Automotive Vloggers (Vol. 5)

Discussion

Thanfully Dan keeps keeping on; and keeps us entertained.

I sometimes even learn something; like what a ballache scraping underseal of a car is....

That tweeked Yaris did look quick on his latest video.

The previous race one in the MR2 was my fave in a long while. After witnessing a disappointing F1 race it was blimmin' refreshing watching proper grass routes racing. The written commentry always helps with the track content. Obviously Dan's fastidious winter preperation in a drafty shed paid off

(I am not sure that he wants the adulation/crticism that often comes with being a YT celeb anyway!

- not that he does not deserve success for the hardwork put in)

I sometimes even learn something; like what a ballache scraping underseal of a car is....

That tweeked Yaris did look quick on his latest video.

The previous race one in the MR2 was my fave in a long while. After witnessing a disappointing F1 race it was blimmin' refreshing watching proper grass routes racing. The written commentry always helps with the track content. Obviously Dan's fastidious winter preperation in a drafty shed paid off

(I am not sure that he wants the adulation/crticism that often comes with being a YT celeb anyway!

- not that he does not deserve success for the hardwork put in)

Hippea said:

Cracking content coming out from DannyDC2 lately, honestly think he’s one of the most underrated YouTubers. I keep thinking he’s going to take off soon, but struggles for views which confuses me.

Consistently my favourite on YT, the humour, the dog, and the content is right up my street, as I like to work on my car, so diy is always interesting. The MR2 racing is exciting too. The underseal vids were daunting, even with a ramp, crikey.

Pommy said:

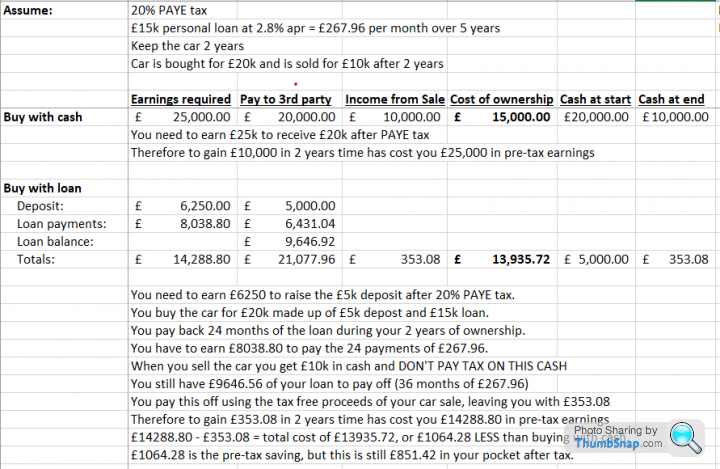

Just listening to the Seen Through Glass Under £20k podcast, can anyone enlighten me as to how Tony thinks you don't pay tax when financing a car given you need to earn money to pay the finance and you'll pay tax on that income before you pay the finance?

Wtf?!

I'm a bit late to this, and was surprised too. I'm in my 50's and buy most of my cars with cash, I just feel more secure that way. I also like a spreadsheet...Turns out Tony is right and I've been an idiot all my life Wtf?!

The key is to have a low interest loan which lasts longer than the time you keep the car, then you're quids in. It's even better if you're a higher rate tax payer. Bugger.

You don't pay tax on the car sale, and you use this to pay off the loan debt. This saves you at least 20% versus paying off the debt a month at a time after PAYE. Obviously your mileage may vary - keep the car longer or have a higher interest loan and it all changes. To be fair I keep most of my cars longer so it makes no real difference to me personally.

Here's my workings, am I wrong?

Anybody else watch Mat Armstrong, latest project is a 2019 Aston Martin Vantage, completely wrecked that he paid £54k.

https://www.youtube.com/watch?v=TCwGHz06U-k

Aston have told him that they will not sell him any parts for it, just wonder if this is a step to far as it is not like you can browse ebay for parts.

https://www.youtube.com/watch?v=TCwGHz06U-k

Aston have told him that they will not sell him any parts for it, just wonder if this is a step to far as it is not like you can browse ebay for parts.

Hippea said:

Cracking content coming out from DannyDC2 lately, honestly think he’s one of the most underrated YouTubers. I keep thinking he’s going to take off soon, but struggles for views which confuses me.

I love watch Danny's video's but its a niche content and wont appeal to the masses. Obviously more views and ultimately more money would no doubt be better, but like other posters have said I don't think thats why he does it. giveitfish said:

Pommy said:

Just listening to the Seen Through Glass Under £20k podcast, can anyone enlighten me as to how Tony thinks you don't pay tax when financing a car given you need to earn money to pay the finance and you'll pay tax on that income before you pay the finance?

