How far will house prices fall [volume 4]

Discussion

jonah35 said:

The long and short of it is people only see property as a one way risk free bet that only goes up in value

They will sell a kidney, a grandma, a foot, wife or sibling to be able to purchase on any terms at all

All these home buyers wouldn’t want to be desperate to get on the property ladder if prices were falling 2% pa and interest rates were 6%

It’s been a one way bet for too long.

Why wouldn’t you hock up a few million for a London flat if it would make you £30k per month in appreciation? That’s everyone’s logic and the sad thing is they’re right!!!!!!!

The govt needs to let property fall for long enough that people realise it is no longer a risk free win

The sad reality is that property is like the banks now; too big to fail. If property started to drop 5%pa and interest rates hit 6% it would be a bloodbath. You think the 2007-2011 recession was a tough time...They will sell a kidney, a grandma, a foot, wife or sibling to be able to purchase on any terms at all

All these home buyers wouldn’t want to be desperate to get on the property ladder if prices were falling 2% pa and interest rates were 6%

It’s been a one way bet for too long.

Why wouldn’t you hock up a few million for a London flat if it would make you £30k per month in appreciation? That’s everyone’s logic and the sad thing is they’re right!!!!!!!

The govt needs to let property fall for long enough that people realise it is no longer a risk free win

anonymous said:

[redacted]

The wife knows a couple teachers ranging from newly qualified to experienced, she also knows the girl who deals with salaries and payroll. The wife was offered the opportunity to go and qualify as a teacher and work at the school so she asked her friend about salaries and thats when she was told it's not a big jump and most of the other teachers are on 25-28k.

I don't know if the NUT site is wrong but I've seen the pay bands for London Borough of Sutton education roles and they don't paling with the NUT scale for sure - they're more along what I posted which is why I questioned you.

p1stonhead said:

snake_oil said:

ashleyman said:

Lots of stuff

I've just done a brief RM search. Seems plenty of 2 bed properties within 5 miles in the mid 200s which don't all look like ghettos, including in Sutton

This is a bit further out but looks nice, for example

ie http://www.rightmove.co.uk/s6p/55077933

If Natwest will only lend me £224,000 how am I supposed to buy something without Help 2 Buy. This was my point, other 2 beds in Sutton are around £300,000, if I can only borrow £224,000 + my deposit of £30,000 I'm at £254,000. That limits my options, Help 2 Buy means we can get something that costs more but then we have a loan AND a mortgage to pay off. It almost feels like we're being pushed to buy something using the Help 2 Buy scheme and based on what everyone has said in here, we can't even afford that.

ashleyman said:

The wife knows a couple teachers ranging from newly qualified to experienced, she also knows the girl who deals with salaries and payroll.

The wife was offered the opportunity to go and qualify as a teacher and work at the school so she asked her friend about salaries and thats when she was told it's not a big jump and most of the other teachers are on 25-28k.

I don't know if the NUT site is wrong but I've seen the pay bands for London Borough of Sutton education roles and they don't paling with the NUT scale for sure - they're more along what I posted which is why I questioned you.

The only uncertainty is about where Sutton is - is it Outer London, or fringe? Otherwise the pay scales are rigid. And it's absolutely standard to get somewhere from a little to a lot through TLR points. Progression to the senior pay scale isn't as automatic as it once was but you're then towards £40K basic,The wife was offered the opportunity to go and qualify as a teacher and work at the school so she asked her friend about salaries and thats when she was told it's not a big jump and most of the other teachers are on 25-28k.

I don't know if the NUT site is wrong but I've seen the pay bands for London Borough of Sutton education roles and they don't paling with the NUT scale for sure - they're more along what I posted which is why I questioned you.

It's possible the numbers that are being bandied around to your wife are after pension and student loan deductions - they make a chunky impact to a low salary.

ashleyman said:

anonymous said:

[redacted]

The wife knows a couple teachers ranging from newly qualified to experienced, she also knows the girl who deals with salaries and payroll. The wife was offered the opportunity to go and qualify as a teacher and work at the school so she asked her friend about salaries and thats when she was told it's not a big jump and most of the other teachers are on 25-28k.

