2 more 'Bond' companies to exercise caution with

Discussion

Following on from the London Capital & Finance disaster I thought it might be useful to highlight the following companies. I will not cast judgement but will provide some facts:

https://minervabondoptions.co.uk

https://www.renewable-bonds.com

I'm not suggesting either of these companies are doing anything illegal or fraudulent, just highlighting that they are very young and offering ridiculous levels of returns.

What could possibly go wrong...

https://minervabondoptions.co.uk

- The company is offering "Secure Investment" in "Asset Back" bonds paying up to 13.9%

- It is completely unregulated by the FCA and has no FSCS protection

- The company is 3 years old and changed its name from HXL Solutions to Minerva Development Group 10 months ago

- It has changed its registered address 4 times since October

- All 7 original directors have resigned and both current directors were appointed on 27 June last year

https://www.renewable-bonds.com

- More "fully asset backed" bonds, this time ethical to boot.

- Returns of up to 12% per annum

- Company incorporated 2 years ago as AMIO WEALTH LIMITED

- Last accounts show £249,970 of current liabilities and a whopping £561 of total equity, including £100 of share capital

- No recourse to the FOS or FSCS

I'm not suggesting either of these companies are doing anything illegal or fraudulent, just highlighting that they are very young and offering ridiculous levels of returns.

What could possibly go wrong...

Ginge R said:

For clarity, there can be redress via FSCS or FOS, even for an unregulated investment if the investment was part of regulated advice. You claim, not via/for the product, but for the advice.

Isn’t IPM Ltd the test case for this? This is due to the Secured Energy Bond minibonds default back in 2015 and it’s only now that the FCA has stated that investors can make a claim. But it is too early to know what any payouts from the FSCS will be. There is also the minefield of ‘advice’ itself and what a consumer may have assumed was actual ‘advice’ in a regulatory manner was not.

The key is that the process is not yet complete. All that is happening at the moment is the official handover of the consumer complaints from the FOS to the FSCS as IPM has now failed and no longer exists. https://www.fscs.org.uk/what-we-cover/investments/...

It is also very important to understand the grounds under which the Ombudsman upheld the two complaints against IPM and what those complaints were.

In short, IPM were on the Board of SEB. That is a huge difference and in reality the Ombudsman is very unlikely to have upheld any complaint if that hadn’t been the case. Which in turn would mean the complaint would have been extremely unlikely to end up at the FSCS.

It is a very, very different scenario to have a regulated advisor effectively representing a minibonds and being its sales agent and facilitator as opposed to a regulated advisor operating at arms length to a minibonds and giving appropriate professional advice after suitable KYC and due diligence on the bond. In the case of the latter it would be inconceivable that there would be any kind of plausible complaint or claim.

I don’t think that it has yet been shown that you can claim for advice but there may well be other minibonds cases that say otherwise?

DonkeyApple said:

Isn’t IPM Ltd the test case for this? This is due to the Secured Energy Bond minibonds default back in 2015 and it’s only now that the FCA has stated that investors can make a claim. But it is too early to know what any payouts from the FSCS will be.

There is also the minefield of ‘advice’ itself and what a consumer may have assumed was actual ‘advice’ in a regulatory manner was not.

The key is that the process is not yet complete. All that is happening at the moment is the official handover of the consumer complaints from the FOS to the FSCS as IPM has now failed and no longer exists. https://www.fscs.org.uk/what-we-cover/investments/...

It is also very important to understand the grounds under which the Ombudsman upheld the two complaints against IPM and what those complaints were.

In short, IPM were on the Board of SEB. That is a huge difference and in reality the Ombudsman is very unlikely to have upheld any complaint if that hadn’t been the case. Which in turn would mean the complaint would have been extremely unlikely to end up at the FSCS.

It is a very, very different scenario to have a regulated advisor effectively representing a minibonds and being its sales agent and facilitator as opposed to a regulated advisor operating at arms length to a minibonds and giving appropriate professional advice after suitable KYC and due diligence on the bond. In the case of the latter it would be inconceivable that there would be any kind of plausible complaint or claim.