Wtf?!

I'm a bit late to this, and was surprised too. I'm in my 50's and buy most of my cars with cash, I just feel more secure that way. I also like a spreadsheet...Turns out Tony is right and I've been an idiot all my life Wtf?!

The key is to have a low interest loan which lasts longer than the time you keep the car, then you're quids in. It's even better if you're a higher rate tax payer. Bugger.

You don't pay tax on the car sale, and you use this to pay off the loan debt. This saves you at least 20% versus paying off the debt a month at a time after PAYE. Obviously your mileage may vary - keep the car longer or have a higher interest loan and it all changes. To be fair I keep most of my cars longer so it makes no real difference to me personally.

Here's my workings, am I wrong?

If you have 20k in savings and buy a car, and then sell the car 2 years later, it's cost you a) 10k in depreciation and b) the lost value of not having the money invested. You get 10k back on the sale of the car so it's cost you 10k

If you have 0k in savings, borrow 20k and then sell the car after 2 years and get 10k, then it's cost you 10k PLUS the interest on the loan over that period. So it's cost you more than 10k and therefore more than if you used your savings

Youve not saved any tax as you had to pay tax on your earnings, earnings used to pay the car loan each month. And youve paid tax before receiving the earning to pay the loan.

So you havent saved any tax by getting a loan. You can only pay the loan each month from post tax income.

And the longer you hold the loan you'll keep paying accrued interest. And it's not tax deductible so it's not going to reduce your income tax either.

Pommy said:

giveitfish said:

Pommy said:

Just listening to the Seen Through Glass Under £20k podcast, can anyone enlighten me as to how Tony thinks you don't pay tax when financing a car given you need to earn money to pay the finance and you'll pay tax on that income before you pay the finance?

Wtf?!

I'm a bit late to this, and was surprised too. I'm in my 50's and buy most of my cars with cash, I just feel more secure that way. I also like a spreadsheet...Turns out Tony is right and I've been an idiot all my life Wtf?!

The key is to have a low interest loan which lasts longer than the time you keep the car, then you're quids in. It's even better if you're a higher rate tax payer. Bugger.

You don't pay tax on the car sale, and you use this to pay off the loan debt. This saves you at least 20% versus paying off the debt a month at a time after PAYE. Obviously your mileage may vary - keep the car longer or have a higher interest loan and it all changes. To be fair I keep most of my cars longer so it makes no real difference to me personally.

Here's my workings, am I wrong?

If you have 20k in savings and buy a car, and then sell the car 2 years later, it's cost you a) 10k in depreciation and b) the lost value of not having the money invested. You get 10k back on the sale of the car so it's cost you 10k

If you have 0k in savings, borrow 20k and then sell the car after 2 years and get 10k, then it's cost you 10k PLUS the interest on the loan over that period. So it's cost you more than 10k and therefore more than if you used your savings

Youve not saved any tax as you had to pay tax on your earnings, earnings used to pay the car loan each month. And youve paid tax before receiving the earning to pay the loan.

So you havent saved any tax by getting a loan. You can only pay the loan each month from post tax income.

And the longer you hold the loan you'll keep paying accrued interest. And it's not tax deductible so it's not going to reduce your income tax either.

I haven’t listened to the podcast so I don’t know the context of what was said, but I believe I know where the confusion comes from.

A few years ago, Tony made a big thing about how some of his cars belonged to him and not his company. This was at a time when they were appreciating in value and, as they were regarded as wasting assets, they weren’t subject to capital gains tax. That kind of backfired on him with the Performante.

To purchase these cars, Tony had to take money from his company. He could do this by salary or dividend, both of which would have tax implications. If he’d taken the full amount to buy the cars outright, the tax would have been significant, but if he just took the deposit and got a loan for the balance, the tax would only apply to the deposit and loan repayments.

The above situation isn’t an option for most people as they don’t have their own companies. Even if it does apply, if you want to take money out of your company, there will be tax implications at the time you take it out, Tony is just using a loan to defer that.

All the example really shows is that if you earn less money, you pay less tax. And it doesn't include national insurance, which will be relevant for most people.

Edited by AJB1971 on Monday 16th May 11:50

giveitfish said:

I'm a bit late to this, and was surprised too. I'm in my 50's and buy most of my cars with cash, I just feel more secure that way. I also like a spreadsheet...Turns out Tony is right and I've been an idiot all my life

The key is to have a low interest loan which lasts longer than the time you keep the car, then you're quids in. It's even better if you're a higher rate tax payer. Bugger.