I don't know if the NUT site is wrong but I've seen the pay bands for London Borough of Sutton education roles and they don't paling with the NUT scale for sure - they're more along what I posted which is why I questioned you.

p1stonhead said:

snake_oil said:

ashleyman said:

Lots of stuff

I've just done a brief RM search. Seems plenty of 2 bed properties within 5 miles in the mid 200s which don't all look like ghettos, including in Sutton This is a bit further out but looks nice, for example

ie http://www.rightmove.co.uk/s6p/55077933

If Natwest will only lend me £224,000 how am I supposed to buy something without Help 2 Buy. This was my point, other 2 beds in Sutton are around £300,000, if I can only borrow £224,000 + my deposit of £30,000 I'm at £254,000. That limits my options, Help 2 Buy means we can get something that costs more but then we have a loan AND a mortgage to pay off. It almost feels like we're being pushed to buy something using the Help 2 Buy scheme and based on what everyone has said in here, we can't even afford that.

anonymous said:

[redacted]

That's I think what many would say would be the ideal cooling scenario, but history possibly doesn't back this up? so perhaps it can be managed differently this time around, but possibly more likely things will snowball with the reverse sentiment in the face of declining prices regardless of what measures are taken to avoid it. I'm no doom merchant but when they come, falls in housing or any asset aren't normally soft/slow are they? ashleyman said:

Yep. Plus the property that guy posted is on an absolute dump of a council estate. It's a horrible place and I know another couple that lived not far from the block he posted and they couldn't wait to leave.

If Natwest will only lend me £224,000 how am I supposed to buy something without Help 2 Buy. This was my point, other 2 beds in Sutton are around £300,000, if I can only borrow £224,000 + my deposit of £30,000 I'm at £254,000. That limits my options, Help 2 Buy means we can get something that costs more but then we have a loan AND a mortgage to pay off. It almost feels like we're being pushed to buy something using the Help 2 Buy scheme and based on what everyone has said in here, we can't even afford that.

I’ll send a pm as I’m local and work in the industry. I may be able to introduce you to people that can assist.If Natwest will only lend me £224,000 how am I supposed to buy something without Help 2 Buy. This was my point, other 2 beds in Sutton are around £300,000, if I can only borrow £224,000 + my deposit of £30,000 I'm at £254,000. That limits my options, Help 2 Buy means we can get something that costs more but then we have a loan AND a mortgage to pay off. It almost feels like we're being pushed to buy something using the Help 2 Buy scheme and based on what everyone has said in here, we can't even afford that.

Obvs it is a given that working in the industry I am an evil person on nearly every level but the offer’s there.

Leave off the Tadworth flat, guys. Trying to make a living here...

scenario8 said:

ashleyman said:

Yep. Plus the property that guy posted is on an absolute dump of a council estate. It's a horrible place and I know another couple that lived not far from the block he posted and they couldn't wait to leave.

If Natwest will only lend me £224,000 how am I supposed to buy something without Help 2 Buy. This was my point, other 2 beds in Sutton are around £300,000, if I can only borrow £224,000 + my deposit of £30,000 I'm at £254,000. That limits my options, Help 2 Buy means we can get something that costs more but then we have a loan AND a mortgage to pay off. It almost feels like we're being pushed to buy something using the Help 2 Buy scheme and based on what everyone has said in here, we can't even afford that.

I’ll send a pm as I’m local and work in the industry. I may be able to introduce you to people that can assist.If Natwest will only lend me £224,000 how am I supposed to buy something without Help 2 Buy. This was my point, other 2 beds in Sutton are around £300,000, if I can only borrow £224,000 + my deposit of £30,000 I'm at £254,000. That limits my options, Help 2 Buy means we can get something that costs more but then we have a loan AND a mortgage to pay off. It almost feels like we're being pushed to buy something using the Help 2 Buy scheme and based on what everyone has said in here, we can't even afford that.

Obvs it is a given that working in the industry I am an evil person on nearly every level but the offer’s there.

