How far will house prices fall [volume 4]

Discussion

Lucas Ayde said:

Depends on how much the government interfere to try to keep prices high.

There was something like a 20% dip in prices around 2007 that looked like developing into something bigger but all the measures like near zero rates, nationalisation for the most reckless lenders (instead of letting them go bust) and unlimited liquidity for the banking system plus daft policies like shared ownership and 'Help to Buy' have more than reversed that.

There are still all manner of stupid moves that they can pull to try to keep the sinking ship afloat for a bit longer. However, if May wins the coming election comfortably she might just decide to have the bust now and capitalise on things recovering in time for the next election five years down the line ... she can blame Brexit for the inevitable collapse of the housing market.

I has thought the same. Let it go to sThere was something like a 20% dip in prices around 2007 that looked like developing into something bigger but all the measures like near zero rates, nationalisation for the most reckless lenders (instead of letting them go bust) and unlimited liquidity for the banking system plus daft policies like shared ownership and 'Help to Buy' have more than reversed that.

There are still all manner of stupid moves that they can pull to try to keep the sinking ship afloat for a bit longer. However, if May wins the coming election comfortably she might just decide to have the bust now and capitalise on things recovering in time for the next election five years down the line ... she can blame Brexit for the inevitable collapse of the housing market.

t for a year or two and then bask in the miraculous recovery. Or just be remembered as the politician that was brave enough to turn the music off for the longer term good of society.

t for a year or two and then bask in the miraculous recovery. Or just be remembered as the politician that was brave enough to turn the music off for the longer term good of society.Lucas Ayde said:

Depends on how much the government interfere to try to keep prices high.

There was something like a 20% dip in prices around 2007 that looked like developing into something bigger but all the measures like near zero rates, nationalisation for the most reckless lenders (instead of letting them go bust) and unlimited liquidity for the banking system plus daft policies like shared ownership and 'Help to Buy' have more than reversed that.

There are still all manner of stupid moves that they can pull to try to keep the sinking ship afloat for a bit longer. However, if May wins the coming election comfortably she might just decide to have the bust now and capitalise on things recovering in time for the next election five years down the line ... she can blame Brexit for the inevitable collapse of the housing market.

Stupid would be pulling the rung from under our consumer (and debt fuelled) economy. Whilst excessive leverage is bad, we need a gradual settling not a frikkin fire sale of assets fuelled by monetary tightening. There was something like a 20% dip in prices around 2007 that looked like developing into something bigger but all the measures like near zero rates, nationalisation for the most reckless lenders (instead of letting them go bust) and unlimited liquidity for the banking system plus daft policies like shared ownership and 'Help to Buy' have more than reversed that.

There are still all manner of stupid moves that they can pull to try to keep the sinking ship afloat for a bit longer. However, if May wins the coming election comfortably she might just decide to have the bust now and capitalise on things recovering in time for the next election five years down the line ... she can blame Brexit for the inevitable collapse of the housing market.

Interest rate reductions and TARP etc, were not a response to house prices coming off 20% but a 15% runoff in the MSCI600 post Lehman collapse - it was a global issue. If Stanley's and Goldman had gone in the week after Lehman, you wouldn't be worrying about house prices more NATO 5.56mm and Duracells.

A slowing of house price inflation is desirable, but it's always about where you buy not where you sell. If you can off plan or from a developer at a whopper of a discount why not (if you have a view on the floor). If you can do it without leverage even better. As Booby Axe once said "what's the point of having f

k you money if you can't say fk you". Sticking it into a developer can't be that bad?hyphen said:

Millionaire tells millennials: if you want a house, stop buying avocado toast https://twitter.com/60Mins/status/8640653465163776...

This sentiment comes up a lot, and I think they've got it the wrong way round. I'm a year or two older than the start of the "millennial" generation, and have a fair few friends slap in the middle of it. Avocado toast is nowhere near their biggest problem. The biggest problem people my age have with home ownership is they want a fully refurbished Victorian property or brand new flat, two bathrooms, near a station in London or another popular city of choice - often because they work in some particular sector that only happens to exist in one tiny part of said city. On top of that, while they're waiting they want to rent something of the same standard, which takes a far bigger chunk out of savings potential than the occasional posh sandwich.The people I know who bought a house in their 20s or very early 30s without any input from Bank of Mum and Dad have the same thing in common: they bought a tired old '70s semi or similar somewhere unfashionable, knowing it would need work and they'd have to live with just one bathroom and stuff breaking down every few months. They still had new phones, nice cars and the occasional brunch, but were willing to lower their expectations when it came to property. Interestingly, after a few years most are now in the position that they could afford that lovingly refurbished Victorian terrace etc. but aren't interested because it represents extremely poor value compared to what they've already got.

