How Far Will House Prices Fall? [Volume 6]

Discussion

skwdenyer said:

If the Govt wishes to really control inflation, it is going to have to take very different steps: rent controls, price controls, tiered energy costs, and so on. At the same time, it needs to invest heavily in building up the UK's manufacturing and food sectors to improve our balance of trade - because otherwise imported inflation is going to get us time and again - not least because we're way past the point where interest rates have any macro impact on FX.

In other words prices and income policies that were tried in the 70s and failed.The current inflation was foreseen by many as it was preceded by a surge in the money supply. The BOE both created that situation and failed to react early enough and are now playing catch-up. The only thing likely to curb inflation in the short term is higher interest rates and tight fiscal policy.

Medium term they need to rethink energy and food production policy entirely throughout western Europe, but that won't help right now.

Whereas I DO think wages are and will continue to form a significant part of inflation. We’re seeing wage inflation all over the place - three examples:

- Union-agreed pay deals: Nurses 7% this year, tube 8%, train drivers 8% over 2 years, and Wales teachers have just agreed 3% now and another 5% in September

- Retail: Pret upped wages 5% in Dec, and another 3% effective April, Tesco have increased base retail pay by 15.5% in the last 10 months

- Professional services: PWC awarded 7% pay rise to staff last July, other Big 4 did similar. The lawyers went absolutely crazy 2021-22.

Ultimately the labour market still remains very tight. Firm profits across many industries were at an all time high in 2022 - and so it is rational for those firms to pass some of those profits on to employees to attract and retain them.

Similarly firms now are saying “it’s an inflationary environment, we have to put up prices”

The only way to stop that wage/price spiral is to dampen demand. Bring some competitiveness back into firm pricing, and some slack into the labour market to dampen wages.

- Union-agreed pay deals: Nurses 7% this year, tube 8%, train drivers 8% over 2 years, and Wales teachers have just agreed 3% now and another 5% in September

- Retail: Pret upped wages 5% in Dec, and another 3% effective April, Tesco have increased base retail pay by 15.5% in the last 10 months

- Professional services: PWC awarded 7% pay rise to staff last July, other Big 4 did similar. The lawyers went absolutely crazy 2021-22.

Ultimately the labour market still remains very tight. Firm profits across many industries were at an all time high in 2022 - and so it is rational for those firms to pass some of those profits on to employees to attract and retain them.

Similarly firms now are saying “it’s an inflationary environment, we have to put up prices”

The only way to stop that wage/price spiral is to dampen demand. Bring some competitiveness back into firm pricing, and some slack into the labour market to dampen wages.

brickwall said:

Whereas I DO think wages are and will continue to form a significant part of inflation. We’re seeing wage inflation all over the place - three examples:

- Union-agreed pay deals: Nurses 7% this year, tube 8%, train drivers 8% over 2 years, and Wales teachers have just agreed 3% now and another 5% in September

- Retail: Pret upped wages 5% in Dec, and another 3% effective April, Tesco have increased base retail pay by 15.5% in the last 10 months

- Professional services: PWC awarded 7% pay rise to staff last July, other Big 4 did similar. The lawyers went absolutely crazy 2021-22.

Ultimately the labour market still remains very tight. Firm profits across many industries were at an all time high in 2022 - and so it is rational for those firms to pass some of those profits on to employees to attract and retain them.

Similarly firms now are saying “it’s an inflationary environment, we have to put up prices”

The only way to stop that wage/price spiral is to dampen demand. Bring some competitiveness back into firm pricing, and some slack into the labour market to dampen wages.

That would be fine, if spending and wages were the leading indicator. They’re not. Not just now, either - look at real terms wage trends.- Union-agreed pay deals: Nurses 7% this year, tube 8%, train drivers 8% over 2 years, and Wales teachers have just agreed 3% now and another 5% in September

- Retail: Pret upped wages 5% in Dec, and another 3% effective April, Tesco have increased base retail pay by 15.5% in the last 10 months

- Professional services: PWC awarded 7% pay rise to staff last July, other Big 4 did similar. The lawyers went absolutely crazy 2021-22.

