Pensions Investments – Gilt Funds

Discussion

After some discussion on another thread on here, regarding who actually knows what funds their pension is invested in, I finally got my backside around to actually investigating what is in mine.

To this point I’ve had no interactive management over the pension, it’s a stakeholder plan I entered via my work and aside from checking an initial box regarding my attitude to risk I’ve left it to do its thing.

Currently the investment is spread across 2 funds; Fund A [~85% of total pot] bought in to up to the end of the 2014 tax year, Fund B [~15% of pot] bought in to since then. As I expected before checking it out, with the market volatility over recent months, its not been a great year. In fact, the return is negative this year against double digit returns in every previous year.

Hence why I’m curious about Gilts. Analysing the funds available to buy through the plan, Gilts are fairing much better than my current funds.

I am not considering selling the other funds [and thereby incurring fees to transfer them], rather considering swapping to buying in to Gilts for some months until the stock market calms down a bit.

The issue I have is the Gilt fund I’m looking at has much stronger returns than the %s I can see quoted for what Gilts are currently being sold at. Over the past 5 years the same fund has averaged ~13%, again, higher than Gilts have been sold at.

Is there anywhere I can educate myself a bit more about Gilts and their index linking?

[My apologies in advance if I’ve missed an already running pension thread this could have been placed in, didn’t see one on the search]

To this point I’ve had no interactive management over the pension, it’s a stakeholder plan I entered via my work and aside from checking an initial box regarding my attitude to risk I’ve left it to do its thing.

Currently the investment is spread across 2 funds; Fund A [~85% of total pot] bought in to up to the end of the 2014 tax year, Fund B [~15% of pot] bought in to since then. As I expected before checking it out, with the market volatility over recent months, its not been a great year. In fact, the return is negative this year against double digit returns in every previous year.

Hence why I’m curious about Gilts. Analysing the funds available to buy through the plan, Gilts are fairing much better than my current funds.

| Fund | YTD | Past 6 Mnths | Past 12 Mnths |

| A | -3.84% | -3.83% | 3.05% |

| B | -2.08% | -5.58% | -3.99% |

| 15Yr UK Index Gilt | 6.83% | 7.30% | 5.51 |

I am not considering selling the other funds [and thereby incurring fees to transfer them], rather considering swapping to buying in to Gilts for some months until the stock market calms down a bit.

The issue I have is the Gilt fund I’m looking at has much stronger returns than the %s I can see quoted for what Gilts are currently being sold at. Over the past 5 years the same fund has averaged ~13%, again, higher than Gilts have been sold at.

Is there anywhere I can educate myself a bit more about Gilts and their index linking?

[My apologies in advance if I’ve missed an already running pension thread this could have been placed in, didn’t see one on the search]

All data is through the fund unit values tables I've downloaded from Fidelity's planviewer website and charted in excel.

Gilt fund I'm looking at is "FIDELITY BLACKROCK OVER 15 YEARS UK GILT INDEX FUND - CLASS 4."

Also looked at "FIDELITY BLACKROCK OVER 5 YEARS INDEX LINKED GILT FUND - CLASS 4" but whilst its growth over the 5 year term is only ~4% lower (61.x vs 57.x iirc, don't have my excel sheet to hand), it has performed significantly less well in the last year.

My 2012-2015 annual statements showed returns in the 14-25% region. I don't expect that out of any Gilt fund but it seems a decent way of offsetting this tax year's current -5.7%

Gilt fund I'm looking at is "FIDELITY BLACKROCK OVER 15 YEARS UK GILT INDEX FUND - CLASS 4."

Also looked at "FIDELITY BLACKROCK OVER 5 YEARS INDEX LINKED GILT FUND - CLASS 4" but whilst its growth over the 5 year term is only ~4% lower (61.x vs 57.x iirc, don't have my excel sheet to hand), it has performed significantly less well in the last year.

My 2012-2015 annual statements showed returns in the 14-25% region. I don't expect that out of any Gilt fund but it seems a decent way of offsetting this tax year's current -5.7%

Edited by emicen on Tuesday 2nd February 18:07

Here's a basic explanation of Gilts. http://moneyweek.com/videos/how-gilts-work/ Let me know if you're looking for something more detailed/complex.

