These fifty grand loans

Discussion

fesuvious said:

It's smelling a lot like subsidies to lenders.

Yes, I know it will be a lifeline for many, but once again banks&lenders are being gifted revenue/profits

If (IF) these loans (and CBILS too?) are at this sort of interest rate - why?

Base rate 0.1%

This is giving business a short term bailout, but banking a long-term bailout.

Yes. Another one. I have argued in several arenas that the BoE / HMRC / HM Treasury could have implemented a direct lending scheme for businesses in the time it has "wasted" trying to get commercial banks to deliver the government's intented outcome of the CBILS type schemes.Yes, I know it will be a lifeline for many, but once again banks&lenders are being gifted revenue/profits

If (IF) these loans (and CBILS too?) are at this sort of interest rate - why?

Base rate 0.1%

This is giving business a short term bailout, but banking a long-term bailout.

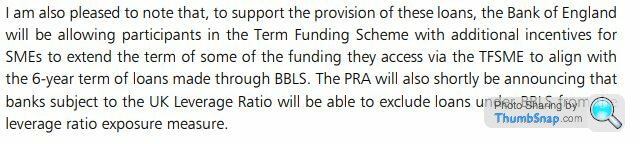

The latest batch of near free money available to banks went live this week too TFSME: 4 year loans from the BoE to commercial banks at base rate linked to how much those banks lend to SMEs

https://www.bankofengland.co.uk/markets/market-not...

Powerfully Built PSC Director - Outside IR35 said:

Interesting...very interesting...

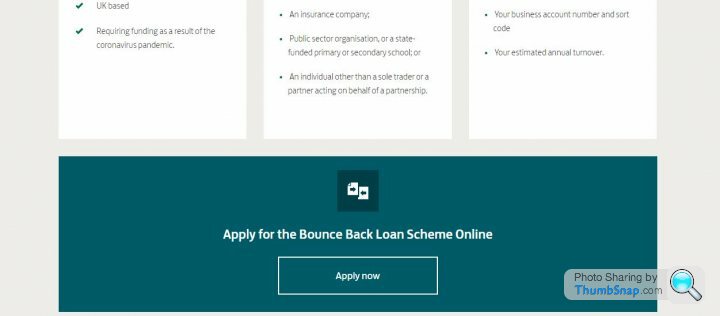

AIUI to obtain a £50k loan would need the PSC to have been doing £200k turnover and not be an undertaking in difficulty on 31 Dec 2019There are some circumstances where popping it the after tax income on £50k PAYE might be attractive, but I think they are fairly few and far between aren't they?

Edited by anonymous-user on Wednesday 29th April 14:27

loafer123 said:

The liquidity the banks use for the loans doesn't cost them 0.1%.

Even LIBOR for 12 months is 0.87%.

It might actually cost them less than 0.1% in the wash up. They will get most of the money through the TFSME, which is 0.1% over 4 years https://www.bankofengland.co.uk/markets/market-not... then, depending on how they can treat the loan from a risk weghting perspective, they might be able to lend more at higher rates as a result of having these loans on their books.Even LIBOR for 12 months is 0.87%.

mondeoman said:

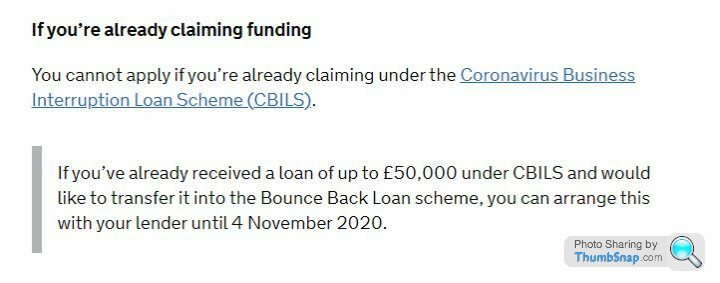

Just wondering if you can have a CBILs loan AND one of these?

https://www.gov.uk/guidance/apply-for-a-coronaviru...