Ultimately the labour market still remains very tight. Firm profits across many industries were at an all time high in 2022 - and so it is rational for those firms to pass some of those profits on to employees to attract and retain them.

Similarly firms now are saying “it’s an inflationary environment, we have to put up prices”

The only way to stop that wage/price spiral is to dampen demand. Bring some competitiveness back into firm pricing, and some slack into the labour market to dampen wages.

If you can tell me how food prices, say, are being driven by excess wages, I’ll be delighted. Likewise energy costs.

As regards imported goods, you have to understand global markets. For instance, I source from - amongst other places - India. Indian inflation has been >7% pa since the mid 2000s. Meanwhile, GBP used to be 2 USD (and we buy in dollars). The price of imports is way higher than it used to be. China helped dampen that for a while with a glut of cheap production, but those days are over.

If all the inflation is imported, dampening it with the cosh of interest rates is just going to destroy our economy. Better to ride it out until equilibrium returns, IMHO.

skwdenyer said:

brickwall said:

Whereas I DO think wages are and will continue to form a significant part of inflation. We’re seeing wage inflation all over the place - three examples:

- Union-agreed pay deals: Nurses 7% this year, tube 8%, train drivers 8% over 2 years, and Wales teachers have just agreed 3% now and another 5% in September

- Retail: Pret upped wages 5% in Dec, and another 3% effective April, Tesco have increased base retail pay by 15.5% in the last 10 months

- Professional services: PWC awarded 7% pay rise to staff last July, other Big 4 did similar. The lawyers went absolutely crazy 2021-22.

Ultimately the labour market still remains very tight. Firm profits across many industries were at an all time high in 2022 - and so it is rational for those firms to pass some of those profits on to employees to attract and retain them.

Similarly firms now are saying “it’s an inflationary environment, we have to put up prices”

The only way to stop that wage/price spiral is to dampen demand. Bring some competitiveness back into firm pricing, and some slack into the labour market to dampen wages.

That would be fine, if spending and wages were the leading indicator. They’re not. Not just now, either - look at real terms wage trends.- Union-agreed pay deals: Nurses 7% this year, tube 8%, train drivers 8% over 2 years, and Wales teachers have just agreed 3% now and another 5% in September

- Retail: Pret upped wages 5% in Dec, and another 3% effective April, Tesco have increased base retail pay by 15.5% in the last 10 months

- Professional services: PWC awarded 7% pay rise to staff last July, other Big 4 did similar. The lawyers went absolutely crazy 2021-22.

Ultimately the labour market still remains very tight. Firm profits across many industries were at an all time high in 2022 - and so it is rational for those firms to pass some of those profits on to employees to attract and retain them.

Similarly firms now are saying “it’s an inflationary environment, we have to put up prices”

The only way to stop that wage/price spiral is to dampen demand. Bring some competitiveness back into firm pricing, and some slack into the labour market to dampen wages.

If you can tell me how food prices, say, are being driven by excess wages, I’ll be delighted. Likewise energy costs.

As regards imported goods, you have to understand global markets. For instance, I source from - amongst other places - India. Indian inflation has been >7% pa since the mid 2000s. Meanwhile, GBP used to be 2 USD (and we buy in dollars). The price of imports is way higher than it used to be. China helped dampen that for a while with a glut of cheap production, but those days are over.

If all the inflation is imported, dampening it with the cosh of interest rates is just going to destroy our economy. Better to ride it out until equilibrium returns, IMHO.

brickwall said:

skwdenyer said:

brickwall said:

Whereas I DO think wages are and will continue to form a significant part of inflation. We’re seeing wage inflation all over the place - three examples:

- Union-agreed pay deals: Nurses 7% this year, tube 8%, train drivers 8% over 2 years, and Wales teachers have just agreed 3% now and another 5% in September

- Retail: Pret upped wages 5% in Dec, and another 3% effective April, Tesco have increased base retail pay by 15.5% in the last 10 months

- Professional services: PWC awarded 7% pay rise to staff last July, other Big 4 did similar. The lawyers went absolutely crazy 2021-22.

