Discussion

Murph7355 said:

So TGLP are s t stirring.

t stirring.

A little, yes. t stirring. But, as mentioned previously, Uber has declared a provision in it's accounts for the potential VAT liability

Also common sense leads one to wonder if Uber would carry the cost of an appeal (that it may or may not win) if the outcome of losing was for HMRC to share the good (to Uber) news that it had not assessed it to a whacking great big VAT bill

Eric Mc said:

I see.

The question is, is Uber one large business with lots of staff (therefore, is all the income generated by the work of the staff really Uber's income and subject in full to VAT or is Uber just liabile to VAT on the bit Uber takes from the drivers in the form of "Commissions" or "Management Charges".

I'm sure this scenario exists for hundreds of businesses - not just Uber.

That's not quite it EricThe question is, is Uber one large business with lots of staff (therefore, is all the income generated by the work of the staff really Uber's income and subject in full to VAT or is Uber just liabile to VAT on the bit Uber takes from the drivers in the form of "Commissions" or "Management Charges".

I'm sure this scenario exists for hundreds of businesses - not just Uber.

The VAT in question is the VAT that would be due on the fare paid by the rider.

It is an Agent / Principal case. Is Uber the principal, or merely an agent. If uber is principal, then VAT would be due on the fare. If uber is merely agent, then VAT would only be due if the driver (or whatever party it was that Uber had introduced the rider to) was liable for VAT (usually based on turnover threshold)

This is why hmrc says it has been so cautious. It has challenged similar sorts of setups before (Secret Hotels is the most often cited) and lost the six most significant cases it has pursued.

The VAT position on the driver's commission is sort of insignificant because the relationship is the provision of a service to a UK driver by Uber in the Netherlands.

Mrr T said:

The reason there is no cross over is that the definition of those who are entitled to employment rights under employment law are fundermantally different to the definition of employment in tax law.

However, this thread is not about a case between HMRC and Uber. Currently there is no case.

This thread is about the attempt by the the Good "left wing" Law project to get HMRC to assess Uber for VAT. It started with them trying to force Uber to issue a VAT invoice for the whole amount of a trip. They lost. Then they tried to force HMRC to assess Uber for VAT. They lost. Now they want HMRC to confirm if they have assessed Uber for VAT. They lost but are appealing.

A total waste of time by a left wing organisation which hates Uber.

GLP won the High Court case about whether the existence, or not, of a VAT assessment should be made public. The court said yes it could & should be made public. It is Uber that is appealing against that decision.However, this thread is not about a case between HMRC and Uber. Currently there is no case.

This thread is about the attempt by the the Good "left wing" Law project to get HMRC to assess Uber for VAT. It started with them trying to force Uber to issue a VAT invoice for the whole amount of a trip. They lost. Then they tried to force HMRC to assess Uber for VAT. They lost. Now they want HMRC to confirm if they have assessed Uber for VAT. They lost but are appealing.

A total waste of time by a left wing organisation which hates Uber.

I don't think GLP hates Uber. I think it hates the fact that it gains an advantage on a questionable implementation of employment and tax law and that there was little evidence that the relevant authorities were ready to challenge those questionable implementations

The drivers had to bring a tribunal to get the "employee / worker / self employed" question looked at - HMRC wouldn't even look, even though it has responsibility for minimum wage and similar

Then GLP had to try several things to even get the VAT question looked at. HMRC doesn't usually comment on it's dealings with any individual tax case, but it can if it wants to. The High Court said HMRC could & should say whether it had made an assessment to VAT of Uber. Uber is the one making the appeal: it says the matter should stay private.

Let's also bear in mind that it isn't just in the UK that Uber is being challenged on these matters. Multiple jurisdictions are asking the same question and usually coming with the same answer in terms of "worker"

Mrr T said:

Is it really an agent/principal relationship. If it was the driver would have to be the principal and Uber the agent. That would mean the driver would have to include the gross cost in their turnover.

Is it not an introduction service. Uber contracts with the passangers and introduces them to the driver who then contract with the passangers.

Despite being outside the UK do Uber not apply UK VAT on the commission? In the same way the Amazon do?

The answer to the agent / principal question will, I expect, be one that the Supreme Court ends up decidingIs it not an introduction service. Uber contracts with the passangers and introduces them to the driver who then contract with the passangers.

Despite being outside the UK do Uber not apply UK VAT on the commission? In the same way the Amazon do?

That’s a good explanation on vat

I’ll add this to it as well. The main uk uber company is uber London ltd which, in it’s last filed accounts, showed ‘vat recoverable’ as a debtor with a value of almost £2.5m (it was nearly £2.9m they previous year).

