Intelligent Money - your investment questions answered

Discussion

No Res Dogs, no. It's a kinda nickname.

Anyhoo. I'm 55 in Aug, and no SIPP wrapper thing, just plain old pension stuff (not great) tbh but plan to work into 70's (I run a small digital agency) as I love what i do. Small mortgage, quite a small life, kids gone. Only recently had any "spare" money.

Anyhoo. I'm 55 in Aug, and no SIPP wrapper thing, just plain old pension stuff (not great) tbh but plan to work into 70's (I run a small digital agency) as I love what i do. Small mortgage, quite a small life, kids gone. Only recently had any "spare" money.

I've spent the last few days reading this thread beginning to end (OK I skimmed a few bits  ) and it's certainly provided me food for thought.

) and it's certainly provided me food for thought.

I've recently had a review with my IFA and he's recommended consolidating my 5 group pension plans from previous employers and investing them into a SIPP. There's a charge to this plus an ongoing fee (plus platform and fund fees). For some reason it just didn't sit right and didn't feel like value. Once again PH has delivered some excellent insights and has confirmed my initial thoughts that it seemed a bit steep. Don't get me wrong, the IFA has provided some decent advice and got my poorly performing investments on track over the last 5 years but reviews have been few and far between plus I haven't received any actually retirement planning which has been mentioned on here a number of times.

Thanks to everyone's input on this thread, I have fired off an email to Nik this afternoon to understand what IM can help me with.

) and it's certainly provided me food for thought. I've recently had a review with my IFA and he's recommended consolidating my 5 group pension plans from previous employers and investing them into a SIPP. There's a charge to this plus an ongoing fee (plus platform and fund fees). For some reason it just didn't sit right and didn't feel like value. Once again PH has delivered some excellent insights and has confirmed my initial thoughts that it seemed a bit steep. Don't get me wrong, the IFA has provided some decent advice and got my poorly performing investments on track over the last 5 years but reviews have been few and far between plus I haven't received any actually retirement planning which has been mentioned on here a number of times.

Thanks to everyone's input on this thread, I have fired off an email to Nik this afternoon to understand what IM can help me with.

Edited by SausageBap on Wednesday 26th February 16:46

MrOrange said:

No Res Dogs, no. It's a kinda nickname.

Anyhoo. I'm 55 in Aug, and no SIPP wrapper thing, just plain old pension stuff (not great) tbh but plan to work into 70's (I run a small digital agency) as I love what i do. Small mortgage, quite a small life, kids gone. Only recently had any "spare" money.

Shame, I had a great story to tell about that! Anyhoo. I'm 55 in Aug, and no SIPP wrapper thing, just plain old pension stuff (not great) tbh but plan to work into 70's (I run a small digital agency) as I love what i do. Small mortgage, quite a small life, kids gone. Only recently had any "spare" money.

You have mail back.

SausageBap said:

I've spent the last few days reading this thread beginning to end (OK I skimmed a few bits ) and it's certainly provided me food for thought.

I've recently had a review with my IFA and he's recommended consolidating my 5 group pension plans from previous employers and investing them into a SIPP. There's a charge to this plus an ongoing fee (plus platform and fund fees). For some reason it just didn't sit right and didn't feel like value. Once again PH has delivered some excellent insights and has confirmed my initial thoughts that it seemed a bit steep. Don't get me wrong, the IFA has provided some decent advice and got my poorly performing investments on track over the last 5 years but reviews have been few and far between plus I haven't received any actually retirement planning which has been mentioned on here a number of times.

Thanks to everyone's input on this thread, I have fired off an email to Nik this afternoon to understand what IM can help me with.

Thank you for taking the time to do so, I am glad it was helpful!) and it's certainly provided me food for thought. I've recently had a review with my IFA and he's recommended consolidating my 5 group pension plans from previous employers and investing them into a SIPP. There's a charge to this plus an ongoing fee (plus platform and fund fees). For some reason it just didn't sit right and didn't feel like value. Once again PH has delivered some excellent insights and has confirmed my initial thoughts that it seemed a bit steep. Don't get me wrong, the IFA has provided some decent advice and got my poorly performing investments on track over the last 5 years but reviews have been few and far between plus I haven't received any actually retirement planning which has been mentioned on here a number of times.

