How Far Will House Prices Fall? [Volume 6]

Discussion

DoubleSix said:

You don’t have to look far back to observe that the low interest rate environment was historically unusual. It would seem incredibly naive to me, disingenuous even, to build one’s personal borrowing around the assumption these things will stay constant when they are known to be variable. If you aren’t making financial decisions with half an eye on “worst case” or even just “very bad” scenarios then you aren’t properly assessing risk in the first place.

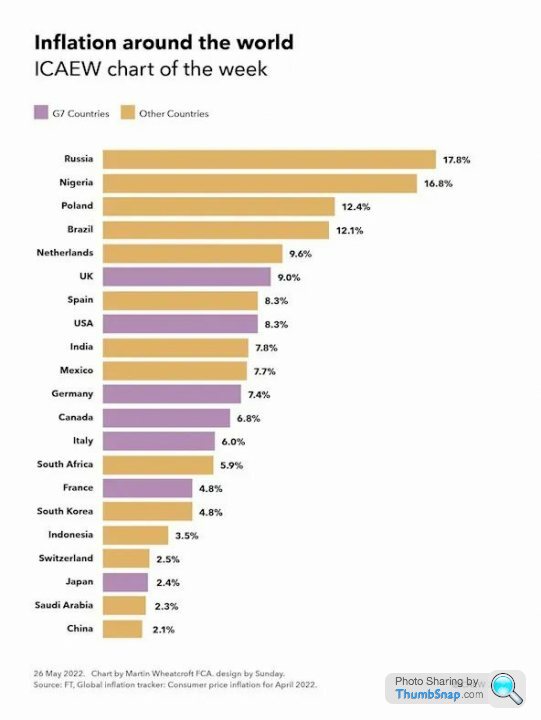

The inflationary issues, and attempts to control them, have been a global phenomenon. Placing these issues at the door of UK Gov when unable to meet personal obligations is frankly to deny ones own agency.

(FWIW: i have very substantial personal borrowings, across multiple properties and projects. My choice. And im confident i can meet my obligations up to double digit interest rates. Beyond that its time to make hard choices and accept things didn’t go my way. I wont be blaming the government for my decision to leverage my own personal borrowing).

Most western governments dealt with Covid in the same fashion. Lockdown of parts of the economy, financed by massive government spending, that was then monetarised. So it is hardly surprising that they have similar numbers, before you look at knock on effects in an inter-connected world.The inflationary issues, and attempts to control them, have been a global phenomenon. Placing these issues at the door of UK Gov when unable to meet personal obligations is frankly to deny ones own agency.

(FWIW: i have very substantial personal borrowings, across multiple properties and projects. My choice. And im confident i can meet my obligations up to double digit interest rates. Beyond that its time to make hard choices and accept things didn’t go my way. I wont be blaming the government for my decision to leverage my own personal borrowing).

Edited by DoubleSix on Friday 31st March 08:36

Added to which are the developing costs of energy policy which again was a deliberate government policy.

number2 said:

I wouldn't blame the government, or the individuals in the main.

We can't mitigate all risk, some we just have to accept.

However, we aren't at that stage yet, things aren't that bad. Rates are only at 4.25pc.

There's a lot of whining certainly, from individuals cherry picked by the media to give them the hard-done-by stories they're after.

With inflation at 9-10% that 4.25% is a negative rate. As long as your income increase keeps up with the rate you're paying then no problem.We can't mitigate all risk, some we just have to accept.

However, we aren't at that stage yet, things aren't that bad. Rates are only at 4.25pc.

There's a lot of whining certainly, from individuals cherry picked by the media to give them the hard-done-by stories they're after.

rovermorris999 said:

number2 said:

I wouldn't blame the government, or the individuals in the main.

We can't mitigate all risk, some we just have to accept.

However, we aren't at that stage yet, things aren't that bad. Rates are only at 4.25pc.

There's a lot of whining certainly, from individuals cherry picked by the media to give them the hard-done-by stories they're after.

With inflation at 9-10% that 4.25% is a negative rate. As long as your income increase keeps up with the rate you're paying then no problem.We can't mitigate all risk, some we just have to accept.

However, we aren't at that stage yet, things aren't that bad. Rates are only at 4.25pc.

There's a lot of whining certainly, from individuals cherry picked by the media to give them the hard-done-by stories they're after.

We can't always be getting richer or be insulated from economic events. However, that appears to be what people expect: always having more, and no external events impacting them.

