How do insurance and negative eq work on a lease?

Discussion

petrolhead4 said:

Suppose I have a car on a 24 month lease, £200 a month and £1500 down.

In month 2 of the lease I have an accident and the vehicle is written off. The price of the car when new is £30,000 - however insurance have decided the market value of the car before the incident is just £24,000. The leasing company, and owner of the vehicle, are now £4300 out of pocket (£30,000 - £1500 - £200 - £24000).

How does this work? Do all leasing companies have gap insurance for their cars, or do they simply take the hit?

No you would take the hit. This is why you can get GAP insurance for lease cars. It is the lease-holders responsibility to return the car to the lease company at the end of the term or cover them financially in the event the car cannot be returned.In month 2 of the lease I have an accident and the vehicle is written off. The price of the car when new is £30,000 - however insurance have decided the market value of the car before the incident is just £24,000. The leasing company, and owner of the vehicle, are now £4300 out of pocket (£30,000 - £1500 - £200 - £24000).

How does this work? Do all leasing companies have gap insurance for their cars, or do they simply take the hit?

Also worth getting is insurance cover for the down payment - writing off a leased vehicle a couple of months into the lease when you have put down a couple of thousand quid up front just means you have lost the downpayment. Expensive.

You can insure that sum up to £2k (ALA cover this with their GAP cover now).

From my own point of view I don't know why people put down anything more than a 1 or 3 months maximum (I used to work in car leasing - it was a maxim of ours - minimum down) - it makes no real difference over the lease term, and better the cash in your bank (offsetting the mortgage or whatever) than in the lease company's coffers.

You can insure that sum up to £2k (ALA cover this with their GAP cover now).

From my own point of view I don't know why people put down anything more than a 1 or 3 months maximum (I used to work in car leasing - it was a maxim of ours - minimum down) - it makes no real difference over the lease term, and better the cash in your bank (offsetting the mortgage or whatever) than in the lease company's coffers.

Truckosaurus said:

It is also worth noting that the lease company would have purchased the car at a significant discount and not paid any VAT on the purchase, so a quite likely to turn a profit on the insurance settlement.

Not sure if they will actually do that. I wrote off a not-even five month old fully loaded E class coupe that I had on lease. The lease company wanted 24K for it which I though was ridiculously low I had made 3 + 4 payments so around £2700. This was below retail so my insurer settled it and I never needed the GAP (I transferred this over to an RTI on my motorbike as it was unused). Car was subsequently auctioned for £9200 at Copart and the claim shows as £14k on my insurance (their figure), which isn't a lot as insurance claims go.

Even if it's a lease there will be an exit charge - usually # months left x monthly charge.

However, given there is no asset to return there would have been a 'valuation' of that vehicle so if that charge doesn't cover that valuation you are liable i.e. the negative equity.

With new cars either on PCP, lease or HP, it's so important to take GAP even if its a minimum product which covers year 1 GAP to finance only. I take 3 year GAP return to invoice as I have a lot of extras, but on a lease car they generally don't have extras (many).

The T&C's will state that you need to inform the lease company ASAP, so that's the best next step, but one thing's for sure, without GAP it's going to cost you.

However, given there is no asset to return there would have been a 'valuation' of that vehicle so if that charge doesn't cover that valuation you are liable i.e. the negative equity.

With new cars either on PCP, lease or HP, it's so important to take GAP even if its a minimum product which covers year 1 GAP to finance only. I take 3 year GAP return to invoice as I have a lot of extras, but on a lease car they generally don't have extras (many).

The T&C's will state that you need to inform the lease company ASAP, so that's the best next step, but one thing's for sure, without GAP it's going to cost you.

petrolhead4 said:

How would this be done? Would the lease-holder inform the leasing company that the car has been written-off in an accident? Would the leasing company charge an early exit-fee, not including the gap, for the contract in the event of an accident because the contract can no longer be fulfilled?

You would have to. I mean, you could continue paying but they still expect a car to be returned at the end of the term.Fees specifically I’m not sure.

bassanclan said:

When my dad's car got stolen a few years ago, his insurance policy had a clause saying he got the brand new cost if the car was less than 12 months old, unfortunately his was 13 months old

Most do, so OP's question is a bit moot. I arranged insurance that has a 24-month new car benefit so that's possible too.

Beyond that, and perhaps even in addition to, best to arrange GAP.

There was quite a lengthy discussion about this on one of the lease deals threads (think maybe the current one).

The people that posted who had been in a lease write off situation had not been asked to pay anything extra. The lease company and insurance provider settled things and that was that - contract terminated.