Thanks to everyone's input on this thread, I have fired off an email to Nik this afternoon to understand what IM can help me with.

Your IFA was always going to make such a recommendation, as they cannot usually earn from you otherwise.

Granted, there needs to be a reason (to make such a recommendation), but from my experience any reason works for them (though not necessarily you).

I am glad to hear your IFA has provided you with some good advice, but they don't actually manage your money. They simply select providers (such as ourselves) to look after this for them and you.

If reviews and financial planning have been few and far between then you are paying for something you are not getting.

Of course there may be other benefits/advantages you receive from you IFA, it sounds as though this is not the case though.

Please post more here or contact Nik (nik.burrows@intelligentmoney.com) or me (just PM me) and we will assist in any way we can, at no charge and with no obligation whatsoever).

Cheers

Julian

gt3rswp said:

@Julian/Nik - how long does to take to execute a switch between funds? Also - is there a phone app, or just the website for now to track SIPP etc?

Many thanks

Internally it is usually 24 hours, but can be up to 48 hours.Many thanks

Externally (moving fund to us) then it is up to the whim of your current investment provide.

Some are quick and some drag it out.

If you give me more details I can give you a more detailed response.

PM me if you prefer.

b hstewie said:

hstewie said:

hstewie said: Julian this isn't a trick question but is there a reason that none of the graphs for PH equity appear to have a legend against them whilst the others do?

Yes, there is a very good reason!I used my own dashboard to create the IM graphs, so I cut out the right hand side, as this would show the amount of money I have invested in the portfolio.

I think this is a private matter and I don't want (or need) to show off!

Good point though. I will get the team to replicate this with in the same format.

I was just doing this using live data fields that were immediately at hand.

Cheers

Edited to add, this is why I also put the performance data under each one.

JulianPH said:

Thank you for taking the time to do so, I am glad it was helpful!

Your IFA was always going to make such a recommendation, as they cannot usually earn from you otherwise.

Granted, there needs to be a reason (to make such a recommendation), but from my experience any reason works for them (though not necessarily you).

I am glad to hear your IFA has provided you with some good advice, but they don't actually manage your money. They simply select providers (such as ourselves) to look after this for them and you.

If reviews and financial planning have been few and far between then you are paying for something you are not getting.

Of course there may be other benefits/advantages you receive from you IFA, it sounds as though this is not the case though.

Please post more here or contact Nik (nik.burrows@intelligentmoney.com) or me (just PM me) and we will assist in any way we can, at no charge and with no obligation whatsoever).

Cheers

Julian

Thanks Julian, I've sent an email to Nik and look forward to discussing it further with him. Your IFA was always going to make such a recommendation, as they cannot usually earn from you otherwise.

Granted, there needs to be a reason (to make such a recommendation), but from my experience any reason works for them (though not necessarily you).

I am glad to hear your IFA has provided you with some good advice, but they don't actually manage your money. They simply select providers (such as ourselves) to look after this for them and you.

If reviews and financial planning have been few and far between then you are paying for something you are not getting.

Of course there may be other benefits/advantages you receive from you IFA, it sounds as though this is not the case though.

Please post more here or contact Nik (nik.burrows@intelligentmoney.com) or me (just PM me) and we will assist in any way we can, at no charge and with no obligation whatsoever).

Cheers

Julian

Good thread by the way, full of genuinely useful information IM related or not.

leef44 said:

Thank you Julian for offering free chat with Nik.

I had a chat with him today. He's been great, providing independent review of my financial investment position.

I'm looking forward to British GT Championship and just emailed him with my jacket sizes.

Thank you for wonderful service

No problem. The great thing about Nik is that he will just tell you as it stands, not try and sell you IM.I had a chat with him today. He's been great, providing independent review of my financial investment position.