I don’t think that it has yet been shown that you can claim for advice but there may well be other minibonds cases that say otherwise?

FSCS will allow a claim for negligent advice. There’s lots I could add, but won’t. The outgoing chief exec of FSCS made some very interesting comments this afternoon. COMP 4.2 refers.There is also the minefield of ‘advice’ itself and what a consumer may have assumed was actual ‘advice’ in a regulatory manner was not.

The key is that the process is not yet complete. All that is happening at the moment is the official handover of the consumer complaints from the FOS to the FSCS as IPM has now failed and no longer exists. https://www.fscs.org.uk/what-we-cover/investments/...

It is also very important to understand the grounds under which the Ombudsman upheld the two complaints against IPM and what those complaints were.

In short, IPM were on the Board of SEB. That is a huge difference and in reality the Ombudsman is very unlikely to have upheld any complaint if that hadn’t been the case. Which in turn would mean the complaint would have been extremely unlikely to end up at the FSCS.

It is a very, very different scenario to have a regulated advisor effectively representing a minibonds and being its sales agent and facilitator as opposed to a regulated advisor operating at arms length to a minibonds and giving appropriate professional advice after suitable KYC and due diligence on the bond. In the case of the latter it would be inconceivable that there would be any kind of plausible complaint or claim.

I don’t think that it has yet been shown that you can claim for advice but there may well be other minibonds cases that say otherwise?

https://www.handbook.fca.org.uk/handbook/COMP/4/2....

Since even this, matters have evolved.

Edited by Ginge R on Wednesday 13th March 21:57

Ginge R said:

FSCS will allow a claim for negligent advice. There’s lots I could add, but won’t. The outgoing chief exec of FSCS made some very interesting comments this afternoon. COMP 4.2 refers.

https://www.handbook.fca.org.uk/handbook/COMP/4/2....

As an aside, and you mention mini bonds, the case of Strand Capital saw the fund managers using client money to invest in their parent company. Again, and I have to ask, where on Earth was the oversight from the SIPP companies which should have been acting as a trustee/gatekeeper? There’s a fascinating Smith and Williamson update from June 2018 out there somewhere.

Since even this, matters have evolved.

I wouldn't add any more, if I were you.https://www.handbook.fca.org.uk/handbook/COMP/4/2....

As an aside, and you mention mini bonds, the case of Strand Capital saw the fund managers using client money to invest in their parent company. Again, and I have to ask, where on Earth was the oversight from the SIPP companies which should have been acting as a trustee/gatekeeper? There’s a fascinating Smith and Williamson update from June 2018 out there somewhere.

Since even this, matters have evolved.

COMP 4 completely proves you are incorrect and backs up DonkeyApple's statement.

Your PDF attachment clearly states Principle 6 (and I quote directly from it):

"SIPP operators are not responsible for the SIPP advice given by third parties such as financial advisers."

You are, basically, arguing against what you quote.

Ginge R said:

FSCS will allow a claim for negligent advice. There’s lots I could add, but won’t. The outgoing chief exec of FSCS made some very interesting comments this afternoon. COMP 4.2 refers.

https://www.handbook.fca.org.uk/handbook/COMP/4/2....

Since even this, matters have evolved.

You seem to be trying to conflate the roles of advisor and administrator, which you obviously can’t. They are two distinct regulatory roles. Not that it is pertinent to your original post re using negligent advice to make a complaint to the ombudsman. Which raises another aspect that the FSCS only comes into play if the advisor ceases to trade, so not immediately or necessarily relevant. Nor are SIPPs necessarily relevant as obviously most minibonds are held outside of tax wrappers. https://www.handbook.fca.org.uk/handbook/COMP/4/2....

Since even this, matters have evolved.

Edited by Ginge R on Wednesday 13th March 21:57

The fundamental issue that surrounds minibonds is that they carry equity style risk of complete capital loss in exchange for bond level returns. As a product they are fundamentally mispriced as a core principle.

They are high risk, speculative products. But that doesn’t mean that an advisor cannot legitimately advise on them. Outside of fraud, you would only have a case against an advisor if their advice did not reflect appropriately both the client’s appetite for risk, suitability and the product’s risk.

