Intelligent Money - your investment questions answered

Discussion

SSG1000 said:

Hi Julian, could I get some more info on the new portfolios that you are launching, please?

Thanks

SSG

Hi SSGThanks

SSG

Good timing as they went live yesterday (but won't be available to clients for another week as we update our website and Key Features documents.

They are also going to be available through our GIA next week too (IM Optimum to follow).

In a nutshell they are a series of purely passive trackers that use the established model of ranging from 100% equities reducing by 20% bonds until you reach 20% equity/80% bonds (so the same as Vanguard LifeStrategy in this respect).

However, unlike LS, I have built these to not carry UK domestic bias with the equities (but instead represent the world proportionately) and all bond exposure is UK Index Linked Gilts.

This would have delivered superior investment returns in the past (highlighted in the table below) and I believe will continue to do this in the future.

It is worth noting however that they do not have the human element of active asset allocation as with IM Optimum.

The charges are a fully inclusive 0.57% a year (which drops to 0.52% after £500k and 0.47% after £1m - I wanted to get these costs lower but it was not economic at the offset) and this includes a pension (with SIPP commercial property functionality), the cost of income drawdown and your own Private Client Manager.

| 1 Year Return | 3 Year Return | 5 Year Return | |

| IM Index 100 | 9.6% | 48.06% | 81.78% |

| Vanguard LS 100 | 7.39% | 42.68% | 71.94% |

| 1 Year Return | 3 Year Return | 5 Year Return | |

| IM Index 80 | 9.31% | 41.32% | 75.62% |

| Vanguard LS 80 | 7.12% | 34.73% | 61.29% |

| 1 Year Return | 3 Year Return | 5 Year Return | |

| IM Index 60 | 9.02% | 34.77% | 69.48% |

| Vanguard LS 60 | 6.84% | 27.09% | 50.74% |

| 1 Year Return | 3 Year Return | 5 Year Return | |

| IM Index 40 | 8.73% | 28.32% | 63.36% |

| Vanguard LS 40 | 6.6% | 19.66% | 40.35% |

| 1 Year Return | 3 Year Return | 5 Year Return | |

| IM Index 20 | 8.44% | 22.06% | 57.24% |

| Vanguard LS 20 | 6.51% | 13.05% | 30.79% |

All figures are based up to 30th June 2019 and please remember that with the Vanguard figures you have to also take away the charges of your platform of choice (and financial adviser fees, where relevant). The IM Index figures are after all charges, have no platform (or advice) fees to be added and as mentioned above include a pension/SIPP and a named Private Client Manager (i.e. the full Private Client service).

In a few weeks time we will also be launching PH Equity.

This is my core "buy and hold" portfolio of 10 global brands. I constructed this portfolio after much research in 2008 as I wanted a portfolio that would do well in the falling market conditions at the time. Over the next 11 years it has thrashed the likes of Lindsell Train and Fundsmith and never had a negative calendar year. It has also done this with much lower volatility than the S&P 500 index (which is where the stocks sit).

I'll post more on this shortly.

Cheers

Julian

Julian, looks like a great alternative to the likes of VLS, and being more global than VLS sits well with my gut feelings - I'm in - just need to decide weightings!. Also looking forward to having 10% (or thereabouts) of PH Equity within my ISA - as a long-term buy and hold these will have a place within my investment/s. As per telephone conversation yesterday - once the app goes live I will transfer my daughters CTF to the IM JISA - thinking probably in a mix of something like 35% Optimum Global Growth, 25% IM Index 100, 25% IM Index 80, and the remainder 15% in PH Equity. Once I get a feel for the way the new app works I will transfer my SIPP and possibly the other ISAs we spoke about.

eta - had a sneak preview of the new app/site yesterday and I think everyone is going to be very happy. Selecting and choosing all IM funds (including weightings) from our phones/tablets/computers etc, without having to do it with someone over the phone is going to make investing with IM an absolute doddle - even more so than it is now. I think when it's officially live you should put some screenshots on the forum Julian

eta - had a sneak preview of the new app/site yesterday and I think everyone is going to be very happy. Selecting and choosing all IM funds (including weightings) from our phones/tablets/computers etc, without having to do it with someone over the phone is going to make investing with IM an absolute doddle - even more so than it is now. I think when it's officially live you should put some screenshots on the forum Julian

Edited by Phooey on Saturday 31st August 19:26

JulianPH said:

rufusgti said:

Hi

As per my thread on investing 1000 pound each for the kids.

https://www.pistonheads.com/gassing/topic.asp?h=0&...