I'm looking forward to British GT Championship and just emailed him with my jacket sizes.

Thank you for wonderful service

He is already self made and only does this because he enjoys it.

He is therefore completely neutral and just says it as it is. Others here will vouch for that.

We try to be refreshing (as the FCA called us)!

Julian

SausageBap said:

Thanks Julian, I've sent an email to Nik and look forward to discussing it further with him.

Good thread by the way, full of genuinely useful information IM related or not.

No problem, Nik will certainly be able to assist regardless of whether you decide to become Private Client or not.Good thread by the way, full of genuinely useful information IM related or not.

It is always about you, not us.

Cheers

Julian

JulianPH said:

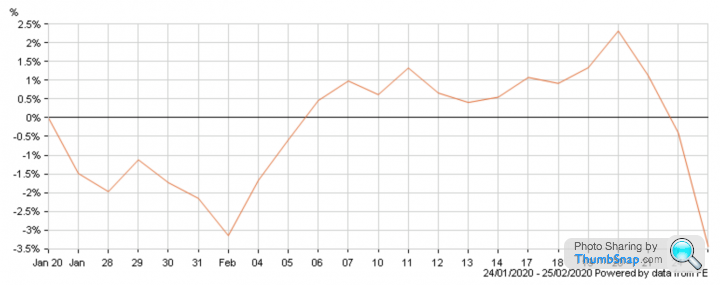

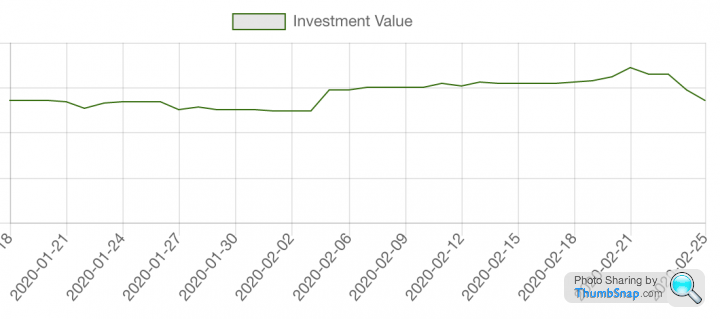

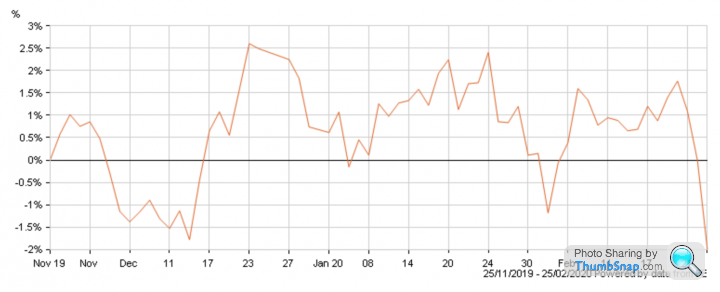

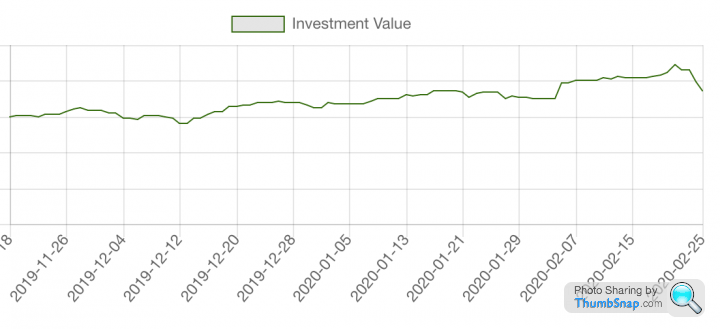

PH Equity Update

Given that markets have taken a bit of a pounding over the last few days and this has obviously impacted on equity investment, including PH Equity, I thought it would be a goo idea to revisit the 1 month and 3 month performance and volitility figures I posted before these falls.

My aim here is to factor in the last few days where things have not been quite so rosy and therefore include some nasty times, rather than just the good.