Personally, I'd tell millennials that if you want to buy a house, don't pick a career that only exists in only one bit of one city in the entire country (while not giving you any transferable skills) and accept that your first property is going to be something deeply unfashionable in a boring no-mark bit of town. You can always move back to the city once you've spent a few years paying down the mortgage and painting over the magnolia until you've got a sizeable deposit.

Timberwolf said:

This sentiment comes up a lot, and I think they've got it the wrong way round. I'm a year or two older than the start of the "millennial" generation, and have a fair few friends slap in the middle of it. Avocado toast is nowhere near their biggest problem. The biggest problem people my age have with home ownership is they want a fully refurbished Victorian property or brand new flat, two bathrooms, near a station in London or another popular city of choice - often because they work in some particular sector that only happens to exist in one tiny part of said city. On top of that, while they're waiting they want to rent something of the same standard, which takes a far bigger chunk out of savings potential than the occasional posh sandwich.

The people I know who bought a house in their 20s or very early 30s without any input from Bank of Mum and Dad have the same thing in common: they bought a tired old '70s semi or similar somewhere unfashionable, knowing it would need work and they'd have to live with just one bathroom and stuff breaking down every few months. They still had new phones, nice cars and the occasional brunch, but were willing to lower their expectations when it came to property. Interestingly, after a few years most are now in the position that they could afford that lovingly refurbished Victorian terrace etc. but aren't interested because it represents extremely poor value compared to what they've already got.

Personally, I'd tell millennials that if you want to buy a house, don't pick a career that only exists in only one bit of one city in the entire country (while not giving you any transferable skills) and accept that your first property is going to be something deeply unfashionable in a boring no-mark bit of town. You can always move back to the city once you've spent a few years paying down the mortgage and painting over the magnolia until you've got a sizeable deposit.

Sorry to say but your view is 15 years out of date.The people I know who bought a house in their 20s or very early 30s without any input from Bank of Mum and Dad have the same thing in common: they bought a tired old '70s semi or similar somewhere unfashionable, knowing it would need work and they'd have to live with just one bathroom and stuff breaking down every few months. They still had new phones, nice cars and the occasional brunch, but were willing to lower their expectations when it came to property. Interestingly, after a few years most are now in the position that they could afford that lovingly refurbished Victorian terrace etc. but aren't interested because it represents extremely poor value compared to what they've already got.

Personally, I'd tell millennials that if you want to buy a house, don't pick a career that only exists in only one bit of one city in the entire country (while not giving you any transferable skills) and accept that your first property is going to be something deeply unfashionable in a boring no-mark bit of town. You can always move back to the city once you've spent a few years paying down the mortgage and painting over the magnolia until you've got a sizeable deposit.

Like others have said - properties in other parts of the country are equally inaffordable in reference to local salaries.

The lower rung of the ladder no longer exists. The first time buyer house no longer exists. First time buyers will have to take on the kind of mortgage the previous generation have never experienced.

The first time house now costs more than the third time house / final house. First time buyers come with no equity handed to them for free. The first time buyers are the ones using mortgage debt to pay the previous generation so that they may crystalize those paper gains. The previous generation get to live in houses they could not afford without those paper equity gains being paid for by the next generation via mortgage debt.

I don't think it is - at best it's 5 years out of date because I'm talking about people who bought in 2012/2013/2014 with higher interest rates and stricter deposit requirements than today. Where I live there are still a few properties that could reasonably be bought by a couple on decent-but-not-spectacular incomes who've been saving a while - the debt is a big number but interest rates are low and you can stretch to 30 years if necessary. Problem is it's a boring commuter town and those properties are '60s flats, maisonettes and small houses.

The "first time house" does exist, but it depends on where you live so, for example, there are 550 houses in Stoke on Trent (my hometown in the Midlands) between 50k-100k yet only 17 in Maidstone in Kent (where I currently work) so geography plays a huge part.

Yes there is a population difference (Stoke has 250k people and Maidstone 110k) but that isn't reflected in Stoke having 32 times more houses available for low earners.

