These fifty grand loans

Discussion

Tyre Smoke said:

You sound exactly who this loan is aimed at. You should take as much as you can get. There is nothing at all to pay for 12 months, so this time next year, pay off what you haven't used and work at the rest over the next few years. It's by far the cheapest form of borrowing.

I intend to clear my overdraft (10% over base) and sit on the rest as back up.

I currently aren't into my overdraft yet and am trying to avoid doing so as the O/D is secured on the business premises (10k O/D secured on 200k property! Would rather not use it if possible). Mine is a very small business, last years turnover only around 95k so based on 25% of that the most I could borrow would be around 24k.I intend to clear my overdraft (10% over base) and sit on the rest as back up.

I agree it might be best to take the maximum possible loan and pay some/all of the unrequired amount back before payments are due. Just a bit wary of taking on a big lump of debt until I'm 100% sure they can't come after me personally if I have to fold the business down the road anyway.

But, at those interest rates it's a spectacular deal on borrowing so it's VERY tempting.

I don't need the money immediately so I was planning to sit it out for the first couple of weeks to see how these loans pan out in reality once the Banks start processing them.

I'm thinking of applying for this and considering it as a business development loan/backup.

Sit on the money until the world stabilises a bit, seeing whether there's demand again for the existing business, and if not, decide whether to "diversify", using the loan, or find salaried work and just send the loan back.

Any reason not to do this?

Sit on the money until the world stabilises a bit, seeing whether there's demand again for the existing business, and if not, decide whether to "diversify", using the loan, or find salaried work and just send the loan back.

Any reason not to do this?

Escapegoat said:

Hmmm...

I wonder how many low-asset Ltd businesses will take it as a last-gasp opportunity to gouge a big salary out of thin air for a year?

I am not an economist but I suspect that is still preferable to just giving money to the Banks as they did in '08.I wonder how many low-asset Ltd businesses will take it as a last-gasp opportunity to gouge a big salary out of thin air for a year?

If it saves a business - great

If it helps a business expand - great

If the boss pisses it up the wall - great, stimulating the economy.

Leave it in the Bank - great, improves Bank liquidity and instantly available if required.

Give it direct to the Banks - not great, they won't lend and will use it to sustain themselves.

crosseyedlion said:

Also, what if you're not with a bank that's currently participating in the scheme?

For the CBIL, the British Business Bank mentions for following:4. IF THE LENDER TURNS YOU DOWN

If one lender turns you down, you can still approach other lenders within the scheme.

Might be the same for the Bounce Back Loan (as in that you don't have to bank with lenders in the scheme).

https://www.british-business-bank.co.uk/ourpartner...

Edited by Powerfully Built PSC Director - Outside IR35 on Saturday 2nd May 16:35

Phooey said:

Sounds a steal. Can your bank turn you away if it doesn't think you need it? I was thinking of buying another pick-up this year (approx £30k+vat) and stuffing a bit more into my pension via a company contribution. I can't really put them 2 reasons down for needing a 50k loan can I?

That would sound like you'd be 'protecting cashflow'.

Phooey said:

Sounds a steal. Can your bank turn you away if it doesn't think you need it? I was thinking of buying another pick-up this year (approx £30k+vat) and stuffing a bit more into my pension via a company contribution. I can't really put them 2 reasons down for needing a 50k loan can I?

Think the pension contribution might be pushing it a bit far :heheJPJPJP said:

mondeoman said:

Just wondering if you can have a CBILs loan AND one of these?

https://www.gov.uk/guidance/apply-for-a-coronaviru...

I reckon if the CBILS is still "in process" (which takes forever, hence the bounce back) and you apply for a bounce back, you could then just cancel the CBILs application.

I need £17k, and I need it next week, but its been so painful getting through to anyone and getting anything started - you'd think the banks wanted businesses to fail.

mondeoman said:

JPJPJP said:

mondeoman said:

Just wondering if you can have a CBILs loan AND one of these?

https://www.gov.uk/guidance/apply-for-a-coronaviru...

