How far will house prices fall [volume 5]

Discussion

An interesting article on how UK house sizes have changed over time:

https://www.labc.co.uk/news/what-average-house-siz...

https://www.labc.co.uk/news/what-average-house-siz...

FocusRS3 said:

2.7% YOY 'Jump' in house prices according to RM figures posted today.

Possibly the end of this thread.........

Jump in asking prices which can be impacted by both the mix of assets offered for sale (goes to reason with more certainty more expensive assets may come to the market) and the prices asked, not necessarily sold...Possibly the end of this thread.........

kiethton said:

Jump in asking prices which can be impacted by both the mix of assets offered for sale (goes to reason with more certainty more expensive assets may come to the market) and the prices asked, not necessarily sold...

Act good point......For some reason i was thinking it was based on SOLD prices......

kiethton said:

FocusRS3 said:

2.7% YOY 'Jump' in house prices according to RM figures posted today.

Possibly the end of this thread.........

Jump in asking prices which can be impacted by both the mix of assets offered for sale (goes to reason with more certainty more expensive assets may come to the market) and the prices asked, not necessarily sold...Possibly the end of this thread.........

s1962a said:

This reminds me of that housepricecrash website. Whether the market was going up/down/sideways the mood was always to prepare for the impending crash, and that anyone buying would be a fool. Broken clock and all that!

With Benign rates property isn't crashing. Reminds me of my old work colleague who viewed 100 flats over 3 years 1997 to 2000 waiting, waiting and finally purchased. He paid 50%+ more than he could have.If you have a 5 year+ view and it's a home just get it bought.

Burwood said:

kiethton said:

FocusRS3 said:

2.7% YOY 'Jump' in house prices according to RM figures posted today.

Possibly the end of this thread.........

Jump in asking prices which can be impacted by both the mix of assets offered for sale (goes to reason with more certainty more expensive assets may come to the market) and the prices asked, not necessarily sold...Possibly the end of this thread.........

Burwood said:

s1962a said:

This reminds me of that housepricecrash website. Whether the market was going up/down/sideways the mood was always to prepare for the impending crash, and that anyone buying would be a fool. Broken clock and all that!

With Benign rates property isn't crashing. Reminds me of my old work colleague who viewed 100 flats over 3 years 1997 to 2000 waiting, waiting and finally purchased. He paid 50%+ more than he could have.If you have a 5 year+ view and it's a home just get it bought.

Some of them have been so brainwashed into thinking the crash was coming that they have put off buying for 10 or even 15 years. Of course they don't want to admit they were wrong, so will try and convince themselves that renting was cheaper anyway.

I think that website has actually caused no end of grief, causing people to put their lives on hold for nothing. The amount of stories I read where the wife was begging the husband to buy somewhere, and the husband forcing the family to stay in rented for the inevitable crash.

Congrats Tonker! I will surely miss your unfairly objective comments on most of the properties shown here!

Can I request one last comment for us? so fire away please...

https://www.zoopla.co.uk/for-sale/details/53910659...

Can I request one last comment for us? so fire away please...

https://www.zoopla.co.uk/for-sale/details/53910659...

HoHoHo said:

Mojooo said:

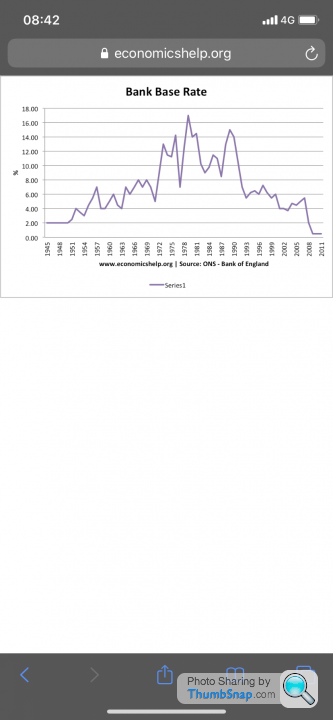

Have we got ourselves in a position now where interest rates simply cannot go up by much because too many people will be affected by a rate rise?

I don’t remember that thought process when rates went to 15% all those years ago............(i don't know, hence i am asking!)

Mojooo said:

HoHoHo said:

Mojooo said:

Have we got ourselves in a position now where interest rates simply cannot go up by much because too many people will be affected by a rate rise?

I don’t remember that thought process when rates went to 15% all those years ago............(i don't know, hence i am asking!)