As usual, old chum, you are absolutely correct. SIPP operators are not responsible for the advice. Never have been. Never will be.

Although the advisers are responsible for the investment advice given, a SIPP operator has a clear responsibility for the quality of the *business* it administers, and the facilitation of the Investments. Just because a SIPP operator *can* offer an unsuitable investment that might decimate a person’s retirement, there is no regulation that says it should or must. The Regulator is quite specific in this regard.

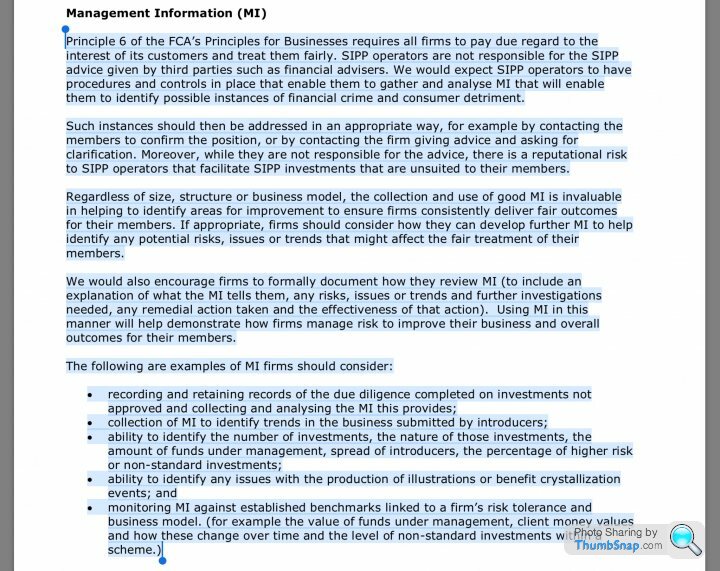

That image that I posted offers examples of how a SIPP operator can use MI to manage risk. Those SIPP operators who didn’t manage risk, who may have allowed the same old rogue advisers to use their facility to facilitate bad investments time and time again will probably be sweating in light of Carey.

Although the advisers are responsible for the investment advice given, a SIPP operator has a clear responsibility for the quality of the *business* it administers, and the facilitation of the Investments. Just because a SIPP operator *can* offer an unsuitable investment that might decimate a person’s retirement, there is no regulation that says it should or must. The Regulator is quite specific in this regard.

That image that I posted offers examples of how a SIPP operator can use MI to manage risk. Those SIPP operators who didn’t manage risk, who may have allowed the same old rogue advisers to use their facility to facilitate bad investments time and time again will probably be sweating in light of Carey.

JulianPH said:

I wouldn't add any more, if I were you.

COMP 4 completely proves you are incorrect and backs up DonkeyApple's statement.

Your PDF attachment clearly states Principle 6 (and I quote directly from it):

"SIPP operators are not responsible for the SIPP advice given by third parties such as financial advisers."

You are, basically, arguing against what you quote.

COMP 4 completely proves you are incorrect and backs up DonkeyApple's statement.

Your PDF attachment clearly states Principle 6 (and I quote directly from it):

"SIPP operators are not responsible for the SIPP advice given by third parties such as financial advisers."

You are, basically, arguing against what you quote.

I don’t think I am conflating them. If that’s how it comes across, I’ve explained it badly, but I am constrained. Greyfriars P6 is a recent, prime example of minibonds being held within a SIPP.

The issue isn’t so much one of the minibond. If someone wants that type of product, then fine. As you imply, the issue is one of provision and facilitation of the said minibond to the wrong type of investor. This is an example (a recent one) of FOS making a determination against an firm selling Greyfriars into a SIPP.

https://citywire.co.uk/new-model-adviser/news/advi...

The issue isn’t so much one of the minibond. If someone wants that type of product, then fine. As you imply, the issue is one of provision and facilitation of the said minibond to the wrong type of investor. This is an example (a recent one) of FOS making a determination against an firm selling Greyfriars into a SIPP.

https://citywire.co.uk/new-model-adviser/news/advi...