Gilt funds have delivered strong returns in recent years as interest rates have stayed "lower for longer" than anyone expected. The oft-repeated advice not to base investment decisions on past performance applies here as the starting conditions for Gilt investment today are very different to those of 5 years ago. Here's one take on the outlook for returns going forward: http://www.morningstar.co.uk/uk/news/146176/gilts-...

This is an interesting subject that it is worth your time and effort to read around.

Gilt funds have delivered strong returns in recent years as interest rates have stayed "lower for longer" than anyone expected. The oft-repeated advice not to base investment decisions on past performance applies here as the starting conditions for Gilt investment today are very different to those of 5 years ago. Here's one take on the outlook for returns going forward: http://www.morningstar.co.uk/uk/news/146176/gilts-...

This is an interesting subject that it is worth your time and effort to read around.

Edited by iantr on Tuesday 2nd February 19:24

How close are you to retirement OP? You would only usually start putting significant sums into gilt funds in the ten years or so before to retirement as they are relatively 'safe' investments that tend to track annuity prices (the latter being less of a concern nowadays of course). If you are further out from retirement than that then you're likely to be better off staying the course with some riskier (but potentially higher yielding) funds.

It seems like it's sort of unfortunate that you've started to take an interest in your pension investments at a time when they happen to have not done too well recently. A lot of people do think along the lines of 'equities have done well for a few years, I'll invest in them', and then if they have a bad period think 'equities aren't doing too well now, I'll take my money out and put it into something safer that's done better recently'. Then once equities have already risen again put it back there. The trouble with this is you never 'buy the dip', and never sell at the top either. The best thing to do IMO is to find a fund that has the right level of risk for you, which has as low a charge as possible, and then (other than banging in the contributions regularly through thick and thin), essentially forget about it until a predetermined point in the future, such as ten years before your intended retirement date.

It is undoubtedly good to take an interest in your pension investments, but it's a very long term thing so you don't want to start fretting about every twist and turn of the markets.

It seems like it's sort of unfortunate that you've started to take an interest in your pension investments at a time when they happen to have not done too well recently. A lot of people do think along the lines of 'equities have done well for a few years, I'll invest in them', and then if they have a bad period think 'equities aren't doing too well now, I'll take my money out and put it into something safer that's done better recently'. Then once equities have already risen again put it back there. The trouble with this is you never 'buy the dip', and never sell at the top either. The best thing to do IMO is to find a fund that has the right level of risk for you, which has as low a charge as possible, and then (other than banging in the contributions regularly through thick and thin), essentially forget about it until a predetermined point in the future, such as ten years before your intended retirement date.

It is undoubtedly good to take an interest in your pension investments, but it's a very long term thing so you don't want to start fretting about every twist and turn of the markets.

ellroy said:

Be wary of gilts at the present time.

As, and when, interest rates climb the capital values have an inverse relationship..........

As, and when, interest rates climb the capital values have an inverse relationship..........

+1

Pension funds like and have regulatory pressure to buy gilts, because the complete return is known long in advance.

However, the history shows they have not beaten equities, and the non indexed gilts can be a disaster when inflation rises.

Someone once said, 'Lending to a government, is akin to tearing up £5 notes'.

Last year a gilt was redeemed, 3.5% War Loan. If someone bought £100 worth in 1918, that would have almost been enough to buy a small house at the time. Interest would have been paid annually to the holder (initially 5%, but later reduced to 3.5%), however last year, all that they received back was £100.

There you are, inflation can be the killer of an investment.

Edited by Jon39 on Thursday 4th February 08:14

Thanks for the replies guys.

Having had a read of the article on Gilt returns and done some more data research, I’m a bit more cautious of a knee jerk reaction.

I’ve previously been guilty in share dabbling of bailing out on the down rather than buying more stock to capitalize on the rebound, which somewhat feels like the position I’m in just now.

Comparing both funds against the FTSE 100, they haven’t taken as bad a battering as the market as a whole has. Without knowing the underlying diversity/makeup of investments its hard to know/predict/guess what the future holds sadly.

I’m 33, so a little young for playing it safe, plus safe isn’t really in my nature

I’m not expecting interest rates to go up much if at all this year, but acknowledge it will inevitably come. At that point it would cost me to trade out of Gilt based funds incurring costs so using them as a hedge wouldn’t be as effective. Drilling in to the data a bit further, the 15yr Gilt fund I was looking at has only really got the 5 year returns it has due to strong 2011-2012 and 2014-2015 tax years, other years it hasn’t been overwhelming

Doing the numbers over the 5 year period I’ve had the pension; the larger fund is in the top 15% of the 40 funds available, the lesser value fund is in the bottom 10%

Time to read some books and educate myself about pension funds a bit more I think. I'm looking at upping my contributions going forward and I think no matter what, the pay ins will be getting spread across more funds, even if it is just 2 or 3.