Yes there is a population difference (Stoke has 250k people and Maidstone 110k) but that isn't reflected in Stoke having 32 times more houses available for low earners.

stongle said:

Stupid would be pulling the rung from under our consumer (and debt fuelled) economy. Whilst excessive leverage is bad, we need a gradual settling not a frikkin fire sale of assets fuelled by monetary tightening.

Interest rate reductions and TARP etc, were not a response to house prices coming off 20% but a 15% runoff in the MSCI600 post Lehman collapse - it was a global issue. If Stanley's and Goldman had gone in the week after Lehman, you wouldn't be worrying about house prices more NATO 5.56mm and Duracells.

A slowing of house price inflation is desirable, but it's always about where you buy not where you sell. If you can off plan or from a developer at a whopper of a discount why not (if you have a view on the floor). If you can do it without leverage even better. As Booby Axe once said "what's the point of having fk you money if you can't say fk you". Sticking it into a developer can't be that bad?

The real issue is that none of the big problems of the "Too big to fail" enterprises from 2007 have been resolved. The TBTFs are even bigger, the public and private sector debts are even bigger (esp public sector), the economy hasn't grown appreciably despite the injection of massive amounts of debt-fuelled liquidity and there's no way to slow things down without going into reverse.Interest rate reductions and TARP etc, were not a response to house prices coming off 20% but a 15% runoff in the MSCI600 post Lehman collapse - it was a global issue. If Stanley's and Goldman had gone in the week after Lehman, you wouldn't be worrying about house prices more NATO 5.56mm and Duracells.

A slowing of house price inflation is desirable, but it's always about where you buy not where you sell. If you can off plan or from a developer at a whopper of a discount why not (if you have a view on the floor). If you can do it without leverage even better. As Booby Axe once said "what's the point of having f

k you money if you can't say fk you". Sticking it into a developer can't be that bad?The number one thing that could be done by governments is to break up the big banks into entities small enough to fail. Instead, the talk is of loosening or removing what capital requirements there are on these behemoths, to allow them to become even bigger and more leveraged. Supposedly, allowing them to create even more credit from their asset base is going to fix the problems that the credit bubble almost bursting in 2007 gave us. Madness.

Tory Manifesto bit on housing

Tory manifesto said:

...and will shortly ban letting agent fees

A Conservative government will reform and modernise the home-buying process so it is more efficient and less costly. We will crack down on unfair practices in leasehold, such as escalating ground rents. We will also improve protections for those who rent, including by looking at how we increase security for good tenants and encouraging landlords to offer longer tenancies as standard.

We will meet our 2015 commitment to deliver a million homes by the end of 2020 and we will deliver half a million more by the end of 2022. We will deliver the reforms proposed in our Housing White Paper to free up more land for new homes in the right places, speed up build-out by encouraging modern methods of construction and give councils powers to intervene where developers do not act on their planning permissions; and we will diversify who builds homes in this country.

More homes will not mean poor quality homes. For too long, careless developers, high land costs and poor planning have conspired to produce housing developments that do not enhance the lives of those living there. We have not provided the infrastructure, parks, quality of space and design that turns housing into community and makes communities prosperous and sustainable. The result is felt by many ordinary, working families. Too often, those renting or buying a home on a modest income have to tolerate

substandard developments -some only a few years old -and are denied a decent place in which to live, where they can put down roots and raise children. For a country boasting the nest architects and planners in the world, this is unacceptable.

We will build better houses, to match the quality of those we have inherited from previous generations. That means supporting high-quality, high-density housing like mansion blocks, mews houses and terraced streets. It means maintaining the existing strong protections on designated land like the Green Belt, National Parks and Areas of Outstanding Natural Beauty. It means not just concentrating development in the south-east but rebalancing housing growth across the country, in line with our modern industrial strategy. It means government building 160,000 houses on its own land. It means supporting specialist housing where it is needed, like multigenerational homes and housing for older people, including by helping housing associations increase their specialist housing stock.

We will never achieve the numbers of new houses we require without the active participation of social and municipal housing providers. This must not be done at the expense of high standards, however: councils have been amongst the worst offenders in failing to build sustainable, integrated communities. In some instances, they have built for political gain rather than for social purpose.

So we will help councils to build, but only those councils who will build high-quality, sustainable and integrated communities. We will enter into new Council Housing Deals with ambitious, pro-development, local authorities to help them build more social housing. We will work with them to improve their capability and capacity to develop more good homes, as well as providing them with significant low-cost capital funding. In doing so, we will build new fixed-term social houses, which will be sold privately after ten to fifteen years with an automatic Right to Buy for tenants, the proceeds of which will be recycled into further homes. We will reform Compulsory Purchase Orders to make them easier and less expensive for councils to use and to make it easier to determine the true market value of sites.

