveiled, but one new model is hardly going to make £1 billion profit to considerably reduce debt.

Ghini said:

Ha yes. I have played with some rough forecasts in the past to see what was needed and how many years it would take to half the dept. It was a harsh reality to see, even with all models and version steadily growing sales numbers, 40% margin, specials etc. DB12 and new Vantage already cost a lot to get on the road, although we do not know what they spend but we do know there is not a lot of money reserved for electrification and other completly new models. (I would love to get a better insight in the financials of the development and how far they are with future projects.) All the money they would earn on current / short term new models is needed for development of the long term future completly new models. It barely covers the costs of that if every models needs to be replaced with a completly new one, even with shared base and on top they need to be electrified, wich costs a lot more. ...

The behind the scenes people talk about ever increasing costs of developing new models.

We only need to think about all the recent compulsory equipment for every car, imposed by regulations.

The major car manufacturers talk of new model development costs in the billions. It is obviously not feasible that it could be that much for Aston Martin, but it is not clear to me, why it can cost less for a small volume manufacturer. The process of design, development, testing, approval etc., must be similar.

The talk of 40% margin must presumably be a gross figure. It is rather like the EBITDA talk, trying to almost make out that is profit in the bank. Mr. Charlie Munger was very outspoken about the (fairly) recent widespread use of EBITDA, which I must not repeat here. His polite version was Earnings before every cost is subtracted (EBE, earnings before everything, ie. meaningless).

Within your forecasting studies, have you researched the 2005 to 2007 period. Production was flat out, unable to meet demand with an annual production record set of about 7,300. Remember too, all of those were sports cars, whereas now 50% of the total are SUVs.

I don't know what the gross profit margin was in those days, it was not something that was mentioned, although the accounts would give an overall indication. You will know that the historic accounts can be inspected on the Companies House website.

That very successful period (not profitable though, without the Ford payments) came to an abrupt end, when the 2008 financial crisis started. Customers cancelled orders and there were redundancies at Gaydon. A difficult time for everyone.

Calinours said:

Another few interesting comments by SSO…

https://karenable.com/santa-grinch/

Scroll to the end. A possible debt for equity swap is hinted for year end. The interest payments on the debt must be crippling, the CFO will likely be hoping for the forecast central bank rate reductions to result in cheaper debt servicing as a result of the ‘fulsome exercise’

https://karenable.com/santa-grinch/

Scroll to the end. A possible debt for equity swap is hinted for year end. The interest payments on the debt must be crippling, the CFO will likely be hoping for the forecast central bank rate reductions to result in cheaper debt servicing as a result of the ‘fulsome exercise’

During the Mr. Stroll era, there has been a continuation of the traditional Aston Martin money raising and (even more) spending.

There is a difference though now. A considerable increase in the magnitude of fund raising and spending. So far since the IPO, about £1,500,000,000 has been raised from shareholders. Any shareholders who have not contributed, have seen their holdings considerably diluted.

The difference of course being, there are now a huge number of shareholders available (and willing) to contribute, compared to earlier times.

Fund raising has tended to take place annually and the next (indicated 2024 Q1), has already been announced during the 2023 Q3 results statement.

Regarding debt reduction. This has been quite strange.

During one fund raising, it was announced, 'up to 50% of the capital raised will be used to reduce debt'.

In the event, far less than 50% was used for debt reduction.

The 2023 fund raising also made reference to a debt reduction in November 2023.

I had expected to see a Company announcement to the London Stock Exchange confirming that had taken place, but I have not noticed an announcement.

Is it perhaps more fun to have money available for spending, than to reduce borrowing ?

Edited by Jon39 on Saturday 30th December 15:08

leef44 said:

No doubt this is the only feasible exit strategy from bankruptcy due to unmanageable debts (where interest payments are so high that there is insufficient cashflow to service). So AM has to manage this to avoid getting into this scenario.

But as you mention, they have to spend to prop up the share price to prove that they are moving forward and growing. It's a fine balance to manage.

But as you mention, they have to spend to prop up the share price to prove that they are moving forward and growing. It's a fine balance to manage.

Most of the present debt, is in the form of fairly short term bonds.

I don't have the details to hand, but the maturity repayment dates might be 2026.

The pattern before, has been to refinance a year or so, in advance of maturity.

The interest rates are at least 10% and those were agreed when bank rate was almost zero.

Now with a bank rate at a more normal 5%, will that make the refinancing negotiations more difficult?

We can follow the UK new registrations monthly, but as for other markets we just have to wait for Company announcements, so to answer your question - No idea.

New sales must have been hindered, by the widespread awareness of a revised Vantage and DBX coming.

Spotting spy shots is one thing, but it is odd that the Company have spoken openly in advance of new model announcements.

12TS said:

They must be suffering in the uk, if Porsche are. ...

That will be a surprise to some people.-

Prior to the public flotation of Aston Martin, amongst the confetti of hype, CEO Andy Palmer said, Aston Martin is no longer a car manufacturer, but a luxury goods business and therefore will no longer be affected by economic downturns.

amongst the people who belived that, were prospective Aston Martin Lagonda shareholders, who thought the Company was worth £4 billion and also City financiers, who could smell the aroma of huge fees.

Gassing Station | Aston Martin | Top of Page | What's New | My Stuff