DonkeyApple said:

You seem to be trying to conflate the roles of advisor and administrator, which you obviously can’t. They are two distinct regulatory roles. Not that it is pertinent to your original post re using negligent advice to make a complaint to the ombudsman. Which raises another aspect that the FSCS only comes into play if the advisor ceases to trade, so not immediately or necessarily relevant. Nor are SIPPs necessarily relevant as obviously most minibonds are held outside of tax wrappers.

The fundamental issue that surrounds minibonds is that they carry equity style risk of complete capital loss in exchange for bond level returns. As a product they are fundamentally mispriced as a core principle.

They are high risk, speculative products. But that doesn’t mean that an advisor cannot legitimately advise on them. Outside of fraud, you would only have a case against an advisor if their advice did not reflect appropriately both the client’s appetite for risk, suitability and the product’s risk.

The fundamental issue that surrounds minibonds is that they carry equity style risk of complete capital loss in exchange for bond level returns. As a product they are fundamentally mispriced as a core principle.

They are high risk, speculative products. But that doesn’t mean that an advisor cannot legitimately advise on them. Outside of fraud, you would only have a case against an advisor if their advice did not reflect appropriately both the client’s appetite for risk, suitability and the product’s risk.

Ginge R said:

I don’t think I am conflating them. If that’s how it comes across, I’ve explained it badly, but I am constrained. Greyfriars P6 is a recent, prime example of minibonds being held within a SIPP.

The issue isn’t so much one of the minibond. If someone wants that type of product, then fine. As you imply, the issue is one of provision and facilitation of the said minibond to the wrong type of investor. This is an example (a recent one) of FOS making a determination against an firm selling Greyfriars into a SIPP.

https://citywire.co.uk/new-model-adviser/news/advi...

But that link completely backs up the point that I was making and is at odds with the tangent that you had speared off on? Negligent or unsuitable advice has recourse to the ombudsman. If the adviser ceases to trade then an application to the FSCS can be made. The issue isn’t so much one of the minibond. If someone wants that type of product, then fine. As you imply, the issue is one of provision and facilitation of the said minibond to the wrong type of investor. This is an example (a recent one) of FOS making a determination against an firm selling Greyfriars into a SIPP.

https://citywire.co.uk/new-model-adviser/news/advi...

DonkeyApple said:

You seem to be trying to conflate the roles of advisor and administrator, which you obviously can’t. They are two distinct regulatory roles. Not that it is pertinent to your original post re using negligent advice to make a complaint to the ombudsman. Which raises another aspect that the FSCS only comes into play if the advisor ceases to trade, so not immediately or necessarily relevant. Nor are SIPPs necessarily relevant as obviously most minibonds are held outside of tax wrappers.

The fundamental issue that surrounds minibonds is that they carry equity style risk of complete capital loss in exchange for bond level returns. As a product they are fundamentally mispriced as a core principle.

They are high risk, speculative products. But that doesn’t mean that an advisor cannot legitimately advise on them. Outside of fraud, you would only have a case against an advisor if their advice did not reflect appropriately both the client’s appetite for risk, suitability and the product’s risk.

The fundamental issue that surrounds minibonds is that they carry equity style risk of complete capital loss in exchange for bond level returns. As a product they are fundamentally mispriced as a core principle.

They are high risk, speculative products. But that doesn’t mean that an advisor cannot legitimately advise on them. Outside of fraud, you would only have a case against an advisor if their advice did not reflect appropriately both the client’s appetite for risk, suitability and the product’s risk.

I don’t wish to be rude but you appear fixated on trying to deviate the subject of the thread to something that has tenuous correlation.

I think we all agree that if an advisor issues erroneous, negligent or unsuitable advice then the consumer has recourse to the ombudsman. But that categorically does not mean per se the same as if an advised investment product or instrument enters into default. A product defaulting is not sufficient grounds alone to uphold a complaint. Even if the default is as a result of fraud or mismanagement of the instrument. The advice, due diligence and or suitability checks of the advisor may well have been 100% appropriate. You have to remember the importance of the ‘small test’ for want of a better term within the function of an advisors due diligence.