Leave off the Tadworth flat, guys. Trying to make a living here...

p1stonhead said:

scenario8 said:

ashleyman said:

Yep. Plus the property that guy posted is on an absolute dump of a council estate. It's a horrible place and I know another couple that lived not far from the block he posted and they couldn't wait to leave.

If Natwest will only lend me £224,000 how am I supposed to buy something without Help 2 Buy. This was my point, other 2 beds in Sutton are around £300,000, if I can only borrow £224,000 + my deposit of £30,000 I'm at £254,000. That limits my options, Help 2 Buy means we can get something that costs more but then we have a loan AND a mortgage to pay off. It almost feels like we're being pushed to buy something using the Help 2 Buy scheme and based on what everyone has said in here, we can't even afford that.

I’ll send a pm as I’m local and work in the industry. I may be able to introduce you to people that can assist.If Natwest will only lend me £224,000 how am I supposed to buy something without Help 2 Buy. This was my point, other 2 beds in Sutton are around £300,000, if I can only borrow £224,000 + my deposit of £30,000 I'm at £254,000. That limits my options, Help 2 Buy means we can get something that costs more but then we have a loan AND a mortgage to pay off. It almost feels like we're being pushed to buy something using the Help 2 Buy scheme and based on what everyone has said in here, we can't even afford that.

Obvs it is a given that working in the industry I am an evil person on nearly every level but the offer’s there.

Leave off the Tadworth flat, guys. Trying to make a living here...

scenario8 said:

p1stonhead said:

scenario8 said:

ashleyman said:

Yep. Plus the property that guy posted is on an absolute dump of a council estate. It's a horrible place and I know another couple that lived not far from the block he posted and they couldn't wait to leave.

If Natwest will only lend me £224,000 how am I supposed to buy something without Help 2 Buy. This was my point, other 2 beds in Sutton are around £300,000, if I can only borrow £224,000 + my deposit of £30,000 I'm at £254,000. That limits my options, Help 2 Buy means we can get something that costs more but then we have a loan AND a mortgage to pay off. It almost feels like we're being pushed to buy something using the Help 2 Buy scheme and based on what everyone has said in here, we can't even afford that.

I’ll send a pm as I’m local and work in the industry. I may be able to introduce you to people that can assist.If Natwest will only lend me £224,000 how am I supposed to buy something without Help 2 Buy. This was my point, other 2 beds in Sutton are around £300,000, if I can only borrow £224,000 + my deposit of £30,000 I'm at £254,000. That limits my options, Help 2 Buy means we can get something that costs more but then we have a loan AND a mortgage to pay off. It almost feels like we're being pushed to buy something using the Help 2 Buy scheme and based on what everyone has said in here, we can't even afford that.

Obvs it is a given that working in the industry I am an evil person on nearly every level but the offer’s there.

Leave off the Tadworth flat, guys. Trying to make a living here...

t. Made stter because of the train crossing.

t. Made stter because of the train crossing.If there was a bridge or tunnel for the train it wouldnt be an issue.

You can wait ten minutes sometimes its ridiculous. Plus the station is right there so trains only ever go through the crossing at about 3mph when about to stop or starting off.

House prices in London fell again in May according to the ONS. They have now been falling for four consecutive months in the capital. This hasn't happened since Sept 2009

http://www.cityam.com/289377/stunted-house-price-g...

Anecdotally, I am trying to sell in Haslemere Surrey and it is pretty dead.

Also today's weaker than expected inflation data has some doubting we will see a BoE rate rise in August.

http://www.cityam.com/289377/stunted-house-price-g...

Anecdotally, I am trying to sell in Haslemere Surrey and it is pretty dead.

Also today's weaker than expected inflation data has some doubting we will see a BoE rate rise in August.

Anything to do with house price declining is a vote loser if it can be linked back to you which only adds to the issue, as it's in no one's (or very few) short term interest to see a decline so this stacks the odds more towards a worst correction, can kicking?

It often seems like a political pass the parcel where no party wants to be in situ when x y z happens because of the potential fallout and baggage they carry forever more when in reality they are all to blame (if that's even the right word) over the years.

It often seems like a political pass the parcel where no party wants to be in situ when x y z happens because of the potential fallout and baggage they carry forever more when in reality they are all to blame (if that's even the right word) over the years.