I reckon if the CBILS is still "in process" (which takes forever, hence the bounce back) and you apply for a bounce back, you could then just cancel the CBILs application.

I need £17k, and I need it next week, but its been so painful getting through to anyone and getting anything started - you'd think the banks wanted businesses to fail.

IMHO, .gov.uk shouldn't rely on banks for such financial assistance. They should use HMRC to credit the "loans" direct to those who need it.

But then again, would that be seen as blatant money printing?

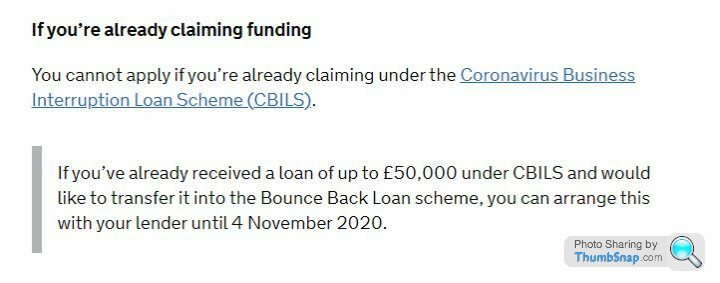

CBILs minimum is now £50,001:

https://assets.publishing.service.gov.uk/governmen...

Interaction between BBLS and the Coronavirus Business Interruption Loan Scheme (CBILS). As you are aware businesses will be able to borrow up to £50,000 under BBLS, capped at 25% of turnover. In order to ensure that businesses have a clear understanding of the support available to them under the loan guarantee schemes, the minimum facility size for term loans and overdrafts under CBILS will increase to £50,001 to avoid any risk of confusion or overlap. Any customer with a CBILS loan or overdraft of £50,000 or less will be able to switch that facility to a BBLS loan should they choose to do so over the next few months. This change to the minimum facility size will not apply to asset finance and invoice finance CBILS facilities.

Does that mean that any CBILs application for under £50k is now void, meaning you have to apply for a BBL instead? What a mess!

https://assets.publishing.service.gov.uk/governmen...

Interaction between BBLS and the Coronavirus Business Interruption Loan Scheme (CBILS). As you are aware businesses will be able to borrow up to £50,000 under BBLS, capped at 25% of turnover. In order to ensure that businesses have a clear understanding of the support available to them under the loan guarantee schemes, the minimum facility size for term loans and overdrafts under CBILS will increase to £50,001 to avoid any risk of confusion or overlap. Any customer with a CBILS loan or overdraft of £50,000 or less will be able to switch that facility to a BBLS loan should they choose to do so over the next few months. This change to the minimum facility size will not apply to asset finance and invoice finance CBILS facilities.

Does that mean that any CBILs application for under £50k is now void, meaning you have to apply for a BBL instead? What a mess!

JamieBeeston said:

No,

just means you've read it wrong.

It's £2k - £50k

the minimum facility size for term loans and overdrafts under CBILS will increase to £50,001just means you've read it wrong.

It's £2k - £50k

What have I read wrong? BBLs is £2k to £50k, my CBILs application is for £17,500 - is my CBILs application now void as the amount requested is below the minimum limit?

mondeoman said:

JamieBeeston said:

No,

just means you've read it wrong.

It's £2k - £50k

the minimum facility size for term loans and overdrafts under CBILS will increase to £50,001just means you've read it wrong.

It's £2k - £50k

What have I read wrong? BBLs is £2k to £50k, my CBILs application is for £17,500 - is my CBILs application now void as the amount requested is below the minimum limit?

Zero reason not to, BBL much better for the borrower.

JamieBeeston said:

mondeoman said:

JamieBeeston said:

No,

just means you've read it wrong.

It's £2k - £50k

the minimum facility size for term loans and overdrafts under CBILS will increase to £50,001just means you've read it wrong.

It's £2k - £50k

What have I read wrong? BBLs is £2k to £50k, my CBILs application is for £17,500 - is my CBILs application now void as the amount requested is below the minimum limit?

Zero reason not to, BBL much better for the borrower.