There is no getting away from the fact PH Equity (like all other equity investments) has taken a hit over the last few days, I just wanted to put this into perspective when compared to Fundsmith and Lindsell Train:

1 Month

Fundsmith Equity

3.4% Down

Lindsell Train Global Equity

4.3% Down

PH Equity

0.17% Up

3 Months

Fundsmith Equity

3.1% Up

Lindsell Train

2% Down

PH Equity

7.53% Up

PS I have no idea whatsoever why when I select 3 months it actually adds on a few more days, but have adjusted the IM data to match.

Cheers

Julian

This is panful for me as I have Fundsmith and LT in my portfolio.... il be speaking to Nik shortly about moving across :-)Given that markets have taken a bit of a pounding over the last few days and this has obviously impacted on equity investment, including PH Equity, I thought it would be a goo idea to revisit the 1 month and 3 month performance and volitility figures I posted before these falls.

My aim here is to factor in the last few days where things have not been quite so rosy and therefore include some nasty times, rather than just the good.

There is no getting away from the fact PH Equity (like all other equity investments) has taken a hit over the last few days, I just wanted to put this into perspective when compared to Fundsmith and Lindsell Train:

1 Month

Fundsmith Equity

3.4% Down

Lindsell Train Global Equity

4.3% Down

PH Equity

0.17% Up

3 Months

Fundsmith Equity

3.1% Up

Lindsell Train

2% Down

PH Equity

7.53% Up

PS I have no idea whatsoever why when I select 3 months it actually adds on a few more days, but have adjusted the IM data to match.

Cheers

Julian

just wanted to say that yes the PH Equity has dropped but its still way higher then November.

as has most funds. Hoping they will bounce back over the next week/month/year/5 years.

Just to highlight the funds in the Index 20 has increased which was a silver lining.

as has most funds. Hoping they will bounce back over the next week/month/year/5 years.

Just to highlight the funds in the Index 20 has increased which was a silver lining.

Edited by superlightr on Thursday 27th February 10:06

Kingdom35 said:

This is panful for me as I have Fundsmith and LT in my portfolio.... il be speaking to Nik shortly about moving across :-)

Their long term performance has been impressive though, so don't beat yourself up to much! The issue is they have taken far higher levels of volatility for lower returns than PH Equity.

You may be best not to read the reply I am about to post to Superlightr though!

JulianPH said:

Their long term performance has been impressive though, so don't beat yourself up to much!

The issue is they have taken far higher levels of volatility for lower returns than PH Equity.

You may be best not to read the reply I am about to post to Superlightr though!

hehe - just checked the dashboard and see the index 20 is down a bit now The issue is they have taken far higher levels of volatility for lower returns than PH Equity.

You may be best not to read the reply I am about to post to Superlightr though!

doh but the PH equity has improved a bit ! Ying and Yang.

Can't touch it for 5 years anyway.

superlightr said:

just wanted to say that yes the PH Equity has dropped but its still way higher then November.

as has most funds. Hoping they will bounce back over the next week/month/year/5 years.

Just to highlight the funds in the Index 20 has increased which was a silver lining.

That is a very pragmatic way of viewing things.as has most funds. Hoping they will bounce back over the next week/month/year/5 years.

Just to highlight the funds in the Index 20 has increased which was a silver lining.

When you log in today you will see PH Equity wass up nearly 1% on the day yesterday (0.86%).

Lindsell Train was down 1.96% on the day.

Fundsmith was down 2.17% on the day.

That's a 3% performance gap between PH Equity and Fundsmith in one day!

Quick question if I may!

I am considering dropping a few £k in over coming weeks.....but with the market looking a bit 'jittery', my preference would be to filter it in across a few tranches.

Are there any noticeable differences in costs between (for example) popping 10K in as one lump sum, or £2k a week over 5 weeks (or indeed £1k a day for 10 days!)?

I imagine there would be some dealing costs, but since that is wrapped up in the 0.67% cost for PHequity, perhaps no there is zero difference in costs to me?