You don't pay tax on the car sale, and you use this to pay off the loan debt. This saves you at least 20% versus paying off the debt a month at a time after PAYE. Obviously your mileage may vary - keep the car longer or have a higher interest loan and it all changes. To be fair I keep most of my cars longer so it makes no real difference to me personally.

Here's my workings, am I wrong?

I've run the numbers myself and apart from the small error (I think you used 25% for PAYE not 20%), numbers check out. To me this feels totally wrong, the key thing is with the finance you have had to earn less to have the car, hence payed less tax.The key is to have a low interest loan which lasts longer than the time you keep the car, then you're quids in. It's even better if you're a higher rate tax payer. Bugger.

You don't pay tax on the car sale, and you use this to pay off the loan debt. This saves you at least 20% versus paying off the debt a month at a time after PAYE. Obviously your mileage may vary - keep the car longer or have a higher interest loan and it all changes. To be fair I keep most of my cars longer so it makes no real difference to me personally.

Here's my workings, am I wrong?

Here is an extreme thought experiment to show why it's that way.

Finance: You buy a £100,000 car, no deposit, pay £1000 a month and sell it after a year for the exact loan amount, lets say £90,000. It cost you 12 monthly payments of £1000 that you paid tax on, £14,400 to own the car for a year.

Savings: Same rules, total cost is £120,000 in earnings to buy the thing, giving you £90,000 in your pocket at the end. So it cost you £40,000 to own the car for a year.

I know there are loads of things in the real world that complicates it, the big one in this example is, with savings there is zero earned tax on the next car, you have already paid it. The finance person will need to pay it again, and the interest etc. After enough cars the bought outright person would have paid less (no interest at any point) but now I see when viewed in isolation it works that way. Sorry this is really off topic. Should I post some YT channels to make up for it?

WarrenB said:

aundre-3000 said:

KillerHERTZ said:

jamesth32 said:

Wow shmees new video with that merc he’s a hell of a driver for a non professional driver

Yep, check out some of his 'ring laps also. But of course this is an anti Shmee thread so noone will agree

Didn't some tool on here also claim he wasn't a Petrolhead also?

I've said before i'm not a fan of his but i'll give him credit, he's living his best life right now doing what he lives for. Oh and he can peddle a car alright, he's a far far far better driver than i ever was or ever will be

wpa1975 said:

Anybody else watch Mat Armstrong, latest project is a 2019 Aston Martin Vantage, completely wrecked that he paid £54k.

https://www.youtube.com/watch?v=TCwGHz06U-k

Aston have told him that they will not sell him any parts for it, just wonder if this is a step to far as it is not like you can browse ebay for parts.

I've spoke to a number of people now who've done the "Copart rebuild" thing. It can work - and it can also go hideously wrong. Mat himself has experienced both.https://www.youtube.com/watch?v=TCwGHz06U-k

Aston have told him that they will not sell him any parts for it, just wonder if this is a step to far as it is not like you can browse ebay for parts.

From a purely business perspective, as he's going to be raffling the car off at the end that's probably the only way to make it work. A Cat Vantage is going to be worth what, 75-80 so if he paid 54 for it that doesn't leave masses of budget to fix it up and still turn a profit if you're selling it the old fashioned way.

This being said, if that is what saves the car from going to the crusher - I'm all for it.

jayemm89 said:

wpa1975 said:

Anybody else watch Mat Armstrong, latest project is a 2019 Aston Martin Vantage, completely wrecked that he paid £54k.

https://www.youtube.com/watch?v=TCwGHz06U-k

Aston have told him that they will not sell him any parts for it, just wonder if this is a step to far as it is not like you can browse ebay for parts.

I've spoke to a number of people now who've done the "Copart rebuild" thing. It can work - and it can also go hideously wrong. Mat himself has experienced both.https://www.youtube.com/watch?v=TCwGHz06U-k

Aston have told him that they will not sell him any parts for it, just wonder if this is a step to far as it is not like you can browse ebay for parts.

From a purely business perspective, as he's going to be raffling the car off at the end that's probably the only way to make it work. A Cat Vantage is going to be worth what, 75-80 so if he paid 54 for it that doesn't leave masses of budget to fix it up and still turn a profit if you're selling it the old fashioned way.

This being said, if that is what saves the car from going to the crusher - I'm all for it.

Presumably, even if the car breaks even, then channel revenue will still be generated and given his other half is involved in one of the raffle companies, it's likely it'll go down that route again. Seems a very lucrative way to 'sell' a car, particularly if the car has a profile on Youtube.

