How far will house prices fall [volume 4]

Discussion

menousername said:

But what happened to the local average salary in that time?

And what are employment prospects like?

What has local average salary got to do with it? Surely all that matters is your salary and the price of the house you want to buy.And what are employment prospects like?

Take the example of the £500k bog standard semi in Didsdbury.

Somebody working in the city centre and wanting to live in Didsbury might not be able to afford £500k for a semi (I certainly couldn't), so what should they they do - throw their hands up and complain that house prices aren't affordable - or do they simply cast their net a bit wider?

£500k might only get you a bog standard semi in Didsbury - but in Droylsden (*other areas beginning with "D" are available) you'll pay around 1/3rd of that for a similar property.

I've picked one as I'm tied up at the mo

http://www.rightmove.co.uk/property-for-sale/prope...

It needs gutting completely

Looking at landregistry.data.go.uk

Apart from a few spikes most recent - almost all are identical on that road/a estate build (2009+) sold for 150-180k on that road.

I know recently from personal experience as I've bought twice in the south Manchester area in the last 10years and I'm always glancing at prices. A recently arranged viewing was turned into a open house/closed offers on the day for once house that we were interested in last month. That particular house went for 20k over the asking price.

http://www.rightmove.co.uk/property-for-sale/prope...

It needs gutting completely

Looking at landregistry.data.go.uk

Apart from a few spikes most recent - almost all are identical on that road/a estate build (2009+) sold for 150-180k on that road.

I know recently from personal experience as I've bought twice in the south Manchester area in the last 10years and I'm always glancing at prices. A recently arranged viewing was turned into a open house/closed offers on the day for once house that we were interested in last month. That particular house went for 20k over the asking price.

anonymous said:

[redacted]

The point is that just because at this precise moment in time interest rates are at a historical low, that does not make housing ¨affordable¨.Someone might be able to ¨afford¨ the house at the current historically low interest rates - that is to say, make the monthly mortgage payments - but will the buyer be able to meet repayments when rates rise to something closer to the long term norm?

Or do you simply never look beyond the current monthly payment?

Sa Calobra said:

Looking at the sold prices for two similar houses on that street (numbers 11 and 13). They appear to have jumped around 2.5x between 2002 and 2016.Whilst that is an above inflation rise over the same 14 year period - it's doesn't support your assertion of a tripling of prices over 5 years.

anonymous said:

[redacted]

If you are wanting to de risk then 10 year fixed rate mortgages are available for low 2%'s. I fail to see the problem.

If you elect to go variable rate to save v fixed rate then you have to be prepared for upward interest rate risk if not cake and eat it springs to mind.

Lucas Ayde said:

The point is that just because at this precise moment in time interest rates are at a historical low, that does not make housing ¨affordable¨.

Someone might be able to ¨afford¨ the house at the current historically low interest rates - that is to say, make the monthly mortgage payments - but will the buyer be able to meet repayments when rates rise to something closer to the long term norm?

Or do you simply never look beyond the current monthly payment?

i think that the problem is that we have had low interest rates for so long that a lot of people don't know anything else. £500k is now seen as £850 a month on an interest only mortgage. That is very affordable if you had the income to secure the mortgage in the first place, and even if you took a significant pay cut afterwards.Someone might be able to ¨afford¨ the house at the current historically low interest rates - that is to say, make the monthly mortgage payments - but will the buyer be able to meet repayments when rates rise to something closer to the long term norm?

Or do you simply never look beyond the current monthly payment?

That is why you can't buy much of a house for £500k any more. Of course things should change, but will they? A few of the reasons why they might not:

1. The 'cat is out of the bag' with respect to prices, people are used to talking about these huge sums of money for houses, even if they are many many times what they earn and increasing more quickly.

2. As illusatrated by a lot of the comments on here, a lot of people think high house prices are a good thing. A lot of this is (rightfully) out of fear, we have got ourselves into this situation, how can we reduce prices without causing wider economic problems?

3. How long will it be before interest rates rise to anything like their long term average again? BoE are starting to talk about raising them, but I can't see how the base rate can go much higher than 1.5 or 2% for years to come. I am still seeing 10 year fixed rate mortgages on offer for 2.49% from mainstream lenders, so they seem fairly confident of this too.

Edited by kingston12 on Tuesday 11th July 10:01

Sa Calobra said:

I've picked one as I'm tied up at the mo

http://www.rightmove.co.uk/property-for-sale/prope...

It needs gutting completely

Looking at landregistry.data.go.uk

Apart from a few spikes most recent - almost all are identical on that road/a estate build (2009+) sold for 150-180k on that road.

I know recently from personal experience as I've bought twice in the south Manchester area in the last 10years and I'm always glancing at prices. A recently arranged viewing was turned into a open house/closed offers on the day for once house that we were interested in last month. That particular house went for 20k over the asking price.