Having had a read of the article on Gilt returns and done some more data research, I’m a bit more cautious of a knee jerk reaction.

I’ve previously been guilty in share dabbling of bailing out on the down rather than buying more stock to capitalize on the rebound, which somewhat feels like the position I’m in just now.

Comparing both funds against the FTSE 100, they haven’t taken as bad a battering as the market as a whole has. Without knowing the underlying diversity/makeup of investments its hard to know/predict/guess what the future holds sadly.

I’m 33, so a little young for playing it safe, plus safe isn’t really in my nature

I’m not expecting interest rates to go up much if at all this year, but acknowledge it will inevitably come. At that point it would cost me to trade out of Gilt based funds incurring costs so using them as a hedge wouldn’t be as effective. Drilling in to the data a bit further, the 15yr Gilt fund I was looking at has only really got the 5 year returns it has due to strong 2011-2012 and 2014-2015 tax years, other years it hasn’t been overwhelming

Doing the numbers over the 5 year period I’ve had the pension; the larger fund is in the top 15% of the 40 funds available, the lesser value fund is in the bottom 10%

Time to read some books and educate myself about pension funds a bit more I think. I'm looking at upping my contributions going forward and I think no matter what, the pay ins will be getting spread across more funds, even if it is just 2 or 3.

emicen said:

I’m 33, so a little young for playing it safe, plus safe isn’t really in my nature

Well then you definitely don't want to be in gilt funds! I'm only a couple of years older than you and FWIW my approach has been to simply find an equity tracker fund with rock bottom fees and bung everything into that, probably to be revisited in ten years or so. It isn't nice to see the value of my investment tanking at the moment but then I just think of how many more units I'm buying each month with my contributions - same as with the employer sharesave schemes I'm in. Bit of an update, doubled my pension contributions going forwards based on some projections and the realization, I need to stop ignoring pension provision entirely, even if I do have other plans on funding at least part of my retirement.

The fund I was being invested in to, I have stuck with [sort of]. Its bottom 10% performance in terms of growth possibly reflects a certain element of stability within the fund, it has not taken as big a bath as most have in the last 3 months. Some reading in to what exactly my “multi asset allocator growth fund” is in to revealed;

- 58% equities [UK and North America elements being over 40%, the rest mostly Europe and Japan]

- 15% in commodities [no further detail]

- 13.5% in UK and global fixed interest bonds

- 12% cash

- 8% property

The cash element isn’t very appealing but there is at least quite a broad spread of underlying assets which seems sensible.

When I said I have “sort of” stuck with it, I’ve re-distributed how future contributions will be invested, spread evenly across 5 funds; the aforementioned multi asset fund, a global real estate fund with some cash and stocks also held, a UK equity fund and 2 North American equity funds.

Criteria for selection? My personal view/feeling/guess at how the underlying stocks in each fund will probably fair going forwards and combining that with looking at a lot of data for their quarterly performance for the last 5 years and how they have been doing this year. Global real estate fund isn’t stellar in terms of past 3 years performance, but it also hasn’t shrunk this year which is something no other available fund [within my provider’s selection] can say unless it is purely a cash / Gilt / corporate bond affair.

So, now I’ll just have to see how the markets perform…

The fund I was being invested in to, I have stuck with [sort of]. Its bottom 10% performance in terms of growth possibly reflects a certain element of stability within the fund, it has not taken as big a bath as most have in the last 3 months. Some reading in to what exactly my “multi asset allocator growth fund” is in to revealed;

- 58% equities [UK and North America elements being over 40%, the rest mostly Europe and Japan]

- 15% in commodities [no further detail]

- 13.5% in UK and global fixed interest bonds

- 12% cash

- 8% property

The cash element isn’t very appealing but there is at least quite a broad spread of underlying assets which seems sensible.

When I said I have “sort of” stuck with it, I’ve re-distributed how future contributions will be invested, spread evenly across 5 funds; the aforementioned multi asset fund, a global real estate fund with some cash and stocks also held, a UK equity fund and 2 North American equity funds.