This is a house price thread so that's my focus here, not people on NMW or unable to work, in 'social' housing who are struggling with cost of living.

classicaholic said:

I feel sorry for the people with 500k+ mortgages when their 1% fixed deals come to an end & suddenly they are faced with 5 or more % deals, it’s going to hurt finding an extra £1600 - 2000 month. It’s not the people buying the houses fault, I blame the government for making money so cheap for the last 10 years, mind you I am bitter because I had to pay 10% for my 1st mortgage!

When you've realised the link between interest rates and house prices, give that some more thought.z4RRSchris said:

i have a small Edwardian terrace in z3/4, got a 650k mortgage

I gather from your posts here that you're doing quite well, but a £650k mortgage makes me personally quite nervous! (I'm an 2022/23 additional rate tax payer with a £250k mortgage).Perhaps similar to the poster above re his daughter and her husband--I think I'm too risk averse to climb to those multiples!

We're seeing prices here (East Anglia) generally hold-- one particular property in our village was advertised at £695k before lockdown and has just sold for over £900k with no obvious additions. Another was advertised for £1M and sold within two weeks. I guess there's still demand for 'special' places, perhaps the bottom/mid tiers things are quite different.

Edited by LittleBigPlanet on Thursday 6th April 11:59

Assuming you mean 45% rate then yes. Very risk averse. You also have something that Chris and myself don’t have so much - the luxury of choice - there aren’t any houses in London you’d want to live in that cost under £1m. So you either save up for years on end while prices run away from your saving rate or you borrow it and let wage inflation eat the debt.

The other aspect is that for many in London that’s not where they will stay longer term. In that regard it is really just a savings account free of CGT that classically rises a bit more than most areas and gains can be realised when we move out - and 99% of places are cheaper so it kind of makes sense.

My mortgage 750k but I wish I’d borrowed more tbh

The other aspect is that for many in London that’s not where they will stay longer term. In that regard it is really just a savings account free of CGT that classically rises a bit more than most areas and gains can be realised when we move out - and 99% of places are cheaper so it kind of makes sense.

My mortgage 750k but I wish I’d borrowed more tbh

Edited by okgo on Friday 31st March 09:23

Edited by okgo on Friday 31st March 09:27

okgo said:

Assuming you mean 45% rate then yes. Very risk averse. You also have something that Chris and myself don’t have so much - the luxury of choice - there aren’t any houses in London you’d want to live in that cost under £1m. So you either save up for years on end while prices run away from your saving rate or you borrow it and let wage inflation eat the debt.

The other aspect is that for many in London that’s not where they will stay longer term. In that regard it is really just a savings account free of CGT that classically rises a bit more than most areas and gains can be realised when we move out - and 99% of places are cheaper so it kind of makes sense.

My mortgage 750k but I wish I’d borrowed more tbh

Yes, the additional rate being 45% at the 2022/23 threshold. We bought about six years ago in what could be our forever home (will extend next year pushing mortgage up by £100k). The other aspect is that for many in London that’s not where they will stay longer term. In that regard it is really just a savings account free of CGT that classically rises a bit more than most areas and gains can be realised when we move out - and 99% of places are cheaper so it kind of makes sense.

My mortgage 750k but I wish I’d borrowed more tbh

Edited by okgo on Friday 31st March 09:23

Edited by okgo on Friday 31st March 09:27

Your points about choice (and a forever home in London) are spot on--many of my friends have established themselves with careers in London (I commute) with a view to moving further afield in the near term (some have already done this with the flexibility wrt WFH).

A £750k mortgage makes me wince!

LittleBigPlanet said:

Yes, the additional rate being 45% at the 2022/23 threshold. We bought about six years ago in what could be our forever home (will extend next year pushing mortgage up by £100k).

Your points about choice (and a forever home in London) are spot on--many of my friends have established themselves with careers in London (I commute) with a view to moving further afield in the near term (some have already done this with the flexibility wrt WFH).

A £750k mortgage makes me wince!

I'd suggest you're quite risk averse if your mortgage multiple has to be <2x gross salary to make you feel comfortable. Mine is much higher than that as a multiple of salary.Your points about choice (and a forever home in London) are spot on--many of my friends have established themselves with careers in London (I commute) with a view to moving further afield in the near term (some have already done this with the flexibility wrt WFH).

A £750k mortgage makes me wince!