Is there any products that Intelligent Money can offer that would suit me.

Looking to invest for circa 15 years my children are 5 and 7. I can add approximately 200-300 each year, plus birthday money etc.

Many thanks

Hi thereAs per my thread on investing 1000 pound each for the kids.

https://www.pistonheads.com/gassing/topic.asp?h=0&...

Is there any products that Intelligent Money can offer that would suit me.

Looking to invest for circa 15 years my children are 5 and 7. I can add approximately 200-300 each year, plus birthday money etc.

Many thanks

A Junior ISA seems to be a logical starting point and also (once you have set it up) has the ability for grandparents and the like to make contributions.

It takes 5 to 10 minutes (max) to set up online here:

https://www.intelligentmoney.com/private-clients/

Click the apply button top right.

I do this for my daughter using IM Optimum Global Growth. You are free, of course, to select which ever portfolio you like and if you are not sure you can pick a target dated portfolio (whereby the risk/reward level is managed down the closer it gets to your children accessing the money).

Remember to put the code PH2607 into the 'Additional notes box on the personal details page to remove the initial charge. There is also no minimum investment criteria for the Junior ISA.

Please let me know if I can be of any further help.

Cheers

Julian

When will I get the log in details, it's asking for a client ref which was not in the email.

Cheers

Phooey said:

Julian, looks like a great alternative to the likes of VLS, and being more global than VLS sits well with my gut feelings - I'm in - just need to decide weightings!. Also looking forward to having 10% (or thereabouts) of PH Equity within my ISA - as a long-term buy and hold these will have a place within my investment/s. As per telephone conversation yesterday - once the app goes live I will transfer my daughters CTF to the IM JISA - thinking probably in a mix of something like 35% Optimum Global Growth, 25% IM Index 100, 25% IM Index 80, and the remainder 15% in PH Equity. Once I get a feel for the way the new app works I will transfer my SIPP and possibly the other ISAs we spoke about.

eta - had a sneak preview of the new app/site yesterday and I think everyone is going to be very happy. Selecting and choosing all IM funds (including weightings) from our phones/tablets/computers etc, without having to do it with someone over the phone is going to make investing with IM an absolute doddle - even more so than it is now. I think when it's officially live you should put some screenshots on the forum Julian

Hi mate, thanks for the very positive feedback!eta - had a sneak preview of the new app/site yesterday and I think everyone is going to be very happy. Selecting and choosing all IM funds (including weightings) from our phones/tablets/computers etc, without having to do it with someone over the phone is going to make investing with IM an absolute doddle - even more so than it is now. I think when it's officially live you should put some screenshots on the forum Julian

Edited by Phooey on Saturday 31st August 19:26

I think the new app/site is much more logical and simpler to use, so I was very pleased with your response when I gave you a sneak preview.

I can also see the sense in your investment selection for your daughter given the time frames involved.

Good idea about posting some screen shots, I'll do so when it goes live in the week.

Cheers

Julian

rufusgti said:

Thanks for your help with this. I have just set up the first junior ISA for my son through the site and sent the funds. All very straight forward.

When will I get the log in details, it's asking for a client ref which was not in the email.

Cheers

Absolutely no problem and I'm glad you found the process straight forward.When will I get the log in details, it's asking for a client ref which was not in the email.

Cheers

Welcome as an IM Private Client. Nik will get in touch with your to give you his contact details and will be available to you whenever you need any assistance with anything related to your finances (not just IM).

It is entirely up to you as to how you want to utilise his services. For some people, having a qualified and experienced financial profession available to them to go over all areas of their financial planning (without having to pay any advice fees) is a core driver in becoming a Private Client. For others, they are just happy to know he is always there if needed.

It has been a long time since I set up my IM account, but IIRC the client reference is generated when you submit the application. If you PM me with your name and postcode I will have someone find yours and Nik can send it to you tomorrow when he introduces himself.

Alternatively, just email Nik directly at nik.burrows@intelligentmoney.com

Cheers

Julian

Julian/Nik,

Hello, hope you are both well. I've been reading the thread and its my time for a question.

Bit of background:

I'm 49, hoping to retire at 55. Need about £2.5k per month for a nice retirement.