I don’t know if it’s vat quarters are aligned with it’s year end, but that could be £10m or more in vat reclaims in a full year

Nothing wrong with that of course, it’s how VAT works in the setup uber has.

I’ll add this to it as well. The main uk uber company is uber London ltd which, in it’s last filed accounts, showed ‘vat recoverable’ as a debtor with a value of almost £2.5m (it was nearly £2.9m they previous year).

I don’t know if it’s vat quarters are aligned with it’s year end, but that could be £10m or more in vat reclaims in a full year

Nothing wrong with that of course, it’s how VAT works in the setup uber has.

The reality of the agreements between rider, driver and uber is yet to be legally settled in the UK

"Does uber sell rides (and is therefore a transportation services provider), or does it sell software to providers of transportation services?" has not been answered to the complete satisfaction of all concerned.

That is why the employment tribunal found drivers to be workers when uber said they were independent users of it's software and is, therefore, appealing the ET, EAT and Court of Appeal decisions in the Supreme Court.

That is why HMRC would (we will know if it has soon after the appeal court hearing on 1/2 April) raise a protective assessment on VAT. If HMRC does pursue uber for VAT it will, almost certainly, also end up in Supreme Court. I just can't see Uber accepting the outcome against it in any lower court / tribunal.

That is why many other jurisdictions other than the UK are testing the reality of those agreements through their legal systems too. In the US for instance, there was a case in North California District in which the court concluded that "Uber does not simply sell software; it sells rides. Uber is no more a "technology company" than Yellow Cab is a "technology company" because it uses CB radios to dispatch taxi cabs."

It is relatively easy to see both sides of the argument on a forum thread, but it will take at least one Supreme Court ruling on aspects of the way Uber works before the legal position is clear.

"Does uber sell rides (and is therefore a transportation services provider), or does it sell software to providers of transportation services?" has not been answered to the complete satisfaction of all concerned.

That is why the employment tribunal found drivers to be workers when uber said they were independent users of it's software and is, therefore, appealing the ET, EAT and Court of Appeal decisions in the Supreme Court.

That is why HMRC would (we will know if it has soon after the appeal court hearing on 1/2 April) raise a protective assessment on VAT. If HMRC does pursue uber for VAT it will, almost certainly, also end up in Supreme Court. I just can't see Uber accepting the outcome against it in any lower court / tribunal.

That is why many other jurisdictions other than the UK are testing the reality of those agreements through their legal systems too. In the US for instance, there was a case in North California District in which the court concluded that "Uber does not simply sell software; it sells rides. Uber is no more a "technology company" than Yellow Cab is a "technology company" because it uses CB radios to dispatch taxi cabs."

It is relatively easy to see both sides of the argument on a forum thread, but it will take at least one Supreme Court ruling on aspects of the way Uber works before the legal position is clear.

Edited by anonymous-user on Friday 28th February 16:18

Mrr T said:

In a post above you note Uber London Ltd is due tax refunds. I looked at the accounts and the reason is obvious.

As for your explanation above it misses the point. I am positive the contract between Uber and its drivers is clear. The driver appoints Uber to find them fare?. I am positive because I am sure Uber employed expensive lawyer to write it. So in any dispute between Uber and a driver under contract law the position would not be challenged.

Now under employment law the relationship matters more than the legal contract. Whether I agree with this or not does not matter. That why contractors now get holiday and sick pay.

I cannot say much about the law on taxi licensing but as Uber was the licenced business I assume it also looks at other aspects of the relationship.

Tax, including I assume VAT, views relationships in legal terms. There are exceptions. For example IR35, although that really only affect the way the sub contractor pays tax, not the legal relationship. Under tax law, I have less knowledge of VAT regulation, there are anti avoidence provisions (Dawson provisions) which allow HMRC to ignore step in a legal structure if the steps are artificial and only present to reduce the tax payable.

I cannot see any tax provisions which would allow HMRC to simply rewrite a legal relationship.

Have you read the employment tribunal, employment appeal tribunal and court of appeal judgments? Or the appellant & respondent submissions and judgments in the various ‘vat’ cases that have been brought?As for your explanation above it misses the point. I am positive the contract between Uber and its drivers is clear. The driver appoints Uber to find them fare?. I am positive because I am sure Uber employed expensive lawyer to write it. So in any dispute between Uber and a driver under contract law the position would not be challenged.

Now under employment law the relationship matters more than the legal contract. Whether I agree with this or not does not matter. That why contractors now get holiday and sick pay.

I cannot say much about the law on taxi licensing but as Uber was the licenced business I assume it also looks at other aspects of the relationship.

Tax, including I assume VAT, views relationships in legal terms. There are exceptions. For example IR35, although that really only affect the way the sub contractor pays tax, not the legal relationship. Under tax law, I have less knowledge of VAT regulation, there are anti avoidence provisions (Dawson provisions) which allow HMRC to ignore step in a legal structure if the steps are artificial and only present to reduce the tax payable.