You've dug yourself into a hole. Need to stop digging http://www.rightmove.co.uk/property-for-sale/prope...

It needs gutting completely

Looking at landregistry.data.go.uk

Apart from a few spikes most recent - almost all are identical on that road/a estate build (2009+) sold for 150-180k on that road.

I know recently from personal experience as I've bought twice in the south Manchester area in the last 10years and I'm always glancing at prices. A recently arranged viewing was turned into a open house/closed offers on the day for once house that we were interested in last month. That particular house went for 20k over the asking price.

Moonhawk said:

Looking at the sold prices for two similar houses on that street (numbers 11 and 13). They appear to have jumped around 2.5x between 2002 and 2016.

Whilst that is an above inflation rise over the same 14 year period - it's doesn't support your assertion of a tripling of prices over 5 years.

Scroll down there are alot more house results on that street on that pageWhilst that is an above inflation rise over the same 14 year period - it's doesn't support your assertion of a tripling of prices over 5 years.

Sa Calobra said:

Moonhawk said:

Looking at the sold prices for two similar houses on that street (numbers 11 and 13). They appear to have jumped around 2.5x between 2002 and 2016.

Whilst that is an above inflation rise over the same 14 year period - it's doesn't support your assertion of a tripling of prices over 5 years.

Scroll down there are alot more house results on that street on that pageWhilst that is an above inflation rise over the same 14 year period - it's doesn't support your assertion of a tripling of prices over 5 years.

And compare nos 11 & 17 - dropped in price from 2007 to 2012. So pick that 5yr period and things are very different.

kingston12 said:

i think that the problem is that we have had low interest rates for so long that a lot of people don't know anything else. £500k is now seen as £850 a month on an interest only mortgage. That is very affordable if you had the income to secure the mortgage in the first place, and even if you took a significant pay cut afterwards.

That is why you can't buy much of a house for £500k any more. Of course things should change, but will they? A few of the reasons why they might not:

1. The 'cat is out of the bag' with respect to prices, people are used to talking about these huge sums of money for houses, even if they are many many times what they earn and increasing more quickly.

2. As illusatrated by a lot of the comments on here, a lot of people think high house prices are a good thing. A lot of this is (rightfully) out of fear, we have got ourselves into this situation, how can we reduce prices without causing wider economic problems?

3. How long will it be before interest rates rise to anything like their long term average again? BoE are starting to talk about raising them, but I can't see how the base rate can go much higher than 1.5 or 2% for years to come. I am still seeing 10 year fixed rate mortgages on offer for 2.49% from mainstream lenders, so they seem fairly confident of this too.

Actually, I would say that the tide appears to be turning WRT public opinion on high house prices. More and more people - the younger generation principally - are being disadvantaged by the silly price of property.That is why you can't buy much of a house for £500k any more. Of course things should change, but will they? A few of the reasons why they might not:

1. The 'cat is out of the bag' with respect to prices, people are used to talking about these huge sums of money for houses, even if they are many many times what they earn and increasing more quickly.

2. As illusatrated by a lot of the comments on here, a lot of people think high house prices are a good thing. A lot of this is (rightfully) out of fear, we have got ourselves into this situation, how can we reduce prices without causing wider economic problems?

3. How long will it be before interest rates rise to anything like their long term average again? BoE are starting to talk about raising them, but I can't see how the base rate can go much higher than 1.5 or 2% for years to come. I am still seeing 10 year fixed rate mortgages on offer for 2.49% from mainstream lenders, so they seem fairly confident of this too.

Edited by kingston12 on Tuesday 11th July 10:01

Demographics are shifting and political parties will seek to appease the voter base, just as they did by pulling almost every trick in the book to keep existing homeowners happy by price-boosting economic policies when the demographic was in favour of high prices.

Lucas Ayde said:

Actually, I would say that the tide appears to be turning WRT public opinion on high house prices. More and more people - the younger generation principally - are being disadvantaged by the silly price of property.

And amongst us and our friends (somewhat older people) we aren't thrilled that our kids are struggling and that we're being leaned on for financial assistance.Sheepshanks said:

And amongst us and our friends (somewhat older people) we aren't thrilled that our kids are struggling and that we're being leaned on for financial assistance.

Genuine question: would you rather lend money to your children to get a property or see your property drop in value and not have to lend them money?Lucas Ayde said:

kingston12 said:

i think that the problem is that we have had low interest rates for so long that a lot of people don't know anything else. £500k is now seen as £850 a month on an interest only mortgage. That is very affordable if you had the income to secure the mortgage in the first place, and even if you took a significant pay cut afterwards.