No mortgage/debts.

We were opted out of serps (i think that is the correct way to say it), so I'll only get the standard old age pension.

My company closed their DB scheme this year and are desperate to get people out of it. In view of this they are offering 20% extra on top of my pot to get out.

Just had my ETV offer and its £675k.

I'd like to use the 25% tax free allowance to help my kids as they need it. So maybe take out 20% at 55. Leaving to option of another 5% at a later date if needed.

Does this sound feasible?

Also which of your products do you think would suit me?

Kind regards.

Dave.

Hello, hope you are both well. I've been reading the thread and its my time for a question.

Bit of background:

I'm 49, hoping to retire at 55. Need about £2.5k per month for a nice retirement.

No mortgage/debts.

We were opted out of serps (i think that is the correct way to say it), so I'll only get the standard old age pension.

My company closed their DB scheme this year and are desperate to get people out of it. In view of this they are offering 20% extra on top of my pot to get out.

Just had my ETV offer and its £675k.

I'd like to use the 25% tax free allowance to help my kids as they need it. So maybe take out 20% at 55. Leaving to option of another 5% at a later date if needed.

Does this sound feasible?

Also which of your products do you think would suit me?

Kind regards.

Dave.

Edited by DaveV6 on Monday 2nd September 15:06

Edited by DaveV6 on Monday 2nd September 15:13

DaveV6 said:

Julian/Nik,

Hello, hope you are both well. I've been reading the thread and its my time for a question.

Bit of background:

I'm 49, hoping to retire at 55. Need about £2.5k per month for a nice retirement.

No mortgage/debts.

We were opted out of serps (i think that is the correct way to say it), so I'll only get the standard old age pension.

My company closed their DB scheme this year and are desperate to get people out of it. In view of this they are offering 20% extra on top of my pot to get out.

Just had my ETV offer and its £675k.

I'd like to use the 25% tax free allowance to help my kids as they need it. So maybe take out 20% at 55. Leaving to option of another 5% at a later date if needed.

Does this sound feasible?

Also which of your products do you think would suit me?

Kind regards.

Dave.

Hi Dave, I am still alive (thank you!) and Nik is as annoyingly as he ever was!Hello, hope you are both well. I've been reading the thread and its my time for a question.

Bit of background:

I'm 49, hoping to retire at 55. Need about £2.5k per month for a nice retirement.

No mortgage/debts.

We were opted out of serps (i think that is the correct way to say it), so I'll only get the standard old age pension.

My company closed their DB scheme this year and are desperate to get people out of it. In view of this they are offering 20% extra on top of my pot to get out.

Just had my ETV offer and its £675k.

I'd like to use the 25% tax free allowance to help my kids as they need it. So maybe take out 20% at 55. Leaving to option of another 5% at a later date if needed.

Does this sound feasible?

Also which of your products do you think would suit me?

Kind regards.

Dave.

Edited by DaveV6 on Monday 2nd September 15:06

Edited by DaveV6 on Monday 2nd September 15:13

You are very close in terms of income drawdown, but you have to seriously consider what you may be giving up.

If you use your tax free allowance right now this will set you back (obviously).

There are many options open to you though. Have a chat with Nik, he really does know what he is talking about).

I couldn't possibly tell you which of our portfolios best suited you. I could explain the differences between them though.

Just post here (or send me a PM).

Cheers

Julian

Julian,

Thank you for the response.

When you say I need to think about what I'm giving up. If that relates to the DB pension, I will get £26k a year without any lump sum (or £19k a year and £126k), but I'd need to work till I'm 65 to get that.

As I said the company wants people out of the scheme, probably to make it look good, sell it on and remove themselves from any liability.

So I think it is the right thing to get out, 10 years is a long time.

I'll give Nik a ring next week (I work shifts and start tomorrow), and discuss it with him.

All the best.

Dave.

Thank you for the response.

When you say I need to think about what I'm giving up. If that relates to the DB pension, I will get £26k a year without any lump sum (or £19k a year and £126k), but I'd need to work till I'm 65 to get that.

As I said the company wants people out of the scheme, probably to make it look good, sell it on and remove themselves from any liability.

So I think it is the right thing to get out, 10 years is a long time.

I'll give Nik a ring next week (I work shifts and start tomorrow), and discuss it with him.

All the best.

Dave.