We will also give greater exibility to housing associations to increase their housing stock, building on their considerable track record in recent years. And we will work with private and public sector house builders to capture the increase in land value created when they build to reinvest in local infrastructure, essential services and further housing, making it both easier and more certain that public sector landowners, and communities themselves, benefit from the increase in land value from urban regeneration and development. And we will continue our £2.5 billion flood defence programme that will put in place protection for 300,000 existing homes by 2021.

These ambitious policies will mean more and better homes, welcomed by existing communities because they add, rather than subtract, from what is already there. This is the sustainable development we need to see happen in every village, town and city

across our country. These policies will take time, and meanwhile we will continue to support those struggling to buy or rent a home, including those living in a home owned by a housing association.

A Conservative government will reform and modernise the home-buying process so it is more efficient and less costly. We will crack down on unfair practices in leasehold, such as escalating ground rents. We will also improve protections for those who rent, including by looking at how we increase security for good tenants and encouraging landlords to offer longer tenancies as standard.

We will meet our 2015 commitment to deliver a million homes by the end of 2020 and we will deliver half a million more by the end of 2022. We will deliver the reforms proposed in our Housing White Paper to free up more land for new homes in the right places, speed up build-out by encouraging modern methods of construction and give councils powers to intervene where developers do not act on their planning permissions; and we will diversify who builds homes in this country.

More homes will not mean poor quality homes. For too long, careless developers, high land costs and poor planning have conspired to produce housing developments that do not enhance the lives of those living there. We have not provided the infrastructure, parks, quality of space and design that turns housing into community and makes communities prosperous and sustainable. The result is felt by many ordinary, working families. Too often, those renting or buying a home on a modest income have to tolerate

substandard developments -some only a few years old -and are denied a decent place in which to live, where they can put down roots and raise children. For a country boasting the nest architects and planners in the world, this is unacceptable.

We will build better houses, to match the quality of those we have inherited from previous generations. That means supporting high-quality, high-density housing like mansion blocks, mews houses and terraced streets. It means maintaining the existing strong protections on designated land like the Green Belt, National Parks and Areas of Outstanding Natural Beauty. It means not just concentrating development in the south-east but rebalancing housing growth across the country, in line with our modern industrial strategy. It means government building 160,000 houses on its own land. It means supporting specialist housing where it is needed, like multigenerational homes and housing for older people, including by helping housing associations increase their specialist housing stock.

We will never achieve the numbers of new houses we require without the active participation of social and municipal housing providers. This must not be done at the expense of high standards, however: councils have been amongst the worst offenders in failing to build sustainable, integrated communities. In some instances, they have built for political gain rather than for social purpose.

So we will help councils to build, but only those councils who will build high-quality, sustainable and integrated communities. We will enter into new Council Housing Deals with ambitious, pro-development, local authorities to help them build more social housing. We will work with them to improve their capability and capacity to develop more good homes, as well as providing them with significant low-cost capital funding. In doing so, we will build new fixed-term social houses, which will be sold privately after ten to fifteen years with an automatic Right to Buy for tenants, the proceeds of which will be recycled into further homes. We will reform Compulsory Purchase Orders to make them easier and less expensive for councils to use and to make it easier to determine the true market value of sites.

We will also give greater exibility to housing associations to increase their housing stock, building on their considerable track record in recent years. And we will work with private and public sector house builders to capture the increase in land value created when they build to reinvest in local infrastructure, essential services and further housing, making it both easier and more certain that public sector landowners, and communities themselves, benefit from the increase in land value from urban regeneration and development. And we will continue our £2.5 billion flood defence programme that will put in place protection for 300,000 existing homes by 2021.

These ambitious policies will mean more and better homes, welcomed by existing communities because they add, rather than subtract, from what is already there. This is the sustainable development we need to see happen in every village, town and city

across our country. These policies will take time, and meanwhile we will continue to support those struggling to buy or rent a home, including those living in a home owned by a housing association.

Edited by hyphen on Thursday 18th May 14:45

Lucas Ayde said:

The real issue is that none of the big problems of the "Too big to fail" enterprises from 2007 have been resolved. The TBTFs are even bigger, the public and private sector debts are even bigger (esp public sector), the economy hasn't grown appreciably despite the injection of massive amounts of debt-fuelled liquidity and there's no way to slow things down without going into reverse.