Article 2 (18) of the Commission Regulation (EU) no. 651/2014 of 17 June 2014

https://eur-lex.europa.eu/legal-content/EN/TXT/PDF...

(18) ‘undertaking in difficulty’ means an undertaking in respect of which at least one of the following circumstances occurs:

(a) In the case of a limited liability company (other than an SME that has been in existence for less than three years or, for the purposes of eligibility for risk finance aid, an SME within 7 years from its first commercial sale that qualifies for risk finance investments following due diligence by the selected financial intermediary), where more than half of its subscribed share capital has disappeared as a result of accumulated losses. This is the case when deduction of accumulated losses from reserves (and all other elements generally considered as part of the own funds of the company) leads to a negative cumulative amount that exceeds half of the subscribed share capital. For the purposes of this provision, ‘limited liability company’ refers in particular to the types of company mentioned in Annex I of Directive 2013/34/EU (1 ) and ‘share capital’ includes, where relevant, any share premium.

(b) In the case of a company where at least some members have unlimited liability for the debt of the company (other than an SME that has been in existence for less than three years or, for the purposes of eligibility for risk finance aid, an SME within 7 years from its first commercial sale that qualifies for risk finance investments following due diligence by the selected financial intermediary), where more than half of its capital as shown in the company accounts has disappeared as a result of accumulated losses. For the purposes of this provision, ‘a company where at least some members have unlimited liability for the debt of the company’ refers in particular to the types of company mentioned in Annex II of Directive 2013/34/EU.

(c) Where the undertaking is subject to collective insolvency proceedings or fulfils the criteria under its domestic law for being placed in collective insolvency proceedings at the request of its creditors.

(d) Where the undertaking has received rescue aid and has not yet reimbursed the loan or terminated the guarantee, or has received restructuring aid and is still subject to a restructuring plan.

(e) In the case of an undertaking that is not an SME, where, for the past two years: (1) the undertaking's book debt to equity ratio has been greater than 7,5 and (2) the undertaking's EBITDA interest coverage ratio has been below 1,0.

https://eur-lex.europa.eu/legal-content/EN/TXT/PDF...

(18) ‘undertaking in difficulty’ means an undertaking in respect of which at least one of the following circumstances occurs:

(a) In the case of a limited liability company (other than an SME that has been in existence for less than three years or, for the purposes of eligibility for risk finance aid, an SME within 7 years from its first commercial sale that qualifies for risk finance investments following due diligence by the selected financial intermediary), where more than half of its subscribed share capital has disappeared as a result of accumulated losses. This is the case when deduction of accumulated losses from reserves (and all other elements generally considered as part of the own funds of the company) leads to a negative cumulative amount that exceeds half of the subscribed share capital. For the purposes of this provision, ‘limited liability company’ refers in particular to the types of company mentioned in Annex I of Directive 2013/34/EU (1 ) and ‘share capital’ includes, where relevant, any share premium.

(b) In the case of a company where at least some members have unlimited liability for the debt of the company (other than an SME that has been in existence for less than three years or, for the purposes of eligibility for risk finance aid, an SME within 7 years from its first commercial sale that qualifies for risk finance investments following due diligence by the selected financial intermediary), where more than half of its capital as shown in the company accounts has disappeared as a result of accumulated losses. For the purposes of this provision, ‘a company where at least some members have unlimited liability for the debt of the company’ refers in particular to the types of company mentioned in Annex II of Directive 2013/34/EU.

(c) Where the undertaking is subject to collective insolvency proceedings or fulfils the criteria under its domestic law for being placed in collective insolvency proceedings at the request of its creditors.

(d) Where the undertaking has received rescue aid and has not yet reimbursed the loan or terminated the guarantee, or has received restructuring aid and is still subject to a restructuring plan.

(e) In the case of an undertaking that is not an SME, where, for the past two years: (1) the undertaking's book debt to equity ratio has been greater than 7,5 and (2) the undertaking's EBITDA interest coverage ratio has been below 1,0.

Gassing Station | Business | Top of Page | What's New | My Stuff