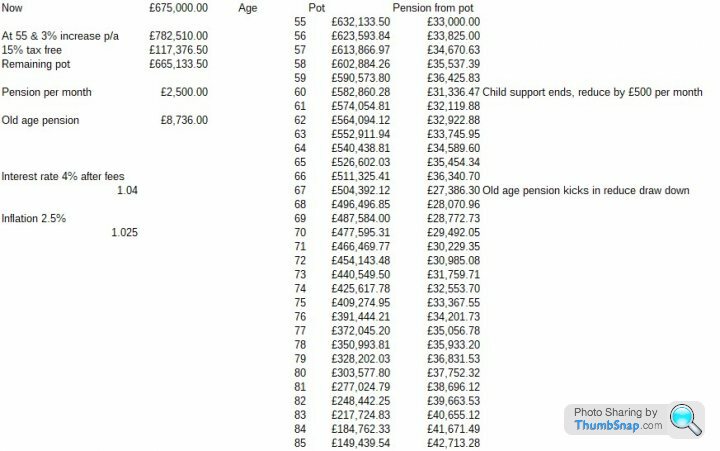

Just to try and understand my options I've created a very simple spreadsheet. Helps to play around to see what effect taking tax free at the start and other things.

Of course I'm trying to predict the future, which is never a good idea. Worst case I lose it all, but I've got a tent and family with land

Right, time for a cup of tea and a cigarette (hence spreadsheet only goes to age 85).

Of course I'm trying to predict the future, which is never a good idea. Worst case I lose it all, but I've got a tent and family with land

Right, time for a cup of tea and a cigarette (hence spreadsheet only goes to age 85).

DaveV6 said:

Julian,

Thank you for the response.

When you say I need to think about what I'm giving up. If that relates to the DB pension, I will get £26k a year without any lump sum (or £19k a year and £126k), but I'd need to work till I'm 65 to get that.

As I said the company wants people out of the scheme, probably to make it look good, sell it on and remove themselves from any liability.

So I think it is the right thing to get out, 10 years is a long time.

I'll give Nik a ring next week (I work shifts and start tomorrow), and discuss it with him.

All the best.

Dave.

Hi Dave, yes, that was what I was referring to. It is not just the benefits though, it is the guarantees and the fact the investment risk sits with them and not you.Thank you for the response.

When you say I need to think about what I'm giving up. If that relates to the DB pension, I will get £26k a year without any lump sum (or £19k a year and £126k), but I'd need to work till I'm 65 to get that.

As I said the company wants people out of the scheme, probably to make it look good, sell it on and remove themselves from any liability.

So I think it is the right thing to get out, 10 years is a long time.

I'll give Nik a ring next week (I work shifts and start tomorrow), and discuss it with him.

All the best.

Dave.

Of course the flip side is that you have far greater flexibility and control, can select your own level of tax free cash and your own level of income drawdown (as you have illustrated!).

You also have the benefit of leaving your fund to your partner and children free of IHT.

DaveV6 said:

Just to try and understand my options I've created a very simple spreadsheet. Helps to play around to see what effect taking tax free at the start and other things.

Of course I'm trying to predict the future, which is never a good idea. Worst case I lose it all, but I've got a tent and family with land

Right, time for a cup of tea and a cigarette (hence spreadsheet only goes to age 85).

I think you have been pessimistic in average annual growth of 4% over the next 30 years, but there is nothing wrong with that! Of course I'm trying to predict the future, which is never a good idea. Worst case I lose it all, but I've got a tent and family with land

Right, time for a cup of tea and a cigarette (hence spreadsheet only goes to age 85).

I'm also not sure (as I can't see the calculations) how you have arrived at the figures.

Please feel free to send me a PM so I can go over your calculations as, for example, £675,000 growing at a 3% compound annual would be worth £907,143 rather than £782,510.

Edited to add the blindingly obvious fact you have 6 years until you are 55, not 10, so please ignore my last point!

Cheers

Julian

Edited by JulianPH on Tuesday 3rd September 12:24

nicklaus1988 said:

Hi all

Have both my SIPP and ISA in Fidelity, waiting for ISA transfer to happen.

Do people have the same investments in both their SIPPs and ISA or a different strategy for both?

Also do you adjust your deposits for inflation on an annual basis or more often than that?

Thank you

Hi nicklaus1988Have both my SIPP and ISA in Fidelity, waiting for ISA transfer to happen.