Ultimately the labour market still remains very tight. Firm profits across many industries were at an all time high in 2022 - and so it is rational for those firms to pass some of those profits on to employees to attract and retain them.

Similarly firms now are saying “it’s an inflationary environment, we have to put up prices”

The only way to stop that wage/price spiral is to dampen demand. Bring some competitiveness back into firm pricing, and some slack into the labour market to dampen wages.

That would be fine, if spending and wages were the leading indicator. They’re not. Not just now, either - look at real terms wage trends.- Union-agreed pay deals: Nurses 7% this year, tube 8%, train drivers 8% over 2 years, and Wales teachers have just agreed 3% now and another 5% in September

- Retail: Pret upped wages 5% in Dec, and another 3% effective April, Tesco have increased base retail pay by 15.5% in the last 10 months

- Professional services: PWC awarded 7% pay rise to staff last July, other Big 4 did similar. The lawyers went absolutely crazy 2021-22.

Ultimately the labour market still remains very tight. Firm profits across many industries were at an all time high in 2022 - and so it is rational for those firms to pass some of those profits on to employees to attract and retain them.

Similarly firms now are saying “it’s an inflationary environment, we have to put up prices”

The only way to stop that wage/price spiral is to dampen demand. Bring some competitiveness back into firm pricing, and some slack into the labour market to dampen wages.

If you can tell me how food prices, say, are being driven by excess wages, I’ll be delighted. Likewise energy costs.

As regards imported goods, you have to understand global markets. For instance, I source from - amongst other places - India. Indian inflation has been >7% pa since the mid 2000s. Meanwhile, GBP used to be 2 USD (and we buy in dollars). The price of imports is way higher than it used to be. China helped dampen that for a while with a glut of cheap production, but those days are over.

If all the inflation is imported, dampening it with the cosh of interest rates is just going to destroy our economy. Better to ride it out until equilibrium returns, IMHO.

This is an interesting one. Property shows no sales history on right move.

https://www.rightmove.co.uk/properties/131354048#/...

But searching for recently sold in same area brings up this

https://www.rightmove.co.uk/house-prices/details/e...

Which seems to be same place. So one "quick sale" followed by another being back on sale ten months later, without any work being done apart from a little bit of painting, and for £22K more

https://www.rightmove.co.uk/properties/131354048#/...

But searching for recently sold in same area brings up this

https://www.rightmove.co.uk/house-prices/details/e...

Which seems to be same place. So one "quick sale" followed by another being back on sale ten months later, without any work being done apart from a little bit of painting, and for £22K more

brickwall said:

skwdenyer said:

brickwall said:

Whereas I DO think wages are and will continue to form a significant part of inflation. We’re seeing wage inflation all over the place - three examples:

- Union-agreed pay deals: Nurses 7% this year, tube 8%, train drivers 8% over 2 years, and Wales teachers have just agreed 3% now and another 5% in September

- Retail: Pret upped wages 5% in Dec, and another 3% effective April, Tesco have increased base retail pay by 15.5% in the last 10 months

- Professional services: PWC awarded 7% pay rise to staff last July, other Big 4 did similar. The lawyers went absolutely crazy 2021-22.

Ultimately the labour market still remains very tight. Firm profits across many industries were at an all time high in 2022 - and so it is rational for those firms to pass some of those profits on to employees to attract and retain them.

Similarly firms now are saying “it’s an inflationary environment, we have to put up prices”

The only way to stop that wage/price spiral is to dampen demand. Bring some competitiveness back into firm pricing, and some slack into the labour market to dampen wages.

That would be fine, if spending and wages were the leading indicator. They’re not. Not just now, either - look at real terms wage trends.- Union-agreed pay deals: Nurses 7% this year, tube 8%, train drivers 8% over 2 years, and Wales teachers have just agreed 3% now and another 5% in September

- Retail: Pret upped wages 5% in Dec, and another 3% effective April, Tesco have increased base retail pay by 15.5% in the last 10 months

- Professional services: PWC awarded 7% pay rise to staff last July, other Big 4 did similar. The lawyers went absolutely crazy 2021-22.