I cannot see any tax provisions which would allow HMRC to simply rewrite a legal relationship.

Mrr T said:

I have read some but not all.

Unless I am mistaken the employment law on benefits for employees is based on statute, may even have been an EU directive, which creates a substance over form test. Since its statute law it implications would have been restricted to specific circumstances. No court would consider applying it in other areas of law since that was not the intension of parliament.

The Dawson principal which is now statue is very specific. It allow HMRC to ignore certain steps in a contractual chain if those steps meet certain tests. However, the legislation is clear HMRC can ignore steps they cannot create steps which do not exist. Think of it as a rubber not a pen.

The Good "left wing" Law Project want the court to create a contractual relationship where one does not exist. The is no foundation for this in tax law and while not an expert I would thing in VAT law.

I would suggest the idea is bad law. Do you really want a system where courts can ignore contracts and create contractual relationships which do not exist? That would rather undermine the basis of good legal system.

I want a system under which when a contract that claims to reflect reality is challenged as not doing so, that the truth of the matter is decided by the courts, not by the party that wrote the contract.Unless I am mistaken the employment law on benefits for employees is based on statute, may even have been an EU directive, which creates a substance over form test. Since its statute law it implications would have been restricted to specific circumstances. No court would consider applying it in other areas of law since that was not the intension of parliament.

The Dawson principal which is now statue is very specific. It allow HMRC to ignore certain steps in a contractual chain if those steps meet certain tests. However, the legislation is clear HMRC can ignore steps they cannot create steps which do not exist. Think of it as a rubber not a pen.

The Good "left wing" Law Project want the court to create a contractual relationship where one does not exist. The is no foundation for this in tax law and while not an expert I would thing in VAT law.

I would suggest the idea is bad law. Do you really want a system where courts can ignore contracts and create contractual relationships which do not exist? That would rather undermine the basis of good legal system.

GLP should not really have had the need, or indeed the opportunity, to get involved in this. It has milked the situation for a lot of publicity (some good, lots bad). HMRC should have addressed the VAT question of it's own accord. For all that we know, it may well have been investigating before GLP even knew what an uber was. But, that GLP's action have caused HMRC to act more quickly and more publicly than it otherwise would is a certainty. Whether that is good or bad is for debate, but we are where we are.

Similarly, drivers should not really have had the need to challenge their status as independent contractor / worker / employee. That is something that HMRC should and could have picked up and run with too.

The gig economy: by the speed it has grown; by the international nature of the players involved and as it operates on the fringes of existing legislation, is slightly ahead of regulations / legislation just now. There is some catching up to be done and this is one part of that catching up.

GLP's action can't create any new contractual relationship. All it's action seek to do is to have HMRC and the courts clarify the nature of the relationship between rider, driver and uber and, in doing so, have the parties involved treated accordingly (for VAT).

At it's simplest, uber says it is a technology company that acts as agent for independent drivers.

Those challenging that say that uber is a provider of transportation services: that a rider books a ride through uber, pays uber and complains to uber if something is wrong. A rider has no real say over which driver the ride is provided by, other than it is a driver registered with uber, vetted by uber, driving a vehicle covered in uber signage, carrying an uber identification badge, told about the existence of, scope of and other conditions associated with the ride by uber and paid for completing the ride by uber (paid an amount determined more by uber, than by the amount paid to uber by the rider).

The driver / uber relationship has been picked apart in the ET / EAT / Court of Appeal already and doesn't need repeating here prior to the supreme court having it's say too.

The contracts that have been written by uber (and it's expensive lawyers) are already under significant question from an employment law perspective and, it appears based on the actions of hmrc, uber and the high court, also from a VAT perspective.

In such circumstances, it is for the courts to decide if the contracts are in compliance with the laws under which they are governed. It isn't beyond the realms of possibility that the contracts are not compliant. Contracts are judged to be incorrect in law very regularly and very frequently by the courts.

Just one more thing on the VAT point. Canada and Australia are among the jurisdictions that, despite how uber originally set out it's contracts in those countries, did subsequently act to legislate that VAT (GST / HST) should apply on uber fares. Whilst those cases are not directly comparable to the UK situation, that's how it is.

Edited by anonymous-user on Saturday 29th February 10:05

On my understanding, the HMRC are interested in what the actual reality of a relationship is, and a contract claiming one thing is another does not override that reality.

That is not to say HMRC overriding a contractual position under VAT law means that same contract would then automatically be overridden under employment or commercial law, and vice versa.

That is not to say HMRC overriding a contractual position under VAT law means that same contract would then automatically be overridden under employment or commercial law, and vice versa.