Do people have the same investments in both their SIPPs and ISA or a different strategy for both?

Also do you adjust your deposits for inflation on an annual basis or more often than that?

Thank you

A very interesting question!

If you are using these tax wrappers for the same purpose (retirement income) then it makes sense for the investments held within them to be the same.

But if you are using them for different purposes then the investments held within them may benefit from being different.

For example, you might have a shorter time frame for an ISA holding than for your pension. You should therefore be considering moving to a lower risk/reward strategy with these investments.

Conversely, many people see their pension as a bedrock foundation and want to reduce volatility on the investments held within this, but will take a greater level of rick/reward with their ISA investments.

There is no right or wrong answer here. It is all about personal preference and sleeping easily each night.

I am unclear on your final point (it is probably just the semantics) but we rebalance every 3 months. If this is not the answer you were seeking please just give me a shout and I'll try to do better next time!

If I can give a better answer to any point raised then please let me know and I will be more than happy to expand on the above.

cbehagg242 said:

Taken the plunge and initiated the transfer of an old pension to IM following the sound advice from Julian on my recent SIPP post.

Look forward to see how things pan out and will potentially move my HL SIPP into this at a later date.

Welcome as a Private Client Craig! Look forward to see how things pan out and will potentially move my HL SIPP into this at a later date.

Nik is now at your disposal for any financial matters.

Please feel free to give me a shout whenever you like though.

We won't pester you, we take the view that you know where we are and will get in touch with when you need us, not the other way round (other than reminders you have asked us to give you).

Cheers

Julian

JulianPH said:

Welcome as a Private Client Craig!

Nik is now at your disposal for any financial matters.

Please feel free to give me a shout whenever you like though.

We won't pester you, we take the view that you know where we are and will get in touch with when you need us, not the other way round (other than reminders you have asked us to give you).

Cheers

Julian

Cheers Julian, works for me!Nik is now at your disposal for any financial matters.

Please feel free to give me a shout whenever you like though.

We won't pester you, we take the view that you know where we are and will get in touch with when you need us, not the other way round (other than reminders you have asked us to give you).

Cheers

Julian

JulianPH said:

I am unclear on your final point (it is probably just the semantics) but we rebalance every 3 months. If this is not the answer you were seeking please just give me a shout and I'll try to do better next time!

If I can give a better answer to any point raised then please let me know and I will be more than happy to expand on the above.

Thanks Julian. If I can give a better answer to any point raised then please let me know and I will be more than happy to expand on the above.

For example drip feeding £1000 per month into SIPP and inflation is 2%, would you only increase the deposit amount on annual basis to keep the monthly deposit the same?

Does this make sense?

nicklaus1988 said:

Thanks Julian.

For example drip feeding £1000 per month into SIPP and inflation is 2%, would you only increase the deposit amount on annual basis to keep the monthly deposit the same?

Does this make sense?

Hi nicklaus1988,For example drip feeding £1000 per month into SIPP and inflation is 2%, would you only increase the deposit amount on annual basis to keep the monthly deposit the same?

Does this make sense?

We wouldn't increase it at all. This would be up to you.

There is no minimum (for PHers) and you can increase/decrease/start/stop as suits you.

If you would like us to increase your contributions automatically then we can do this, but it is always your call.

Cheers

Hi guys

Was quite amazed when I found investments forum on pistonheads, I thought this place was for wasting money!

Anyway, to cut a long story short the wife and I have up to £150k to do something with.... Any ideas

Mortgage is paid and have no debts or dependents. Her pension is pretty healthy, mine less so, but after a good friend with a huge pension pot passed away early it made me reconsider putting everything away for much later in life (rightly or wrongly).

Thanks in advance for your thoughts!

Was quite amazed when I found investments forum on pistonheads, I thought this place was for wasting money!

Anyway, to cut a long story short the wife and I have up to £150k to do something with.... Any ideas

Mortgage is paid and have no debts or dependents. Her pension is pretty healthy, mine less so, but after a good friend with a huge pension pot passed away early it made me reconsider putting everything away for much later in life (rightly or wrongly).

Thanks in advance for your thoughts!

ddpunter said:

Hi guys

Was quite amazed when I found investments forum on pistonheads, I thought this place was for wasting money!