Attempting to bring this back to minibonds, it is extremely pertinent to any complaint to the ombudsman that these instruments are manifestly and overtly not covered by the FSCS and categorised as non vanilla from a tax wrapper perspective. Is non-mainstream the specific industry terminology?

You need to read my opening post again. It was in response to Julian’s assertion that there was “No recourse to the FOS or FSCS”. That is factually incorrect and I just wanted to set the record straight for anyone who may have been lead astray by that.

There *is* redress available, and it’s via the delivery of the advice, not the investment into the product. If the advice was good, then clearly the issue of compensation is irrelevant. I wasn’t commenting on your subsequent points, in fact, I stated that I wouldn’t be. I wasn’t commenting either way on the matter of default. And I won’t be.

This is my post.

<<For clarity, there can be redress via FSCS or FOS, even for an unregulated investment if the investment was part of regulated advice. You claim, not via/for the product, but for the advice.>>

As an aside, mini bonds are mostly, currently, accessed via the SIPP wrapper. I think your final point might be covered by the vernacular ‘NSI’, or Non Standard Investments. The issue of pertinence is, as you say, a highly relevant one, but not so in the context of this thread (certainly it’s not an issue I’m contending either way).

In July 2014, the Regulator wrote to CEO reminding them of their responsibilities to the matter of NSI research and due diligence. Crucially, it also slipped in the point on the final page of the letter of the follow up about those aspects also relating to so called ‘Standard’ investments.

There *is* redress available, and it’s via the delivery of the advice, not the investment into the product. If the advice was good, then clearly the issue of compensation is irrelevant. I wasn’t commenting on your subsequent points, in fact, I stated that I wouldn’t be. I wasn’t commenting either way on the matter of default. And I won’t be.

This is my post.

<<For clarity, there can be redress via FSCS or FOS, even for an unregulated investment if the investment was part of regulated advice. You claim, not via/for the product, but for the advice.>>

As an aside, mini bonds are mostly, currently, accessed via the SIPP wrapper. I think your final point might be covered by the vernacular ‘NSI’, or Non Standard Investments. The issue of pertinence is, as you say, a highly relevant one, but not so in the context of this thread (certainly it’s not an issue I’m contending either way).

In July 2014, the Regulator wrote to CEO reminding them of their responsibilities to the matter of NSI research and due diligence. Crucially, it also slipped in the point on the final page of the letter of the follow up about those aspects also relating to so called ‘Standard’ investments.

Ginge R said:

You need to read my opening post again. It was in response to Julian’s assertion that there was “No recourse to the FOS or FSCS”. That is factually incorrect and I just wanted to set the record straight for anyone who may have been lead astray by that.

There *is* redress available, and it’s via the delivery of the advice, not the investment into the product. If the advice was good, then clearly the issue of compensation is irrelevant. I wasn’t commenting on your subsequent points, in fact, I stated that I wouldn’t be. I wasn’t commenting either way on the matter of default. And I won’t be.

This is my post.

<<For clarity, there can be redress via FSCS or FOS, even for an unregulated investment if the investment was part of regulated advice. You claim, not via/for the product, but for the advice.>>

Well, no, the original post is not factually incorrect. Your post is a supplementary observation that in the event that a regulated FCA adviser sold investment advice in regards to the minibond investment the investor may approach the ombudsman if they feel there is a case against the adviser on the grounds of either a failure of due diligence on the product or a failure of suitability on the client, typically.There *is* redress available, and it’s via the delivery of the advice, not the investment into the product. If the advice was good, then clearly the issue of compensation is irrelevant. I wasn’t commenting on your subsequent points, in fact, I stated that I wouldn’t be. I wasn’t commenting either way on the matter of default. And I won’t be.

This is my post.

<<For clarity, there can be redress via FSCS or FOS, even for an unregulated investment if the investment was part of regulated advice. You claim, not via/for the product, but for the advice.>>

This is something that we all will agree with. To all of us as market professionals it is an obvious supplementary aspect. In this instance here instead of it being treated as the supplemental observation that is it is appears instead to be being used as some form of weapon of attack or points scoring. As was the strange tangent that looked to wrap administrators into the same role as advisers. Personally, I feel this to be disingenuous and don't think it is conducive to a thread that could, over time, be useful for fellow investors.