Scootersp said:

It often seems like a political pass the parcel where no party wants to be in situ when x y z happens because of the potential fallout and baggage they carry forever more when in reality they are all to blame (if that's even the right word) over the years.

Except for increasing National Debt. Labour are masters at this - spank the credit card and then blame the next government for not reducing the deficit. Voters lap it up because most of them can't even work out their utility bill unless Martin Lewis explains it to them. So we'll just get small rate rises whenever inflation strays too far - which I suppose is preferable to sharp house price falls.Edited by fido on Wednesday 18th July 14:58

fido said:

Scootersp said:

It often seems like a political pass the parcel where no party wants to be in situ when x y z happens because of the potential fallout and baggage they carry forever more when in reality they are all to blame (if that's even the right word) over the years.

Except for increasing National Debt. Labour are masters at this - spank the credit card and then blame the next government for not reducing the deficit. Voters lap it up because most of them can't even work out their utility bill unless Martin Lewis explains it to them.It’s just what happens in politics. Blame and credit is given and taken by the new kids on the block.

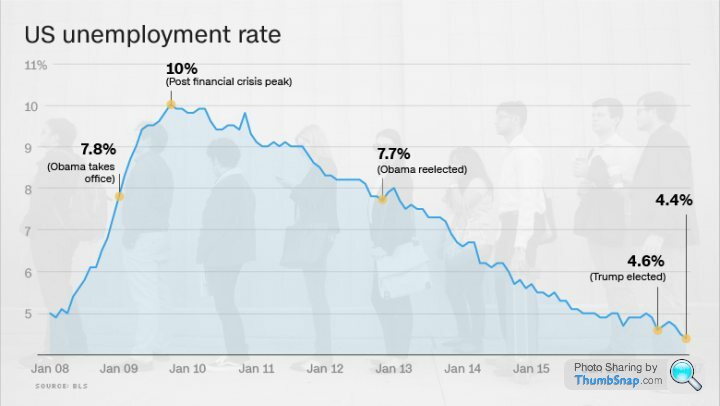

See Donald Trump - “unemployment at all time low!” despite the fact he started his run on the economy where he did

gibbon said:

im tempted to say there will no further rises in 2018....

Too much going on, not enough growth. The only upside to hiking at the moment is to be able to cut again once things really start getting stinky.

It's a perfect storm IMO for a number of reasons and I cannot see many ways out. As tonker says, sadly all I can see is to turn on the printing machine and inflate away and watch Sterling slide. Particularly with Brexit on the horizon that is externally damaging but at least props up the UK internally for now and avoids Armageddon. Too much going on, not enough growth. The only upside to hiking at the moment is to be able to cut again once things really start getting stinky.

Shnozz said:

It's a perfect storm IMO for a number of reasons and I cannot see many ways out. As tonker says, sadly all I can see is to turn on the printing machine and inflate away and watch Sterling slide. Particularly with Brexit on the horizon that is externally damaging but at least props up the UK internally for now and avoids Armageddon.

Armageddon is already happening because of Trump & Brexit. It is in advertising anyway.I've had 4 separate conversations over the last 2 days with about why things have stalled. Companies have stopped spending on ads & marketing. Because they've stopped spending, agencies aren't art buying. Because there's no art buying, contractors and freelancers have had no income. No income = no money to spend.

It's insane. The company I work for had 3x £30k briefs pulled in January. One client shot 17 projects in 2017 and in 2018 has shot 1 single brief. It's looking like it might p buck up in Sep, Oct, Nov but it might all slide to next year. It's very worrying.

Was 2007-2009 a good time to move further up the ladder, assuming you still had a stable income, or did things just kind of stop, no buyers for your current property etc?

Knew someone who sold to move into rented in 2007 only to buy a do-uppable barn conversion in 2009, no idea if they planned it but it saved them a fortune!

Knew someone who sold to move into rented in 2007 only to buy a do-uppable barn conversion in 2009, no idea if they planned it but it saved them a fortune!

Gassing Station | News, Politics & Economics | Top of Page | What's New | My Stuff