Anyway, to cut a long story short the wife and I have up to £150k to do something with.... Any ideas

Mortgage is paid and have no debts or dependents. Her pension is pretty healthy, mine less so, but after a good friend with a huge pension pot passed away early it made me reconsider putting everything away for much later in life (rightly or wrongly).

Thanks in advance for your thoughts!

Hi there!Was quite amazed when I found investments forum on pistonheads, I thought this place was for wasting money!

Anyway, to cut a long story short the wife and I have up to £150k to do something with.... Any ideas

Mortgage is paid and have no debts or dependents. Her pension is pretty healthy, mine less so, but after a good friend with a huge pension pot passed away early it made me reconsider putting everything away for much later in life (rightly or wrongly).

Thanks in advance for your thoughts!

Over the years I have never ceased to be amazed that there is always a thread and/or very knowledgeable people on PH who can cover virtually every subject under the sun!

You have already covered my first suggestions by saying you have no mortgage or debts.

Pensions and ISAs may be a good move forward. Your age and tax bracket will influence what is the right mixture between the two.

Pensions and ISAs are just tax allowances (or "wrappers"). It is the investments that you hold within them that are the important thing.

If you have income taxed at the higher rate then putting the equivalent of this into a pension is very tax efficient. There are also rules that enable you to use any available contributions still available from the previous 3 years (providing you had any sort of pension running for those tax years).

The downside is you can't access this money until you are 55 (increasing to 57 by 2028).

You mention a fried who passed away early with a large pension fund, so it is worth me pointing out that if you die before age 75 your wife can receive your entire pension fund tax free (with death from 75 onwards she will still be able to receive your pension fund, but simply have to pay income tax on any money she takes out of it).

Assuming your wife is in a Defined Contribution scheme (also called Money Purchase scheme) the same applies to you with her pension.

So your friends pension investments would certainly not have been lost.

When it comes to ISAs these are simpler. You can both put up to £20,000 a year into your ISA and all growth and income is tax free. You are also not tied in until a particular age and can take your money out (or make tax free income withdrawals) whenever you like.

Finally, any money you want to invest that you can't get into a pension/ISA straight away (due to the contribution limits) can be held in a General Investment Account.

This is just a way of saying "outside of the two tax wrappers", whereby you still benefit from your tax free annual divided allowance and tax free capital gains tax allowance.

So the ability to be highly tax effective with with lump sum is very achievable.

The next question you need to ask yourself is how you want to invest the money. If you want to manage it yourself and pick and monitor your own investments there are plenty of platforms that enable you to do this.

If you want it managed for you that is something we are happy to do and, ironically, this can often be cheaper than managing it all yourself!

Another advantage of using IM is that you get a named Private Client Manager (Nik, in your case as a PHer) who is a qualified and experienced financial professional who is on hand whenever you need to go over any aspect of your financial position and planning -without you having to pay financial adviser fees.

So I would start off by dropping Nik an email (nik.burrows@intelligentmoney.com) and arranging a time to have a chat over the phone and possibly a face to face meeting (if you would prefer this).

He will be able to go over all of your options in plain English and leave you very informed. There is no charge and certainly no obligation to use us (as many people here will testify, Nik will point you in another direction if he thinks that is better for you - but the decision as to what to do always remains with you).

I hope that has been helpful and not too long winded!

Cheers

Julian

Afternoon all.

I have been reading this thread for a bit and have decided I'd like advice. From Julian and IM if I'm honest.

I'm 52 (nearly) I have a final salary pension which is deferred and two smaller private pensions plus a final salary pension I am paying into at the moment.

It now seems to me that the 3 pensions which are not being paid into could be doing better for me in regards to growth.

If I don't move house in the next 2 years, I would like to try and stop working at 55, I have some numbers in my head which would convince me to do it.

Can someone PM me or can you let me know who to contact to discuss the whole thing.

I have been reading this thread for a bit and have decided I'd like advice. From Julian and IM if I'm honest.

I'm 52 (nearly) I have a final salary pension which is deferred and two smaller private pensions plus a final salary pension I am paying into at the moment.

It now seems to me that the 3 pensions which are not being paid into could be doing better for me in regards to growth.

If I don't move house in the next 2 years, I would like to try and stop working at 55, I have some numbers in my head which would convince me to do it.

Can someone PM me or can you let me know who to contact to discuss the whole thing.

Gassing Station | Finance | Top of Page | What's New | My Stuff