Ultimately the labour market still remains very tight. Firm profits across many industries were at an all time high in 2022 - and so it is rational for those firms to pass some of those profits on to employees to attract and retain them.

Similarly firms now are saying “it’s an inflationary environment, we have to put up prices”

The only way to stop that wage/price spiral is to dampen demand. Bring some competitiveness back into firm pricing, and some slack into the labour market to dampen wages.

If you can tell me how food prices, say, are being driven by excess wages, I’ll be delighted. Likewise energy costs.

As regards imported goods, you have to understand global markets. For instance, I source from - amongst other places - India. Indian inflation has been >7% pa since the mid 2000s. Meanwhile, GBP used to be 2 USD (and we buy in dollars). The price of imports is way higher than it used to be. China helped dampen that for a while with a glut of cheap production, but those days are over.

If all the inflation is imported, dampening it with the cosh of interest rates is just going to destroy our economy. Better to ride it out until equilibrium returns, IMHO.

That being so, it would be useful to try to characterise the extent of that modifier, so as to be able to decide whether the benefit of a small modification to FX rates is worth the domestic pain of the rise.

There is also a circular component to the problem: if a rate rise reinforces FX rates, but at the same time depresses the economy, in turn leading to a fall in FX rates due to other underlying drivers, which is the optimum strategy?

Of the multitude of effects driving FX rates, it seems to me that interest rates are not high on the list. Confidence in the UK economy (not good), growth (very poor), lack of clarity / belief in future growth (so no point in speculating on higher rates), current account deficit (not good), low domestic investment, and so on are all important drivers that are likely to be rather more important than short-term interest rate movements. They explain the collapse in the value of Sterling over the last few years.

For my money, a decent economic policy focussed on growth and prosperity is likely to be far more beneficial all round, rather than using interest rates in a (IMHO vain) attempt to support the currency. But it would be interesting to hear from some FX professionals on this.

JagLover said:

This is an interesting one. Property shows no sales history on right move.

https://www.rightmove.co.uk/properties/131354048#/...

But searching for recently sold in same area brings up this

https://www.rightmove.co.uk/house-prices/details/e...

Which seems to be same place. So one "quick sale" followed by another being back on sale ten months later, without any work being done apart from a little bit of painting, and for £22K more

Something odd about that. Rightmove says previously listed for sale Jan 2018. The listing for last time it was on RM is here:https://www.rightmove.co.uk/properties/131354048#/...

But searching for recently sold in same area brings up this

https://www.rightmove.co.uk/house-prices/details/e...

Which seems to be same place. So one "quick sale" followed by another being back on sale ten months later, without any work being done apart from a little bit of painting, and for £22K more

https://www.rightmove.co.uk/properties/49883592#/?...

with an asking of £157,500. But it isn't clear when exactly that was.

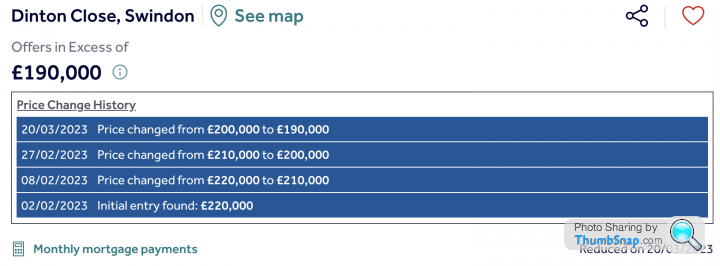

Also notable that the £190k asking is the *reduced* figure - look at the price history:

Imo the inflation has now become embedded and will be fully felt nearer to the end of this year.

The job outlook in the tech industry has changed markedly in the past few months.

In the area I'm in (AV) the excessive lead times and price increases on equipment over the past couple of years has pushed back so many projects that many have now been written off by the clients.

Back to house prices, saw this article on the BBC and wondered what sort of property or mortgage this guy they use as an example of the cost of living crisis must own?