Criteria for selection? My personal view/feeling/guess at how the underlying stocks in each fund will probably fair going forwards and combining that with looking at a lot of data for their quarterly performance for the last 5 years and how they have been doing this year. Global real estate fund isn’t stellar in terms of past 3 years performance, but it also hasn’t shrunk this year which is something no other available fund [within my provider’s selection] can say unless it is purely a cash / Gilt / corporate bond affair.

So, now I’ll just have to see how the markets perform…

emicen said:

Bit of an update, doubled my pension contributions going forwards based on some projections and the realization, I need to stop ignoring pension provision entirely, even if I do have other plans on funding at least part of my retirement.

The fund I was being invested in to, I have stuck with [sort of]. Its bottom 10% performance in terms of growth possibly reflects a certain element of stability within the fund, it has not taken as big a bath as most have in the last 3 months. Some reading in to what exactly my “multi asset allocator growth fund” is in to revealed;

- 58% equities [UK and North America elements being over 40%, the rest mostly Europe and Japan]

- 15% in commodities [no further detail]

- 13.5% in UK and global fixed interest bonds

- 12% cash

- 8% property

The cash element isn’t very appealing but there is at least quite a broad spread of underlying assets which seems sensible.

When I said I have “sort of” stuck with it, I’ve re-distributed how future contributions will be invested, spread evenly across 5 funds; the aforementioned multi asset fund, a global real estate fund with some cash and stocks also held, a UK equity fund and 2 North American equity funds.

Criteria for selection? My personal view/feeling/guess at how the underlying stocks in each fund will probably fair going forwards and combining that with looking at a lot of data for their quarterly performance for the last 5 years and how they have been doing this year. Global real estate fund isn’t stellar in terms of past 3 years performance, but it also hasn’t shrunk this year which is something no other available fund [within my provider’s selection] can say unless it is purely a cash / Gilt / corporate bond affair.

So, now I’ll just have to see how the markets perform…

Sounds like you've thought this through and have a plan. At some point you might gain further diversification by adding in some Asian equity exposure, maybe an actively managed fund with a broad regional (incl. Aus) mandate...?The fund I was being invested in to, I have stuck with [sort of]. Its bottom 10% performance in terms of growth possibly reflects a certain element of stability within the fund, it has not taken as big a bath as most have in the last 3 months. Some reading in to what exactly my “multi asset allocator growth fund” is in to revealed;

- 58% equities [UK and North America elements being over 40%, the rest mostly Europe and Japan]

- 15% in commodities [no further detail]

- 13.5% in UK and global fixed interest bonds

- 12% cash

- 8% property

The cash element isn’t very appealing but there is at least quite a broad spread of underlying assets which seems sensible.

When I said I have “sort of” stuck with it, I’ve re-distributed how future contributions will be invested, spread evenly across 5 funds; the aforementioned multi asset fund, a global real estate fund with some cash and stocks also held, a UK equity fund and 2 North American equity funds.

Criteria for selection? My personal view/feeling/guess at how the underlying stocks in each fund will probably fair going forwards and combining that with looking at a lot of data for their quarterly performance for the last 5 years and how they have been doing this year. Global real estate fund isn’t stellar in terms of past 3 years performance, but it also hasn’t shrunk this year which is something no other available fund [within my provider’s selection] can say unless it is purely a cash / Gilt / corporate bond affair.

So, now I’ll just have to see how the markets perform…

Definitely.

The global asset fund has some Japan, Pacific ex-Japan and emerging market equities in it, a total of about 8% of the fund.

The real estate fund has more exposure with Australia, Japan, India and Asia ex-Japan.

There's been some strong results from Australia recently, like their Dominos franchise owner, but wary of how much impact mining has on their whole market at the moment. Similarly, China seems a wobbly prospect. India on the other hand seems quite prosperous. Need to do more research on the various areas before committing to anything.

The global asset fund has some Japan, Pacific ex-Japan and emerging market equities in it, a total of about 8% of the fund.

The real estate fund has more exposure with Australia, Japan, India and Asia ex-Japan.

There's been some strong results from Australia recently, like their Dominos franchise owner, but wary of how much impact mining has on their whole market at the moment. Similarly, China seems a wobbly prospect. India on the other hand seems quite prosperous. Need to do more research on the various areas before committing to anything.