It only takes a significant financial change and bosh......

We didn’t know WTF hit us when rates went that high on black Monday and I don’t see any reason why it should happen but you simply never know and can’t guarantee anything in this world.

We should avoid all personal responsibility for decisions to borrow and only think of thickos who have overextended themselves and/ or haven’t fixed their rates when considering the wider economy.

Oh actually, f k them. They’re the minority, or BTL miwyonaaaaares who are being shaken out by more subtle means anyway.

k them. They’re the minority, or BTL miwyonaaaaares who are being shaken out by more subtle means anyway.

Back to the topic, how is SW (of) London looking, as in Richmond, Twickenham, immediate surrounds?

I don’t know it at all but have family looking, in Zone 1 post election askings have gone up, not sure if that’s translating to action, not sure what is happening in more commuterville.

Oh actually, f

k them. They’re the minority, or BTL miwyonaaaaares who are being shaken out by more subtle means anyway.Back to the topic, how is SW (of) London looking, as in Richmond, Twickenham, immediate surrounds?

I don’t know it at all but have family looking, in Zone 1 post election askings have gone up, not sure if that’s translating to action, not sure what is happening in more commuterville.

Mojooo said:

Have we got ourselves in a position now where interest rates simply cannot go up by much because too many people will be affected by a rate rise?

Very much this, its also the bigger picture:We have a Tory government - people that own houses vote conservative, the current government don't want to p

s off their own Social care time bomb - we have the boomers beginning to reach old age. In general, liquid assets are a very small proportion of total net worth, maintaining house values remains key to paying for thier future social care needs.....house prices fall, they can't be paid and the government picks up the bill...they don't want that...

Interest rates - look at where LIBOR is and the trend - looking a where we are interest rates are likely to go down further - MMR and wage inflation is the limit on house prices now - currently stress-tested against rates we are unlikely to ever see - these could be reduced....

I came across a very good article the other day which explains all of this very well

https://bankunderground.co.uk/2020/01/13/whats-bee...

Mojooo said:

is it a different world now?

(i don't know, hence i am asking!)

(i don't know, hence i am asking!)

I don’t think there’s not thing particularly unusual about low interest rates, they maybe slightly lower than normal currently and I can’t see that changing until we start getting high inflation.

People are still feeling the impact from wage stagnation over the last 12 years.

Tlandcruiser said:

I don’t think there’s not thing particularly unusual about low interest rates, they maybe slightly lower than normal currently and I can’t see that changing until we start getting high inflation.

People are still feeling the impact from wage stagnation over the last 12 years.

What is doesn't show is that they have now been there for twelve years. To me, that is not only unusual, it is unprecedented.

Definitely agree that it won't change much, and the next move is probably down rather than up.

Wage stagnation is only part of the problem in my opinion. If wage stagnation had caused house price stagnation, most people would be better off now. House prices wouldn't be so stretched compared to incomes and there wouldn't be constant talk about crashes. Instead, low interest rates, increased LTV mortgages, Help to Buy etc. have all kept prices going up more than if wages had actually grown.

That doesn't mean that there will be any type of crash of course, just that the Government have to be increasingly careful what they do to keep the plates spinning. A 0.25% drop should probably be enough for now.

ooid said:

Congrats Tonker! I will surely miss your unfairly objective comments on most of the properties shown here!

Can I request one last comment for us? so fire away please...

https://www.zoopla.co.uk/for-sale/details/53910659...

ooidCan I request one last comment for us? so fire away please...

https://www.zoopla.co.uk/for-sale/details/53910659...

that house is waaaaaay too close to the green man interchange and the A12 - both in noise and pollution terms.

Mojooo said:

Have we got ourselves in a position now where interest rates simply cannot go up by much because too many people will be affected by a rate rise?

They could go back to 4-5% but the outlook is for historically low rates. In fact the BOE predicts low rates for 20 years. The driver behind OUR interest rates is mainly inflation which is low and has been for 15 years+. I remember it was 10%+ in the 80sMy first job before Uni was working for a stock brokerage, 1987 just before the crash. The Principal of the firm had a 1M overdraft (we opened all the mail) which he had to buy the house next door and build a tennis court. He was paying 25% interest on this money but serious money. Then boom. His firm was gone and he went off to a hospital to recover from depression. Crazy times.

Gassing Station | News, Politics & Economics | Top of Page | What's New | My Stuff