Treasury has done as much as it can: 2.4% spread to the banks, 100% guarantee, not really included in risk weighting

It is over to the commercial banks now. Unless they really do just quickly push this money out of the door to pretty much every business that applies, they aren't going with the spirit of the Chancellor's intentions imo

It is over to the commercial banks now. Unless they really do just quickly push this money out of the door to pretty much every business that applies, they aren't going with the spirit of the Chancellor's intentions imo

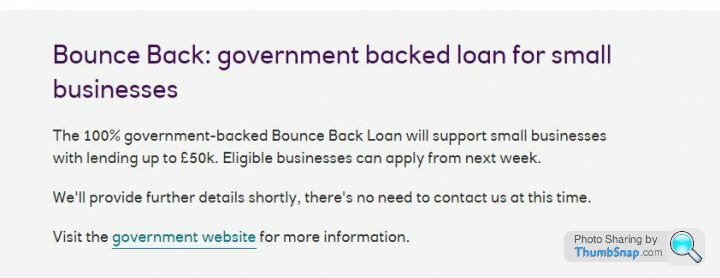

Gov 'apply' site updated

The long and short of it is that you should apply, in the first instance, through your own bank

https://www.gov.uk/guidance/apply-for-a-coronaviru...

it now links to https://www.british-business-bank.co.uk/ourpartner...

and then this detailed page on various things to do with it

https://www.british-business-bank.co.uk/ourpartner...

The long and short of it is that you should apply, in the first instance, through your own bank

https://www.gov.uk/guidance/apply-for-a-coronaviru...

it now links to https://www.british-business-bank.co.uk/ourpartner...

and then this detailed page on various things to do with it

https://www.british-business-bank.co.uk/ourpartner...

Tyre Smoke said:

No sign of HSBC there.

no mention of the BBL on the hsbc website yet...lloyds has an apply now button https://www.lloydsbank.com/business/coronavirus/bb...

Filled in the first form on natwest's site. Message says You will receive an email confirmation of this enquiry.... You will receive another email to start your application

So far all it has asked me is if the business is affected by covid 19, if I am an existing natwest customer and then for my contact details

So far all it has asked me is if the business is affected by covid 19, if I am an existing natwest customer and then for my contact details

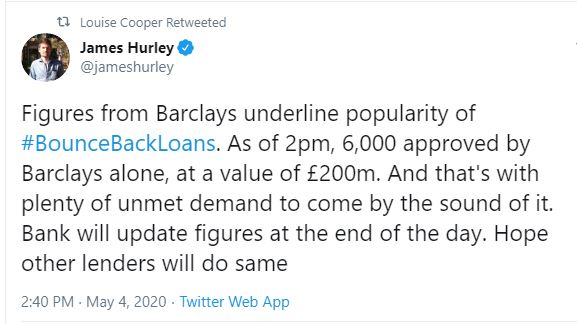

Barclays saying it done 6,000 loans / £200m by 2pm

https://twitter.com/jameshurley/status/12573040805...

https://twitter.com/jameshurley/status/12573040805...

akirk said:

well not technically - as the money will come out of their lending pot...

the government is underwriting risk and subbing the first chunk of interest payment

so the only public money will be that first interest payment and any otherwise non-retrievable loans

Barclays figure of 6,000 loans at 200 million suggests an average loan of £33,000

That suggests companies with an average turnover of 33,000 x 4 = £132k

That is lots of companies who are VAT registered and making profits - loss of their Corp tax / PAYE / income tax / NI / VAT would probably be more than a average interest payment of £833 by the government - should be beneficial to the public purse... They will also know the stats on likely failures of businesses and will have considered the cost of picking up those loans & the interest payments and seen it as less than loss of taxes / having to support unemployed staff...

The banks have a cost to put this together - IT / internal / etc.