(& yes, I do appreciate that the reality is that for around 65% of the time, I would always be better off lobbing it all in....but the markets are at an interesting point right now, I feel!)

I am considering dropping a few £k in over coming weeks.....but with the market looking a bit 'jittery', my preference would be to filter it in across a few tranches.

Are there any noticeable differences in costs between (for example) popping 10K in as one lump sum, or £2k a week over 5 weeks (or indeed £1k a day for 10 days!)?

I imagine there would be some dealing costs, but since that is wrapped up in the 0.67% cost for PHequity, perhaps no there is zero difference in costs to me?

(& yes, I do appreciate that the reality is that for around 65% of the time, I would always be better off lobbing it all in....but the markets are at an interesting point right now, I feel!)

JulianPH said:

Bam89 said:

Happy New Year to all at IM!

I made a resolution to sort myself out financially this year, and have taken advantage of the quiet time off work this week to read through the first six months of this thread, after seeing it crop up on the forums throughout 2019. Despite working in finance throughout my career, I feel rather incompetent when it comes to the personal investment side of things

I don't want to waste anyone's time, so was hoping Julian / Nik / anyone else who understands this stuff a lot better than I do may be able to advise whether I'm barking up the wrong tree with my understanding of how IM may be able to help me, current situation is as follows after tracking down all the paperwork!

- 30 years old, currently a "self employed" contractor in finance roles with my own limited company

- I have 3 workplace pensions from full time employment, all quite small due to my stupidity in not maxing out employer contributions in my younger years, the combined total is around £15k

- I have a pot of cash in a cash ISA with tiny returns which is earmarked for my wedding at the end of this year, another smaller chunk which is the start of savings for a house deposit in the next year or two, and savings of a few months outgoings which is to cover any time I have between contracts

I think I am right in saying that IM would be able to help me combine the three pensions into a SIPP, but what I am not sure of is whether I would be able to do this as a standalone product? I would look to make regular pension contributions from my limited company directly into this, but not quite sure of the process (might be a question for my accountant rather than here!)

If I am not able to set up a SIPP as a standalone product, I would be willing to invest a small amount and then make regular deposits into a S&S type of arrangement, but would likely be more cautious with the risk profile with this than the pension

My fiancee is in a similar situation with multiple workplace pensions, so potentially would look to set her up on a very similar basis in future if at all possible

Feel like I'm rambling on without getting to the point, so to summarise my questions are

- Can I set up a standalone SIPP with IM, combining my 3 existing workplace pensions then make regular contributions from my limited company

- If I can't set up as a standalone, is a small investment into a S&S arrangement enough to qualify as a private client and then be able to set up the SIPP

- Will it be possible to have my fiancee join in a few months time as a completely separate client

Thanks in advance

HI Bam89I made a resolution to sort myself out financially this year, and have taken advantage of the quiet time off work this week to read through the first six months of this thread, after seeing it crop up on the forums throughout 2019. Despite working in finance throughout my career, I feel rather incompetent when it comes to the personal investment side of things

I don't want to waste anyone's time, so was hoping Julian / Nik / anyone else who understands this stuff a lot better than I do may be able to advise whether I'm barking up the wrong tree with my understanding of how IM may be able to help me, current situation is as follows after tracking down all the paperwork!

- 30 years old, currently a "self employed" contractor in finance roles with my own limited company

- I have 3 workplace pensions from full time employment, all quite small due to my stupidity in not maxing out employer contributions in my younger years, the combined total is around £15k

- I have a pot of cash in a cash ISA with tiny returns which is earmarked for my wedding at the end of this year, another smaller chunk which is the start of savings for a house deposit in the next year or two, and savings of a few months outgoings which is to cover any time I have between contracts

I think I am right in saying that IM would be able to help me combine the three pensions into a SIPP, but what I am not sure of is whether I would be able to do this as a standalone product? I would look to make regular pension contributions from my limited company directly into this, but not quite sure of the process (might be a question for my accountant rather than here!)

