Final salary pension - transfer to drawdown?

Discussion

CarlosFandango11 said:

Still not sure what you mean by transfer limit from the above.

Why did you previously say the LTA is less than 850k and above correctly £1m?

I didn't. I said that despite my pension predicting to pay out more pa than Craigs1912 my LTA is less than his £850k.Why did you previously say the LTA is less than 850k and above correctly £1m?

I'm no expert and perhaps someone can tell us if the 'Transfer value' is the same as the LTA. I;m more than happy with my pension arrangements so am not in the position where I want to transfer it to anywhere else.

Everyone's LTA is the same, £1m. You can breach it, and for some people, it can make sense to do so. Take regulated advice on that, though.

Your Transfer Value is a sum that's always moving. It will depend on many factors, e.g:

1. The size of the pension you have earned, sounds daft, but it's the basis for everything!

2. The age it would be payable from (your scheme Normal Retirement Age) and how close you are to it.

3. The percentage/amount of your pension that would be payable to your spouse/partner on your death.

4. The rate(s) by which your pension will increase when it’s paid (or while you’re not receiving a pension from that scheme for example if you’re younger than the scheme’s retirement age).

5. I work with military clients a lot, and on divorce, a partner's AFPS (mil pension scheme) pension will decrease by c5% pa every year it is drawn earlier.

6. The amount of money the scheme has, if it is 'funded'. The scheme may reduce transfer values from time to time.

7. Whether the employer is actually/actively supporting the scheme by allowing higher transfer values.

8. The way a scheme invests its money (the split between equities, gilts, bonds etc, see my post of earlier.).

9. The method of calculation the trustees decide to use (again, see my post earlier today in this thread).

10. Would love to have made ten good ones, can't, sorry.

That list isn't even remotely exhaustive.

Even a Defined Benefit scheme can pull a nasty surprise (BHS etc). Every year (or sometimes less) your Trustees will present you with a Summary Funding Statement (SFS) which purports to show you how the scheme is getting on. It should show the scheme’s assets and it's liabilities (namely the present value of its pension promises). For many schemes this will show they don’t have enough money right now. But don't automatically worry needlessly based on that alone.

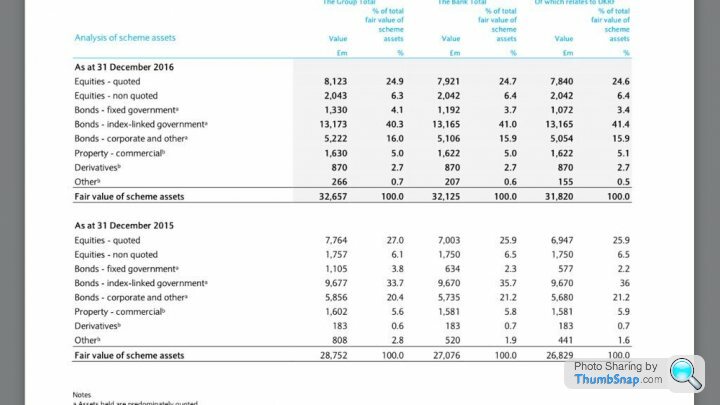

Today, I have been working on a outline transfer summary thought for a client who works for a major bank, which, earlier this year, had to pledge giving £1.25bn to its scheme this year. This certainly doesn't automatically mean the employer is in danger of going bust, if could be partly caused by the way the scheme values its promises which have become more expensive for many schemes over the years. Again, my post of earlier today explains that.

This is a grab of the scheme in question, it has c60% invested in Fixed Interest/Gilt and I'd be amazed if the derivative wasn't based on the same. You'll see how that ratio has increased in the year to December 2016, a definite investment decision to de risk. The plunging yields, and that, will (probably!) have seen a sharp upturn in that particular scheme's transfer values out of proportion to the period, and possibly, to other schemes.

Your Transfer Value is a sum that's always moving. It will depend on many factors, e.g:

1. The size of the pension you have earned, sounds daft, but it's the basis for everything!

2. The age it would be payable from (your scheme Normal Retirement Age) and how close you are to it.

3. The percentage/amount of your pension that would be payable to your spouse/partner on your death.

4. The rate(s) by which your pension will increase when it’s paid (or while you’re not receiving a pension from that scheme for example if you’re younger than the scheme’s retirement age).

5. I work with military clients a lot, and on divorce, a partner's AFPS (mil pension scheme) pension will decrease by c5% pa every year it is drawn earlier.

6. The amount of money the scheme has, if it is 'funded'. The scheme may reduce transfer values from time to time.

7. Whether the employer is actually/actively supporting the scheme by allowing higher transfer values.

8. The way a scheme invests its money (the split between equities, gilts, bonds etc, see my post of earlier.).

9. The method of calculation the trustees decide to use (again, see my post earlier today in this thread).

10. Would love to have made ten good ones, can't, sorry.

That list isn't even remotely exhaustive.

Even a Defined Benefit scheme can pull a nasty surprise (BHS etc). Every year (or sometimes less) your Trustees will present you with a Summary Funding Statement (SFS) which purports to show you how the scheme is getting on. It should show the scheme’s assets and it's liabilities (namely the present value of its pension promises). For many schemes this will show they don’t have enough money right now. But don't automatically worry needlessly based on that alone.

Today, I have been working on a outline transfer summary thought for a client who works for a major bank, which, earlier this year, had to pledge giving £1.25bn to its scheme this year. This certainly doesn't automatically mean the employer is in danger of going bust, if could be partly caused by the way the scheme values its promises which have become more expensive for many schemes over the years. Again, my post of earlier today explains that.

This is a grab of the scheme in question, it has c60% invested in Fixed Interest/Gilt and I'd be amazed if the derivative wasn't based on the same. You'll see how that ratio has increased in the year to December 2016, a definite investment decision to de risk. The plunging yields, and that, will (probably!) have seen a sharp upturn in that particular scheme's transfer values out of proportion to the period, and possibly, to other schemes.

Gassing Station | Finance | Top of Page | What's New | My Stuff