The number one thing that could be done by governments is to break up the big banks into entities small enough to fail. Instead, the talk is of loosening or removing what capital requirements there are on these behemoths, to allow them to become even bigger and more leveraged. Supposedly, allowing them to create even more credit from their asset base is going to fix the problems that the credit bubble almost bursting in 2007 gave us. Madness.

The Capital point is wrong, only the EU is proposing lowering the Capital floor. UK and US banks are pushing the other way. And certainly we are breaking up the banks unlike the EUs nonsense holding co rules at resolution. Balance sheet or credit creation is becoming exceptionally difficult (expensive) as the regulators are focusing on the building blocks. Creating smaller, less visible banks (or institutions) could increase shadow banking risks.The number one thing that could be done by governments is to break up the big banks into entities small enough to fail. Instead, the talk is of loosening or removing what capital requirements there are on these behemoths, to allow them to become even bigger and more leveraged. Supposedly, allowing them to create even more credit from their asset base is going to fix the problems that the credit bubble almost bursting in 2007 gave us. Madness.

We've not seen the balance sheets decrease yet, as the regs are only just being filtered in. I don't think Leverage Ratio is fully binding yet (only reporting) and LLPs are a dog fight right now (again UK plc is ahead in introducing IFRS9).

It's probable that the full post 2007 regulatory fixes won't be in place till 2022 onwards (again EU can kicking creating regulatory arbitrage).

Until we get off the crack of Monetary Policy to fuel spending credit supply is abundant. I hope To see more fiscal spend to balance the economy and work / housing distribution. I think a lot of price softening is sentiment driven and lack of outside cash. It's a house price crash just a cooling. Over priced tat will come off more than something desirable (might be some position bias have a house in London).

Agggresive intervention will cause a collapse in the consumer economy and then we are proper f

ked.London and the surrounding area seems to still be very strong at the lower end of the market. In my opinion it's because there are still a tremendous number of young professional couples out there with household incomes in the £50-100k range. With the return of 95% LTV mortgages they've actually got a surprising amount of buying power, especially if they're willing to go for a 30+ year loan with the view of overpaying early and often.

I think the London market is flattening, by that i mean say sub 600k properties are strong, but as you climb to more expensive levels property gets softer and softer.

I think this is in part due the high outright price levels meaning incremental increases are that much more in notional terms, think selling your 750k flat to buy a 1.2m small house, or selling your 1.2m small house to buy the larger family house for £1.6m. Each incremental change represents huge sums and i think people are genuinely struggling to move up.

The other issue at the larger / more expensive property end of the market is the cost to sell and buy, its huge, to move up to that family home can cost you £100k just in fees and stamp duty.

Thus, i think theres an opportunity if you are cash rich to squeeze the price on that next move up house.

I think this is in part due the high outright price levels meaning incremental increases are that much more in notional terms, think selling your 750k flat to buy a 1.2m small house, or selling your 1.2m small house to buy the larger family house for £1.6m. Each incremental change represents huge sums and i think people are genuinely struggling to move up.

The other issue at the larger / more expensive property end of the market is the cost to sell and buy, its huge, to move up to that family home can cost you £100k just in fees and stamp duty.

Thus, i think theres an opportunity if you are cash rich to squeeze the price on that next move up house.

IanH755 said:

The "first time house" does exist, but it depends on where you live so, for example, there are 550 houses in Stoke on Trent (my hometown in the Midlands) between 50k-100k yet only 17 in Maidstone in Kent (where I currently work) so geography plays a huge part.

Yes there is a population difference (Stoke has 250k people and Maidstone 110k) but that isn't reflected in Stoke having 32 times more houses available for low earners.

I just plugged that into Rightmove got 1 hit for Maidstone which looked like some kind of 1 bed house shared ownership yet to be built affair.Yes there is a population difference (Stoke has 250k people and Maidstone 110k) but that isn't reflected in Stoke having 32 times more houses available for low earners.

Had to go to a 15 miles radius to get 7 hits and that included a boat house and a caravan / static home....

menousername said:

I just plugged that into Rightmove got 1 hit for Maidstone which looked like some kind of 1 bed house shared ownership yet to be built affair.

Had to go to a 15 miles radius to get 7 hits and that included a boat house and a caravan / static home....