The job outlook in the tech industry has changed markedly in the past few months.

In the area I'm in (AV) the excessive lead times and price increases on equipment over the past couple of years has pushed back so many projects that many have now been written off by the clients.

Back to house prices, saw this article on the BBC and wondered what sort of property or mortgage this guy they use as an example of the cost of living crisis must own?

BBC article said:

Neil Sutton's monthly mortgage payments were £255 before they started going up in January 2022, but they will rise to £1465 from next month

https://www.bbc.com/news/business-65048756

https://www.bbc.com/news/business-65048756

untakenname said:

Imo the inflation has now become embedded and will be fully felt nearer to the end of this year.

The job outlook in the tech industry has changed markedly in the past few months.

In the area I'm in (AV) the excessive lead times and price increases on equipment over the past couple of years has pushed back so many projects that many have now been written off by the clients.

Back to house prices, saw this article on the BBC and wondered what sort of property or mortgage this guy they use as an example of the cost of living crisis must own?

The £150 additional sum suggests its a typo and should be £255>£465.The job outlook in the tech industry has changed markedly in the past few months.

In the area I'm in (AV) the excessive lead times and price increases on equipment over the past couple of years has pushed back so many projects that many have now been written off by the clients.

Back to house prices, saw this article on the BBC and wondered what sort of property or mortgage this guy they use as an example of the cost of living crisis must own?

BBC article said:

Neil Sutton's monthly mortgage payments were £255 before they started going up in January 2022, but they will rise to £1465 from next month

https://www.bbc.com/news/business-65048756

https://www.bbc.com/news/business-65048756

Shnozz said:

untakenname said:

Imo the inflation has now become embedded and will be fully felt nearer to the end of this year.

The job outlook in the tech industry has changed markedly in the past few months.

In the area I'm in (AV) the excessive lead times and price increases on equipment over the past couple of years has pushed back so many projects that many have now been written off by the clients.

Back to house prices, saw this article on the BBC and wondered what sort of property or mortgage this guy they use as an example of the cost of living crisis must own?

The £150 additional sum suggests its a typo and should be £255>£465.The job outlook in the tech industry has changed markedly in the past few months.

In the area I'm in (AV) the excessive lead times and price increases on equipment over the past couple of years has pushed back so many projects that many have now been written off by the clients.

Back to house prices, saw this article on the BBC and wondered what sort of property or mortgage this guy they use as an example of the cost of living crisis must own?

BBC article said:

Neil Sutton's monthly mortgage payments were £255 before they started going up in January 2022, but they will rise to £1465 from next month

https://www.bbc.com/news/business-65048756

https://www.bbc.com/news/business-65048756

Shnozz said:

untakenname said:

Imo the inflation has now become embedded and will be fully felt nearer to the end of this year.

The job outlook in the tech industry has changed markedly in the past few months.

In the area I'm in (AV) the excessive lead times and price increases on equipment over the past couple of years has pushed back so many projects that many have now been written off by the clients.

Back to house prices, saw this article on the BBC and wondered what sort of property or mortgage this guy they use as an example of the cost of living crisis must own?

The £150 additional sum suggests its a typo and should be £255>£465.The job outlook in the tech industry has changed markedly in the past few months.

In the area I'm in (AV) the excessive lead times and price increases on equipment over the past couple of years has pushed back so many projects that many have now been written off by the clients.

Back to house prices, saw this article on the BBC and wondered what sort of property or mortgage this guy they use as an example of the cost of living crisis must own?

BBC article said:

Neil Sutton's monthly mortgage payments were £255 before they started going up in January 2022, but they will rise to £1465 from next month

https://www.bbc.com/news/business-65048756

https://www.bbc.com/news/business-65048756

Assume it must be an interest only mortage.

skwdenyer said:

Something odd about that. Rightmove says previously listed for sale Jan 2018. The listing for last time it was on RM is here:

https://www.rightmove.co.uk/properties/49883592#/?...

with an asking of £157,500. But it isn't clear when exactly that was.