Ginge R said:

As an aside, mini bonds are mostly, currently, accessed via the SIPP wrapper. I think your final point might be covered by the vernacular ‘NSI’, or Non Standard Investments. The issue of pertinence is, as you say, a highly relevant one, but not so in the context of this thread (certainly it’s not an issue I’m contending either way).

In July 2014, the Regulator wrote to CEO reminding them of their responsibilities to the matter of NSI research and due diligence. Crucially, it also slipped in the point on the final page of the letter of the follow up about those aspects also relating to so called ‘Standard’ investments.

This again is attempting to conflate the roles of administrator and adviser. The concept of 'Due diligence' arguably actually has different guidance and interpretation between the two roles. And what you are talking about above is specifically related to 'advice' which is not the role of an administrator.In July 2014, the Regulator wrote to CEO reminding them of their responsibilities to the matter of NSI research and due diligence. Crucially, it also slipped in the point on the final page of the letter of the follow up about those aspects also relating to so called ‘Standard’ investments.

Donkey Apple,

Once more, and at the risk of sounding like a broken record, it’s you who is introducing the distinction between the roles of advice/administrator. I never mentioned the role of fund manager and/or scheme administrator, when referring to FSCS/FOS. My first post refers. After that, you launched into a post which assumed I had conflated the two in the matter of compensation. I hadn’t. I even said I wasn’t being drawn into it.

Me: “For clarity, there can be redress via FSCS or FOS, even for an unregulated investment if the investment was part of regulated advice. You claim, not via/for the product, but for the advice.”

Me: “FSCS will allow a claim for negligent advice.”

I never mentioned the role of the Scheme administrator in the compensation process. You did. I didn’t even comment on IPM, and won’t, but even went so far as to mention a FOS case involving an, erm, adviser. I shan’t even comment on your thoughts about the distinction between the two levels of due diligence responsibilities.

Where I have made more general reference to the role of the administrator in determining its role, there is guidance in place for its obligations and responsibilities. In many instances, we see use or abuse of the so called Agent as Client protocol, but that again, is a completely different matter. I think Carey will be a game changer though. At least, I hope it will.

Once more, and at the risk of sounding like a broken record, it’s you who is introducing the distinction between the roles of advice/administrator. I never mentioned the role of fund manager and/or scheme administrator, when referring to FSCS/FOS. My first post refers. After that, you launched into a post which assumed I had conflated the two in the matter of compensation. I hadn’t. I even said I wasn’t being drawn into it.

Me: “For clarity, there can be redress via FSCS or FOS, even for an unregulated investment if the investment was part of regulated advice. You claim, not via/for the product, but for the advice.”

Me: “FSCS will allow a claim for negligent advice.”

I never mentioned the role of the Scheme administrator in the compensation process. You did. I didn’t even comment on IPM, and won’t, but even went so far as to mention a FOS case involving an, erm, adviser. I shan’t even comment on your thoughts about the distinction between the two levels of due diligence responsibilities.

Where I have made more general reference to the role of the administrator in determining its role, there is guidance in place for its obligations and responsibilities. In many instances, we see use or abuse of the so called Agent as Client protocol, but that again, is a completely different matter. I think Carey will be a game changer though. At least, I hope it will.

Ginge R said:

As usual, old chum, you are absolutely correct. SIPP operators are not responsible for the advice. Never have been. Never will be.

Although the advisers are responsible for the investment advice given, a SIPP operator has a clear responsibility for the quality of the *business* it administers, and the facilitation of the Investments. Just because a SIPP operator *can* offer an unsuitable investment that might decimate a person’s retirement, there is no regulation that says it should or must. The Regulator is quite specific in this regard.

That image that I posted offers examples of how a SIPP operator can use MI to manage risk. Those SIPP operators who didn’t manage risk, who may have allowed the same old rogue advisers to use their facility to facilitate bad investments time and time again will probably be sweating in light of Carey.