That is why you can't buy much of a house for £500k any more. Of course things should change, but will they? A few of the reasons why they might not:

1. The 'cat is out of the bag' with respect to prices, people are used to talking about these huge sums of money for houses, even if they are many many times what they earn and increasing more quickly.

2. As illusatrated by a lot of the comments on here, a lot of people think high house prices are a good thing. A lot of this is (rightfully) out of fear, we have got ourselves into this situation, how can we reduce prices without causing wider economic problems?

3. How long will it be before interest rates rise to anything like their long term average again? BoE are starting to talk about raising them, but I can't see how the base rate can go much higher than 1.5 or 2% for years to come. I am still seeing 10 year fixed rate mortgages on offer for 2.49% from mainstream lenders, so they seem fairly confident of this too.

Actually, I would say that the tide appears to be turning WRT public opinion on high house prices. More and more people - the younger generation principally - are being disadvantaged by the silly price of property.That is why you can't buy much of a house for £500k any more. Of course things should change, but will they? A few of the reasons why they might not:

1. The 'cat is out of the bag' with respect to prices, people are used to talking about these huge sums of money for houses, even if they are many many times what they earn and increasing more quickly.

2. As illusatrated by a lot of the comments on here, a lot of people think high house prices are a good thing. A lot of this is (rightfully) out of fear, we have got ourselves into this situation, how can we reduce prices without causing wider economic problems?

3. How long will it be before interest rates rise to anything like their long term average again? BoE are starting to talk about raising them, but I can't see how the base rate can go much higher than 1.5 or 2% for years to come. I am still seeing 10 year fixed rate mortgages on offer for 2.49% from mainstream lenders, so they seem fairly confident of this too.

Edited by kingston12 on Tuesday 11th July 10:01

Demographics are shifting and political parties will seek to appease the voter base, just as they did by pulling almost every trick in the book to keep existing homeowners happy by price-boosting economic policies when the demographic was in favour of high prices.

Some of the anecdotal comments I hear don't make much sense to me - e.g. someone on this thread told me that it was easier to move up the property ladder during times of high price increases, and I recently overheard a conversation in my local pub referring to a £750k Victorian cottage in zone 6 as being 'too cheap'!

You are right, though, if we ever do get a far-left Corbyn-style government that represents the current sub-25 generation then things will change very quickly. Until then, they will remain unrepresented in this argument and some of them will reluctantly get on a much lower rung of the ladder than the previous generation and start cheering the price increases as well...

Sa Calobra said:

Scroll down there are alot more house results on that street on that page

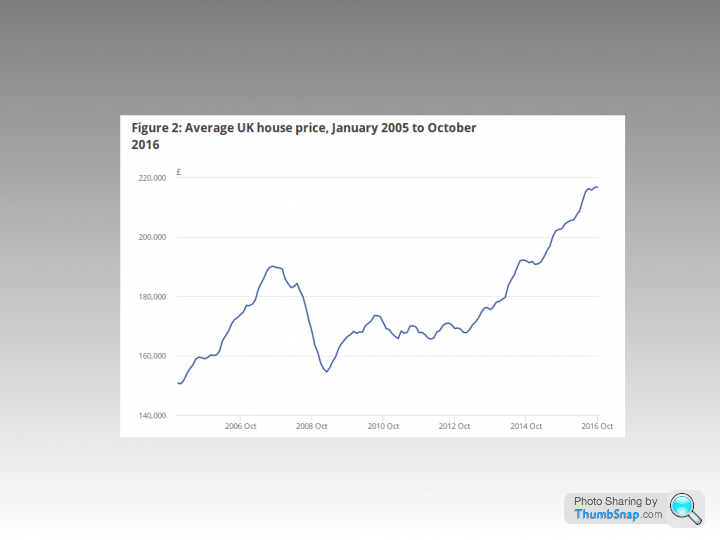

From the ONS, average UK house prices Jan 2005 to Oct 2016 ....https://www.ons.gov.uk/economy/inflationandpricein...

Maybe a 50% increase over the already stupid prices back then.

There was the beginning of a proper correction in 2007 but all manner of dodgy financial policies were brought forward to save the market and keep houses overpriced.

Lucas Ayde said:

From the ONS, average UK house prices Jan 2005 to Oct 2016 ....

https://www.ons.gov.uk/economy/inflationandpricein...

Maybe a 50% increase over the already stupid prices back then.

There was the beginning of a proper correction in 2007 but all manner of dodgy financial policies were brought forward to save the market and keep houses overpriced.

To save the banks and all the companies who have cash as deposits yes https://www.ons.gov.uk/economy/inflationandpricein...

Maybe a 50% increase over the already stupid prices back then.

There was the beginning of a proper correction in 2007 but all manner of dodgy financial policies were brought forward to save the market and keep houses overpriced.

Gassing Station | News, Politics & Economics | Top of Page | What's New | My Stuff