Mat's is one of my favourite channels but I wasn't too impressed with the 'wait until the next episode' ending of the Aston vid. Let's not turn it into Eastenders please!

ro250 said:

jayemm89 said:

wpa1975 said:

Anybody else watch Mat Armstrong, latest project is a 2019 Aston Martin Vantage, completely wrecked that he paid £54k.

https://www.youtube.com/watch?v=TCwGHz06U-k

Aston have told him that they will not sell him any parts for it, just wonder if this is a step to far as it is not like you can browse ebay for parts.

I've spoke to a number of people now who've done the "Copart rebuild" thing. It can work - and it can also go hideously wrong. Mat himself has experienced both.https://www.youtube.com/watch?v=TCwGHz06U-k

Aston have told him that they will not sell him any parts for it, just wonder if this is a step to far as it is not like you can browse ebay for parts.

From a purely business perspective, as he's going to be raffling the car off at the end that's probably the only way to make it work. A Cat Vantage is going to be worth what, 75-80 so if he paid 54 for it that doesn't leave masses of budget to fix it up and still turn a profit if you're selling it the old fashioned way.

This being said, if that is what saves the car from going to the crusher - I'm all for it.

Presumably, even if the car breaks even, then channel revenue will still be generated and given his other half is involved in one of the raffle companies, it's likely it'll go down that route again. Seems a very lucrative way to 'sell' a car, particularly if the car has a profile on Youtube.

Mat's is one of my favourite channels but I wasn't too impressed with the 'wait until the next episode' ending of the Aston vid. Let's not turn it into Eastenders please!

wpa1975 said:

Anybody else watch Mat Armstrong, latest project is a 2019 Aston Martin Vantage, completely wrecked that he paid £54k.

https://www.youtube.com/watch?v=TCwGHz06U-k

Aston have told him that they will not sell him any parts for it, just wonder if this is a step to far as it is not like you can browse ebay for parts.

Yes just started to get into these. That Range Rover! Particularly when he took the dash out with about a million bolts/screws, and still had 7 left over at the end when he put it back in https://www.youtube.com/watch?v=TCwGHz06U-k

Aston have told him that they will not sell him any parts for it, just wonder if this is a step to far as it is not like you can browse ebay for parts.

Not sure I would want to take a risk on any of those cars from a raffle even if it did only cost me a tenner or whatever.

Not sure I would want to take a risk on any of those cars from a raffle even if it did only cost me a tenner or whatever.The AM does have a lot of Merc bits though so may be able to get most of the bits he needs through other channels and not Aston.

littleendbearing said:

I've run the numbers myself and apart from the small error (I think you used 25% for PAYE not 20%), numbers check out. To me this feels totally wrong, the key thing is with the finance you have had to earn less to have the car, hence payed less tax.

Here is an extreme thought experiment to show why it's that way.

Finance: You buy a £100,000 car, no deposit, pay £1000 a month and sell it after a year for the exact loan amount, lets say £90,000. It cost you 12 monthly payments of £1000 that you paid tax on, £14,400 to own the car for a year.

Savings: Same rules, total cost is £120,000 in earnings to buy the thing, giving you £90,000 in your pocket at the end. So it cost you £40,000 to own the car for a year.

I know there are loads of things in the real world that complicates it, the big one in this example is, with savings there is zero earned tax on the next car, you have already paid it. The finance person will need to pay it again, and the interest etc. After enough cars the bought outright person would have paid less (no interest at any point) but now I see when viewed in isolation it works that way. Sorry this is really off topic. Should I post some YT channels to make up for it?

Yes, that's it exactly Here is an extreme thought experiment to show why it's that way.

Finance: You buy a £100,000 car, no deposit, pay £1000 a month and sell it after a year for the exact loan amount, lets say £90,000. It cost you 12 monthly payments of £1000 that you paid tax on, £14,400 to own the car for a year.

Savings: Same rules, total cost is £120,000 in earnings to buy the thing, giving you £90,000 in your pocket at the end. So it cost you £40,000 to own the car for a year.

I know there are loads of things in the real world that complicates it, the big one in this example is, with savings there is zero earned tax on the next car, you have already paid it. The finance person will need to pay it again, and the interest etc. After enough cars the bought outright person would have paid less (no interest at any point) but now I see when viewed in isolation it works that way. Sorry this is really off topic. Should I post some YT channels to make up for it?

I think the 20% PAYE in my sheet is correct - if you earn £25k you pay 20% tax. 20% of £25k is £5k, so you only take home £20k after tax.

I won't post any more as it's not what this thread is about, but I found it interesting to work through. Looking back over my car history it adds up to the square root of sod all, but it does show how I could have funded braver purchases with the same earnings.

Gassing Station | TV, Film, Video Streaming & Radio | Top of Page | What's New | My Stuff