You are confused. SIPP operators to not 'offer' the investments you are referring to. Advisers (and clients) select them from third party providers.Although the advisers are responsible for the investment advice given, a SIPP operator has a clear responsibility for the quality of the *business* it administers, and the facilitation of the Investments. Just because a SIPP operator *can* offer an unsuitable investment that might decimate a person’s retirement, there is no regulation that says it should or must. The Regulator is quite specific in this regard.

That image that I posted offers examples of how a SIPP operator can use MI to manage risk. Those SIPP operators who didn’t manage risk, who may have allowed the same old rogue advisers to use their facility to facilitate bad investments time and time again will probably be sweating in light of Carey.

JulianPH said:

I wouldn't add any more, if I were you.

COMP 4 completely proves you are incorrect and backs up DonkeyApple's statement.

Your PDF attachment clearly states Principle 6 (and I quote directly from it):

"SIPP operators are not responsible for the SIPP advice given by third parties such as financial advisers."

You are, basically, arguing against what you quote.

COMP 4 completely proves you are incorrect and backs up DonkeyApple's statement.

Your PDF attachment clearly states Principle 6 (and I quote directly from it):

"SIPP operators are not responsible for the SIPP advice given by third parties such as financial advisers."

You are, basically, arguing against what you quote.

I cannot speak for any other SIPP providers, but we are certainly not sweating in light of Carey as unlike them (and many others) we only work with regulated advisers and allow investments into standard assets via regulated investment managers.

Carey and the like were working with unregulated introducers recommending unregulated investments. There is a world of difference.

We establish that the FCA has authorised every firm we deal with and granted them the permissions to carry out the regulated activities they do - and even then we restrict them to standard assets only.

This covers our responsibility to ensure all available investments are suitable for a pension. It is however, as you correctly state, the regulated adviser's responsibility to ensure they are suitable for their clients, not us as provider.

JulianPH said:

You are confused. SIPP operators to not 'offer' the investments you are referring to. Advisers (and clients) select them from third party providers.

I cannot speak for any other SIPP providers, but we are certainly not sweating in light of Carey as unlike them (and many others) we only work with regulated advisers and allow investments into standard assets via regulated investment managers.

Carey and the like were working with unregulated introducers recommending unregulated investments. There is a world of difference.

We establish that the FCA has authorised every firm we deal with and granted them the permissions to carry out the regulated activities they do - and even then we restrict them to standard assets only.

This covers our responsibility to ensure all available investments are suitable for a pension. It is however, as you correctly state, the regulated adviser's responsibility to ensure they are suitable for their clients, not us as provider.

I concede, ‘offer’ was not the best choice of word, but my meaning was more reflective. You use the word ‘provider’ - we have to be careful. Maybe facilitator would be more accurate. I cannot speak for any other SIPP providers, but we are certainly not sweating in light of Carey as unlike them (and many others) we only work with regulated advisers and allow investments into standard assets via regulated investment managers.

Carey and the like were working with unregulated introducers recommending unregulated investments. There is a world of difference.

We establish that the FCA has authorised every firm we deal with and granted them the permissions to carry out the regulated activities they do - and even then we restrict them to standard assets only.

This covers our responsibility to ensure all available investments are suitable for a pension. It is however, as you correctly state, the regulated adviser's responsibility to ensure they are suitable for their clients, not us as provider.

I wasn’t suggesting at all that you would be sweating, Julian, far from it. But, seeing as you make the point, how would you guys conduct and retain research and due diligence on something such as Greyfriars Portfolio 6 which contained such gems as car parking space investments. Surely, if an adviser approached you and wanted to transfer a bunch of clients out of a DB Scheme in a short space of time and from a tightly defined geographical area, how do you manage to manage risk, by judicial use of MI? We all knew Greyfriars was a crock long before it went under, as we suspected the same of Strand. I’m sure you’d draw the conclusion in your DD that it fails the sniff test, and Standard or not, Car Parking spaces and Green recycling facilities are manifestly unsuitable for nearly everyone, let alone a clutch of workers from, for instance, a couple of square miles. I’m genuinely interested in your answer. The FCA is clear about responsibility - just because some of those ‘bad’ SIPP operators *can* do something, it doesn’t mean that they must or should, right?

Gassing Station | Finance | Top of Page | What's New | My Stuff