I was going to contradict and say 11, but you are of course correct. The nonsense over 60 prices and shared ownership trickery really should be displayed at FMV.Had to go to a 15 miles radius to get 7 hits and that included a boat house and a caravan / static home....

loafer123 said:

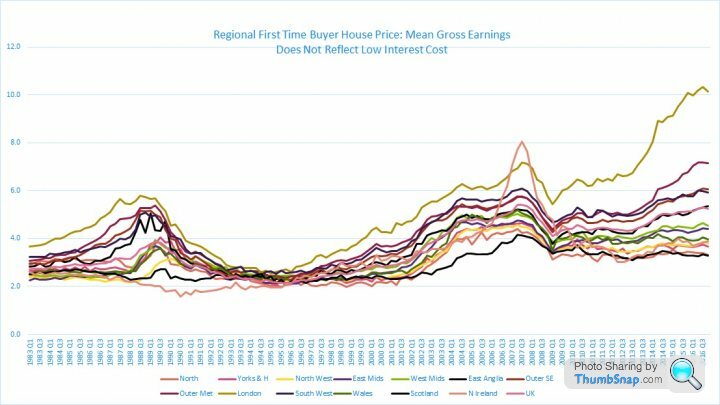

Clearly, this is only half the story, as low interest rates means the payments FTB's are making are alot lower than historically.

I found it surprising that, for all the booms and busts we've had over the years, monthly mortgage payments for an average house have remained remarkably constant at about a third of average household take-home pay. There have been big jumps caused by the change from single-income to dual-income houses, house prices have leapt all over the place in response to inflation and interest rate changes, but somewhere around 33% of household take-home has remained remarkably constant since the late '60s, and I only mention that date because one of my data sets didn't go back any further. There are aberrations - for a while after the '90s slump it hovered at around 25%, and the liar loans boom of the late 2000s pushed it up to 40% or so - but it's actually remarkably constant.As a shorter range example, I bought my first house in 2013 (on a single income, which was all kinds of pain in today's couple-oriented market) and despite all the ridiculous paper gains since then for London and the South East, someone buying it today with exactly the same deposit would end up with almost exactly the same mortgage payment, once taking into account the relatively paltry wage inflation over the last four years.

My view is that the main thing causing the market to slow down, especially in the expensive parts of London, is the deposit and transaction costs have reached their saturation point. While borrowing large sums of money has become easy, saving large sums of it hasn't. If anything, it's harder than it used to be thanks to below-inflation returns in many places. Hence FTBs in popular, in-demand locations needing to be very wealthy... and for the overheated parts of London and the top end of the market, there's just not a big enough supply of rich people. As said before, the cheaper and lower end parts of the market are still doing okay for now, because while the supply of rich people is small even in the capital, the supply of comfortably well off people is enormous.

Slackening LTV requirements from lenders can go some way to helping with this deposit problem (I can still remember brokers telling you not to bother unless you had 20% burning a hole in your pocket) but eventually you hit the problem that stamp duty and legal fees are bigger than the deposit fund - second-steppers particularly being afflicted by this, as they face not only a massive gap to the next property but a huge chunk of the equity and savings they need for that move going straight to the transaction costs. Hence the returning popularity of the sideways move from a London flat to a big house somewhere in the commuter belt and, of course, the gradual march towards an end state where every last semi in Zone 3 has a massive box on the roof.

Edited by Timberwolf on Friday 19th May 19:28

. And, of course, entirely accurate.

. And, of course, entirely accurate.Timberwolf said:

Eventually you hit the problem that stamp duty and legal fees are bigger than the deposit fund - second-steppers particularly being afflicted by this, as they face not only a massive gap to the next property but a huge chunk of the equity and savings they need for that move going straight to the transaction costs.

I'm in exactly this situation. Bought first house 2.5 years ago. A combination of some value-adding refurbishment, pay-down on the mortgage, saving, and pay rises means my 'war-chest' if I were to go house-shopping now would be up to current value of house + £250k.

Great, you think.

Until you realise that

a) £250k extra really doesn't move me into anything that I'd be especially excited to buy. Certainly nothing I know I'd stay in for the long term.

b) The whole moving and transaction process would cost me at least £30k

So I sit tight in the current place, keep paying down the mortgage and adding to the savings account. Given the transaction costs, I think I'll only move if either

a) Life forces me to. Maybe I need to move for a job, or for someone special

b) I find myself in the lucky financial position to significantly upgrade, with the expectation that I'd stay in the new place a long while.

Gassing Station | News, Politics & Economics | Top of Page | What's New | My Stuff