There is no defence of glp by me here: as I said it shouldn’t have had the need or opportunity to be involved

But for you to defend uber on the basis that it’s contracts must be good because they were expensive is nonsense.

Multiple jurisdictions have already ruled that Uber’s contractual position on employment and tax were wrong and it looks quite possible that the uk will too. If, as seems likely, HMRC has raised a protective assessment on vat, then glp’s position becomes defensible. Not needed, but defensible.

The different route that Canada / Australia took re vat means that the uk will not need to change legislation to collect the vat (if it was / is due), it will simply collect it under the terms of the protective assessment historically and force uber to collect it in future. But the option to change legislation to collect vat on fares remains as an option if deemed necessary and approved by parliament

If, as you seem to think, Uber’s position is correct, then it will collect a slug of money for it’s costs and carry on re vat as it has done so far.

Let’s see

But for you to defend uber on the basis that it’s contracts must be good because they were expensive is nonsense.

Multiple jurisdictions have already ruled that Uber’s contractual position on employment and tax were wrong and it looks quite possible that the uk will too. If, as seems likely, HMRC has raised a protective assessment on vat, then glp’s position becomes defensible. Not needed, but defensible.

The different route that Canada / Australia took re vat means that the uk will not need to change legislation to collect the vat (if it was / is due), it will simply collect it under the terms of the protective assessment historically and force uber to collect it in future. But the option to change legislation to collect vat on fares remains as an option if deemed necessary and approved by parliament

If, as you seem to think, Uber’s position is correct, then it will collect a slug of money for it’s costs and carry on re vat as it has done so far.

Let’s see

A schedule update for Uber's appeal against the High Court decision that would otherwise have allowed HMRC to state if it had / had not assessed Uber to VAT

Now expected 9 April by video

https://twitter.com/GoodLawProject/status/12431293...

Now expected 9 April by video

https://twitter.com/GoodLawProject/status/12431293...

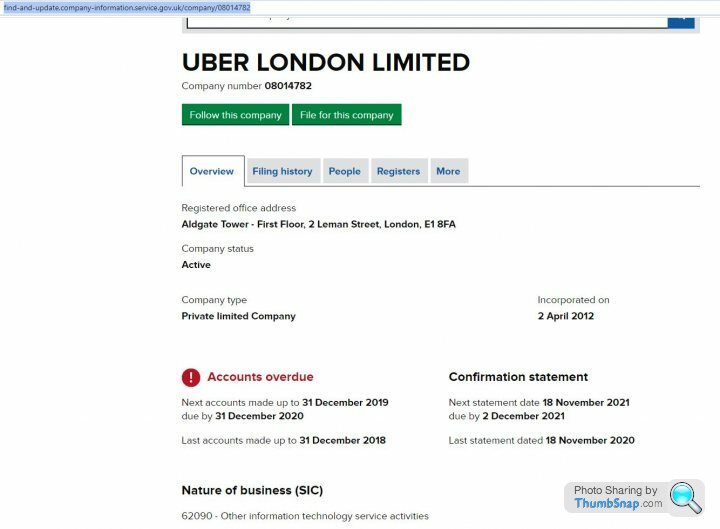

Just a month late with the filing of the accounts - marked by CH as received 29 Jan 2021

Unsurprisingly, the £6.2m profit before tax it made from its £82.5m turnover doesn't actually result in a cheque being cut to HMRC for any corporation tax. On the contrary, it creates a £132k tax credit to carry forward for future use

Unsurprisingly, the £6.2m profit before tax it made from its £82.5m turnover doesn't actually result in a cheque being cut to HMRC for any corporation tax. On the contrary, it creates a £132k tax credit to carry forward for future use

JPJPJP said:

Just a month late with the filing of the accounts - marked by CH as received 29 Jan 2021

Unsurprisingly, the £6.2m profit before tax it made from its £82.5m turnover doesn't actually result in a cheque being cut to HMRC for any corporation tax. On the contrary, it creates a £132k tax credit to carry forward for future use

Presuming they're carrying forward losses from previous years, is there any problem with that?Unsurprisingly, the £6.2m profit before tax it made from its £82.5m turnover doesn't actually result in a cheque being cut to HMRC for any corporation tax. On the contrary, it creates a £132k tax credit to carry forward for future use

RonaldMcDonaldAteMyCat said:

Presuming they're carrying forward losses from previous years, is there any problem with that?

I have no issue with there being no ct liability. Your presumption isn’t the main factor in the computation: it is mostly due to the way share based awards to staff are treated. Quite common in companies like this where the shares involved are in the parent co.

Gassing Station | News, Politics & Economics | Top of Page | What's New | My Stuff