What it did mean was that their initial payment was lost - maybe not such a big deal if you're on a 1+ or even 3+ profile, but when you get to bigger initials gap insurance to cover the initial helped at least one person recover that payment. Although I seem to recall it took months of trying to claim it and being refused before the gap provider eventually coughed up.

One person was provided a brand new car of the same spec and continued the lease contract as if nothing had happened.

The people that posted who had been in a lease write off situation had not been asked to pay anything extra. The lease company and insurance provider settled things and that was that - contract terminated.

What it did mean was that their initial payment was lost - maybe not such a big deal if you're on a 1+ or even 3+ profile, but when you get to bigger initials gap insurance to cover the initial helped at least one person recover that payment. Although I seem to recall it took months of trying to claim it and being refused before the gap provider eventually coughed up.

One person was provided a brand new car of the same spec and continued the lease contract as if nothing had happened.

PistonBroker said:

bassanclan said:

When my dad's car got stolen a few years ago, his insurance policy had a clause saying he got the brand new cost if the car was less than 12 months old, unfortunately his was 13 months old

Most do, so OP's question is a bit moot. I arranged insurance that has a 24-month new car benefit so that's possible too.

Beyond that, and perhaps even in addition to, best to arrange GAP.

One thing to bear in mind, if it's your only car, is that if you're hoping to replace it with a new one you may have a long wait. So you need to cover that gap somehow.

Yep, my 5 month old E class - LV (who were brilliant) simply dealt direct with the lease company. Beyond copying them in together on an email that was it. They paid out what the leaseco wanted for the car and that was that. No fees, nothing. Crashed the car on a Monday afternoon, car was sorted and claim paid the following Tuesday. Never ever got a bill for all the armco and motorway stuff.

Dog Star said:

Yep, my 5 month old E class - LV (who were brilliant) simply dealt direct with the lease company. Beyond copying them in together on an email that was it. They paid out what the leaseco wanted for the car and that was that. No fees, nothing. Crashed the car on a Monday afternoon, car was sorted and claim paid the following Tuesday. Never ever got a bill for all the armco and motorway stuff.

LV (most of our insurance is with them) are not unique in this but they pay quickly to get you out of the courtesy car ASAP - they want it back 4 days after the cheque is posted.Sheepshanks said:

LV (most of our insurance is with them) are not unique in this but they pay quickly to get you out of the courtesy car ASAP - they want it back 4 days after the cheque is posted.

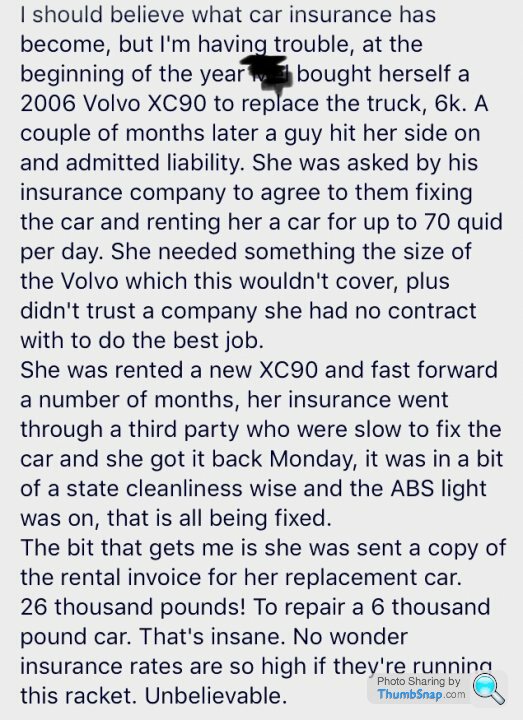

I suspect that courtesy cars cost inscos more than injuries these days - take my example, total cost £14k for writing off a 5 month old MBNow take a friends example - 2006 Volvo XC90 dented door. What with all the accident management company shenanigans (needed an identical car to take brownies to camp!) with the hire car the total claim was £26k - just for the "hire car"

They need to stamp this kind of caper out.

Here’s a screenshot of his FB post on the subject....

Dog Star said:

Now take a friends example - 2006 Volvo XC90 dented door. What with all the accident management company shenanigans (needed an identical car to take brownies to camp!) with the hire car the total claim was £26k - just for the "hire car"

They need to stamp this kind of caper out.

As best I can gather third party insurers don't pay those kind of bills, they're generally settled for far less. Accident management companies won't risk going to court as they might not get anything at all.They need to stamp this kind of caper out.

Gassing Station | Car Buying | Top of Page | What's New | My Stuff