I like the second one, it's pegged against an index of gilt funds so it's a good like for like and I've done well with it. The first is a different gilt proposition so is pegged against something completely different; a medium risk basket of actively managed funds. The second is a very low risk/volatility steady Eddie of about 7 funds, I like it.

Any idea which government organisation is the only public sector occupational pension fund to be invested entirely in gilts..?

Any idea which government organisation is the only public sector occupational pension fund to be invested entirely in gilts..?

iantr said:

The BoE, AICMFP..!

Not actually true...http://www.bankofengland.co.uk/about/documents/hum...

15-20% in non-Gilts for both the Feb '14 and Feb '15 valuations...

Ginge R said:

I like the second one, it's pegged against an index of gilt funds so it's a good like for like and I've done well with it. The first is a different gilt proposition so is pegged against something completely different; a medium risk basket of actively managed funds. The second is a very low risk/volatility steady Eddie of about 7 funds, I like it.

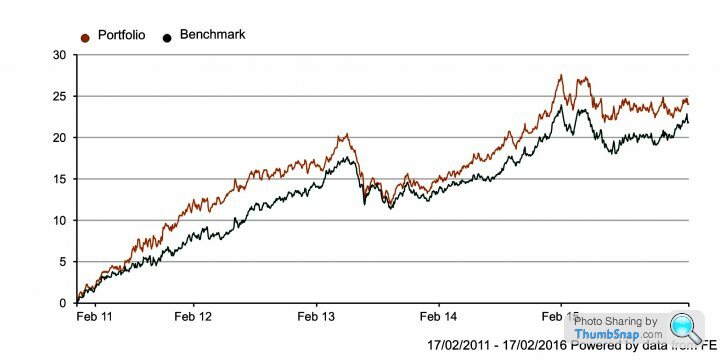

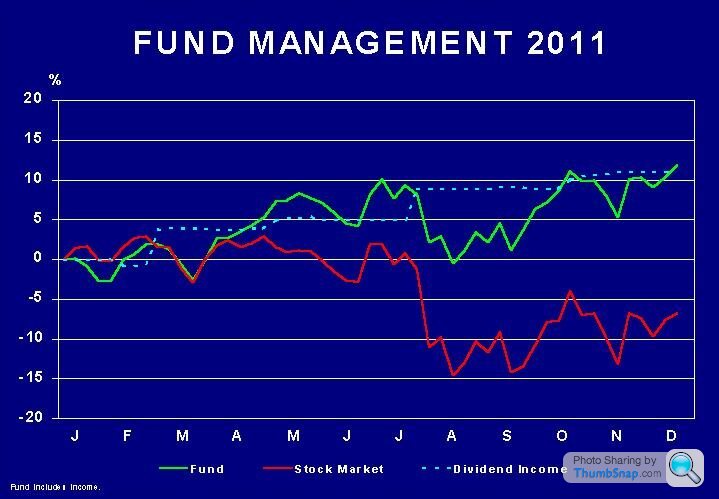

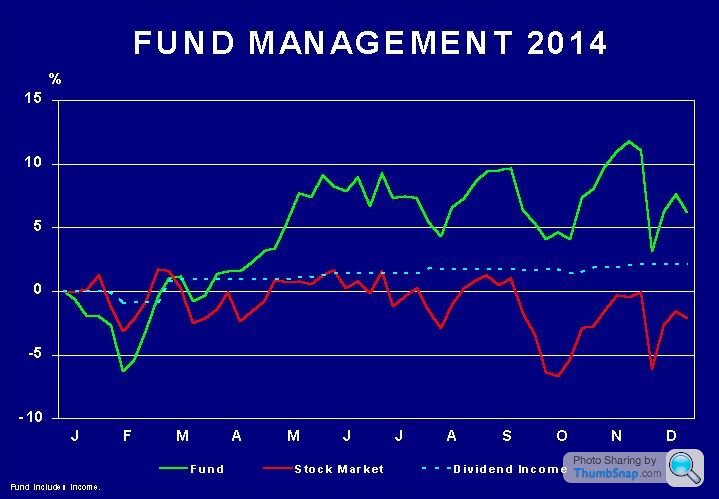

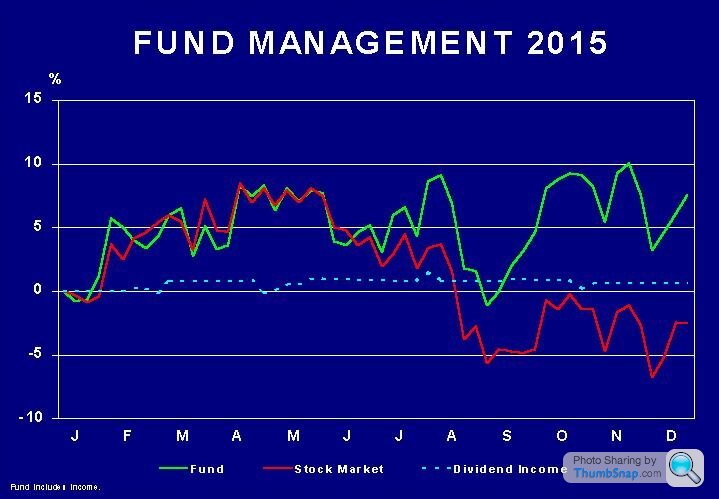

Charts - excellent, always the best way of describing a financial investment story.

I read your 5 year performance as +25%, and the 3 year fund as +20%.

To me, it is the percentage that is important, which I then compare to a widely respected, broad index (FTSE All-Share Index). If you want to you could easily check, but certainly your 3 year performance, and possibly your 5 year may have beaten the All-Share Index.

The use of benchmarks is something that I noticed being used a few years ago. How long this has been going on, I do not know. The sceptical might suggest, that using a suitably benchmark, you could prove black is white.

With Gilts, as has already been mentioned by several contributors, beware when (perhaps if with so much World debt) interest rates begin to rise. History will reveal what happens (inverse relationship with Gilts).

Years ago I did buy Gilts, at a time when it was clear that inflation would be falling. Consequently interest rates also moved down, and so Gilt capital values moved up. Those particular circumstances I think, only became obvious to me on one occasion, so since then I have only invested in equities of large UK businesses.

I do not have 5 year charts, because I treat each calendar year individually, but if you might be interested, here are my charts covering the periods of your own charts.

You can add the percentages to see who won, if you want to.

Best of luck to you, and keep up your interest in the subject.

Edited by Jon39 on Thursday 18th February 20:38

contango said:

Your charts look a little odd to me. You have a definite correlation with the "stock market", but a higher beta.

How many individual stocks do you have in your portfolio compared to your "stock market"?

Normally the stock market and index is made up of many stocks, to have such a close tracking correlation over a multi year period with no doubt fewer selected sample holdings seems incredible.

Maybe I am losing something in the translation of scale of the chart representation?

Impressive performance none the less!

How many individual stocks do you have in your portfolio compared to your "stock market"?

Normally the stock market and index is made up of many stocks, to have such a close tracking correlation over a multi year period with no doubt fewer selected sample holdings seems incredible.

Maybe I am losing something in the translation of scale of the chart representation?

Impressive performance none the less!

Holdings are normally 25 to 30, which mostly have remained unchanged for many years.

Helped by a particular sector, which has gradually become a bigger proportion.

Yes, index made up of many stocks, but with the weighted basis, the biggest companies have far more effect on index movements.

The red line (market) is the FTSE All-Share Index, and you might have noticed the green line includes dividends received during each individual year. Yes I know, the comparison is helped a little by that particular cheat.

The dotted blue line represents percentage change to overall dividend total, based on previous 12 months dividend announcements. You may have noticed the upward blip each spring. Many big companies have a financial year end of 31 December, so announce their finals around now. You will also see how that spring blip has recently become smaller. Not so easy at present for some businesses.

I started this chart system in 1988, prior to that without computers, it would have been impossibly time consuming.

Edited by Jon39 on Thursday 18th February 22:52

Ginge R said:

Jon,

Your graphs; large caps?

I use my gilt portfolios to dampen things down a little sometimes, and to make strategic shifts.

Your graphs; large caps?

I use my gilt portfolios to dampen things down a little sometimes, and to make strategic shifts.

Yes, large caps.

If the green line at the end of each year, is usually ahead of the red, I don't change any of the holdings. Very little work therefore.

Large caps. seem much better for this type of long-term fund, because they usually have the 'fire power' to deal with shocks (financial resources or management changes etc.) The UK large caps. of course mostly do business around the world, so there is built exposure to other countries and currencies. I tend to avoid the cyclical sectors, and this has worked really well during recessions.

Gassing Station | Finance | Top of Page | What's New | My Stuff