If I am not able to set up a SIPP as a standalone product, I would be willing to invest a small amount and then make regular deposits into a S&S type of arrangement, but would likely be more cautious with the risk profile with this than the pension

My fiancee is in a similar situation with multiple workplace pensions, so potentially would look to set her up on a very similar basis in future if at all possible

Feel like I'm rambling on without getting to the point, so to summarise my questions are

- Can I set up a standalone SIPP with IM, combining my 3 existing workplace pensions then make regular contributions from my limited company

- If I can't set up as a standalone, is a small investment into a S&S arrangement enough to qualify as a private client and then be able to set up the SIPP

- Will it be possible to have my fiancee join in a few months time as a completely separate client

Thanks in advance

Happy New Year to you too!

First the important things. At 30 you are still very definitely in your "younger years" (I'm just clinging on to my 40's!!!) and even more importantly - congratulations to you and your fiancée on your wedding later this year!

Now the boring things! Yes, you can do everything you are looking at doing.

- You can consolidate your previous workplace pensions with us on a stand alone basis and make regular or ad hoc contributions as you see fit.

- Nik would be your Private Client Manager and therefore be available whenever you like, to assist you with maximising you tax efficiency and financial planning in all such matters (and any others).

- You can also use us for ISA management, but there is no requirement to do so in order to use us for pension/SIPP management.

- Your fiancée can join as a separate client whenever she wants.

Just remember to use the code PH2607 in the "Additional Notes" box when you (and your wife to be) put in your personal details. This removes both the initial charge and the £100k minimum.

If you would like to chat anything through please contact Nik at nik.burrows@intelligentmoney.com or PM me.

Cheers

Julian

I'm quite happy to just leave the Aviva one as it is for now.

But I want to do something with my old Equitable Life one which I took out in 1983 - and ran when I was self-employed until all the trouble circa 1998 - and since when has laid dormant again. Being a lazy SoB I paid scant attention to it over the years but knew the pot was creeping up slowly. Now EL have sold the with-profits policies to Utmost Life & Pensions and there's been a huge uplift in the fund's value. I want to take advantage of this and take out the 25% tax-free part of the new figure - lots of things to do with it house/garden/family/car wise etc - and am aware I have to have some kind of financial product with the rest, I can't leave it with Utmost.

Do I sound like the kind of situation you can assist with? Again, not looking for HUGE risk - aim to retire in 10 years or so more or less - aged 57 now. Have had recent discussions with an annuity company but the returns look pretty dire (albeit 100% safe)*

Any help appreciated ...

-

Unless Trump or his North Korean mate push the Red Button

mikeiow said:

Quick question if I may!

I am considering dropping a few £k in over coming weeks.....but with the market looking a bit 'jittery', my preference would be to filter it in across a few tranches.

Are there any noticeable differences in costs between (for example) popping 10K in as one lump sum, or £2k a week over 5 weeks (or indeed £1k a day for 10 days!)?

I imagine there would be some dealing costs, but since that is wrapped up in the 0.67% cost for PHequity, perhaps no there is zero difference in costs to me?

(& yes, I do appreciate that the reality is that for around 65% of the time, I would always be better off lobbing it all in....but the markets are at an interesting point right now, I feel!)

Hi MikeI am considering dropping a few £k in over coming weeks.....but with the market looking a bit 'jittery', my preference would be to filter it in across a few tranches.

Are there any noticeable differences in costs between (for example) popping 10K in as one lump sum, or £2k a week over 5 weeks (or indeed £1k a day for 10 days!)?

I imagine there would be some dealing costs, but since that is wrapped up in the 0.67% cost for PHequity, perhaps no there is zero difference in costs to me?

(& yes, I do appreciate that the reality is that for around 65% of the time, I would always be better off lobbing it all in....but the markets are at an interesting point right now, I feel!)

Zero difference in costs for you which ever way you do it, as we absorb the dealing costs ourselves within the 0.67% fee, rather than pass these onto our clients.

Of course this means it costs us more in dealing costs!

Gassing Station | Finance | Top of Page | What's New | My Stuff