They are then committing 100s of millions of loans at a rate much lower than would be normal with this sector - so there is some potential loss of profit there (one assumes mitigated by reduction in risk)

Assuming that the government have the same arrangement as with the CBILS then they will have priority in a liquidation / etc. - meaning that if the business has any other debt, the BB loan will take priority - this makes the government risk lower on these loans and changes the risk profile of other debt - presumably to the detriment of those lenders - so if a business has assets of £50,000 on turnover of £250,000 - and already has a debt profile of £40,000 (e.g. an overdraft, or mortgage on a small unit) - currently the debt is covered by the assets - however, that business can apply for £50,000 of BB loan - if it takes priority and they fail, their assets will pay back the BB loan - suddenly the previous £40k debt which was amply secured, is wide open and likely not to be repayed... this dramatically changes the risk profile of that current debt - which the banks would have to be adjusting for - and it is completely outside their control and completely negative for them alone. It is one of the reasons why CBILS failed for many companies - but with the BB loans, the banks are not being allowed to apply any risk / credit analysis to the business before saying yes or no...

so it is not all in favour of the banks by any means...

the tfsme is giving a wodge of the money to lenders at 0.1% and these loans are broadly outside risk weighting / cetier calculations aiui - there was a letter from the chancellor linked earlier that outlined thisthe government is underwriting risk and subbing the first chunk of interest payment

so the only public money will be that first interest payment and any otherwise non-retrievable loans

Barclays figure of 6,000 loans at 200 million suggests an average loan of £33,000

That suggests companies with an average turnover of 33,000 x 4 = £132k

That is lots of companies who are VAT registered and making profits - loss of their Corp tax / PAYE / income tax / NI / VAT would probably be more than a average interest payment of £833 by the government - should be beneficial to the public purse... They will also know the stats on likely failures of businesses and will have considered the cost of picking up those loans & the interest payments and seen it as less than loss of taxes / having to support unemployed staff...

The banks have a cost to put this together - IT / internal / etc.

They are then committing 100s of millions of loans at a rate much lower than would be normal with this sector - so there is some potential loss of profit there (one assumes mitigated by reduction in risk)

Assuming that the government have the same arrangement as with the CBILS then they will have priority in a liquidation / etc. - meaning that if the business has any other debt, the BB loan will take priority - this makes the government risk lower on these loans and changes the risk profile of other debt - presumably to the detriment of those lenders - so if a business has assets of £50,000 on turnover of £250,000 - and already has a debt profile of £40,000 (e.g. an overdraft, or mortgage on a small unit) - currently the debt is covered by the assets - however, that business can apply for £50,000 of BB loan - if it takes priority and they fail, their assets will pay back the BB loan - suddenly the previous £40k debt which was amply secured, is wide open and likely not to be repayed... this dramatically changes the risk profile of that current debt - which the banks would have to be adjusting for - and it is completely outside their control and completely negative for them alone. It is one of the reasons why CBILS failed for many companies - but with the BB loans, the banks are not being allowed to apply any risk / credit analysis to the business before saying yes or no...

so it is not all in favour of the banks by any means...

so it isn't a massive earner for the banks, but they will do ok

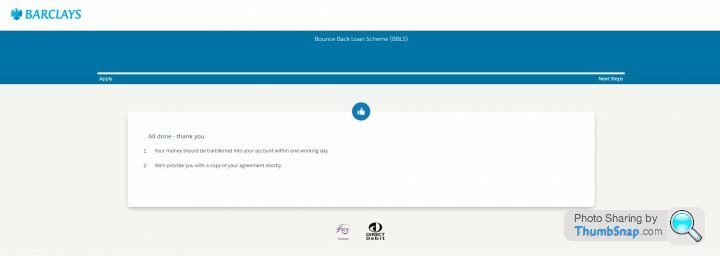

Anyone had anything from Barclays? My parents applied yesterday and had the approval message + a note saying they will send the agreement through shortly and not a peep since. It did say the money should reach them within one working day but its slightly over a working day now. Nothing either from HSBC since applying (For a separate business)

janesmith1950 said:

I bank business and personally with Barclays. Did the online application for £50k yesterday morning. At the end of the process it said the money would be in the account within a working day, but no other communications from them (not checked the account yet).

Just to help if anone else uses the Barclays online application, this is what it looked like at the end of my application...

Gassing Station | Business | Top of Page | What's New | My Stuff