Also notable that the £190k asking is the *reduced* figure - look at the price history:

Wasn't aware of all those reductions, though was aware it was reduced.https://www.rightmove.co.uk/properties/49883592#/?...

with an asking of £157,500. But it isn't clear when exactly that was.

Also notable that the £190k asking is the *reduced* figure - look at the price history:

So bought for £167,500 in April of 2022 and they wanted £220K for it ten months later after doing no work on it in the meantime other than painting the bathroom a worse colour.

Either they have very unrealistic expectations or have a very poor agent.

To be fair £167,500 was on the low side, those flats perched atop three garages are common in the area, "coach houses", and do command a substantial premium.

untakenname said:

Imo the inflation has now become embedded and will be fully felt nearer to the end of this year.

The job outlook in the tech industry has changed markedly in the past few months.

In the area I'm in (AV) the excessive lead times and price increases on equipment over the past couple of years has pushed back so many projects that many have now been written off by the clients.

Back to house prices, saw this article on the BBC and wondered what sort of property or mortgage this guy they use as an example of the cost of living crisis must own?

When you say AV are you mainly referring of physical Video Conference faculties? Only asking because while we see a lot of manufacturers pushing the physical meeting angle, no one that works for us cares about AV equipment and in any five week most of it gets unplugged. The job outlook in the tech industry has changed markedly in the past few months.

In the area I'm in (AV) the excessive lead times and price increases on equipment over the past couple of years has pushed back so many projects that many have now been written off by the clients.

Back to house prices, saw this article on the BBC and wondered what sort of property or mortgage this guy they use as an example of the cost of living crisis must own?

BBC article said:

Neil Sutton's monthly mortgage payments were £255 before they started going up in January 2022, but they will rise to £1465 from next month

https://www.bbc.com/news/business-65048756

https://www.bbc.com/news/business-65048756

In terms of ownership, my take is that you’re still better off buying - we will likely see stagnation, but I doubt properties will become markedly cheaper.

https://www.bbc.co.uk/news/business-65112278

700m borrowed for mortgages in February, versus 2bn borrowed in January.

Is that not a catastrophic reduction in borrowing sums?

700m borrowed for mortgages in February, versus 2bn borrowed in January.

Is that not a catastrophic reduction in borrowing sums?

G-wiz said:

https://www.bbc.co.uk/news/business-65112278

700m borrowed for mortgages in February, versus 2bn borrowed in January.

Is that not a catastrophic reduction in borrowing sums?

Not the best news for the market. 700m borrowed for mortgages in February, versus 2bn borrowed in January.

Is that not a catastrophic reduction in borrowing sums?

Oddly enough ( typical of our timing) we had an EA round this morning who is coming back to us.

Nothing for sale locally so would suggest everyone’s staying put

GT3Manthey said:

Not the best news for the market.

Oddly enough ( typical of our timing) we had an EA round this morning who is coming back to us.

Nothing for sale locally so would suggest everyone’s staying put

We’ve had nothing on the market on our development for a while, then one came up a couple of months ago and sold straight away. Three more have come up in the last fortnight, two of which are SSTC (and the third one they’ve buggered about so much with the configuration that I doubt it will sell in a hurry).Oddly enough ( typical of our timing) we had an EA round this morning who is coming back to us.

Nothing for sale locally so would suggest everyone’s staying put

May be O/T but a house near me is up for sale with the option of reduced price for people aged over 60 through Homewise's Home for Life Plan.

Says savings can be between 8% and 59% depending on age and other circumstances.

Never heard of this.

House hasn't got a for sale board outside but is also advertised by a local 'normal' EA for £300k.

Is this similar to the companies who will remortgage part of your house and let you stay in it?

Says savings can be between 8% and 59% depending on age and other circumstances.

Never heard of this.

House hasn't got a for sale board outside but is also advertised by a local 'normal' EA for £300k.

Is this similar to the companies who will remortgage part of your house and let you stay in it?

Gassing Station | News, Politics & Economics | Top of Page | What's New | My Stuff