Nationwide announcing the biggest annual decline in house prices since 2009 at 3.1% today. We'd need about 7 years of this to erode the increases of the last couple of years!

DoubleSix said:

The inflationary issues, and attempts to control them, have been a global phenomenon. Placing these issues at the door of UK Gov when unable to meet personal obligations is frankly to deny ones own agency.

I think Turkey has had over 50% inflation rates last two years, and it's not on that chart.Edited by DoubleSix on Friday 31st March 08:36

U.K. is not uniquely placed on house price index in comparison to Europe, loads of countries have more multiples than earnings at the moment. (Holland, Belgium, Sweden and etc..)

Nationwide are showing another fall.

https://www.bbc.co.uk/news/business-65135405

Still a long way above March 2020 prices though.

https://www.bbc.co.uk/news/business-65135405

Still a long way above March 2020 prices though.

JagLover said:

Nationwide are showing another fall.

https://www.bbc.co.uk/news/business-65135405

Still a long way above March 2020 prices though.

This is the thing . https://www.bbc.co.uk/news/business-65135405

Still a long way above March 2020 prices though.

Question is do we think they are heading back to those levels ?

GT3Manthey said:

This is the thing .

Question is do we think they are heading back to those levels ?

Prices were still not great from an affordability perspective in March 2020, but I would regard the surge since then as being driven by artificial factors, Stamp duty holiday + QE, so we may well see a reversion to close to that level. Question is do we think they are heading back to those levels ?

JagLover said:

okgo said:

When’s this data from again? Is it lagging data from land registry or?

Think it is based on mortgage offers in month, adjusted for property mix and seasonality. Will exclude houses with cash buyers. DoubleSix said:

Why?

It’s not the governments fault if people haven’t looked beyond the end of their own nose and notionally stress tested their household finances against a different economic landscape.

People who borrow are adults last I checked. The warnings when taking on a mortgage are tediously repetitive when last I checked.

I couldn’t disagree with your statement more.

People didn't have much choice though - vast majority are buying for somewhere to live, not as an investment. I guess some will have stretched themselves unncessarily and bought a house bigger than their families needs, but most will have bought the cheapest place that just about fits their needs. Maybe there's an element of sheep mentality with it - following the herd and ignoring the prospect of rapidly increasing interest rates.It’s not the governments fault if people haven’t looked beyond the end of their own nose and notionally stress tested their household finances against a different economic landscape.

People who borrow are adults last I checked. The warnings when taking on a mortgage are tediously repetitive when last I checked.

I couldn’t disagree with your statement more.

The problem has been caused by low interest rates over the last 10-12 years. It's allowed people to afford bigger mortgages which has then pushed up house prices. That's the governments fault for keeping interest rates too low for too long. The only way to get it back under control is higher interest rates, but that's going to be a hard pill to swallow for some.

greggy50 said:

Sheepshanks said:

I don;t know what's reasonable to spend?

My daughter and her husband are a little above average - total gross income about £90K. Got two kids at primary school, so clear of nursery fees etc.

They're the very oppisite of the "leased white Audi" brigade many on here like to cite - his car is 14yrs old, and hers is 9. No Sky TV or latest phone etc.

They have £135K mortgage on a fix for a while (might be 5yrs, done at a lowish rate). House maybe £250K.

I asked if they were thinking about moving up and they were absolutely horrified that I'd think they should even consider it.

That does seem a tiny mortgage for that wage if they are young.My daughter and her husband are a little above average - total gross income about £90K. Got two kids at primary school, so clear of nursery fees etc.

They're the very oppisite of the "leased white Audi" brigade many on here like to cite - his car is 14yrs old, and hers is 9. No Sky TV or latest phone etc.

They have £135K mortgage on a fix for a while (might be 5yrs, done at a lowish rate). House maybe £250K.

I asked if they were thinking about moving up and they were absolutely horrified that I'd think they should even consider it.

We took on £365k mortgage against a £432k house when I was 29 and my wife was 26 with a similar joint income as I backed myself to progress at the time.

18 months later thats more like £120k joint now and if it wasnt for a bloody expensive wedding we are paying off we would be very comfortable especially as my student loan is about to go which costs me £400pm currently.

No kids however...

Of relevance to house prices, though, is a worthwhile step up for them is going to take them into the sort of price bracket you're in - so perhaps a £300K mortgage. Understandably that probably does seem bonkers to them.

Gassing Station | News, Politics & Economics | Top of Page | What's New | My Stuff